Key Insights

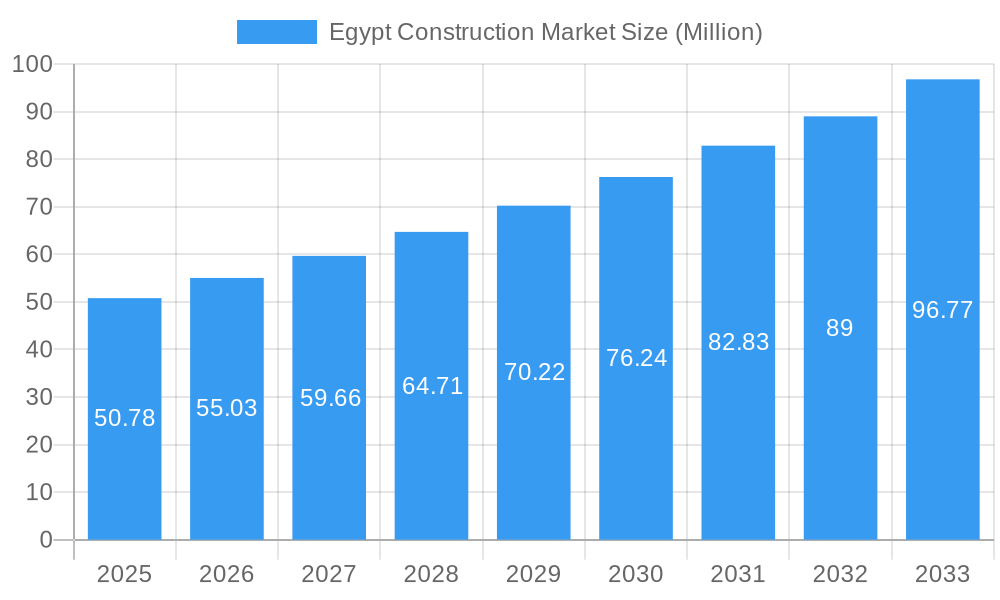

The Egyptian construction market is poised for substantial expansion, demonstrating a robust CAGR of 8.39% and a projected market size of USD 50.78 million in 2025. This growth is primarily fueled by significant government investment in infrastructure development, including ambitious projects like the New Administrative Capital and widespread urban renewal initiatives. The residential sector continues to be a dominant force, driven by a growing population and increasing demand for affordable housing solutions. Additionally, the commercial and energy & utilities segments are experiencing healthy growth, propelled by foreign direct investment and the nation's focus on renewable energy projects and power generation capacity enhancement. Key drivers include government stimulus packages, a favorable investment climate, and the expansion of the Suez Canal Economic Zone, which is attracting considerable industrial and logistical development.

Egypt Construction Market Market Size (In Million)

While the market exhibits strong upward momentum, certain restraints could influence the pace of growth. These include potential challenges related to fluctuating raw material prices, the availability of skilled labor, and the regulatory environment for new projects. However, the overarching trend indicates a positive trajectory, with emerging opportunities in sustainable construction practices and smart city technologies. The industrial sector is also set to benefit from localization efforts and the drive to boost manufacturing output. With a strategic focus on infrastructure and housing, coupled with a conducive economic policy, Egypt's construction landscape is expected to remain dynamic and attractive to both domestic and international stakeholders throughout the forecast period of 2025-2033.

Egypt Construction Market Company Market Share

Egypt Construction Market: Comprehensive Industry Analysis & Future Outlook (2019-2033)

This in-depth report provides a dynamic, SEO-optimized analysis of the Egypt construction market. Leveraging high-volume keywords such as Egypt real estate development, construction companies Egypt, infrastructure projects Egypt, and MENA construction market, this study offers critical insights for stakeholders including investors, developers, contractors, and government agencies. Our analysis spans the historical period (2019-2024), the base year (2025), and the forecast period (2025-2033), with a specific focus on trends, opportunities, and the competitive landscape.

Egypt Construction Market Market Structure & Competitive Landscape

The Egypt construction market is characterized by a moderately concentrated structure, with a few large, established players dominating significant portions of key infrastructure projects Egypt and large-scale residential developments. Innovation drivers are increasingly centered around sustainable building practices, digital construction technologies, and the adoption of modern materials. Regulatory impacts are significant, with government initiatives aimed at streamlining approvals and encouraging foreign investment playing a crucial role. Product substitutes are limited in core construction but emerge in specialized areas like alternative building materials and pre-fabricated components. End-user segmentation reveals a strong demand across residential construction Egypt, commercial real estate Egypt, and burgeoning industrial construction Egypt. Merger and acquisition (M&A) trends are indicative of market consolidation and strategic expansion, particularly among companies seeking to enhance their capabilities in specialized sectors like renewable energy infrastructure. Quantitative data points to a significant increase in project financing, with M&A volumes projected to rise by an estimated 15% over the forecast period.

- Market Concentration: Dominated by a mix of large national players and international firms with a strong local presence.

- Innovation Drivers: Sustainable materials, smart building technology, and pre-fabrication.

- Regulatory Impact: Government support for megaprojects and simplified investment procedures.

- End-User Segmentation: Residential, commercial, and infrastructure sectors showing robust growth.

- M&A Trends: Strategic acquisitions to expand service offerings and market reach.

Egypt Construction Market Market Trends & Opportunities

The Egypt construction market is experiencing a robust growth trajectory, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 7.8% during the forecast period (2025-2033). This expansion is fueled by a confluence of factors, including significant government investment in national development plans, a rapidly growing population driving demand for housing and urban infrastructure, and an increasing influx of foreign direct investment into the country. The market is witnessing a notable technological shift, with the adoption of Building Information Modeling (BIM), 3D printing construction, and advanced project management software becoming more prevalent. Consumer preferences are evolving, with a growing emphasis on sustainable, energy-efficient, and smart homes and commercial spaces. Competitive dynamics are intensifying, pushing companies to differentiate through innovation, cost-efficiency, and the ability to deliver complex projects on time and within budget. Opportunities abound in the development of new cities, the expansion of transportation networks, and the retrofitting of existing infrastructure to meet modern standards. Market penetration rates for advanced construction techniques are still relatively low, presenting a significant opportunity for early adopters. The Egyptian construction industry is poised for sustained growth, driven by both public and private sector initiatives. The MENA construction sector outlook also benefits from Egypt's strategic position and economic reforms.

Dominant Markets & Segments in Egypt Construction Market

The Residential segment is a dominant force within the Egypt construction market, driven by a burgeoning population and government initiatives to address housing shortages. Significant growth is also observed in Transportation Infrastructure, bolstered by ambitious government plans to upgrade and expand road networks, railways, and ports across the nation. The Energy and Utilities sector is another key area of expansion, with substantial investments in renewable energy projects and power generation facilities.

- Residential Construction:

- Key Growth Drivers: Rapid urbanization, increasing disposable incomes, and government housing programs like "Hayah Karima."

- Market Dominance: Driven by demand for affordable housing, luxury apartments, and integrated community developments.

- Transportation Infrastructure:

- Key Growth Drivers: Government vision for a connected Egypt, facilitating trade and tourism, and the development of new economic zones.

- Market Dominance: Includes major highway expansion projects, high-speed rail development, and port modernization initiatives.

- Energy and Utilities:

- Key Growth Drivers: Egypt's commitment to renewable energy targets, expansion of the national grid, and increasing demand for power from industrial and residential sectors.

- Market Dominance: Focus on solar, wind energy projects, and upgrades to existing power transmission and distribution networks.

- Commercial Construction:

- Key Growth Drivers: Growing tourism sector, expansion of retail and hospitality, and the development of new business districts.

- Industrial Construction:

- Key Growth Drivers: Government efforts to attract foreign investment in manufacturing and the development of industrial zones.

Egypt Construction Market Product Analysis

The Egypt construction market is witnessing a surge in product innovations driven by a need for greater efficiency, sustainability, and resilience. Advanced materials, such as high-performance concrete, eco-friendly insulation, and modular building components, are gaining traction, offering enhanced durability and reduced environmental impact. Applications span across all segments, from energy-efficient residential units to robust infrastructure projects. Technological advancements in pre-fabrication and 3D printing construction are providing competitive advantages by significantly reducing construction timelines and labor costs. These innovations are crucial for meeting the fast-paced development demands and aligning with global sustainability standards.

Key Drivers, Barriers & Challenges in Egypt Construction Market

Key Drivers, Barriers & Challenges in Egypt Construction Market

Key Drivers: The Egypt construction market is propelled by several key drivers. Foremost is the substantial government investment in infrastructure development, exemplified by mega-projects aimed at modernizing the nation. Economic reforms and incentives are attracting significant foreign direct investment, further fueling construction activity. A growing young population and increasing urbanization create a persistent demand for residential and commercial spaces. Technological advancements, such as the adoption of BIM and sustainable building materials, are enhancing efficiency and project quality.

Barriers & Challenges: Despite the positive outlook, the market faces several challenges. Supply chain disruptions, particularly for imported materials, can lead to project delays and cost overruns. Regulatory complexities and bureaucratic hurdles, although being streamlined, can still pose obstacles. Fierce competition among a large number of local and international players can put pressure on profit margins. Access to skilled labor remains a concern, necessitating investment in training and development programs. Securing consistent and accessible financing for projects of all scales is also a crucial consideration.

Growth Drivers in the Egypt Construction Market Market

Key growth drivers in the Egypt construction market include substantial government impetus for national development plans, such as the Vision 2030 strategy, which prioritizes infrastructure upgrades and urban expansion. The government's commitment to attracting foreign investment through favorable policies and economic reforms is a significant catalyst. Furthermore, Egypt's rapidly growing population and high urbanization rate are creating sustained demand for housing, commercial spaces, and essential public infrastructure. Technological adoption, particularly in digitalization and sustainable construction methods, is enhancing project delivery and creating new market opportunities.

Challenges Impacting Egypt Construction Market Growth

Several challenges impact the Egypt construction market growth. Persistent supply chain issues, particularly for specialized materials and equipment, can lead to project delays and increased costs. Regulatory frameworks, while improving, can still present complexities and administrative burdens for new entrants and ongoing projects. Intense competitive pressures among a large number of local and international firms can affect project pricing and profitability. The availability of skilled labor also remains a concern, requiring continuous investment in training and development to meet industry demands for specialized expertise.

Key Players Shaping the Egypt Construction Market Market

- RAYA Holdings

- Osman Group

- Palm Hills Developments

- AL-AHLY Development

- GAMA Constructions

- DORRA Group

- The Arab Contractors

- Construction & Reconstruction Engineering Company

- Energya- PTS

- H A Construction (H A C)

Significant Egypt Construction Market Industry Milestones

- October 2022: ERG Developments commenced construction on the residential complex Ri8 in the New Administrative Capital (NAC), with an estimated investment of 3.5 billion Egyptian pounds. This 25-acre project, part of Zawya Projects, is designed in three phases and will feature 34 residential structures comprising 1,063 units.

- November 2022: Orascom Construction PLC announced a strategic partnership with COBOD, a Danish company, to introduce 3D Printing Construction (3DPC) technology to Egypt for the first time. This collaboration aims to explore project completion, equipment sales, and operation and maintenance, with a long-term vision of using 3DPC for constructing entire buildings within the Egyptian market.

Future Outlook for Egypt Construction Market Market

The Egypt construction market is poised for sustained and significant growth in the coming years. Key growth catalysts include ongoing mega-infrastructure projects, such as the expansion of the Suez Canal economic zone and new city developments. The government's continued focus on attracting foreign investment and its commitment to sustainable development practices will further bolster the sector. Strategic opportunities lie in the increasing adoption of green building technologies, smart city solutions, and the development of renewable energy infrastructure. The market's potential is immense, driven by a young demographic and ambitious national development agendas.

Egypt Construction Market Segmentation

-

1. Sector

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

- 1.4. Transportation Infrastructure

- 1.5. Energy and Utilities

Egypt Construction Market Segmentation By Geography

- 1. Egypt

Egypt Construction Market Regional Market Share

Geographic Coverage of Egypt Construction Market

Egypt Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.1.4. Transportation Infrastructure

- 5.1.5. Energy and Utilities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Egypt Construction Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Industrial

- 6.1.4. Transportation Infrastructure

- 6.1.5. Energy and Utilities

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 RAYA Holdings**List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Osman Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Palm Hills Developments

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 AL-AHLY Development

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 GAMA Constructions

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 DORRA Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 The Arab Contractors

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Construction & Reconstruction Engineering Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Energya- PTS

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 H A Construction (H A C)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 RAYA Holdings**List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Egypt Construction Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Egypt Construction Market Share (%) by Company 2025

List of Tables

- Table 1: Egypt Construction Market Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: Egypt Construction Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Egypt Construction Market Revenue Million Forecast, by Sector 2020 & 2033

- Table 4: Egypt Construction Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Egypt Construction Market?

The projected CAGR is approximately 8.39%.

2. Which companies are prominent players in the Egypt Construction Market?

Key companies in the market include RAYA Holdings**List Not Exhaustive, Osman Group, Palm Hills Developments, AL-AHLY Development, GAMA Constructions, DORRA Group, The Arab Contractors, Construction & Reconstruction Engineering Company, Energya- PTS, H A Construction (H A C).

3. What are the main segments of the Egypt Construction Market?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.78 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing demand for green construction to reduce carbon footprint4.; Introduction of technology for manufactruing the of building construction material.

6. What are the notable trends driving market growth?

Increased investment in residential segment by government driving the market.

7. Are there any restraints impacting market growth?

4.; High cost of purchasing the equipment for development and manufacturing of various construction material.

8. Can you provide examples of recent developments in the market?

October 2022: ERG Developments in the New Administrative Capital (NAC) has begun construction on the residential complex Ri8 for an estimated 3.5 billion Egyptian pounds. The 25-acre Ri8 Compound is part of Zawya Projects, which was to be built in three phases and includes 34 residential structures with 1,063 units.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Egypt Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Egypt Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Egypt Construction Market?

To stay informed about further developments, trends, and reports in the Egypt Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence