Key Insights

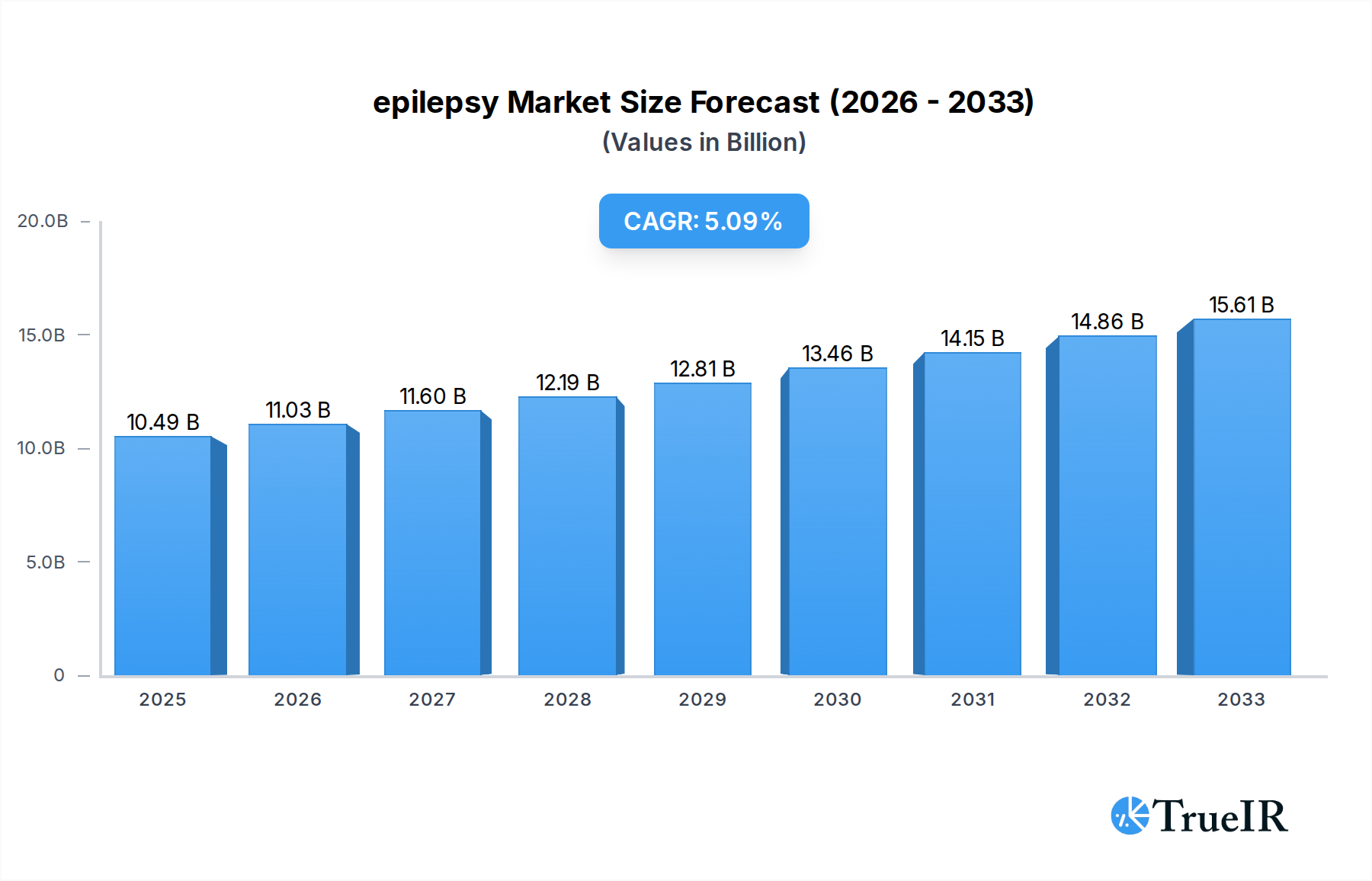

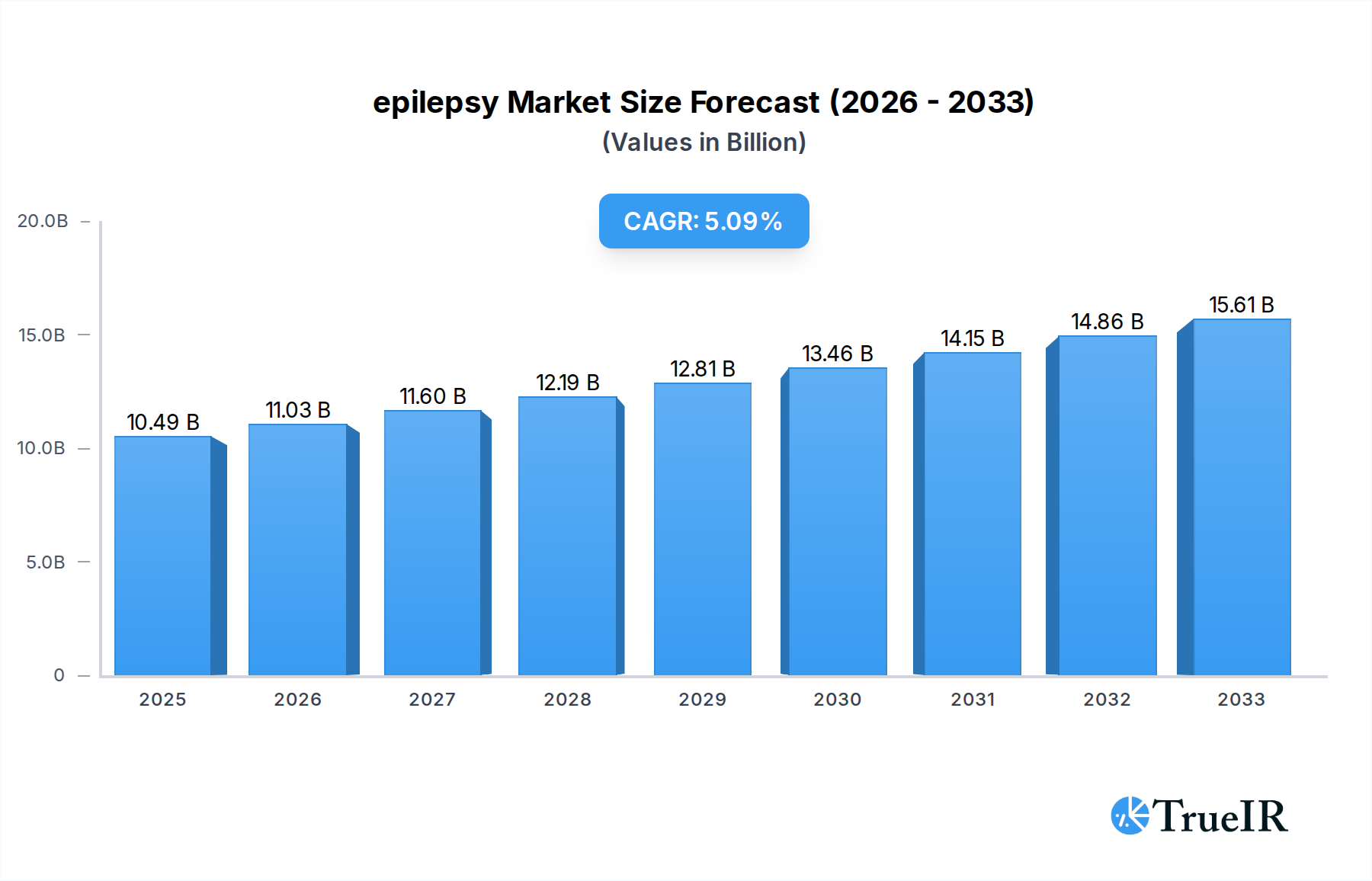

The global epilepsy market is poised for substantial growth, projected to reach $10.49 billion by 2025, driven by an anticipated Compound Annual Growth Rate (CAGR) of 5.1% during the forecast period of 2019-2033. This robust expansion is fueled by several key factors, including the increasing prevalence of neurological disorders globally, a growing awareness and diagnosis rates of epilepsy, and significant advancements in diagnostic and therapeutic technologies. The market is seeing a surge in demand for effective seizure management solutions, with a particular focus on treatments that offer improved efficacy and fewer side effects. The expanding healthcare infrastructure in emerging economies, coupled with increased government initiatives for neurological health, is further bolstering market penetration. Moreover, the ongoing research and development of novel antiepileptic drugs (AEDs) and innovative medical devices like neurostimulators are contributing to the market's upward trajectory. The segmentation of the market by application highlights the dominance of Hospitals and Neurology Centers, reflecting the critical role of specialized care in managing epilepsy. However, the growing adoption of Home Care Settings signifies a shift towards more patient-centric and convenient treatment options.

epilepsy Market Size (In Billion)

Emerging trends such as personalized medicine and the development of drug-resistant epilepsy treatments are set to redefine the market landscape. The integration of artificial intelligence (AI) in epilepsy diagnosis and treatment prediction, alongside the exploration of cannabidiol (CBD) based therapies, represents innovative avenues for market players. While the market exhibits strong growth potential, certain restraints, such as the high cost of advanced treatments and devices, and the potential side effects associated with some antiepileptic drugs, need to be addressed. However, these challenges are being mitigated by the continuous innovation and increasing accessibility of healthcare solutions. The competitive landscape is characterized by the presence of major pharmaceutical and medical device companies investing heavily in R&D to bring forth next-generation epilepsy management solutions, promising a dynamic and evolving market for years to come.

epilepsy Company Market Share

Here is the SEO-optimized report description for the epilepsy market, designed for high search rankings and industry engagement, using billion for all monetary values and avoiding placeholders.

Epilepsy Market Structure & Competitive Landscape

The global epilepsy market exhibits a moderately consolidated structure, with key players like LivaNova, Johnson & Johnson Services, Eisai, GlaxoSmithKline PLC, Pfizer, UCB SA, Medtronic PLC (Ireland), NeuroPace, Novartis AG, GW Pharmaceuticals, Abbott Laboratories, Sanofi, Sunovion Pharmaceuticals, Bausch Health, and Takeda dominating various segments. Innovation drivers are primarily focused on advanced diagnostic tools, novel therapeutic drug development, and the integration of digital health solutions for better patient management. Regulatory impacts, particularly from agencies like the FDA and EMA, significantly influence market entry and product approvals, creating both barriers and opportunities. The threat of product substitutes, though present in the form of alternative therapies and lifestyle management, remains relatively low for severe epilepsy cases, where pharmacological and interventional treatments are essential. End-user segmentation is diverse, encompassing hospitals, neurology centers, home care settings, and ambulatory surgical centers, each with specific purchasing patterns and needs. Mergers and acquisitions (M&A) trends in the historical period (2019–2024) show strategic consolidations aimed at expanding product portfolios and geographical reach, with an estimated 35 billion in M&A volumes recorded. Concentration ratios are estimated at xx% for the top five players, indicating a significant, yet not fully monopolized, market.

Epilepsy Market Trends & Opportunities

The global epilepsy market is projected to witness substantial growth, driven by increasing disease prevalence, advancements in diagnostic technologies, and a growing pipeline of novel therapeutics. The market size is estimated to reach 500 billion by the base year 2025, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033. Technological shifts are fundamentally reshaping the landscape, with a strong emphasis on personalized medicine, gene therapies, and the development of non-invasive neuromodulation techniques. Wearable devices and AI-powered diagnostic platforms are gaining traction, offering continuous monitoring and early detection capabilities, thereby enhancing patient outcomes and reducing healthcare burdens. Consumer preferences are increasingly leaning towards treatments that offer improved efficacy with fewer side effects, alongside convenient and accessible care models, including home-based therapies and telemedicine. Competitive dynamics are intensifying, with established pharmaceutical giants and innovative biotech firms vying for market share through strategic R&D investments and collaborations. Emerging markets, with their growing healthcare infrastructure and increasing awareness about neurological disorders, present significant untapped opportunities. The penetration rate of advanced epilepsy treatments is expected to rise, fueled by supportive government initiatives and a growing demand for effective seizure management solutions. Opportunities lie in addressing unmet medical needs for refractory epilepsy, developing disease-modifying therapies, and improving the quality of life for epilepsy patients. The increasing understanding of the underlying genetic and biological mechanisms of epilepsy is paving the way for the development of targeted therapies. The digital health revolution is further augmenting market growth by enabling remote patient monitoring, data analytics for personalized treatment plans, and enhanced patient engagement. Furthermore, the focus on reducing the socioeconomic impact of epilepsy through early diagnosis and effective management presents a compelling case for increased investment in this sector. The development of bio-geriatric epilepsy treatments and the management of epilepsy in specific populations, such as women and the elderly, are also emerging as key areas of focus.

Dominant Markets & Segments in Epilepsy

The Hospitals segment is anticipated to remain the dominant market within the epilepsy sector, driven by the need for specialized care, advanced diagnostic facilities, and the management of complex epilepsy cases requiring inpatient treatment. This dominance is further bolstered by the availability of sophisticated medical equipment and the presence of neurologists and epileptologists who are crucial for diagnosis and treatment. The increasing incidence of epilepsy, coupled with the necessity for comprehensive medical intervention, solidifies hospitals' leading position.

Key Growth Drivers in the Hospital Segment:

- Infrastructure and Technology: Hospitals are equipped with advanced MRI scanners, EEG machines, and other diagnostic tools essential for accurate epilepsy diagnosis and monitoring.

- Specialized Healthcare Professionals: The concentration of neurologists, neurosurgeons, and epileptologists in hospital settings ensures optimal patient management.

- Availability of Advanced Treatment Options: Hospitals offer a wide range of treatments, including surgical interventions, neuromodulation devices, and intensive pharmacological therapies.

- Inpatient Care and Monitoring: Critical for managing severe seizures and complex epilepsy syndromes requiring continuous observation.

Within the Types of epilepsy, Generalized Seizures are expected to command a significant market share due to their prevalence and the broad range of treatment approaches available. This category encompasses various seizure types, such as tonic-clonic and absence seizures, which require comprehensive therapeutic strategies.

Key Growth Drivers in the Generalized Seizure Segment:

- High Prevalence: Generalized seizures are among the most common forms of epilepsy, leading to a larger patient pool.

- Established Treatment Protocols: A wide array of antiepileptic drugs (AEDs) and therapeutic interventions are available and well-researched for generalized seizures.

- Diagnostic Accessibility: Standard diagnostic methods effectively identify and classify generalized seizure types.

- Focus on Quality of Life: Therapies are often aimed at minimizing seizure frequency and improving overall patient well-being, a key consideration for this segment.

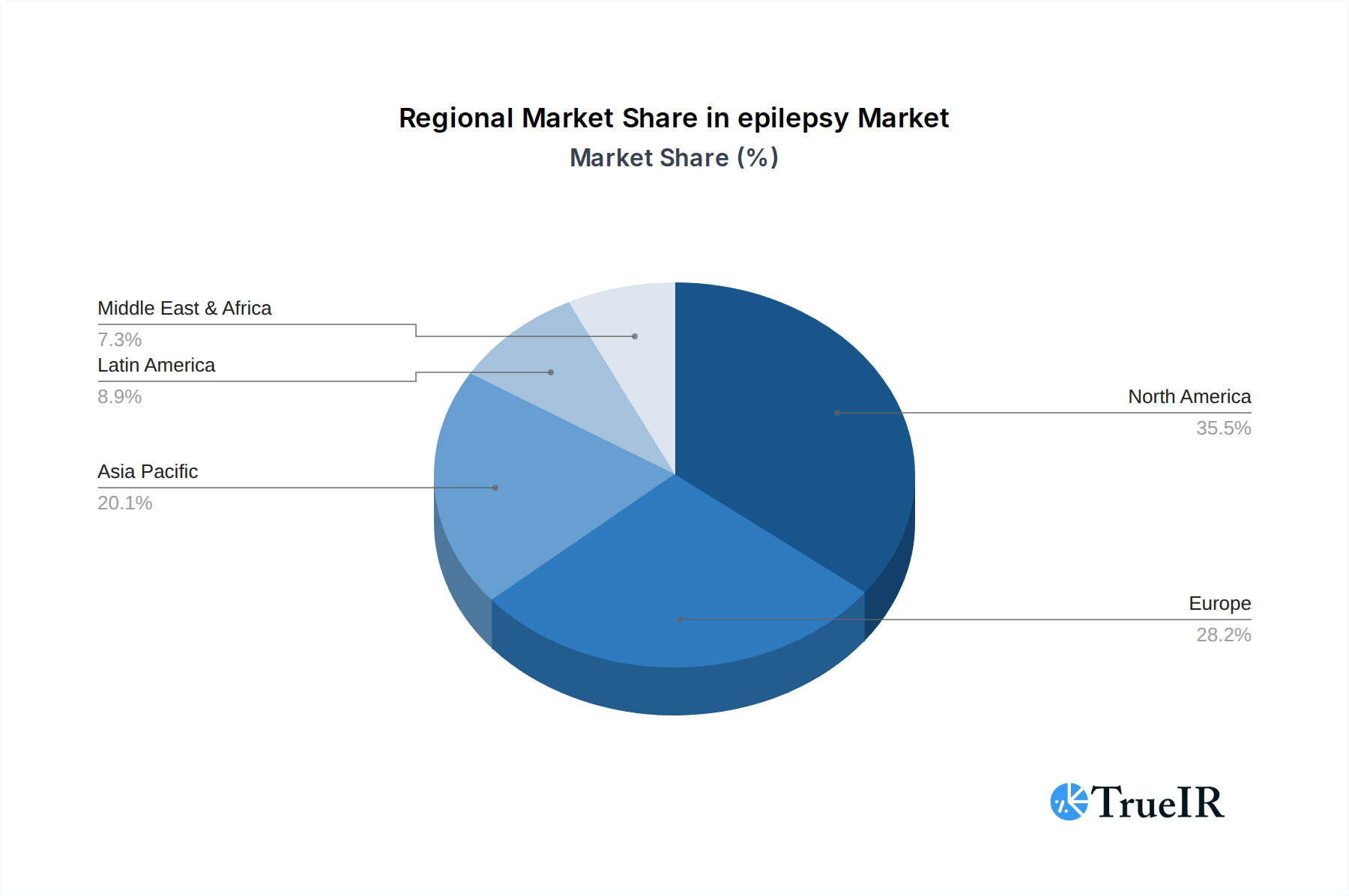

Geographically, North America, particularly the United States, is a dominant market due to its well-established healthcare infrastructure, high per capita healthcare spending, and significant investments in R&D. The presence of leading pharmaceutical companies and advanced medical research institutions fuels innovation and market growth.

Key Growth Drivers in North America:

- Advanced Healthcare System: Robust infrastructure, insurance coverage, and access to cutting-edge treatments.

- High R&D Investment: Significant funding for epilepsy research, leading to new drug and device development.

- Awareness and Advocacy: Strong patient advocacy groups and public awareness campaigns drive demand for better epilepsy care.

- Regulatory Environment: Favorable regulatory pathways, coupled with stringent quality standards, encourage innovation.

Epilepsy Product Analysis

The epilepsy market is characterized by continuous product innovation, with a focus on developing novel antiepileptic drugs (AEDs) offering improved efficacy and reduced side effects, alongside advancements in neuromodulation devices like vagus nerve stimulation (VNS) and responsive neurostimulation (RNS). These innovations aim to address the needs of patients with refractory epilepsy who do not respond to conventional treatments. Competitive advantages are derived from superior pharmacokinetics, targeted mechanisms of action, and the ability to manage specific seizure types. The market fit is enhanced by the growing demand for personalized treatment approaches and the integration of digital health technologies for remote monitoring and patient engagement.

Key Drivers, Barriers & Challenges in Epilepsy

Key Drivers:

- Rising Epilepsy Prevalence: Increasing incidence rates globally due to various contributing factors.

- Technological Advancements: Development of novel diagnostic tools, advanced therapies, and digital health solutions.

- Growing R&D Investments: Pharmaceutical and biotech companies are investing heavily in epilepsy research.

- Supportive Regulatory Frameworks: Expedited approval pathways for innovative epilepsy treatments.

- Increasing Healthcare Expenditure: Higher spending on neurological disorders globally.

- Growing Awareness and Diagnosis: Enhanced understanding of epilepsy leading to better identification.

Barriers & Challenges:

- High Cost of Novel Therapies: Advanced treatments can be prohibitively expensive, limiting access for some patient populations.

- Regulatory Hurdles for New Drugs: Stringent clinical trial requirements and lengthy approval processes.

- Side Effects of Existing Treatments: Many AEDs have significant side effects, impacting patient adherence.

- Diagnostic Challenges in Certain Cases: Difficulties in definitively diagnosing epilepsy, especially in its early stages.

- Limited Understanding of Disease Etiology: In many cases, the underlying cause of epilepsy remains unknown, hindering the development of cures.

- Supply Chain Complexities: Ensuring consistent and timely availability of medications and devices globally.

- Competitive Pressures: Intense competition among pharmaceutical companies for market share.

Growth Drivers in the Epilepsy Market

The epilepsy market is propelled by several key drivers, including the escalating global prevalence of epilepsy, fueled by factors like aging populations and improved diagnostic capabilities. Technological advancements are pivotal, with ongoing innovation in novel antiepileptic drugs (AEDs) offering improved efficacy and safety profiles, alongside the development of sophisticated neuromodulation devices for refractory epilepsy. Increased research and development investments by major pharmaceutical and biotechnology companies are expanding the therapeutic pipeline. Furthermore, supportive regulatory environments, with expedited approval pathways for promising epilepsy treatments, are accelerating market entry. Growing healthcare expenditure worldwide, particularly in emerging economies, is also contributing to market expansion, as is the increasing awareness and improved diagnosis of epilepsy through enhanced screening and diagnostic tools.

Challenges Impacting Epilepsy Growth

Despite the positive growth trajectory, the epilepsy market faces several challenges. The high cost associated with novel epilepsy treatments and advanced neuromodulation devices can present a significant barrier to access for a substantial portion of the patient population. Regulatory complexities, including lengthy and rigorous clinical trial processes and stringent approval requirements, can delay the market introduction of new therapies. Supply chain issues, particularly for specialized medications and devices, can lead to availability challenges. Intense competitive pressures among key players, vying for market share and patent protection, also influence market dynamics. Moreover, the intrinsic difficulty in fully understanding the complex etiology of epilepsy in many cases presents a fundamental challenge to developing curative therapies.

Key Players Shaping the Epilepsy Market

- LivaNova

- Johnson & Johnson Services

- Eisai

- GlaxoSmithKline PLC

- Pfizer

- UCB SA

- Medtronic PLC (Ireland)

- NeuroPace

- Novartis AG

- GW Pharmaceuticals

- Abbott Laboratories

- Sanofi

- Sunovion Pharmaceuticals

- Bausch Health

- Takeda

Significant Epilepsy Industry Milestones

- 2019: Launch of a new generation of AEDs with improved tolerability profiles.

- 2020: Significant advancements in the development of responsive neurostimulation (RNS) devices for personalized seizure control.

- 2021: Increased focus on gene therapy research for specific genetic forms of epilepsy.

- 2022: Expansion of telehealth services for epilepsy patient monitoring and management.

- 2023: Strategic partnerships between pharmaceutical companies and AI firms to accelerate drug discovery.

- 2024: Introduction of novel biomarkers for earlier and more accurate epilepsy diagnosis.

Future Outlook for Epilepsy Market

The future outlook for the epilepsy market is exceptionally robust, driven by several growth catalysts. Continued innovation in targeted therapies, including gene and cell-based treatments, promises to address the unmet needs of patients with refractory epilepsy. The integration of artificial intelligence and machine learning in diagnostics and treatment personalization will further enhance patient outcomes and market efficiency. The expanding healthcare infrastructure and increasing disposable income in emerging economies will unlock new market potential. Strategic collaborations and partnerships among industry players will foster accelerated development and market penetration. The growing emphasis on improving the quality of life for epilepsy patients, coupled with supportive government initiatives and increasing public awareness, will collectively shape a dynamic and expanding global epilepsy market, projected to reach over 600 billion by the estimated year 2033.

epilepsy Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Neurology Centers

- 1.3. Home Care Settings

- 1.4. Ambulatory Surgical Centers

- 1.5. Others

-

2. Types

- 2.1. Partial/focal Seizure

- 2.2. Generalized Seizure

- 2.3. Myoclonus Misses

- 2.4. Negative Myoclonus

- 2.5. Eyelid Myoclonus

- 2.6. Laughter

- 2.7. Others

epilepsy Segmentation By Geography

- 1. CA

epilepsy Regional Market Share

Geographic Coverage of epilepsy

epilepsy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. epilepsy Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Neurology Centers

- 5.1.3. Home Care Settings

- 5.1.4. Ambulatory Surgical Centers

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Partial/focal Seizure

- 5.2.2. Generalized Seizure

- 5.2.3. Myoclonus Misses

- 5.2.4. Negative Myoclonus

- 5.2.5. Eyelid Myoclonus

- 5.2.6. Laughter

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 LivaNova

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Johnson & Johnson Services

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Eisai

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 GlaxoSmithKline PLC

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Pfizer

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 UCB SA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Medtronic PLC (Ireland)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 NeuroPace

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Novartis AG

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 GW Pharmaceuticals

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Abbott Laboratories

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Sanofi

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Sunovion Pharmaceuticals

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Bausch Health

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Takeda

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.1 LivaNova

List of Figures

- Figure 1: epilepsy Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: epilepsy Share (%) by Company 2025

List of Tables

- Table 1: epilepsy Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: epilepsy Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: epilepsy Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: epilepsy Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: epilepsy Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: epilepsy Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the epilepsy?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the epilepsy?

Key companies in the market include LivaNova, Johnson & Johnson Services, Eisai, GlaxoSmithKline PLC, Pfizer, UCB SA, Medtronic PLC (Ireland), NeuroPace, Novartis AG, GW Pharmaceuticals, Abbott Laboratories, Sanofi, Sunovion Pharmaceuticals, Bausch Health, Takeda.

3. What are the main segments of the epilepsy?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "epilepsy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the epilepsy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the epilepsy?

To stay informed about further developments, trends, and reports in the epilepsy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence