Key Insights

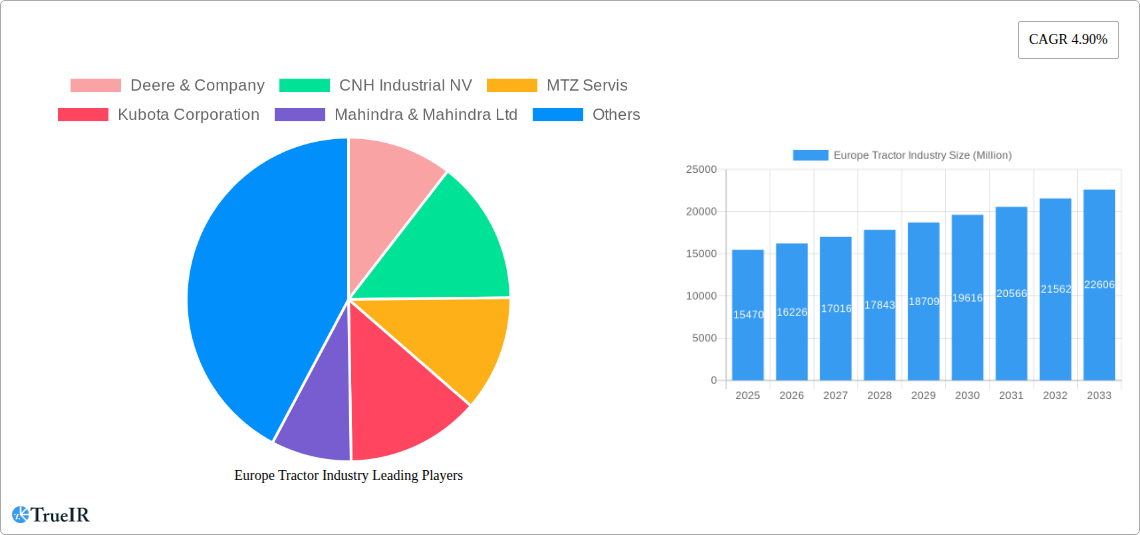

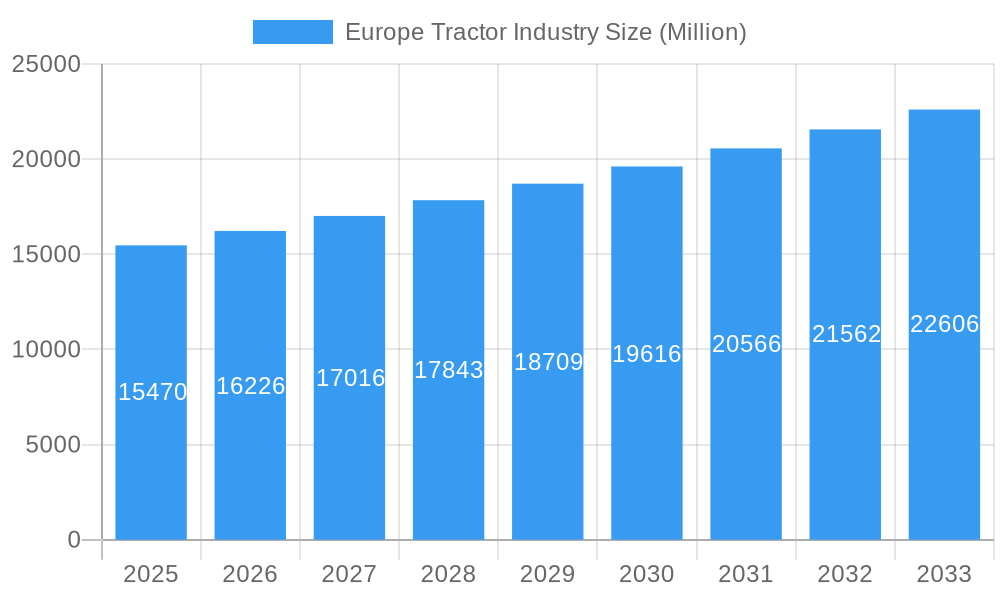

The European tractor market, valued at €15.47 billion in 2025, is projected to experience robust growth, driven by increasing agricultural mechanization needs and rising demand for high-horsepower tractors to enhance productivity. Factors such as favorable government policies promoting sustainable agriculture and technological advancements leading to improved fuel efficiency and precision farming capabilities further stimulate market expansion. The segment encompassing tractors with 100-200 HP is expected to dominate the market due to its versatility and suitability for large-scale farming operations prevalent across Europe. Key players like Deere & Company, CNH Industrial, and Kubota Corporation are actively investing in research and development to introduce innovative tractor models equipped with advanced features like GPS-guided systems and automated functionalities, thus catering to the growing demand for precision agriculture solutions. Competition within the market is intense, with established players facing challenges from both regional and global competitors. The market’s growth is, however, subject to fluctuations in agricultural commodity prices and potential economic downturns impacting farmer investments.

Europe Tractor Industry Market Size (In Billion)

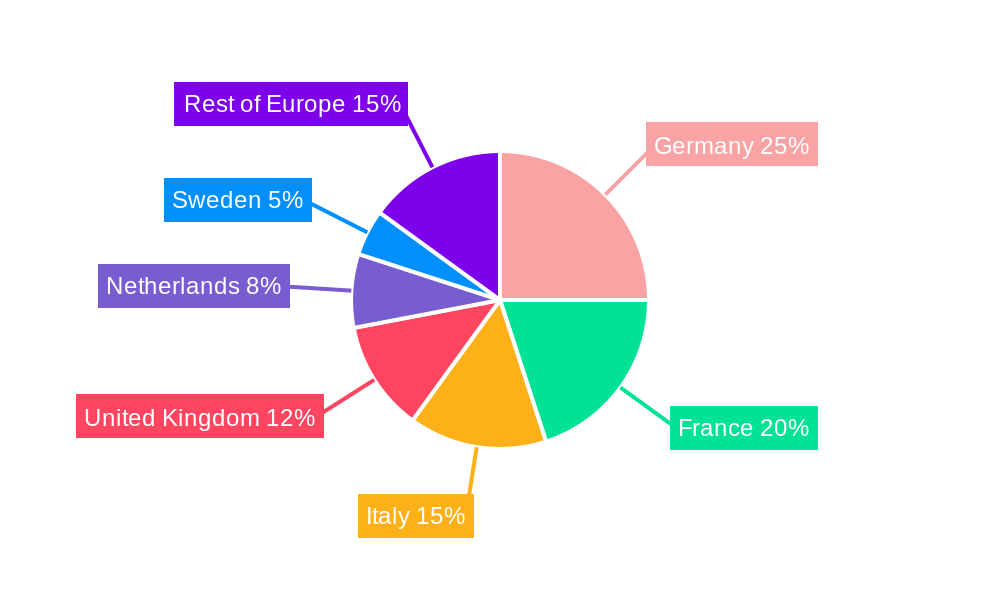

A regional analysis reveals significant variations across European markets. Germany, France, Italy, and the United Kingdom are expected to remain major contributors, driven by their extensive agricultural sectors and established dealer networks. The Rest of Europe region exhibits promising growth potential owing to the increasing adoption of mechanization in smaller farming operations. While the 4.90% CAGR indicates steady growth, the actual pace will be influenced by factors like climate change impacting crop yields, variations in fuel costs, and ongoing geopolitical instability. Future market success will depend on manufacturers' agility in adapting to evolving farmer needs, integrating technological advancements, and achieving sustainable manufacturing practices. The emphasis on efficient and sustainable agricultural practices will become increasingly crucial, shaping future demand for tractors and associated technologies in Europe.

Europe Tractor Industry Company Market Share

Europe Tractor Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe tractor industry, encompassing market size, segmentation, competitive landscape, key players, and future growth prospects. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. This report is essential for industry stakeholders, investors, and strategic decision-makers seeking to understand and capitalize on the opportunities within this dynamic market.

Europe Tractor Industry Market Structure & Competitive Landscape

The European tractor market is characterized by a moderately concentrated structure. The leading five global manufacturers, including Deere & Company, CNH Industrial NV, Kubota Corporation, Mahindra & Mahindra Ltd, and AGCO Corporation, are expected to collectively command a substantial market share, estimated at approximately XX% in 2025. This dominance is underpinned by significant advantages such as economies of scale, robust and expansive distribution networks, and deeply ingrained brand loyalty. Nonetheless, the market also provides fertile ground for smaller, specialized players who excel in niche segments, such as the production of smaller horsepower tractors tailored for specific horticultural or vineyard applications, or those focusing on highly specialized agricultural machinery.

Innovation serves as a critical differentiator and a primary engine for competitive advantage. Manufacturers are channeling substantial investments into the research and development of cutting-edge technologies, including sophisticated precision farming solutions, advancements in autonomous operation, and the continuous refinement of engine efficiency to meet evolving environmental standards. The regulatory landscape, particularly concerning emissions, with directives like Stage V and forthcoming stricter regulations, is a powerful catalyst for market transformation, compelling manufacturers to accelerate their adoption and development of cleaner, more sustainable technologies. Direct product substitution remains a limited factor, as tractors continue to be the indispensable primary power source for large-scale agricultural operations. The primary customer base comprises large-scale commercial farms and agricultural cooperatives, alongside a significant segment of smaller farms and individual landowners.

Mergers and acquisitions (M&A) have been a notable feature of the European tractor industry in recent years, with a strategic focus on consolidating market presence and broadening product offerings. The total value of M&A transactions within the European tractor industry between 2019 and 2024 is estimated to be in the region of XX Million USD. These strategic moves frequently involve forming key alliances and partnerships, enabling companies to synergize complementary technological capabilities and extend their market reach more effectively.

Europe Tractor Industry Market Trends & Opportunities

The European tractor market is projected to experience significant growth during the forecast period (2025-2033), with a Compound Annual Growth Rate (CAGR) estimated at xx%. This growth is fueled by several factors:

- Increased agricultural output: Rising global food demand drives the need for increased agricultural productivity, boosting tractor demand.

- Technological advancements: Precision farming technologies, automation, and connected machinery are enhancing efficiency and yield, making tractors more attractive investments.

- Favorable government policies: Subsidies and incentives for agricultural modernization in certain European countries are stimulating tractor adoption.

- Consolidation in the agricultural sector: Larger farms are increasingly adopting advanced machinery, including tractors, to optimize operations.

Market penetration of advanced technologies, such as GPS-guided systems and telematics, remains relatively low but is expected to increase significantly over the forecast period. Consumer preferences are shifting toward fuel-efficient, technologically advanced, and operator-friendly tractors. The competitive dynamics are characterized by intense competition based on innovation, pricing, and brand reputation.

Dominant Markets & Segments in Europe Tractor Industry

Germany, France, and Italy represent the largest tractor markets within Europe, accounting for an estimated xx% of total sales in 2025. Growth in these markets is driven by factors such as strong agricultural output, high levels of mechanization, and supportive government policies.

- Germany: Strong agricultural sector, high investment in technology, and well-developed infrastructure.

- France: Large agricultural land area and significant government support for agricultural modernization.

- Italy: Significant presence of specialized farming, demanding high-performance tractors.

In terms of horsepower segments, the 40-99 HP segment holds the largest market share in 2025, followed by the 100-150 HP segment. Growth in higher horsepower segments (151-200 HP and above 200 HP) is anticipated due to the increasing adoption of large-scale farming practices and the need for high-capacity tractors. The less than 40 HP segment, though smaller in size, is also seeing steady growth driven by small-scale farming and horticultural applications.

Europe Tractor Industry Product Analysis

The European tractor market presents a rich and varied product portfolio, spanning from compact utility tractors designed for versatile tasks to high-horsepower models equipped with the latest technological innovations. Key advancements are increasingly incorporating higher levels of automation, significant improvements in fuel efficiency, enhanced operator ergonomics for greater comfort and reduced fatigue, and sophisticated precision farming functionalities. Competition among manufacturers is fierce, centered on a combination of advanced technological features, unwavering durability, superior fuel economy, and compelling price-performance ratios. A pronounced trend is the seamless integration of precision agriculture technologies. This includes, but is not limited to, advanced GPS guidance systems for pinpoint accuracy, automated steering for reduced operator input, and integrated yield monitoring systems. These innovations collectively contribute to enhanced operational efficiency, optimized utilization of agricultural inputs, and ultimately, improved profitability for farming enterprises.

Key Drivers, Barriers & Challenges in Europe Tractor Industry

Key Drivers: Technological advancements, increasing agricultural productivity demands, favorable government policies, and consolidation within the agricultural sector are key drivers for growth. The increasing adoption of precision agriculture technologies offers significant growth opportunities. Economic growth and government support for agricultural development further stimulate market expansion.

Challenges: Supply chain disruptions (particularly regarding components and raw materials), stringent emission regulations, intense competition, and rising input costs pose significant challenges. Supply chain vulnerabilities, exacerbated by geopolitical events, have impacted production and increased manufacturing costs. Furthermore, the fluctuating prices of raw materials and energy add to the operational complexity faced by manufacturers.

Growth Drivers in the Europe Tractor Industry Market

Technological advancements, particularly in precision agriculture, are a major driver. Growing demand for food, government support for agricultural modernization, and the trend towards larger, more efficient farming operations also contribute significantly.

Challenges Impacting Europe Tractor Industry Growth

The industry faces a multifaceted landscape of challenges. The escalating stringency of environmental emission regulations necessitates continuous and substantial financial investment in the research, development, and implementation of cleaner, more sustainable technologies. Persistent supply chain vulnerabilities, especially concerning critical components, present ongoing obstacles to maintaining consistent production schedules and ensuring timely delivery to customers. Furthermore, intense competition, emanating from both established global players and agile new entrants, demands relentless innovation, aggressive cost optimization strategies, and a proactive approach to market adaptation.

Key Players Shaping the Europe Tractor Industry Market

Significant Europe Tractor Industry Industry Milestones

- July 2020: Deere & Company expanded its utility tractor line with the launch of the innovative 3D Series compact utility tractors.

- September 2020: AGCO's premium Fendt brand unveiled the robust Fendt 900 Vario MT Series, featuring advanced track tractor technology.

- December 2020: AGCO further strengthened its track tractor offerings with the introduction of the powerful Challenger MT800 Series.

- December 2021: SDF SpA and DEUTZ AG solidified their strategic alliance through an extended long-term agreement for the supply of advanced engines, ensuring continued technological collaboration.

Future Outlook for Europe Tractor Industry Market

The European tractor market is poised for continued growth, driven by technological advancements, increasing agricultural efficiency demands, and supportive government policies. Strategic partnerships, focus on sustainability, and innovative product offerings will be crucial for success in this competitive landscape. The market presents significant opportunities for companies capable of adapting to changing regulatory environments and leveraging technological advancements to enhance efficiency and productivity within the agricultural sector.

Europe Tractor Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Tractor Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Tractor Industry Regional Market Share

Geographic Coverage of Europe Tractor Industry

Europe Tractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization

- 3.3. Market Restrains

- 3.3.1. Heavy Initial Procurement Cost and High Expenditure on Maintenance

- 3.4. Market Trends

- 3.4.1. Rising Farm Labor Cost is Driving the Market for Tractors

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Tractor Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Deere & Company

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 CNH Industrial NV

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 MTZ Servis

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Kubota Corporation

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Mahindra & Mahindra Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Argo Tractors SpA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Claas KGaA mbH

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Tractors and Farm Equipment Limited

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 SDF SpA

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 AGCO Corporation

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Deere & Company

List of Figures

- Figure 1: Europe Tractor Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Tractor Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Tractor Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Tractor Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Tractor Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Tractor Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Tractor Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Tractor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Europe Tractor Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Tractor Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Tractor Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Tractor Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Tractor Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Tractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Tractor Industry?

The projected CAGR is approximately 4.90%.

2. Which companies are prominent players in the Europe Tractor Industry?

Key companies in the market include Deere & Company, CNH Industrial NV, MTZ Servis, Kubota Corporation, Mahindra & Mahindra Ltd, Argo Tractors SpA, Claas KGaA mbH, Tractors and Farm Equipment Limited, SDF SpA, AGCO Corporation.

3. What are the main segments of the Europe Tractor Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.47 Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Rising Farm Labor Cost is Driving the Market for Tractors.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

December 2021: A strategic partnership between SDF and DEUTZ was expanded. Both companies have a successful business partnership that began in the 1980s. The companies have reached an agreement for a long-term supply agreement to provide both the sub-4 and above-4 liter range engines and the DEUTZ TCD 4.1, 6.1, and 7.8 engines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Tractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Tractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Tractor Industry?

To stay informed about further developments, trends, and reports in the Europe Tractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence