Key Insights

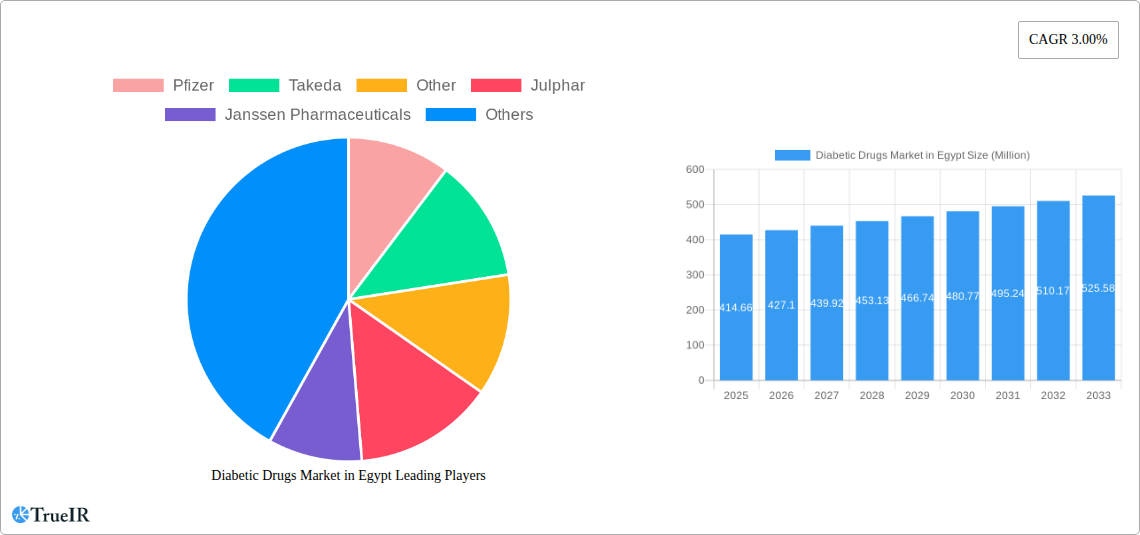

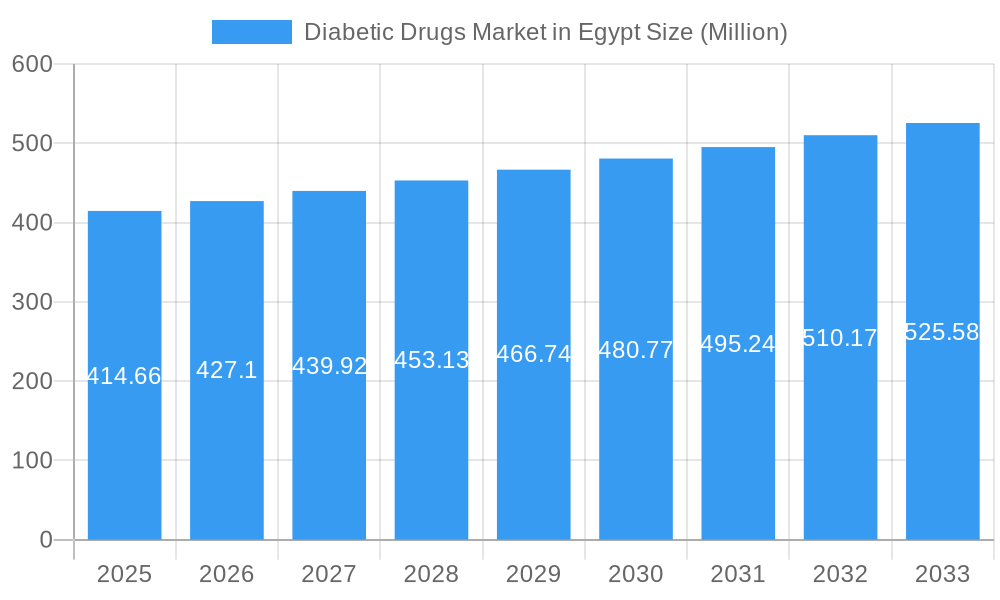

The Egyptian diabetic drugs market is poised for steady growth, estimated at a market size of USD 414.66 million in 2025, with a projected Compound Annual Growth Rate (CAGR) of 3.00% through 2033. This expansion is primarily driven by the increasing prevalence of diabetes, particularly Type 2 diabetes, within the Egyptian population. Factors such as lifestyle changes, including dietary habits and reduced physical activity, contribute significantly to this rising incidence. The market's expansion is further supported by advancements in pharmaceutical research and development, leading to the introduction of more effective and patient-friendly treatment options. Key product segments such as Insulins and Oral Antidiabetic Drugs (OADs) are expected to dominate, catering to the diverse needs of diabetic patients across different stages of the disease.

Diabetic Drugs Market in Egypt Market Size (In Million)

Distribution channels like hospitals and pharmacies will continue to be primary avenues for drug accessibility, while the growing adoption of online pharmacies is expected to open new avenues for market penetration and convenience for patients. While the market benefits from increased awareness and accessibility of treatments, certain challenges exist. These include potential price sensitivity among a segment of the population and the need for continuous healthcare infrastructure development to manage the growing burden of diabetes. However, with a strong focus on improving patient outcomes and the introduction of innovative therapies, the Egyptian diabetic drugs market is well-positioned for sustained growth and greater impact on public health in the coming years.

Diabetic Drugs Market in Egypt Company Market Share

Diabetic Drugs Market in Egypt: Comprehensive Market Analysis and Future Outlook (2019-2033)

Dive deep into the burgeoning Diabetic Drugs Market in Egypt with our latest, SEO-optimized report. This in-depth analysis provides critical insights for stakeholders navigating the evolving landscape of diabetes management in Egypt. Covering the study period of 2019–2033, with 2025 as the base year and estimated year, this report meticulously details market dynamics, growth trajectories, and competitive strategies. Uncover the projected CAGR of XX% from 2025–2033 and understand the intricate factors driving the Egyptian diabetes market.

Diabetic Drugs Market in Egypt Market Structure & Competitive Landscape

The Diabetic Drugs Market in Egypt exhibits a moderately concentrated structure, with established global pharmaceutical giants alongside a growing presence of local and regional players. Innovation is primarily driven by ongoing research and development into novel therapeutic agents, including next-generation insulins, advanced oral antidiabetic drugs (OADs), and innovative non-insulin injectables, with a significant focus on improving patient outcomes and adherence. Regulatory impacts from the Egyptian Drug Authority (EDA) play a crucial role, influencing drug approvals, pricing, and market access for both innovative and generic medications.

The threat of product substitutes, particularly from advancements in non-pharmacological interventions like bariatric surgery and continuous glucose monitoring systems, is a growing consideration. End-user segmentation reveals a strong demand across Type 1 and Type 2 diabetes, with Type 2 diabetes currently dominating due to its higher prevalence. Mergers and acquisitions (M&A) trends are anticipated to accelerate as companies seek to expand their portfolios, gain market share, and enhance their R&D capabilities. For instance, strategic partnerships aimed at local manufacturing and distribution are becoming increasingly prevalent.

- Market Concentration: Moderately concentrated with key players.

- Innovation Drivers: Novel drug development, personalized medicine.

- Regulatory Impacts: EDA approval processes, pricing controls.

- Product Substitutes: Non-pharmacological interventions, lifestyle modifications.

- End-User Segmentation: Dominance of Type 2 diabetes treatment.

- M&A Trends: Increasing focus on portfolio expansion and market access.

Diabetic Drugs Market in Egypt Market Trends & Opportunities

The Diabetic Drugs Market in Egypt is experiencing robust growth, propelled by an escalating prevalence of diabetes, a growing aging population, and increasing healthcare expenditure. Market size is projected to reach USD XXX Million by 2033, exhibiting a compelling CAGR of XX% during the forecast period (2025–2033). Technological shifts are profoundly impacting treatment paradigms, with a noticeable rise in the adoption of GLP-1 receptor agonists and SGLT2 inhibitors, offering improved glycemic control and cardiovascular benefits. Consumer preferences are increasingly leaning towards convenient and effective treatment options, driving demand for oral medications and less invasive injectable therapies.

Competitive dynamics are intensifying, with both global pharmaceutical leaders and emerging local manufacturers vying for market share. The rising awareness campaigns by governmental and non-governmental organizations regarding diabetes prevention and management are further contributing to market expansion by encouraging early diagnosis and treatment. Opportunities abound for companies focusing on the development and marketing of biosimilar insulins and innovative OADs that address unmet patient needs, such as reducing the risk of hypoglycemia and promoting weight loss. Furthermore, the Egyptian government's focus on enhancing healthcare infrastructure and promoting local pharmaceutical manufacturing presents significant opportunities for investment and growth. The increasing penetration of online pharmacies is also opening new distribution channels and enhancing accessibility for diabetic patients.

Dominant Markets & Segments in Diabetic Drugs Market in Egypt

The Diabetic Drugs Market in Egypt is characterized by the dominance of specific therapeutic areas and product types, driven by underlying epidemiological trends and market dynamics. Type 2 diabetes consistently represents the largest segment, accounting for over XX% of the total diabetes burden in Egypt. This is attributed to lifestyle factors, sedentary habits, and genetic predispositions prevalent in the population. Consequently, the demand for Oral Antidiabetic Drugs (OADs), which are the primary treatment modality for Type 2 diabetes, remains exceptionally high. Within the OAD segment, metformin continues to be a cornerstone, but newer classes like DPP-4 inhibitors, SGLT2 inhibitors, and GLP-1 receptor agonists are witnessing significant growth due to their efficacy and complementary mechanisms of action.

Insulins constitute another vital segment, crucial for both Type 1 and advanced Type 2 diabetes management. The market for insulins in Egypt is evolving with the introduction of biosimilar insulins and advancements in delivery devices, aiming to improve affordability and patient convenience. Non-insulin injectables, while currently a smaller segment, are poised for substantial growth, driven by the therapeutic advantages of GLP-1 receptor agonists in terms of glycemic control, weight management, and cardiovascular benefits.

The pharmacies distribution channel holds the largest share in the Egyptian diabetic drug market, owing to their widespread accessibility and the over-the-counter nature of some diabetes management products and the prescription dispensing of most medications. Hospitals play a critical role in managing complex diabetes cases and in initial diagnosis and treatment initiation. The online retailers segment, though nascent, is rapidly expanding, driven by the convenience and accessibility it offers to patients, especially in urban areas.

- Dominant Therapeutic Area: Type 2 Diabetes.

- Key Growth Drivers: High prevalence, lifestyle factors, aging population.

- Detailed Analysis: Type 2 diabetes requires long-term management, driving consistent demand for a broad range of pharmacotherapies.

- Dominant Product Type: Oral Antidiabetic Drugs (OADs).

- Key Growth Drivers: First-line therapy for Type 2 diabetes, affordability of generics, introduction of novel drug classes.

- Detailed Analysis: The extensive patient pool for Type 2 diabetes directly translates to a large market for OADs.

- Dominant Distribution Channel: Pharmacies.

- Key Growth Drivers: Extensive network, accessibility, prescription dispensing.

- Detailed Analysis: Pharmacies serve as the primary point of access for diabetic medications across Egypt.

Diabetic Drugs Market in Egypt Product Analysis

The Egyptian diabetic drugs market is characterized by a dynamic product landscape featuring both established and emerging therapeutic options. Innovations are centered on enhancing glycemic control, minimizing side effects, and improving patient adherence. The development of novel insulin formulations, including ultra-long-acting insulins and pre-mixed insulins, aims to simplify treatment regimens. In the OAD segment, advancements focus on combination therapies and drugs with dual mechanisms of action, offering synergistic benefits. The rise of GLP-1 receptor agonists and SGLT2 inhibitors is a significant trend, with these non-insulin injectables and oral agents demonstrating robust efficacy in managing blood glucose, promoting weight loss, and providing cardiovascular protection. Competitive advantages lie in drugs that offer improved safety profiles, reduced risk of hypoglycemia, and enhanced patient convenience, aligning with the evolving needs of the Egyptian diabetic population.

Key Drivers, Barriers & Challenges in Diabetic Drugs Market in Egypt

Key Drivers:

- Rising Diabetes Prevalence: The escalating incidence of diabetes in Egypt, driven by lifestyle changes and an aging population, is the primary growth catalyst.

- Increasing Healthcare Expenditure: Government initiatives and rising disposable incomes are boosting overall healthcare spending, including investments in diabetes management.

- Technological Advancements: Introduction of novel drug classes (GLP-1 RAs, SGLT2 inhibitors) and improved delivery systems enhance treatment efficacy and patient outcomes.

- Government Support for Local Manufacturing: Policies encouraging domestic production can lead to increased availability and potentially lower costs of diabetic medications.

Barriers & Challenges:

- Pricing Pressures and Affordability: While generics offer some relief, the cost of newer, innovative therapies can be a barrier for a significant portion of the population.

- Regulatory Hurdles: Stringent approval processes and post-market surveillance can impact the speed of new drug introductions.

- Supply Chain Complexities: Ensuring consistent availability of essential diabetic drugs across all regions of Egypt can be challenging, particularly for imported medications.

- Limited Access to Advanced Diagnostics: Inadequate access to advanced diagnostic tools can lead to delayed diagnosis and suboptimal treatment initiation.

- Competition from Counterfeit Drugs: The prevalence of counterfeit medications poses a significant risk to patient safety and undermines legitimate market players.

Growth Drivers in the Diabetic Drugs Market in Egypt Market

The Diabetic Drugs Market in Egypt is fueled by several powerful growth drivers. Epidemiological trends, specifically the increasing prevalence of Type 2 diabetes, form the bedrock of market expansion, creating a sustained demand for therapeutic interventions. Economic factors such as rising per capita income and growing government investment in healthcare infrastructure are crucial enablers, enhancing access to and affordability of diabetes medications. Technological advancements in pharmaceutical research and development have led to the introduction of more effective and patient-friendly drugs, including advanced insulins, oral antidiabetic drugs (OADs) with improved safety profiles, and innovative non-insulin injectables like GLP-1 receptor agonists and SGLT2 inhibitors. These innovations not only improve glycemic control but also offer cardiovascular and renal protective benefits, aligning with the growing understanding of diabetes as a systemic disease. Furthermore, increasing health awareness among the Egyptian population, spurred by public health campaigns and media coverage, is driving earlier diagnosis and a proactive approach to diabetes management, thereby expanding the market for diabetic drugs.

Challenges Impacting Diabetic Drugs Market in Egypt Growth

The Diabetic Drugs Market in Egypt faces significant challenges that can impede its growth trajectory. Regulatory complexities present a consistent hurdle; while aimed at ensuring quality and safety, the lengthy approval processes for new drugs can delay market entry and limit the availability of cutting-edge treatments. Supply chain inefficiencies are another critical concern, with geographical disparities in distribution networks and potential import/export challenges impacting the consistent availability of essential medications across the country. Pricing pressures remain a substantial restraint, as the cost of innovative therapies can be prohibitive for a large segment of the Egyptian population, leading to reliance on more affordable, and sometimes less effective, generic options. Intense competitive pressure from both global pharmaceutical giants and a growing number of local manufacturers can lead to price erosion and necessitate significant marketing investments. Lastly, challenges related to patient education and adherence, coupled with limited access to advanced diabetes monitoring technologies in certain regions, can affect optimal treatment outcomes and market penetration for advanced therapies.

Key Players Shaping the Diabetic Drugs Market in Egypt Market

- Pfizer

- Takeda

- Julphar

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- Merck and Co

- AstraZeneca

- Sanofi Aventis

- Bristol Myers Squibb

- Novo Nordisk A/S

- Boehringer Ingelheim

- Astellas

Significant Diabetic Drugs Market in Egypt Industry Milestones

- November 2023: Novo Nordisk initiated a Phase III comparative trial for their pipeline drug CagriSema against the recently approved Zepbound, signaling potential future competition in the rapidly evolving weight management and diabetes treatment space.

- October 2022: The Ministry of Industry and Advanced Technology announced MOUs worth USD 70.8 million between pharmaceutical and medical device companies in the UAE. This initiative, aligning with national strategies, aims to attract investment and foster local production, including the establishment of the first factory in the Middle East for Glargine (a type of insulin) by PureHealth and Gulf Pharmaceutical Industries Company, impacting regional supply chains and manufacturing capabilities.

Future Outlook for Diabetic Drugs Market in Egypt Market

The Diabetic Drugs Market in Egypt is poised for continued expansion, driven by an enduring high prevalence of diabetes and an increasing focus on proactive health management. Strategic opportunities lie in the burgeoning demand for advanced therapeutics, including innovative oral antidiabetic drugs (OADs) and non-insulin injectables like GLP-1 receptor agonists and SGLT2 inhibitors, which offer superior glycemic control and added metabolic benefits. The market potential is further amplified by government initiatives promoting local pharmaceutical manufacturing and the increasing penetration of online retail channels, enhancing accessibility and affordability. As healthcare expenditure rises and public awareness grows, the Egyptian diabetic drugs market represents a promising landscape for pharmaceutical innovation and investment, with a strong emphasis on patient-centric solutions that improve quality of life and long-term health outcomes.

Diabetic Drugs Market in Egypt Segmentation

-

1. Product Type

- 1.1. Insulins

- 1.2. OADs

- 1.3. non-insulin injectables

-

2. Therapeutic Area

- 2.1. Type 1 diabetes

- 2.2. Type 2 diabetes

-

3. Distribution Channel

- 3.1. Hospitals

- 3.2. pharmacies

- 3.3. online retailers

Diabetic Drugs Market in Egypt Segmentation By Geography

- 1. Egypt

Diabetic Drugs Market in Egypt Regional Market Share

Geographic Coverage of Diabetic Drugs Market in Egypt

Diabetic Drugs Market in Egypt REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Insulins

- 5.1.2. OADs

- 5.1.3. non-insulin injectables

- 5.2. Market Analysis, Insights and Forecast - by Therapeutic Area

- 5.2.1. Type 1 diabetes

- 5.2.2. Type 2 diabetes

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hospitals

- 5.3.2. pharmacies

- 5.3.3. online retailers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Diabetic Drugs Market in Egypt Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Insulins

- 6.1.2. OADs

- 6.1.3. non-insulin injectables

- 6.2. Market Analysis, Insights and Forecast - by Therapeutic Area

- 6.2.1. Type 1 diabetes

- 6.2.2. Type 2 diabetes

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hospitals

- 6.3.2. pharmacies

- 6.3.3. online retailers

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pfizer

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Takeda

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Other

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Julphar

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Janssen Pharmaceuticals

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Eli Lilly

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Novartis

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Merck and Co

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AstraZeneca

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sanofi Aventis

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Bristol Myers Squibb

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Novo Nordisk A/S

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Boehringer Ingelheim

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Sanofi Aventis

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Astellas

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Pfizer

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global Diabetic Drugs Market in Egypt Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Diabetic Drugs Market in Egypt Volume Breakdown (Egypt, %) by Region 2025 & 2033

- Figure 3: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Product Type 2025 & 2033

- Figure 4: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Product Type 2025 & 2033

- Figure 5: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Product Type 2025 & 2033

- Figure 7: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Therapeutic Area 2025 & 2033

- Figure 8: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Therapeutic Area 2025 & 2033

- Figure 9: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Therapeutic Area 2025 & 2033

- Figure 10: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Therapeutic Area 2025 & 2033

- Figure 11: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 12: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Distribution Channel 2025 & 2033

- Figure 13: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 14: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 15: Egypt Diabetic Drugs Market in Egypt Revenue (Million), by Country 2025 & 2033

- Figure 16: Egypt Diabetic Drugs Market in Egypt Volume (Egypt), by Country 2025 & 2033

- Figure 17: Egypt Diabetic Drugs Market in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 18: Egypt Diabetic Drugs Market in Egypt Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Product Type 2020 & 2033

- Table 3: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Therapeutic Area 2020 & 2033

- Table 4: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Therapeutic Area 2020 & 2033

- Table 5: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Distribution Channel 2020 & 2033

- Table 7: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Region 2020 & 2033

- Table 9: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Product Type 2020 & 2033

- Table 11: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Therapeutic Area 2020 & 2033

- Table 12: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Therapeutic Area 2020 & 2033

- Table 13: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Diabetic Drugs Market in Egypt Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Diabetic Drugs Market in Egypt Volume Egypt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetic Drugs Market in Egypt?

The projected CAGR is approximately 3.00%.

2. Which companies are prominent players in the Diabetic Drugs Market in Egypt?

Key companies in the market include Pfizer, Takeda, Other, Julphar, Janssen Pharmaceuticals, Eli Lilly, Novartis, Merck and Co, AstraZeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Boehringer Ingelheim, Sanofi Aventis, Astellas.

3. What are the main segments of the Diabetic Drugs Market in Egypt?

The market segments include Product Type, Therapeutic Area, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 414.66 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The oral anti-diabetic drugs segment holds the highest market share in the Egypt Diabetes Drugs Market in the current year.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

Novmber 2023: Novo Nordisk's initiation of a Phase III comparative trial for their pipeline drug CagriSema against the recently approved Zepbound suggests the potential for direct competition between the two drugs upon Novo Nordisk's candidate entering the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Egypt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetic Drugs Market in Egypt," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetic Drugs Market in Egypt report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetic Drugs Market in Egypt?

To stay informed about further developments, trends, and reports in the Diabetic Drugs Market in Egypt, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence