Key Insights

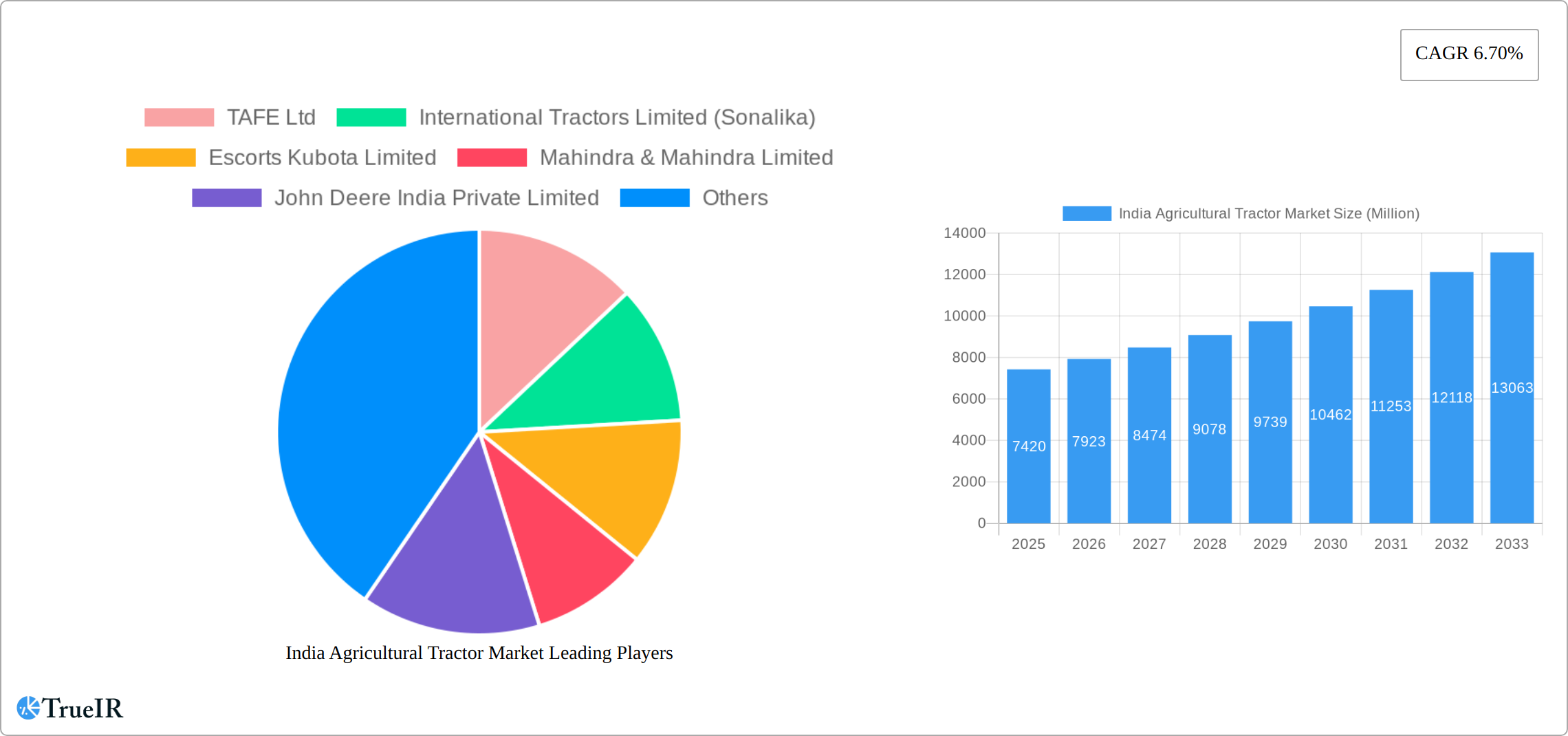

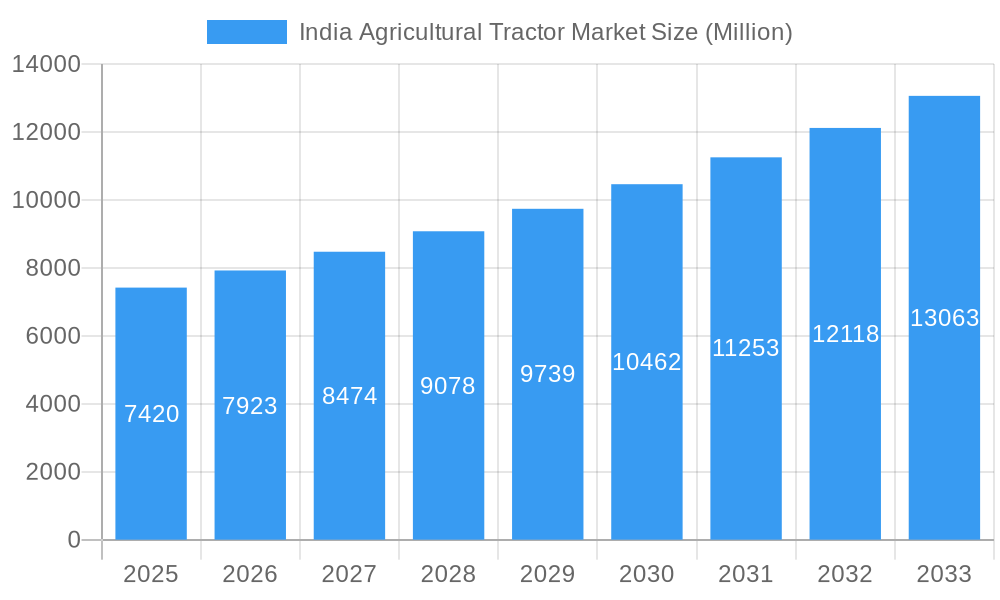

The India agricultural tractor market, valued at $7.42 billion in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 6.70% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, increasing government initiatives promoting mechanization in agriculture, coupled with favorable government policies aimed at boosting agricultural productivity, are significantly contributing to market growth. Secondly, rising farmer incomes and a growing awareness of the benefits of tractor usage—improved efficiency, reduced labor costs, and timely harvests—are driving adoption, particularly in regions like North and West India where large-scale farming is prevalent. Furthermore, technological advancements in tractor design, including features like enhanced fuel efficiency, improved power output, and advanced GPS-guided systems, are enhancing the appeal of modern tractors. The market segmentation reveals significant demand across various engine power categories, with the 31-50 HP and 51-80 HP segments particularly strong, reflecting the diverse needs of Indian farmers. The four-wheel-drive segment is also witnessing substantial growth due to its suitability for varied terrains and demanding agricultural practices. Leading players like TAFE, Mahindra & Mahindra, and John Deere are capitalizing on these trends through strategic product launches, expansion of their dealer networks, and investment in R&D to meet evolving farmer demands. However, the market faces challenges like high initial investment costs, limited access to credit for smaller farmers, and the need for enhanced farmer training and awareness to fully realize the benefits of tractor technology.

India Agricultural Tractor Market Market Size (In Billion)

Despite these challenges, the long-term outlook for the India agricultural tractor market remains positive. The ongoing expansion of the agricultural sector, coupled with the increasing adoption of precision farming techniques and the government's continued support for agricultural modernization, is expected to drive sustained market expansion over the forecast period. The competitive landscape is dynamic, with both domestic and international players vying for market share. This competitive environment is likely to further stimulate innovation and provide farmers with a wider range of choices and technologies, leading to further market growth and improved agricultural efficiency across India.

India Agricultural Tractor Market Company Market Share

This comprehensive report provides a detailed analysis of the India Agricultural Tractor Market, offering invaluable insights for industry stakeholders, investors, and researchers. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market trends, competitive dynamics, and future growth potential. The Indian agricultural tractor market is poised for significant expansion, driven by technological advancements, government initiatives, and evolving farming practices. This report unravels the complexities of this dynamic sector, providing actionable intelligence for strategic decision-making.

India Agricultural Tractor Market Market Structure & Competitive Landscape

The Indian agricultural tractor market is characterized by a dynamic and moderately concentrated structure, with a few dominant indigenous and international players leading the market, complemented by a robust ecosystem of smaller manufacturers and assemblers that foster intense competition. As of 2024, the market's concentration ratio (CR4) is estimated to be around xx%, indicating a consolidated yet fiercely competitive environment. A significant driver of this market is relentless innovation, with companies spearheading the introduction of technologically advanced tractors equipped with features such as GPS auto-steer, advanced telemetry for farm management, variable transmission systems, and enhanced fuel efficiency. Stringent government regulations, particularly concerning emission standards (Bharat Stage VI equivalent), safety protocols, and the promotion of farm mechanization, play a pivotal role in shaping market dynamics and R&D investments. While tractors remain indispensable for large-scale agricultural operations, emerging technologies like autonomous drones for precision spraying and seeding, and advanced robotic harvesters are beginning to present themselves as potential complements rather than direct substitutes in specific niche applications. The end-user segment is a broad spectrum, predominantly comprising small and marginal farmers who form the backbone of Indian agriculture, alongside medium-sized holdings and large commercial agribusinesses. Mergers and acquisitions (M&A) activity within the sector, while not overwhelmingly frequent, has seen strategic consolidations and partnerships. Approximately xx major mergers and acquisitions were recorded between 2019 and 2024, reflecting a trend towards leveraging synergies, expanding product portfolios, and strengthening market reach.

- Market Concentration: CR4 (2024) estimated at xx%, highlighting a blend of market leadership and diverse participation.

- Innovation Drivers: Focus on electrification, smart farming integration, AI-powered analytics, telematics, and precision agriculture technologies.

- Regulatory Impacts: Evolving emission norms, enhanced safety mandates, government subsidies and financing schemes (e.g., mechanization schemes), and policies promoting sustainable agriculture.

- Product Substitutes: While direct substitutes are limited for core tractor functions, advanced agricultural machinery like specialized harvesters and automated planting systems, alongside the growing adoption of drones for specific tasks, are influencing the market.

- End-User Segmentation: Predominantly smallholder farmers (owning <2 hectares), followed by medium-scale farmers (2-10 hectares), and progressively larger commercial agricultural enterprises.

- M&A Trends: xx significant transactions between 2019 and 2024, driven by strategic acquisitions for technology integration, market expansion, and brand consolidation.

India Agricultural Tractor Market Market Trends & Opportunities

The India agricultural tractor market exhibits robust growth, with a Compound Annual Growth Rate (CAGR) of xx% projected from 2025 to 2033. This growth is fueled by increasing mechanization in agriculture, government support for farmers through subsidies and credit facilities, and rising disposable incomes in rural areas. Technological shifts towards advanced features like GPS-guided tractors, auto-steer capabilities, and precision farming tools are transforming the market. Consumer preferences are shifting towards fuel-efficient, high-performing tractors with enhanced comfort and safety features. The competitive landscape is dynamic, with established players and new entrants vying for market share. Market penetration rates vary significantly across regions, with higher adoption in states with favorable agricultural conditions and better infrastructure. The government's initiatives to promote agricultural mechanization and its focus on improving rural infrastructure are creating significant opportunities for market expansion. The increasing adoption of precision farming techniques is also creating demand for sophisticated tractor technology. Overall, the market's growth trajectory is positive and promising.

Dominant Markets & Segments in India Agricultural Tractor Market

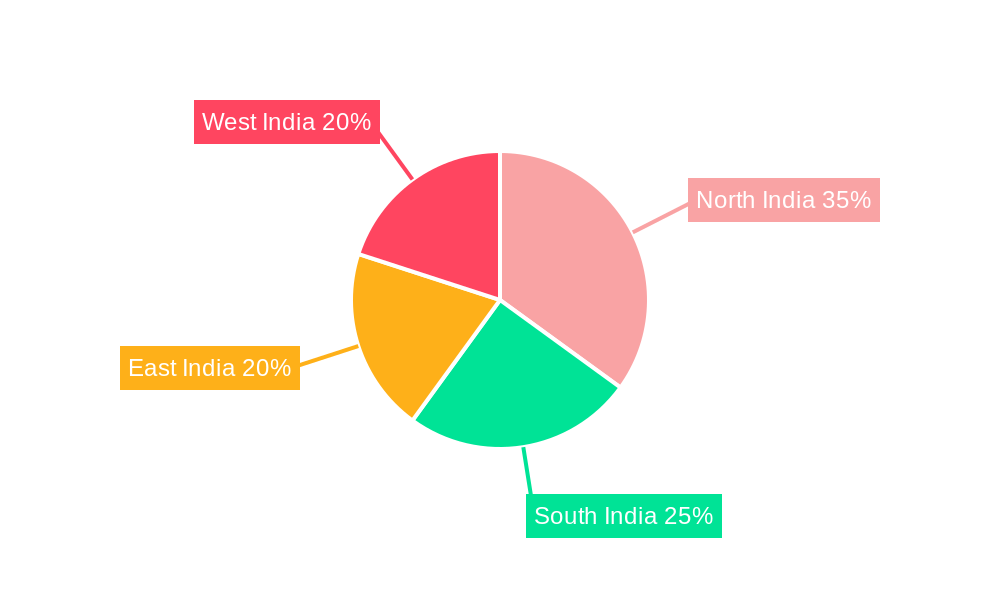

The Indian agricultural tractor market exhibits significant geographical and segment-wise variations, with states like Punjab, Haryana, Uttar Pradesh, Madhya Pradesh, and Rajasthan consistently leading in terms of sales volume and demand. These regions are characterized by their strong agrarian economies, favorable cropping patterns, higher disposable incomes among farmers, robust irrigation infrastructure, and a greater prevalence of medium to large farm holdings. In terms of engine power, the 51-80 HP segment continues to dominate the market share, catering to the diverse operational needs of a vast majority of Indian farmers for tasks ranging from plowing and tilling to harvesting. However, there is a discernible and growing demand for both lower HP tractors (below 40 HP) for small landholdings and higher HP tractors (above 80 HP) for large-scale commercial farming and specialized applications. The adoption of four-wheel-drive (4WD) tractors is rapidly increasing, particularly in regions with challenging soil conditions, undulating terrain, and for heavier draft work, offering enhanced traction and stability. While row crop tractors remain the workhorse due to their versatility across multiple crops and farming practices, there's a burgeoning interest in specialized tractors such as horticultural tractors, vineyard tractors, and compact tractors designed for specific niche applications and smaller land parcels.

- Leading Regions: Punjab, Haryana, Uttar Pradesh, Madhya Pradesh, Rajasthan, and Gujarat are key demand centers.

- Dominant Engine Power Segment: 51-80 HP remains the largest segment, with growing contributions from <40 HP and >80 HP categories.

- Leading Drive Type: Four-wheel drive (4WD) tractors are experiencing significant market penetration and growth.

- Primary Application: Row crop tractors are the most prevalent, but demand for specialized tractors for horticulture and vineyard operations is rising.

- Key Growth Drivers:

- Continued government impetus on farm mechanization and subsidies.

- Expansion and modernization of agricultural infrastructure, including irrigation and storage.

- Increasing farmer awareness and adoption of advanced farming techniques.

- Improved access to rural credit and flexible financing schemes.

- Rising rural disposable incomes and aspirations for modern farm equipment.

- The increasing need for fuel-efficient and low-maintenance tractors.

India Agricultural Tractor Market Product Analysis

The Indian agricultural tractor market is a vibrant arena of product evolution, driven by a clear mandate for manufacturers to deliver enhanced value to farmers. Key product development initiatives are centered around optimizing fuel efficiency through advanced engine technologies and lighter materials, boosting operational performance with improved power-to-weight ratios and transmission systems, and integrating cutting-edge technologies for greater precision and automation. Tractors equipped with advanced GPS guidance systems, sophisticated auto-steer functionalities, telematics for real-time farm management data, and integrated precision planting or spraying modules are no longer niche offerings but are becoming increasingly sought after. These features collectively contribute to significant reductions in input costs (fertilizers, pesticides, fuel), minimize labor requirements, and substantially enhance overall farm productivity and crop yields. The market is also witnessing a growing demand for a wider array of specialized tractors tailored for specific agricultural needs, including compact tractors for orchards and vineyards, high-clearance tractors for plantation crops, and tractors designed for specialized tasks like paddy transplantation. Manufacturers are actively focusing on developing products that address the diverse requirements of Indian farmers, taking into account varying landholding sizes, the specific types of crops cultivated, soil characteristics, and the prevailing climatic conditions, thereby ensuring relevance and broad market appeal.

Key Drivers, Barriers & Challenges in India Agricultural Tractor Market

Key Drivers: Government policies promoting agricultural mechanization, rising disposable incomes in rural areas, favorable climatic conditions in many parts of the country, and technological advancements leading to improved tractor efficiency and performance.

Challenges: High initial investment costs for farmers, limited access to credit and financing in certain regions, inconsistent infrastructure (especially in remote areas), dependence on monsoon rainfall (vulnerability to drought), and intense competition among manufacturers. The impact of these challenges can be quantified through reduced market penetration in certain segments and geographical areas.

Growth Drivers in the India Agricultural Tractor Market Market

Technological advancements in tractor design and manufacturing, including features like auto-steer and precision farming technologies, are significantly driving market growth. Government initiatives such as subsidies and credit schemes aimed at promoting farm mechanization also contribute. Additionally, a rising trend of consolidation within the agricultural sector, with larger farms adopting more advanced machinery, fuels demand.

Challenges Impacting India Agricultural Tractor Market Growth

The India Agricultural Tractor Market, while robust, navigates a landscape fraught with several persistent challenges. Volatile input costs, particularly for steel, rubber, and other essential manufacturing components, coupled with fluctuating diesel prices, create significant unpredictability for both manufacturers and end-users, impacting pricing strategies and farmer affordability. Fragmented landholdings, inconsistent monsoon patterns, and unpredictable agricultural policies can lead to fluctuations in farmer demand and investment capacity. Supply chain vulnerabilities and logistical bottlenecks, especially in remote rural areas, continue to impede efficient distribution networks and timely after-sales service. Furthermore, the market is characterized by fierce price competition among a large number of manufacturers, which often leads to margin pressures and necessitates continuous investment in cost-effective innovation to maintain competitive pricing and differentiation. Limited access to affordable credit for small and marginal farmers remains a significant barrier to adoption of higher-priced, technologically advanced tractors.

Key Players Shaping the India Agricultural Tractor Market Market

- TAFE Ltd

- International Tractors Limited (Sonalika)

- Escorts Kubota Limited

- Mahindra & Mahindra Limited

- John Deere India Private Limited

- Indo Farm Equipment Limited

- Captain Tractors Private Limited

- CNH Industrial (India) Pvt Ltd

- VST Tillers Tractors Limited

- Preet Tractors (P) Limited

Significant India Agricultural Tractor Market Industry Milestones

- January 2024: Tractors and Farm Equipment Limited (TAFE) showcased its range of electric tractors at the Tamil Nadu Global Investors Meet (TN GIM) 2024, signaling a strong commitment to sustainable and emission-free agricultural solutions.

- March 2024: Sonalika International Tractors Ltd. announced a substantial investment of USD 157.4 Million towards establishing two new state-of-the-art manufacturing plants in Punjab, a move aimed at significantly bolstering its production capacity and reinforcing its market leadership.

- April 2024: Swaraj Tractors, a subsidiary of Mahindra & Mahindra, celebrated its 50th anniversary by launching a special limited-edition series comprising five distinct tractor variants, effectively leveraging brand legacy and celebrity endorsements to enhance market visibility and farmer engagement.

- May 2024: Mahindra & Mahindra unveiled its new range of 'Yuvo Tech Plus' tractors, emphasizing enhanced performance, fuel efficiency, and advanced features, targeting the discerning needs of Indian farmers in the mid-range HP segment.

- June 2024: Escorts Kubota Limited announced a strategic partnership with an Italian firm to explore the development and manufacturing of advanced agricultural implements, aiming to broaden its product portfolio and offer integrated farming solutions.

Future Outlook for India Agricultural Tractor Market Market

The Indian agricultural tractor market is projected to experience continued robust growth, driven by technological advancements, government support, and a growing demand for efficient and technologically advanced farming equipment. The market presents significant opportunities for players who can adapt to evolving consumer preferences, leverage technological innovation, and effectively address the challenges associated with rural infrastructure and access to credit. The increasing adoption of precision farming techniques and the potential for further government investments in agricultural infrastructure are expected to further accelerate market growth.

India Agricultural Tractor Market Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

India Agricultural Tractor Market Segmentation By Geography

- 1. India

India Agricultural Tractor Market Regional Market Share

Geographic Coverage of India Agricultural Tractor Market

India Agricultural Tractor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Mechanization Trend in Agriculture Sector; Trend of Custom Hiring of Tractors

- 3.3. Market Restrains

- 3.3.1. Lack of Awareness and Skilled Manpower; Poor Economic Condition of Farmers

- 3.4. Market Trends

- 3.4.1. 30-50 HP Tractors Are Widely Preferred

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Agricultural Tractor Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. India

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 TAFE Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 International Tractors Limited (Sonalika)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Escorts Kubota Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Mahindra & Mahindra Limited

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 John Deere India Private Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Indo Farm Equipment Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Captain Tractors Private Limited*List Not Exhaustive

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 CNH Industrial (India) Pvt Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 VST Tillers Tractors Limited

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Preet Tractors (P) Limited

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 TAFE Ltd

List of Figures

- Figure 1: India Agricultural Tractor Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Agricultural Tractor Market Share (%) by Company 2025

List of Tables

- Table 1: India Agricultural Tractor Market Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: India Agricultural Tractor Market Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: India Agricultural Tractor Market Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: India Agricultural Tractor Market Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: India Agricultural Tractor Market Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: India Agricultural Tractor Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: India Agricultural Tractor Market Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: India Agricultural Tractor Market Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: India Agricultural Tractor Market Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: India Agricultural Tractor Market Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: India Agricultural Tractor Market Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: India Agricultural Tractor Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Agricultural Tractor Market?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the India Agricultural Tractor Market?

Key companies in the market include TAFE Ltd, International Tractors Limited (Sonalika), Escorts Kubota Limited, Mahindra & Mahindra Limited, John Deere India Private Limited, Indo Farm Equipment Limited, Captain Tractors Private Limited*List Not Exhaustive, CNH Industrial (India) Pvt Ltd, VST Tillers Tractors Limited, Preet Tractors (P) Limited.

3. What are the main segments of the India Agricultural Tractor Market?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.42 Million as of 2022.

5. What are some drivers contributing to market growth?

Mechanization Trend in Agriculture Sector; Trend of Custom Hiring of Tractors.

6. What are the notable trends driving market growth?

30-50 HP Tractors Are Widely Preferred.

7. Are there any restraints impacting market growth?

Lack of Awareness and Skilled Manpower; Poor Economic Condition of Farmers.

8. Can you provide examples of recent developments in the market?

April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, has MS Dhoni's signature as a symbol of gratitude to the customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Agricultural Tractor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Agricultural Tractor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Agricultural Tractor Market?

To stay informed about further developments, trends, and reports in the India Agricultural Tractor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence