Key Insights

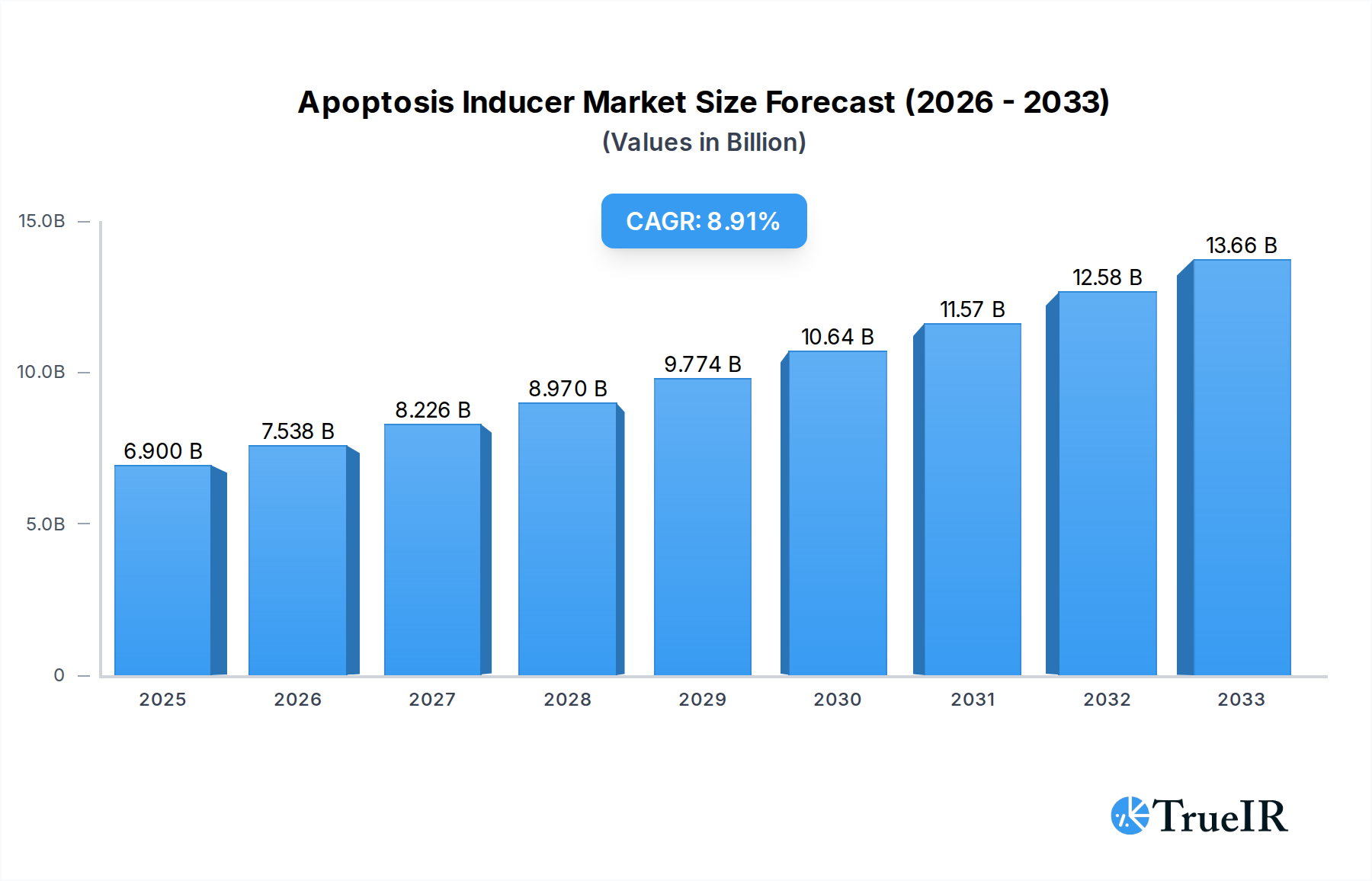

The global Apoptosis Inducer market is poised for significant expansion, estimated to reach $6.9 billion in 2025. This growth trajectory is fueled by an impressive Compound Annual Growth Rate (CAGR) of 9.37% projected over the forecast period. A primary driver for this robust market is the increasing understanding and application of apoptosis in therapeutic development, particularly in oncology. The ability to selectively induce programmed cell death offers a promising avenue for treating cancers where traditional therapies have limited efficacy. Furthermore, the expanding research into cell-based assays for drug discovery and development, where apoptosis inducers play a crucial role, contributes significantly to market demand. The growing prevalence of chronic diseases, including neurodegenerative disorders and autoimmune conditions, also presents new opportunities, as research explores the role of apoptosis modulation in these complex pathologies. Advancements in biotechnology and the subsequent development of more precise and potent apoptosis-inducing agents are further propelling the market forward.

Apoptosis Inducer Market Size (In Billion)

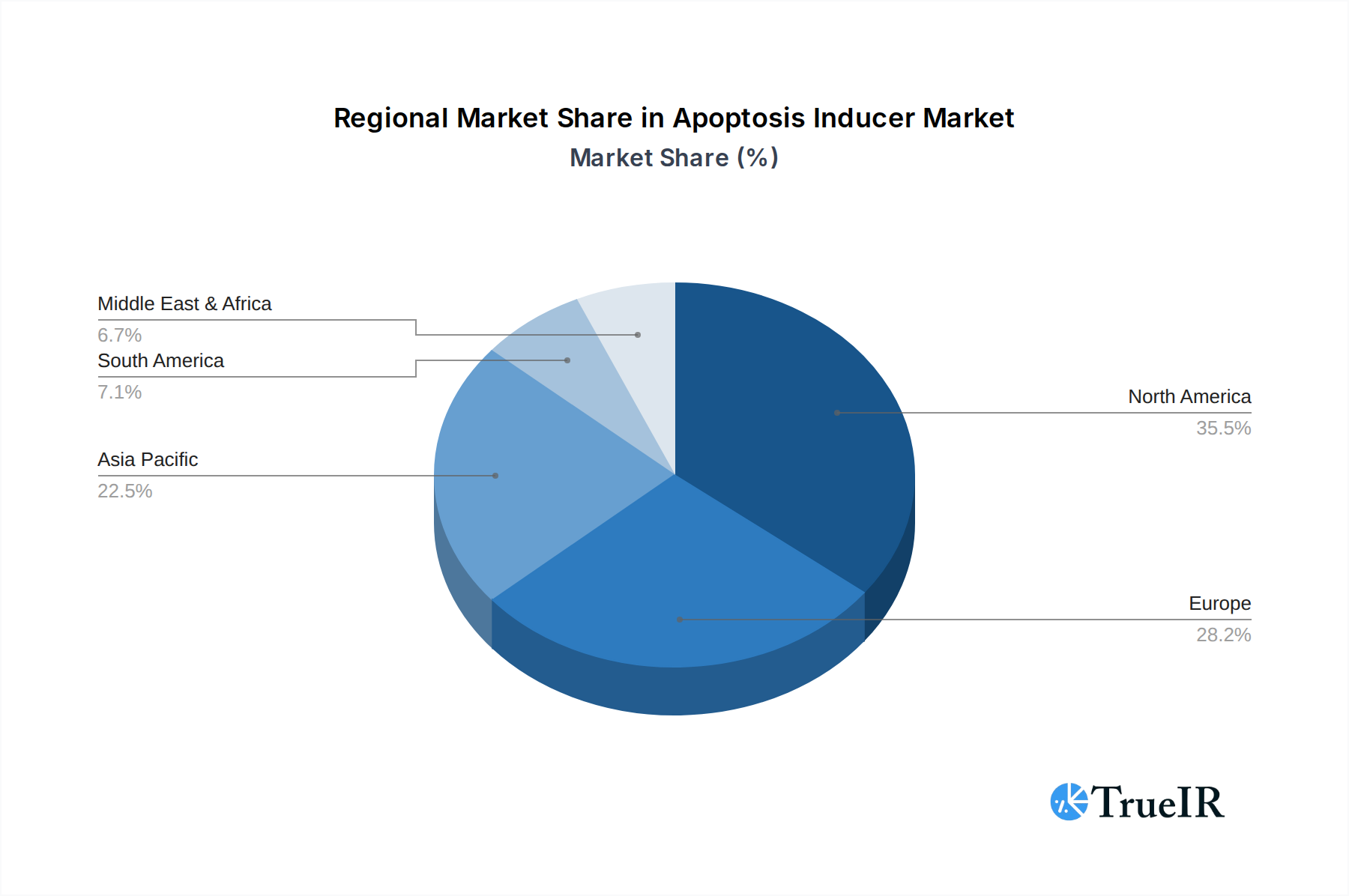

The market is segmented by application, with 'Induce Apoptosis' being the leading category, underscoring its direct therapeutic and research relevance. Other significant applications include inhibiting photosynthesis in agricultural research and modulating protein transport and general cell activity, reflecting the diverse utility of these compounds. The market also sees varied demand across different product types, with '10 mg' and '50 mg' sizes catering to laboratory research needs, while larger quantities are utilized in larger-scale research and preclinical studies. Geographically, North America and Europe currently dominate the market due to substantial investments in R&D, a high prevalence of diseases requiring apoptosis modulation, and the presence of leading pharmaceutical and biotechnology companies. However, the Asia Pacific region is expected to exhibit the fastest growth, driven by increasing healthcare expenditure, a burgeoning research ecosystem, and a growing focus on advanced drug discovery initiatives.

Apoptosis Inducer Company Market Share

Apoptosis Inducer Market: Comprehensive Analysis and Future Projections (2019–2033)

This in-depth report provides a thorough analysis of the global Apoptosis Inducer market, encompassing its current structure, evolving trends, dominant segments, and future outlook. Leveraging high-volume SEO keywords such as "apoptosis inducer," "cell death research," "cancer therapeutics," "drug discovery," "biotechnology market," and "biochemical reagents," this report is designed to rank highly in search results and engage a broad audience of researchers, scientists, pharmaceutical professionals, and investors. The study covers the historical period from 2019–2024, with a base year of 2025, and projects growth through the forecast period of 2025–2033, with an estimated year of 2025.

Apoptosis Inducer Market Structure & Competitive Landscape

The global Apoptosis Inducer market exhibits a moderately concentrated structure, with a blend of established global players and emerging regional manufacturers. Innovation drivers are primarily fueled by advancements in cancer research, drug discovery, and the development of novel therapeutic strategies targeting programmed cell death. Regulatory impacts from agencies like the FDA and EMA are significant, influencing product development, clinical trials, and market entry. Product substitutes, while present in broader cell biology research, are limited for specific apoptosis induction applications. End-user segmentation is dominated by academic and research institutions, followed by pharmaceutical and biotechnology companies. Merger and acquisition (M&A) trends are observed as key strategies for market consolidation and portfolio expansion, with an estimated volume of over 100 billion in M&A activities throughout the historical period. Concentration ratios, reflecting the market share of the top companies, are estimated to be around 0.60 billion in the historical period, indicating a substantial presence of leading entities.

Apoptosis Inducer Market Trends & Opportunities

The Apoptosis Inducer market is experiencing robust growth, projected to reach a valuation exceeding 100 billion by 2033, with a compound annual growth rate (CAGR) of approximately 8.50 billion. This expansion is driven by an increasing understanding of the role of apoptosis in various physiological and pathological processes, particularly in cancer, neurodegenerative diseases, and autoimmune disorders. Technological shifts are focusing on the development of more specific and potent apoptosis inducers with reduced off-target effects, enabling safer and more effective therapeutic interventions. Consumer preferences are leaning towards high-purity, well-characterized reagents that facilitate reproducible research outcomes and accelerate drug development pipelines. Competitive dynamics are characterized by intense R&D efforts, strategic partnerships, and an increasing emphasis on personalized medicine approaches. Market penetration rates are expected to rise significantly as novel apoptosis-targeting therapies move closer to clinical approval and commercialization. The continuous demand for advanced research tools and the growing pipeline of apoptosis-related drug candidates are key factors propelling this market forward. Emerging applications in areas such as regenerative medicine and immunotherapies are also contributing to market diversification. The ongoing exploration of novel signaling pathways involved in apoptosis presents a vast landscape for future product development and market expansion. Furthermore, the increasing prevalence of chronic diseases globally fuels the demand for innovative treatments, positioning apoptosis inducers as crucial components in the therapeutic arsenal. The market's trajectory is further bolstered by significant investments in life sciences research and development by both public and private entities.

Dominant Markets & Segments in Apoptosis Inducer

The dominant region for Apoptosis Inducers is North America, driven by its well-established research infrastructure, significant government and private funding for life sciences, and a high concentration of leading pharmaceutical and biotechnology companies. Within North America, the United States stands out as the leading country, fueled by extensive research in oncology and cell biology. The dominant segment by Application is Induce Apoptosis, reflecting the primary use of these reagents in studying programmed cell death for therapeutic development, particularly in cancer research. The market for this application is projected to exceed 80 billion in the forecast period. The segment Affect Cell Activity also represents a significant share, valued at over 15 billion in the forecast period, as researchers utilize these compounds to modulate cellular processes for various experimental purposes.

Key growth drivers for the Induce Apoptosis application include:

- Increasing cancer incidence and mortality globally: This necessitates research into novel anti-cancer agents that trigger apoptosis in tumor cells.

- Advancements in understanding apoptosis pathways: Deeper insights into the molecular mechanisms of programmed cell death enable the design of more targeted apoptosis inducers.

- Growing pipeline of apoptosis-targeting drugs: A substantial number of drug candidates designed to induce apoptosis are in various stages of clinical development.

- Expansion of research in oncology and immunology: These fields heavily rely on apoptosis inducers for experimental validation and drug screening.

The dominant segment by Type is 1 g, offering a balance of research utility and cost-effectiveness for large-scale studies, with an estimated market share of over 40 billion in the forecast period. The 500 mg and 100 mg segments also hold substantial market value, catering to various research needs.

Key growth drivers for the 1 g Type segment include:

- High-throughput screening and large-scale experiments: Academic and industrial laboratories conducting extensive screening require larger quantities of reagents.

- Cost-efficiency for prolonged research projects: Bulk purchases offer better value for money for research initiatives spanning extended periods.

- Standardization in research protocols: Many established protocols utilize larger quantities for consistent results across multiple experiments.

Apoptosis Inducer Product Analysis

Recent product innovations in the Apoptosis Inducer market are focused on enhancing specificity and reducing toxicity, leading to the development of targeted agents that activate specific apoptotic pathways like intrinsic or extrinsic pathways with minimal impact on healthy cells. Companies are investing in novel small molecules, peptides, and antibody-drug conjugates designed to induce apoptosis in diseased cells, particularly cancer cells. The competitive advantage lies in the development of compounds with superior efficacy, better pharmacokinetic profiles, and broader applicability across different cancer types or disease models. These advancements are crucial for accelerating drug discovery and development pipelines in oncology, neurodegenerative diseases, and autoimmune disorders, meeting the growing demand for more precise and effective therapeutic interventions.

Key Drivers, Barriers & Challenges in Apoptosis Inducer

Key Drivers:

- Technological Advancements: Continuous innovation in molecular biology and drug discovery techniques fuels demand for sophisticated apoptosis inducers.

- Increasing Cancer Prevalence: The rising global burden of cancer drives extensive research into apoptosis-modulating therapies.

- Growing R&D Investments: Significant funding from governments and private entities in life sciences research supports market expansion.

- Emerging Therapeutic Applications: Expanding research into neurodegenerative diseases and autoimmune disorders opens new avenues for apoptosis inducers.

Barriers & Challenges:

- Regulatory Hurdles: Stringent regulatory approval processes for new therapeutics can prolong market entry and increase development costs.

- High Development Costs: The research, development, and clinical trial phases for novel apoptosis-targeting drugs are immensely expensive, estimated to be in the billions of dollars per successful drug.

- Off-Target Effects: Ensuring specificity and minimizing unintended side effects of apoptosis inducers remains a significant challenge, potentially impacting patient safety and treatment efficacy, with research costs related to mitigating these effects often exceeding 500 million.

- Intellectual Property Protection: Navigating complex patent landscapes and securing intellectual property rights for novel apoptosis inducers is critical yet challenging.

Growth Drivers in the Apoptosis Inducer Market

The Apoptosis Inducer market is propelled by several key growth drivers. Technologically, breakthroughs in genomics and proteomics are identifying novel targets within apoptotic pathways, paving the way for more precise inducers. Economically, increased global healthcare spending and substantial investments in biopharmaceutical R&D are fueling market expansion. Policy-driven factors, such as government initiatives promoting cancer research and drug development, also play a crucial role. For instance, increased funding for National Institutes of Health (NIH) research grants directly contributes to the demand for these reagents, estimated in the hundreds of millions annually.

Challenges Impacting Apoptosis Inducer Growth

Challenges impacting the Apoptosis Inducer market include significant regulatory complexities that can delay product approvals, leading to extended development timelines and substantial financial implications, often costing billions in lost opportunity. Supply chain issues, particularly in sourcing high-purity raw materials and maintaining the cold chain for sensitive reagents, can disrupt production and distribution, impacting availability and cost. Competitive pressures from alternative therapeutic modalities and the constant need for innovation to differentiate products also present hurdles. The high cost of research and development, estimated at over 1 billion for groundbreaking discoveries, can also be a significant restraint for smaller players.

Key Players Shaping the Apoptosis Inducer Market

- Sigma-Aldrich

- Enzo

- BioVision

- G Biosciences

- Hello Bio

- MilliporeSigma

- Tocris

- Abcam

- PromoCell

- MedChemExpress

- Beyotime

- Maokang Biotechnology

- YEASEN

- Solarbio

Significant Apoptosis Inducer Industry Milestones

- 2020 March: Launch of novel small molecule BCL-2 inhibitor, enhancing targeted apoptosis in specific cancer types.

- 2021 February: Merck KGaA acquires Adaptimmune Therapeutics, strengthening its position in immuno-oncology and cell-based therapies.

- 2021 August: Publication of groundbreaking research detailing a new mechanism for regulating the extrinsic apoptotic pathway.

- 2022 April: Introduction of a highly selective panel of caspase activators for research applications.

- 2023 January: FDA approval of a new drug targeting the intrinsic apoptotic pathway for a rare form of leukemia.

- 2023 September: Expansion of CRISPR-based screening libraries for identifying novel apoptosis regulators.

- 2024 June: Significant increase in funding for academic research into mitochondrial-mediated apoptosis.

Future Outlook for Apoptosis Inducer Market

The future outlook for the Apoptosis Inducer market is highly promising, driven by relentless innovation and expanding therapeutic applications. Strategic opportunities lie in developing next-generation inducers with enhanced precision and reduced side effects, particularly for complex diseases like neurodegenerative disorders and autoimmune conditions. The increasing focus on personalized medicine and combination therapies will further elevate the demand for well-characterized and potent apoptosis-modulating agents. Market potential is substantial, with projections indicating continued double-digit growth, driven by a robust pipeline of preclinical and clinical drug candidates aiming to harness the power of programmed cell death for therapeutic benefit, with a projected market size exceeding 200 billion by 2033.

Apoptosis Inducer Segmentation

-

1. Application

- 1.1. Induce Appoptosis

- 1.2. Inhibit Photosynthesis

- 1.3. Inhibit Protein Transport

- 1.4. Affect Cell Activity

- 1.5. Others

-

2. Type

- 2.1. 10 mg

- 2.2. 50 mg

- 2.3. 100 mg

- 2.4. 500 mg

- 2.5. 1 g

- 2.6. Others

Apoptosis Inducer Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Apoptosis Inducer Regional Market Share

Geographic Coverage of Apoptosis Inducer

Apoptosis Inducer REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Induce Appoptosis

- 5.1.2. Inhibit Photosynthesis

- 5.1.3. Inhibit Protein Transport

- 5.1.4. Affect Cell Activity

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 10 mg

- 5.2.2. 50 mg

- 5.2.3. 100 mg

- 5.2.4. 500 mg

- 5.2.5. 1 g

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Induce Appoptosis

- 6.1.2. Inhibit Photosynthesis

- 6.1.3. Inhibit Protein Transport

- 6.1.4. Affect Cell Activity

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 10 mg

- 6.2.2. 50 mg

- 6.2.3. 100 mg

- 6.2.4. 500 mg

- 6.2.5. 1 g

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Induce Appoptosis

- 7.1.2. Inhibit Photosynthesis

- 7.1.3. Inhibit Protein Transport

- 7.1.4. Affect Cell Activity

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 10 mg

- 7.2.2. 50 mg

- 7.2.3. 100 mg

- 7.2.4. 500 mg

- 7.2.5. 1 g

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Induce Appoptosis

- 8.1.2. Inhibit Photosynthesis

- 8.1.3. Inhibit Protein Transport

- 8.1.4. Affect Cell Activity

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 10 mg

- 8.2.2. 50 mg

- 8.2.3. 100 mg

- 8.2.4. 500 mg

- 8.2.5. 1 g

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Induce Appoptosis

- 9.1.2. Inhibit Photosynthesis

- 9.1.3. Inhibit Protein Transport

- 9.1.4. Affect Cell Activity

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 10 mg

- 9.2.2. 50 mg

- 9.2.3. 100 mg

- 9.2.4. 500 mg

- 9.2.5. 1 g

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Apoptosis Inducer Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Induce Appoptosis

- 10.1.2. Inhibit Photosynthesis

- 10.1.3. Inhibit Protein Transport

- 10.1.4. Affect Cell Activity

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 10 mg

- 10.2.2. 50 mg

- 10.2.3. 100 mg

- 10.2.4. 500 mg

- 10.2.5. 1 g

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sigma-Aldrich

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Enzo

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BioVision

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 G Biosciences

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hello Bio

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MilliporeSigma

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tocris

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Abcam

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PromoCell

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 MedChemExpress

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Beyotime

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Maokang Biotechnology

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 YEASEN

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Solarbio

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Sigma-Aldrich

List of Figures

- Figure 1: Global Apoptosis Inducer Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Apoptosis Inducer Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Apoptosis Inducer Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Apoptosis Inducer Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Apoptosis Inducer Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Apoptosis Inducer Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Apoptosis Inducer Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Apoptosis Inducer Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Apoptosis Inducer Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Apoptosis Inducer Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Apoptosis Inducer Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Apoptosis Inducer Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Apoptosis Inducer Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Apoptosis Inducer Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Apoptosis Inducer Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Apoptosis Inducer Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Apoptosis Inducer Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Apoptosis Inducer Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Apoptosis Inducer Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Apoptosis Inducer Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Apoptosis Inducer Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Apoptosis Inducer Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Apoptosis Inducer Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Apoptosis Inducer Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Apoptosis Inducer Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Apoptosis Inducer Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Apoptosis Inducer Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Apoptosis Inducer Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Apoptosis Inducer Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Apoptosis Inducer Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Apoptosis Inducer Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Apoptosis Inducer Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Apoptosis Inducer Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Apoptosis Inducer Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Apoptosis Inducer Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Apoptosis Inducer Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Apoptosis Inducer Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Apoptosis Inducer Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Apoptosis Inducer Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Apoptosis Inducer Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Apoptosis Inducer?

The projected CAGR is approximately 9.37%.

2. Which companies are prominent players in the Apoptosis Inducer?

Key companies in the market include Sigma-Aldrich, Enzo, BioVision, G Biosciences, Hello Bio, MilliporeSigma, Tocris, Abcam, PromoCell, MedChemExpress, Beyotime, Maokang Biotechnology, YEASEN, Solarbio.

3. What are the main segments of the Apoptosis Inducer?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Apoptosis Inducer," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Apoptosis Inducer report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Apoptosis Inducer?

To stay informed about further developments, trends, and reports in the Apoptosis Inducer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence