Key Insights

The North American agricultural equipment market, valued at approximately $115.58 billion in 2025, is poised for significant expansion. Growth is propelled by the increasing demand for advanced farming solutions and the widespread adoption of precision agriculture techniques. Supportive government initiatives promoting agricultural modernization and substantial investments in irrigation and harvesting technologies further bolster market growth. The market is segmented by equipment type, including 4WD farm tractors, irrigation, harvesting, haying and forage machinery, and others, as well as by tractor type. Key industry leaders like Deere & Company, Kubota Corporation, and AGCO Corporation are driving innovation through R&D investments, integrating advanced features such as GPS guidance and automation to meet evolving farmer needs. Market dynamics are also influenced by fluctuating commodity prices, climate change impacts on crop yields, and agricultural labor shortages, underscoring the necessity for enhanced automation and efficiency.

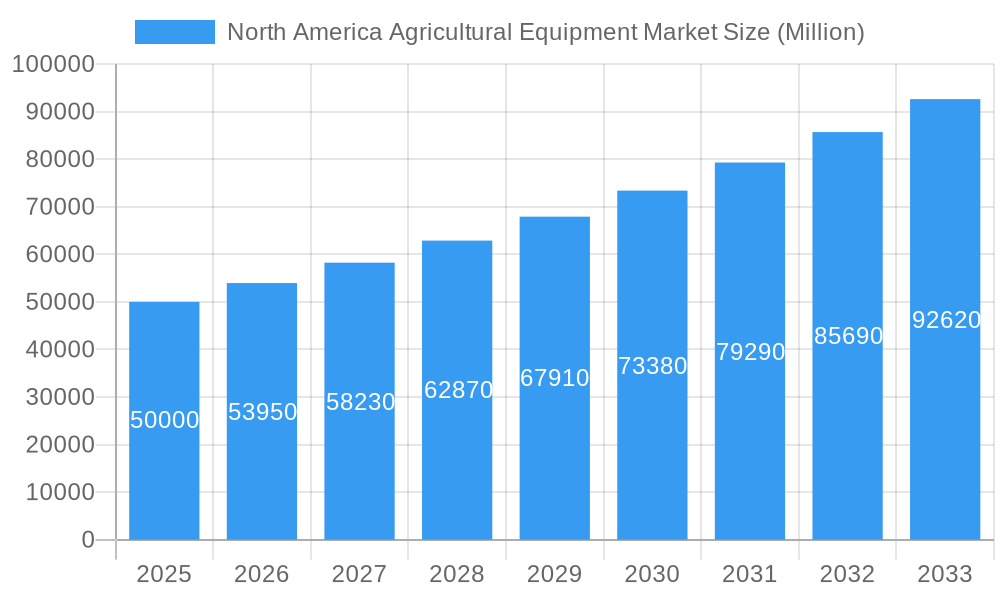

North America Agricultural Equipment Market Market Size (In Billion)

A projected Compound Annual Growth Rate (CAGR) of 4.1% from 2025 to 2033 indicates substantial market growth. Potential market restraints include the inherent cyclicality of agricultural commodity markets, affecting farmer investment decisions, and the high initial cost of sophisticated equipment, which may pose challenges for smaller agricultural operations. However, the availability of flexible financing options, leasing programs, and government subsidies are helping to alleviate these barriers. The ongoing integration of precision agriculture and a growing emphasis on sustainable farming practices are expected to fuel considerable growth in the North American agricultural equipment sector. Regional agricultural practices and climate variations across North America will also shape the market landscape.

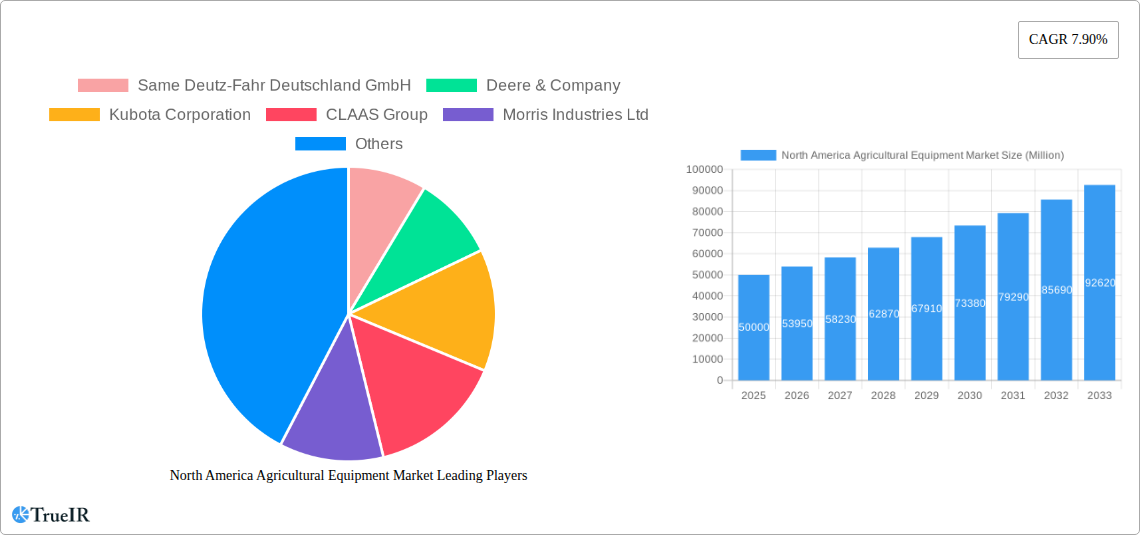

North America Agricultural Equipment Market Company Market Share

This report delivers a comprehensive analysis of the North American agricultural equipment market, providing critical insights for stakeholders, investors, and researchers. Covering the period from 2019 to 2033, with a detailed focus on 2025, this analysis meticulously examines market size, segmentation, competitive landscapes, and future growth trajectories. Optimized with high-impact keywords for enhanced search engine visibility.

North America Agricultural Equipment Market Market Structure & Competitive Landscape

The North American agricultural equipment market is characterized by a moderately concentrated structure, with a few major players holding significant market share. The Herfindahl-Hirschman Index (HHI) for 2024 is estimated at xx, indicating a moderately concentrated market. Innovation is a key driver, with companies continually investing in advanced technologies like automation and precision farming. Regulatory changes, particularly those related to environmental protection and safety standards, significantly impact market dynamics. Product substitutes, such as alternative farming practices, exert limited pressure currently, but their influence is expected to increase over the forecast period.

The market is segmented by end-users, primarily large-scale commercial farms, smaller family-owned farms, and specialized agricultural operations (e.g., vineyards, orchards). Mergers and acquisitions (M&A) activity has been significant, with xx major deals recorded between 2019 and 2024. These acquisitions primarily focused on enhancing technological capabilities and expanding market reach. For example, AGCO's acquisition of JCA Industries in May 2022 aimed to accelerate the development of autonomous machines. The increasing adoption of precision farming technologies is driving consolidation within the market as larger companies seek to acquire smaller, specialized technology firms.

- Market Concentration: Moderately concentrated, HHI (2024) estimated at xx.

- Innovation Drivers: Automation, precision farming, data analytics.

- Regulatory Impacts: Environmental regulations, safety standards.

- Product Substitutes: Limited currently, but growing potential for alternative farming methods.

- End-User Segmentation: Large-scale farms, small farms, specialized operations.

- M&A Trends: Significant activity focused on technology acquisition and market expansion, with xx major deals from 2019-2024.

North America Agricultural Equipment Market Market Trends & Opportunities

The North American agricultural equipment market is experiencing robust growth, driven by several key factors. The market size is projected to reach xx Million by 2025 and is expected to exhibit a compound annual growth rate (CAGR) of xx% from 2025 to 2033. Technological advancements, particularly in automation, precision farming, and data analytics, are transforming the industry. Farmers are increasingly adopting these technologies to enhance productivity, efficiency, and sustainability. Consumer preferences are shifting towards sustainably produced food, driving demand for equipment that minimizes environmental impact.

Intense competition among established players and the emergence of new entrants are shaping market dynamics. Companies are focusing on developing innovative solutions that meet the evolving needs of farmers, while also managing operational costs and supply chain challenges. The market penetration rate of precision farming technologies is increasing steadily, with xx% of farms in North America expected to adopt these technologies by 2033. Opportunities exist for companies that can offer integrated solutions, combining hardware, software, and data services. Further growth will be driven by the increasing adoption of IoT based technologies for improved efficiency and precision. Government initiatives and subsidies promoting sustainable agriculture will further accelerate growth in the coming decade.

Dominant Markets & Segments in North America Agricultural Equipment Market

The North American agricultural equipment market exhibits strong regional variations. The Midwest region of the U.S. and the Prairie provinces of Canada represent the most dominant markets due to their extensive agricultural land and high crop production. Within the market segments, 4WD farm tractors represent the largest segment, followed by other equipment categories like irrigation machinery and harvesting machinery.

- Key Growth Drivers:

- Midwest US & Prairie Canada: Large agricultural land areas, high crop production.

- Technological Advancements: Automation, precision farming, data analytics.

- Government Policies: Subsidies, support for sustainable agriculture.

The dominance of 4WD farm tractors stems from their versatility and suitability for large-scale farming operations. The increasing demand for efficient irrigation systems contributes to the growth of the irrigation machinery segment. Advancements in harvesting technologies, including autonomous harvesters, are driving growth within the harvesting machinery segment. The hay and forage machinery segment benefits from increased livestock farming and the need for efficient feed production. The ‘Other Types’ segment reflects the diverse array of specialized equipment used in agriculture. The tractor segment continues to be a cornerstone of the industry given its versatility and adaptability to a variety of farming applications.

North America Agricultural Equipment Market Product Analysis

The agricultural equipment market is witnessing significant product innovations, with a focus on automation, precision, and data-driven technologies. Products like driverless tractors, autonomous sprayers, and precision seeding equipment are enhancing efficiency and reducing operational costs. These advancements address key challenges faced by farmers, such as labor shortages, increasing input costs, and the need for sustainable farming practices. The competitive advantage lies in offering integrated solutions that combine advanced hardware with intelligent software and data analytics capabilities, providing farmers with real-time insights to optimize their operations.

Key Drivers, Barriers & Challenges in North America Agricultural Equipment Market

Key Drivers:

- Technological advancements: Automation, precision farming, GPS technology, AI/ML, and IoT devices drive productivity, efficiency, and sustainability.

- Rising labor costs: Automation reduces reliance on manual labor, lowering operating expenses.

- Increasing demand for food: Growing global population fuels agricultural output needs, boosting demand.

Key Challenges and Restraints:

- Supply chain disruptions: Component shortages and logistical issues impact production and lead times. Estimated impact on market growth in 2024: xx%.

- High equipment costs: The price point for many advanced technologies can be prohibitive for smaller farms.

- Regulatory uncertainty: Evolving environmental regulations and safety standards may impact the viability of some products.

Growth Drivers in the North America Agricultural Equipment Market Market

The market's growth is primarily fueled by technological advancements in automation, precision farming, and data analytics. These enhancements boost efficiency and output, while addressing labor shortages and promoting sustainable practices. Economic factors, such as the rising global demand for food and the increasing cost of labor, also stimulate market growth. Supportive government policies, including subsidies and incentives promoting technological adoption and sustainable agriculture, further contribute to market expansion.

Challenges Impacting North America Agricultural Equipment Market Growth

The market faces significant challenges, primarily supply chain disruptions leading to production delays and increased costs (estimated impact on market growth in 2024: xx%). Regulatory complexities and compliance requirements also present obstacles. The high initial cost of advanced technologies poses a barrier to entry for smaller farms. Furthermore, intense competition among established players and the emergence of new entrants create a dynamic and often challenging environment for businesses.

Key Players Shaping the North America Agricultural Equipment Market Market

- Same Deutz-Fahr Deutschland GmbH

- Deere & Company

- Kubota Corporation

- CLAAS Group

- Morris Industries Ltd

- AGCO Corporation

- CNH Industrial NV

- Kverneland Group

- Vaderstad Industries Inc

- Netafim Irrigation Inc

Significant North America Agricultural Equipment Market Industry Milestones

- August 2021: John Deere introduced the new 6155MH Tractor, enhancing its M Series offerings in California and Arizona.

- April 2022: Deere & Company and GUSS Automation formed a joint venture, advancing semi-autonomous spraying technology.

- May 2022: AGCO acquired JCA Industries to boost automation capabilities.

- October 2022: Kubota Canada Ltd opened a new corporate headquarters and distribution facility.

- November 2022: Kubota Canada Ltd unveiled the M7-4 diesel tractor at Agri-Trade Equipment Expo.

- December 2022: CNH Industrial launched new Automation and Autonomy Solutions, including driverless tillage and harvest assist technologies.

Future Outlook for North America Agricultural Equipment Market Market

The North American agricultural equipment market is poised for continued growth, driven by technological innovations, increasing food demand, and supportive government policies. Opportunities exist for companies that can provide integrated solutions combining advanced machinery with data-driven services. The focus on sustainable agriculture and the adoption of precision farming techniques will shape future market trends. The market's expansion will be influenced by advancements in automation and artificial intelligence, resulting in increased efficiency and productivity within agricultural operations. The ongoing evolution of technologies promises significant advancements throughout the forecast period.

North America Agricultural Equipment Market Segmentation

-

1. Type

-

1.1. Tractor

- 1.1.1. Less than 40 HP

- 1.1.2. 40 to 100 HP

- 1.1.3. Above 100 HP

- 1.1.4. 4 WD Farm Tractors

-

1.2. Equipment

- 1.2.1. Plows

- 1.2.2. Harrows

- 1.2.3. Cultivators and Tillers

- 1.2.4. Other Equipment

-

1.3. Irrigation Machinery

- 1.3.1. Sprinkler Irrigation

- 1.3.2. Drip Irrigation

- 1.3.3. Other Irrigation Machinery

-

1.4. Harvesting Machinery

- 1.4.1. Combine Harvesters

- 1.4.2. Forage Harvesters

- 1.4.3. Other Harvesting Machinery

-

1.5. Haying and Forage Machinery

- 1.5.1. Mowers

- 1.5.2. Balers

- 1.5.3. Other Haying and Forage Machinery

- 1.6. Other Types

-

1.1. Tractor

-

2. Geography

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

- 2.4. Rest of North America

-

3. Type

-

3.1. Tractor

- 3.1.1. Less than 40 HP

- 3.1.2. 40 to 100 HP

- 3.1.3. Above 100 HP

- 3.1.4. 4 WD Farm Tractors

-

3.2. Equipment

- 3.2.1. Plows

- 3.2.2. Harrows

- 3.2.3. Cultivators and Tillers

- 3.2.4. Other Equipment

-

3.3. Irrigation Machinery

- 3.3.1. Sprinkler Irrigation

- 3.3.2. Drip Irrigation

- 3.3.3. Other Irrigation Machinery

-

3.4. Harvesting Machinery

- 3.4.1. Combine Harvesters

- 3.4.2. Forage Harvesters

- 3.4.3. Other Harvesting Machinery

-

3.5. Haying and Forage Machinery

- 3.5.1. Mowers

- 3.5.2. Balers

- 3.5.3. Other Haying and Forage Machinery

- 3.6. Other Types

-

3.1. Tractor

North America Agricultural Equipment Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

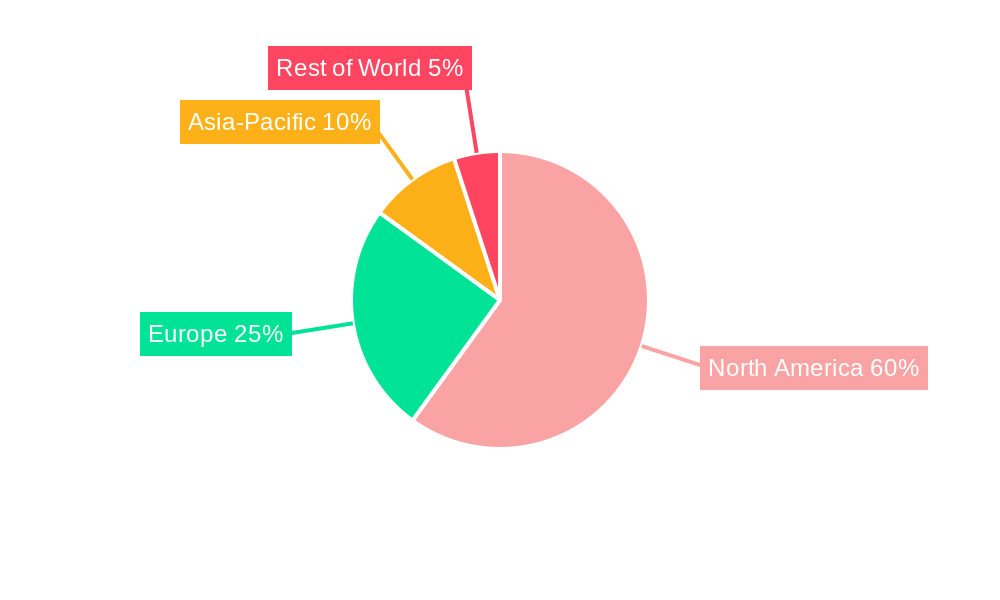

North America Agricultural Equipment Market Regional Market Share

Geographic Coverage of North America Agricultural Equipment Market

North America Agricultural Equipment Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Tractor

- 5.1.1.1. Less than 40 HP

- 5.1.1.2. 40 to 100 HP

- 5.1.1.3. Above 100 HP

- 5.1.1.4. 4 WD Farm Tractors

- 5.1.2. Equipment

- 5.1.2.1. Plows

- 5.1.2.2. Harrows

- 5.1.2.3. Cultivators and Tillers

- 5.1.2.4. Other Equipment

- 5.1.3. Irrigation Machinery

- 5.1.3.1. Sprinkler Irrigation

- 5.1.3.2. Drip Irrigation

- 5.1.3.3. Other Irrigation Machinery

- 5.1.4. Harvesting Machinery

- 5.1.4.1. Combine Harvesters

- 5.1.4.2. Forage Harvesters

- 5.1.4.3. Other Harvesting Machinery

- 5.1.5. Haying and Forage Machinery

- 5.1.5.1. Mowers

- 5.1.5.2. Balers

- 5.1.5.3. Other Haying and Forage Machinery

- 5.1.6. Other Types

- 5.1.1. Tractor

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United States

- 5.2.2. Canada

- 5.2.3. Mexico

- 5.2.4. Rest of North America

- 5.3. Market Analysis, Insights and Forecast - by Type

- 5.3.1. Tractor

- 5.3.1.1. Less than 40 HP

- 5.3.1.2. 40 to 100 HP

- 5.3.1.3. Above 100 HP

- 5.3.1.4. 4 WD Farm Tractors

- 5.3.2. Equipment

- 5.3.2.1. Plows

- 5.3.2.2. Harrows

- 5.3.2.3. Cultivators and Tillers

- 5.3.2.4. Other Equipment

- 5.3.3. Irrigation Machinery

- 5.3.3.1. Sprinkler Irrigation

- 5.3.3.2. Drip Irrigation

- 5.3.3.3. Other Irrigation Machinery

- 5.3.4. Harvesting Machinery

- 5.3.4.1. Combine Harvesters

- 5.3.4.2. Forage Harvesters

- 5.3.4.3. Other Harvesting Machinery

- 5.3.5. Haying and Forage Machinery

- 5.3.5.1. Mowers

- 5.3.5.2. Balers

- 5.3.5.3. Other Haying and Forage Machinery

- 5.3.6. Other Types

- 5.3.1. Tractor

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Agricultural Equipment Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Tractor

- 6.1.1.1. Less than 40 HP

- 6.1.1.2. 40 to 100 HP

- 6.1.1.3. Above 100 HP

- 6.1.1.4. 4 WD Farm Tractors

- 6.1.2. Equipment

- 6.1.2.1. Plows

- 6.1.2.2. Harrows

- 6.1.2.3. Cultivators and Tillers

- 6.1.2.4. Other Equipment

- 6.1.3. Irrigation Machinery

- 6.1.3.1. Sprinkler Irrigation

- 6.1.3.2. Drip Irrigation

- 6.1.3.3. Other Irrigation Machinery

- 6.1.4. Harvesting Machinery

- 6.1.4.1. Combine Harvesters

- 6.1.4.2. Forage Harvesters

- 6.1.4.3. Other Harvesting Machinery

- 6.1.5. Haying and Forage Machinery

- 6.1.5.1. Mowers

- 6.1.5.2. Balers

- 6.1.5.3. Other Haying and Forage Machinery

- 6.1.6. Other Types

- 6.1.1. Tractor

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United States

- 6.2.2. Canada

- 6.2.3. Mexico

- 6.2.4. Rest of North America

- 6.3. Market Analysis, Insights and Forecast - by Type

- 6.3.1. Tractor

- 6.3.1.1. Less than 40 HP

- 6.3.1.2. 40 to 100 HP

- 6.3.1.3. Above 100 HP

- 6.3.1.4. 4 WD Farm Tractors

- 6.3.2. Equipment

- 6.3.2.1. Plows

- 6.3.2.2. Harrows

- 6.3.2.3. Cultivators and Tillers

- 6.3.2.4. Other Equipment

- 6.3.3. Irrigation Machinery

- 6.3.3.1. Sprinkler Irrigation

- 6.3.3.2. Drip Irrigation

- 6.3.3.3. Other Irrigation Machinery

- 6.3.4. Harvesting Machinery

- 6.3.4.1. Combine Harvesters

- 6.3.4.2. Forage Harvesters

- 6.3.4.3. Other Harvesting Machinery

- 6.3.5. Haying and Forage Machinery

- 6.3.5.1. Mowers

- 6.3.5.2. Balers

- 6.3.5.3. Other Haying and Forage Machinery

- 6.3.6. Other Types

- 6.3.1. Tractor

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United States North America Agricultural Equipment Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Tractor

- 7.1.1.1. Less than 40 HP

- 7.1.1.2. 40 to 100 HP

- 7.1.1.3. Above 100 HP

- 7.1.1.4. 4 WD Farm Tractors

- 7.1.2. Equipment

- 7.1.2.1. Plows

- 7.1.2.2. Harrows

- 7.1.2.3. Cultivators and Tillers

- 7.1.2.4. Other Equipment

- 7.1.3. Irrigation Machinery

- 7.1.3.1. Sprinkler Irrigation

- 7.1.3.2. Drip Irrigation

- 7.1.3.3. Other Irrigation Machinery

- 7.1.4. Harvesting Machinery

- 7.1.4.1. Combine Harvesters

- 7.1.4.2. Forage Harvesters

- 7.1.4.3. Other Harvesting Machinery

- 7.1.5. Haying and Forage Machinery

- 7.1.5.1. Mowers

- 7.1.5.2. Balers

- 7.1.5.3. Other Haying and Forage Machinery

- 7.1.6. Other Types

- 7.1.1. Tractor

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United States

- 7.2.2. Canada

- 7.2.3. Mexico

- 7.2.4. Rest of North America

- 7.3. Market Analysis, Insights and Forecast - by Type

- 7.3.1. Tractor

- 7.3.1.1. Less than 40 HP

- 7.3.1.2. 40 to 100 HP

- 7.3.1.3. Above 100 HP

- 7.3.1.4. 4 WD Farm Tractors

- 7.3.2. Equipment

- 7.3.2.1. Plows

- 7.3.2.2. Harrows

- 7.3.2.3. Cultivators and Tillers

- 7.3.2.4. Other Equipment

- 7.3.3. Irrigation Machinery

- 7.3.3.1. Sprinkler Irrigation

- 7.3.3.2. Drip Irrigation

- 7.3.3.3. Other Irrigation Machinery

- 7.3.4. Harvesting Machinery

- 7.3.4.1. Combine Harvesters

- 7.3.4.2. Forage Harvesters

- 7.3.4.3. Other Harvesting Machinery

- 7.3.5. Haying and Forage Machinery

- 7.3.5.1. Mowers

- 7.3.5.2. Balers

- 7.3.5.3. Other Haying and Forage Machinery

- 7.3.6. Other Types

- 7.3.1. Tractor

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Canada North America Agricultural Equipment Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Tractor

- 8.1.1.1. Less than 40 HP

- 8.1.1.2. 40 to 100 HP

- 8.1.1.3. Above 100 HP

- 8.1.1.4. 4 WD Farm Tractors

- 8.1.2. Equipment

- 8.1.2.1. Plows

- 8.1.2.2. Harrows

- 8.1.2.3. Cultivators and Tillers

- 8.1.2.4. Other Equipment

- 8.1.3. Irrigation Machinery

- 8.1.3.1. Sprinkler Irrigation

- 8.1.3.2. Drip Irrigation

- 8.1.3.3. Other Irrigation Machinery

- 8.1.4. Harvesting Machinery

- 8.1.4.1. Combine Harvesters

- 8.1.4.2. Forage Harvesters

- 8.1.4.3. Other Harvesting Machinery

- 8.1.5. Haying and Forage Machinery

- 8.1.5.1. Mowers

- 8.1.5.2. Balers

- 8.1.5.3. Other Haying and Forage Machinery

- 8.1.6. Other Types

- 8.1.1. Tractor

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United States

- 8.2.2. Canada

- 8.2.3. Mexico

- 8.2.4. Rest of North America

- 8.3. Market Analysis, Insights and Forecast - by Type

- 8.3.1. Tractor

- 8.3.1.1. Less than 40 HP

- 8.3.1.2. 40 to 100 HP

- 8.3.1.3. Above 100 HP

- 8.3.1.4. 4 WD Farm Tractors

- 8.3.2. Equipment

- 8.3.2.1. Plows

- 8.3.2.2. Harrows

- 8.3.2.3. Cultivators and Tillers

- 8.3.2.4. Other Equipment

- 8.3.3. Irrigation Machinery

- 8.3.3.1. Sprinkler Irrigation

- 8.3.3.2. Drip Irrigation

- 8.3.3.3. Other Irrigation Machinery

- 8.3.4. Harvesting Machinery

- 8.3.4.1. Combine Harvesters

- 8.3.4.2. Forage Harvesters

- 8.3.4.3. Other Harvesting Machinery

- 8.3.5. Haying and Forage Machinery

- 8.3.5.1. Mowers

- 8.3.5.2. Balers

- 8.3.5.3. Other Haying and Forage Machinery

- 8.3.6. Other Types

- 8.3.1. Tractor

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Mexico North America Agricultural Equipment Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Tractor

- 9.1.1.1. Less than 40 HP

- 9.1.1.2. 40 to 100 HP

- 9.1.1.3. Above 100 HP

- 9.1.1.4. 4 WD Farm Tractors

- 9.1.2. Equipment

- 9.1.2.1. Plows

- 9.1.2.2. Harrows

- 9.1.2.3. Cultivators and Tillers

- 9.1.2.4. Other Equipment

- 9.1.3. Irrigation Machinery

- 9.1.3.1. Sprinkler Irrigation

- 9.1.3.2. Drip Irrigation

- 9.1.3.3. Other Irrigation Machinery

- 9.1.4. Harvesting Machinery

- 9.1.4.1. Combine Harvesters

- 9.1.4.2. Forage Harvesters

- 9.1.4.3. Other Harvesting Machinery

- 9.1.5. Haying and Forage Machinery

- 9.1.5.1. Mowers

- 9.1.5.2. Balers

- 9.1.5.3. Other Haying and Forage Machinery

- 9.1.6. Other Types

- 9.1.1. Tractor

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United States

- 9.2.2. Canada

- 9.2.3. Mexico

- 9.2.4. Rest of North America

- 9.3. Market Analysis, Insights and Forecast - by Type

- 9.3.1. Tractor

- 9.3.1.1. Less than 40 HP

- 9.3.1.2. 40 to 100 HP

- 9.3.1.3. Above 100 HP

- 9.3.1.4. 4 WD Farm Tractors

- 9.3.2. Equipment

- 9.3.2.1. Plows

- 9.3.2.2. Harrows

- 9.3.2.3. Cultivators and Tillers

- 9.3.2.4. Other Equipment

- 9.3.3. Irrigation Machinery

- 9.3.3.1. Sprinkler Irrigation

- 9.3.3.2. Drip Irrigation

- 9.3.3.3. Other Irrigation Machinery

- 9.3.4. Harvesting Machinery

- 9.3.4.1. Combine Harvesters

- 9.3.4.2. Forage Harvesters

- 9.3.4.3. Other Harvesting Machinery

- 9.3.5. Haying and Forage Machinery

- 9.3.5.1. Mowers

- 9.3.5.2. Balers

- 9.3.5.3. Other Haying and Forage Machinery

- 9.3.6. Other Types

- 9.3.1. Tractor

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of North America North America Agricultural Equipment Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Tractor

- 10.1.1.1. Less than 40 HP

- 10.1.1.2. 40 to 100 HP

- 10.1.1.3. Above 100 HP

- 10.1.1.4. 4 WD Farm Tractors

- 10.1.2. Equipment

- 10.1.2.1. Plows

- 10.1.2.2. Harrows

- 10.1.2.3. Cultivators and Tillers

- 10.1.2.4. Other Equipment

- 10.1.3. Irrigation Machinery

- 10.1.3.1. Sprinkler Irrigation

- 10.1.3.2. Drip Irrigation

- 10.1.3.3. Other Irrigation Machinery

- 10.1.4. Harvesting Machinery

- 10.1.4.1. Combine Harvesters

- 10.1.4.2. Forage Harvesters

- 10.1.4.3. Other Harvesting Machinery

- 10.1.5. Haying and Forage Machinery

- 10.1.5.1. Mowers

- 10.1.5.2. Balers

- 10.1.5.3. Other Haying and Forage Machinery

- 10.1.6. Other Types

- 10.1.1. Tractor

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. United States

- 10.2.2. Canada

- 10.2.3. Mexico

- 10.2.4. Rest of North America

- 10.3. Market Analysis, Insights and Forecast - by Type

- 10.3.1. Tractor

- 10.3.1.1. Less than 40 HP

- 10.3.1.2. 40 to 100 HP

- 10.3.1.3. Above 100 HP

- 10.3.1.4. 4 WD Farm Tractors

- 10.3.2. Equipment

- 10.3.2.1. Plows

- 10.3.2.2. Harrows

- 10.3.2.3. Cultivators and Tillers

- 10.3.2.4. Other Equipment

- 10.3.3. Irrigation Machinery

- 10.3.3.1. Sprinkler Irrigation

- 10.3.3.2. Drip Irrigation

- 10.3.3.3. Other Irrigation Machinery

- 10.3.4. Harvesting Machinery

- 10.3.4.1. Combine Harvesters

- 10.3.4.2. Forage Harvesters

- 10.3.4.3. Other Harvesting Machinery

- 10.3.5. Haying and Forage Machinery

- 10.3.5.1. Mowers

- 10.3.5.2. Balers

- 10.3.5.3. Other Haying and Forage Machinery

- 10.3.6. Other Types

- 10.3.1. Tractor

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Same Deutz-Fahr Deutschland GmbH

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Deere & Company

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Kubota Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 CLAAS Group

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Morris Industries Ltd

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 AGCO Corporation

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 CNH Industrial NV

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Kverneland Group

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Vaderstad Industries Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Netafim Irrigation Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Same Deutz-Fahr Deutschland GmbH

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: North America Agricultural Equipment Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Agricultural Equipment Market Share (%) by Company 2025

List of Tables

- Table 1: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Agricultural Equipment Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 4: North America Agricultural Equipment Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 6: North America Agricultural Equipment Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 7: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 8: North America Agricultural Equipment Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 10: North America Agricultural Equipment Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 11: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 12: North America Agricultural Equipment Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 14: North America Agricultural Equipment Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 16: North America Agricultural Equipment Market Revenue billion Forecast, by Country 2020 & 2033

- Table 17: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 18: North America Agricultural Equipment Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 19: North America Agricultural Equipment Market Revenue billion Forecast, by Type 2020 & 2033

- Table 20: North America Agricultural Equipment Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Agricultural Equipment Market?

The projected CAGR is approximately 4.1%.

2. Which companies are prominent players in the North America Agricultural Equipment Market?

Key companies in the market include Same Deutz-Fahr Deutschland GmbH, Deere & Company, Kubota Corporation, CLAAS Group, Morris Industries Ltd, AGCO Corporation, CNH Industrial NV, Kverneland Group, Vaderstad Industries Inc, Netafim Irrigation Inc.

3. What are the main segments of the North America Agricultural Equipment Market?

The market segments include Type, Geography, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 115.58 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Tomato; Adoption of Greenhouse Technology in Tomato Cultivation; Government support.

6. What are the notable trends driving market growth?

High Adoption of and Innovations in Farm Machinery.

7. Are there any restraints impacting market growth?

Increasing Loses due to Physiological Disorder. Pest and Disease; Unfavourable Climatic Condition.

8. Can you provide examples of recent developments in the market?

December 2022: CNH Industrial added new Automation and Autonomy Solutions to the Ag Tech portfolio in Phoenix, Arizona, and the USA. These New Driverless Tillage and Driver Assist Harvest solutions from Raven, and Baler Automation from Case IH and New Holland, can deliver automation and autonomous equipment enhancements and help solve farmers' most significant challenges to increasing productivity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Agricultural Equipment Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Agricultural Equipment Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Agricultural Equipment Market?

To stay informed about further developments, trends, and reports in the North America Agricultural Equipment Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence