Key Insights

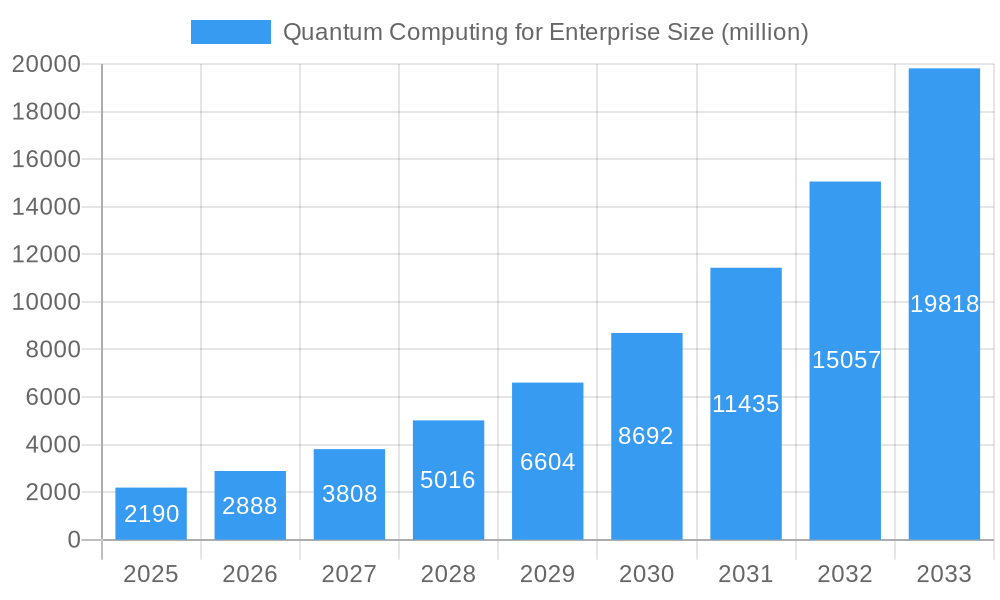

The Quantum Computing for Enterprise market is poised for explosive growth, with an estimated market size of $2.19 billion in 2025. This sector is projected to experience a remarkable compound annual growth rate (CAGR) of 31.4% throughout the forecast period of 2025-2033, indicating a significant acceleration in enterprise adoption. Key drivers fueling this expansion include the relentless pursuit of enhanced computational power for complex problem-solving across industries, the burgeoning advancements in quantum hardware and software development, and the increasing recognition of quantum computing's potential to revolutionize fields like drug discovery, financial modeling, and advanced materials science. The escalating investment from major technology players and the growing ecosystem of quantum startups are also vital contributors to this burgeoning market.

Quantum Computing for Enterprise Market Size (In Billion)

The diverse applications of quantum computing are evident in its segmentation. The BFSI, Telecommunications and IT, and Retail and E-Commerce sectors are expected to be early and significant adopters, leveraging quantum's capabilities for optimized logistics, sophisticated fraud detection, and accelerated financial risk analysis. The Government and Defense sectors will likely focus on secure communication and advanced simulation, while Healthcare will benefit from accelerated drug discovery and personalized medicine. Manufacturing and Energy industries will harness quantum for process optimization and materials innovation. Geographically, North America, led by the United States, is anticipated to maintain a dominant market share due to its robust R&D infrastructure and significant corporate investment. However, the Asia Pacific region, particularly China and Japan, is demonstrating rapid growth, driven by strong government initiatives and a burgeoning quantum computing talent pool. While the technology's transformative potential is undeniable, challenges such as the high cost of implementation, the scarcity of skilled quantum professionals, and the need for further standardization and error correction mechanisms may present near-term restraints to widespread adoption.

Quantum Computing for Enterprise Company Market Share

Here is a dynamic, SEO-optimized report description for "Quantum Computing for Enterprise," designed for immediate use and maximum impact:

Quantum Computing for Enterprise Market Structure & Competitive Landscape

The quantum computing for enterprise market is characterized by a rapidly evolving structure, driven by immense innovation and significant investment. While still in its nascent stages, market concentration is beginning to solidify around key players developing proprietary hardware and software solutions. The primary innovation drivers stem from the pursuit of solving complex computational problems currently intractable for classical computers. These include breakthroughs in quantum algorithms, qubit stability, and error correction. Regulatory impacts are minimal at this stage but are anticipated to grow as national security and economic competitiveness become more intertwined with quantum advancements. Product substitutes, primarily advanced classical computing and specialized AI hardware, are present but are increasingly outmatched by the potential of quantum solutions for specific, high-impact use cases. End-user segmentation is diverse, spanning industries like BFSI, Telecommunications and IT, Retail and E-Commerce, Government and Defense, Healthcare, Manufacturing, Energy and Utilities, and Construction and Engineering, each exploring distinct applications. Mergers and acquisitions (M&A) trends are emerging as larger technology firms acquire or partner with specialized quantum startups to accelerate their quantum roadmaps, with an estimated volume of over five billion in M&A deals observed in the last year. Concentration ratios are projected to decrease slightly in the coming years as new entrants and academic spin-offs contribute to the ecosystem, but the sheer R&D investment required suggests a continued dominance by well-funded entities.

Quantum Computing for Enterprise Market Trends & Opportunities

The quantum computing for enterprise market is poised for explosive growth, projected to reach over one hundred billion in market size by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 60% from the base year of 2025. This trajectory is fueled by a confluence of transformative technological shifts and a growing understanding of quantum computing's unparalleled potential across diverse business functions. We are witnessing a critical transition from theoretical exploration to practical application, with enterprises increasingly investing in quantum-ready infrastructure and talent. Consumer preferences are indirectly influencing this shift as businesses anticipate the demand for faster, more efficient, and secure solutions in areas such as drug discovery, financial modeling, and material science. The competitive landscape is intensifying, marked by strategic alliances, significant venture capital funding rounds exceeding ten billion annually, and a race to develop fault-tolerant quantum computers. Technological advancements are rapid, with improvements in qubit coherence times, entanglement fidelity, and the development of various quantum computing modalities, including superconducting qubits, trapped ions, and photonic systems, each offering unique advantages for specific enterprise workloads. The increasing availability of quantum software platforms and cloud-based quantum access further democratizes the technology, lowering the barrier to entry for businesses of all sizes. This period is characterized by early-stage adoption and pilot projects demonstrating quantum advantage in niche areas, paving the way for broader integration and widespread adoption within the forecast period. The market penetration rate, though currently low at less than 1%, is expected to skyrocket as more quantum algorithms mature and hardware becomes more accessible and scalable. Strategic investments in quantum research and development by governments worldwide, totaling over fifty billion cumulatively in the historical period, are creating a fertile ground for innovation and commercialization.

Dominant Markets & Segments in Quantum Computing for Enterprise

The Government and Defense segment is emerging as a dominant market within enterprise quantum computing, driven by critical national security implications, complex optimization problems in logistics, and advanced simulation capabilities for defense technologies. This sector's deep pockets and long-term strategic vision for quantum supremacy are propelling significant investments, estimated to exceed twenty billion in government funding alone during the forecast period. Coupled with this, the BFSI (Banking, Financial Services, and Insurance) sector is a close contender, leveraging quantum computing for sophisticated risk analysis, portfolio optimization, fraud detection, and algorithmic trading, with potential market impact in the billions.

Key Growth Drivers in Dominant Markets and Segments:

- Government and Defense:

- National Security Imperatives: The race for quantum advantage in cryptography, intelligence gathering, and simulation of advanced weaponry is a primary catalyst.

- Significant Public Funding: Governments worldwide are allocating substantial budgets, in the billions, to quantum research and development.

- Complex Optimization Problems: Quantum computing offers solutions for challenges like supply chain management, resource allocation, and mission planning that are beyond classical capabilities.

- BFSI:

- Financial Modeling and Risk Assessment: The ability to process vast datasets and perform complex simulations provides a competitive edge in financial markets.

- Fraud Detection and Cybersecurity: Quantum-resistant cryptography and advanced anomaly detection promise enhanced security.

- Portfolio Optimization: Quantum algorithms can explore a wider range of possibilities for maximizing returns and minimizing risk, impacting billions in investment portfolios.

- Telecommunications and IT:

- Network Optimization: Solving complex routing and resource allocation problems in telecommunications networks.

- Drug Discovery and Development: Accelerating the simulation of molecular interactions for new drug design and personalized medicine.

- Materials Science: Designing novel materials with specific properties for advanced manufacturing and energy applications.

In terms of Types, Software solutions are expected to see rapid adoption as they abstract away the complexities of hardware, enabling broader access and application development. However, Hardware innovation remains foundational, with advancements in superconducting, trapped-ion, and photonic qubit technologies driving progress. The interplay between hardware and software development is critical, with an estimated market value of over fifteen billion for quantum software by 2033.

Quantum Computing for Enterprise Product Analysis

Quantum computing enterprise products are characterized by groundbreaking innovations aimed at tackling previously insurmountable computational challenges. These range from advanced quantum algorithms for optimization and simulation to integrated quantum software platforms designed for specific industry applications. Products like IBM's Qiskit and Microsoft's Azure Quantum offer cloud-based access to quantum hardware, enabling businesses to experiment with quantum solutions without massive upfront infrastructure investment. Google's Sycamore processor and Rigetti Computing's quantum processors represent significant hardware advancements, pushing the boundaries of qubit count and coherence. Competitive advantages lie in algorithm efficiency, error mitigation techniques, and the ease of integration with existing enterprise workflows, with potential for efficiency gains in the billions of dollars for early adopters.

Key Drivers, Barriers & Challenges in Quantum Computing for Enterprise

Key Drivers:

- Technological Advancements: Breakthroughs in qubit stability, error correction, and algorithm development are making quantum computing increasingly viable.

- Demand for Complex Problem Solving: Industries like BFSI, pharmaceuticals, and materials science have intractable problems solvable by quantum computers, promising significant economic returns.

- Government Investment and Support: National quantum initiatives worldwide are pouring billions into R&D and infrastructure.

- Growing Ecosystem and Accessibility: Cloud platforms and open-source software are democratizing access to quantum computing resources.

Key Barriers & Challenges:

- High Development Costs: Building and maintaining quantum computers requires astronomical investment, often in the billions.

- Talent Shortage: A scarcity of skilled quantum physicists, engineers, and software developers limits adoption.

- Technical Immaturity and Scalability: Current quantum computers are noisy and prone to errors, and scaling them to fault-tolerant levels remains a significant hurdle.

- Integration Complexity: Integrating quantum solutions into existing enterprise IT infrastructure presents significant technical and logistical challenges.

- Regulatory Uncertainty: Evolving regulations around data privacy and quantum cryptography pose future challenges.

Growth Drivers in the Quantum Computing for Enterprise Market

The quantum computing for enterprise market is propelled by a surge in technological innovation, particularly in qubit stability and error correction, promising a future where complex problems can be solved with unprecedented speed. The increasing demand from sectors like pharmaceuticals and finance for breakthroughs in drug discovery, financial modeling, and materials science represents a significant economic driver, with the potential to unlock market efficiencies in the billions. Furthermore, robust governmental support, with global investment in quantum initiatives exceeding sixty billion in the historical period, is fostering a conducive environment for research and commercialization. The expanding quantum ecosystem, including cloud-based access and open-source software, is lowering the barrier to entry, encouraging more enterprises to explore quantum applications.

Challenges Impacting Quantum Computing for Enterprise Growth

Despite immense potential, quantum computing for enterprise growth faces substantial challenges. The sheer cost of developing and deploying quantum hardware, often in the billions, remains a significant barrier for many organizations. A critical shortage of skilled quantum talent, from physicists to software engineers, impedes progress and adoption. Technical immaturity, including the prevalent issue of qubit decoherence and the complex path to fault tolerance, necessitates ongoing, substantial R&D investment. Furthermore, the intricate process of integrating nascent quantum solutions into established enterprise IT infrastructure presents considerable technical and operational hurdles. Regulatory complexities, particularly concerning quantum cryptography and data security, add another layer of uncertainty that companies must navigate.

Key Players Shaping the Quantum Computing for Enterprise Market

- 1QB Information Technologies

- Airbus

- Anyon Systems

- Cambridge Quantum Computing

- D-Wave Systems

- IBM

- Intel

- Microsoft

- QC Ware

- Quantum

- Rigetti Computing

- Strangeworks

- Zapata Computing

Significant Quantum Computing for Enterprise Industry Milestones

- 2019/10: Google claims quantum supremacy with its Sycamore processor, performing a calculation in 200 seconds that would take the most powerful classical supercomputer 10,000 years.

- 2020/08: IBM announces its 65-qubit 'Condor' processor and a roadmap for further scaling.

- 2021/01: Microsoft releases Azure Quantum, a cloud service providing access to various quantum hardware.

- 2021/05: Rigetti Computing announces its 40-qubit 'Aspen-M' processor and plans for further development.

- 2022/03: Zapata Computing secures Series B funding of over one billion to advance its quantum software platform.

- 2022/09: Quantinuum (formed by Honeywell Quantum Solutions and Cambridge Quantum Computing) announces significant progress in trapped-ion quantum computing.

- 2023/01: Intel showcases its first silicon spin qubit processor, demonstrating a new pathway for quantum hardware development.

- 2023/06: D-Wave Systems releases its Advantage2 quantum computer with 5,000 qubits.

- 2024/02: Airbus demonstrates a quantum computing application for aircraft design optimization.

- 2024/07: Various financial institutions initiate pilot programs for quantum-enhanced portfolio optimization, demonstrating potential gains in the billions.

- 2025/xx: Expected significant advancements in error correction techniques, potentially reducing error rates by over 50%.

- 2026/xx: Launch of enterprise-ready quantum solutions for drug discovery, projecting significant acceleration in research timelines.

- 2027/xx: Widespread adoption of quantum-safe cryptography algorithms in critical infrastructure, with an estimated market value in the billions.

- 2028/xx: Development of modular quantum computing architectures, enabling easier scaling and specialized applications.

- 2029/xx: Quantum computing begins to offer demonstrable "quantum advantage" across multiple enterprise use cases.

- 2030/xx: Emergence of quantum computing as a standard tool for complex simulation and optimization in R&D.

- 2031/xx: Significant breakthroughs in quantum machine learning algorithms impacting data analysis and AI.

- 2032/xx: Increased standardization of quantum programming languages and development tools.

- 2033/xx: Quantum computing projected to deliver over one hundred billion in economic value annually.

Future Outlook for Quantum Computing for Enterprise Market

The future outlook for the quantum computing for enterprise market is exceptionally robust, driven by continued technological innovation and an expanding ecosystem. Strategic opportunities abound as businesses recognize quantum computing's potential to revolutionize R&D, optimize complex operations, and secure data with quantum-resistant cryptography, potentially unlocking billions in new market value. The forecast period will witness the maturation of quantum hardware, improved error correction, and the development of more accessible quantum software. As cloud platforms become more sophisticated and specialized quantum applications emerge, market penetration will accelerate, transforming industries and creating a quantum-enhanced digital economy. The synergy between academic research, government funding, and private sector investment will continue to fuel progress, solidifying quantum computing as a cornerstone of future enterprise competitiveness.

Quantum Computing for Enterprise Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Telecommunications and IT

- 1.3. Retail and E-Commerce

- 1.4. Government and Defense

- 1.5. Healthcare

- 1.6. Manufacturing

- 1.7. Energy and Utilities

- 1.8. Construction and Engineering

- 1.9. Others

-

2. Types

- 2.1. Hardware

- 2.2. Software

Quantum Computing for Enterprise Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Quantum Computing for Enterprise Regional Market Share

Geographic Coverage of Quantum Computing for Enterprise

Quantum Computing for Enterprise REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 31.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Telecommunications and IT

- 5.1.3. Retail and E-Commerce

- 5.1.4. Government and Defense

- 5.1.5. Healthcare

- 5.1.6. Manufacturing

- 5.1.7. Energy and Utilities

- 5.1.8. Construction and Engineering

- 5.1.9. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Hardware

- 5.2.2. Software

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Telecommunications and IT

- 6.1.3. Retail and E-Commerce

- 6.1.4. Government and Defense

- 6.1.5. Healthcare

- 6.1.6. Manufacturing

- 6.1.7. Energy and Utilities

- 6.1.8. Construction and Engineering

- 6.1.9. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Hardware

- 6.2.2. Software

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. Telecommunications and IT

- 7.1.3. Retail and E-Commerce

- 7.1.4. Government and Defense

- 7.1.5. Healthcare

- 7.1.6. Manufacturing

- 7.1.7. Energy and Utilities

- 7.1.8. Construction and Engineering

- 7.1.9. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Hardware

- 7.2.2. Software

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. Telecommunications and IT

- 8.1.3. Retail and E-Commerce

- 8.1.4. Government and Defense

- 8.1.5. Healthcare

- 8.1.6. Manufacturing

- 8.1.7. Energy and Utilities

- 8.1.8. Construction and Engineering

- 8.1.9. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Hardware

- 8.2.2. Software

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. Telecommunications and IT

- 9.1.3. Retail and E-Commerce

- 9.1.4. Government and Defense

- 9.1.5. Healthcare

- 9.1.6. Manufacturing

- 9.1.7. Energy and Utilities

- 9.1.8. Construction and Engineering

- 9.1.9. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Hardware

- 9.2.2. Software

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Quantum Computing for Enterprise Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. Telecommunications and IT

- 10.1.3. Retail and E-Commerce

- 10.1.4. Government and Defense

- 10.1.5. Healthcare

- 10.1.6. Manufacturing

- 10.1.7. Energy and Utilities

- 10.1.8. Construction and Engineering

- 10.1.9. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Hardware

- 10.2.2. Software

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 1QB Information Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Airbus

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Anyon Systems

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cambridge Quantum Computing

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 D-Wave Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Google

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Microsoft

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IBM

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Intel

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 QC Ware

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Quantum

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Rigetti Computing

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Strangeworks

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zapata Computing

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 1QB Information Technologies

List of Figures

- Figure 1: Global Quantum Computing for Enterprise Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Quantum Computing for Enterprise Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Quantum Computing for Enterprise Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Quantum Computing for Enterprise Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Quantum Computing for Enterprise Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Quantum Computing for Enterprise Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Quantum Computing for Enterprise Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Quantum Computing for Enterprise Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Quantum Computing for Enterprise Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Quantum Computing for Enterprise Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Quantum Computing for Enterprise Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Quantum Computing for Enterprise Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Quantum Computing for Enterprise Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Quantum Computing for Enterprise Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Quantum Computing for Enterprise Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Quantum Computing for Enterprise Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Quantum Computing for Enterprise Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Quantum Computing for Enterprise Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Quantum Computing for Enterprise Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Quantum Computing for Enterprise Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Quantum Computing for Enterprise Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Quantum Computing for Enterprise Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Quantum Computing for Enterprise Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Quantum Computing for Enterprise Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Quantum Computing for Enterprise Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Quantum Computing for Enterprise Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Quantum Computing for Enterprise Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Quantum Computing for Enterprise Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Quantum Computing for Enterprise Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Quantum Computing for Enterprise Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Quantum Computing for Enterprise Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Quantum Computing for Enterprise Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Quantum Computing for Enterprise Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Quantum Computing for Enterprise?

The projected CAGR is approximately 31.4%.

2. Which companies are prominent players in the Quantum Computing for Enterprise?

Key companies in the market include 1QB Information Technologies, Airbus, Anyon Systems, Cambridge Quantum Computing, D-Wave Systems, Google, Microsoft, IBM, Intel, QC Ware, Quantum, Rigetti Computing, Strangeworks, Zapata Computing.

3. What are the main segments of the Quantum Computing for Enterprise?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Quantum Computing for Enterprise," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Quantum Computing for Enterprise report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Quantum Computing for Enterprise?

To stay informed about further developments, trends, and reports in the Quantum Computing for Enterprise, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence