Key Insights

The Asia-Pacific private equity industry is experiencing robust growth, driven by a confluence of factors including increasing institutional investor interest, a burgeoning middle class fueling consumer spending, and supportive government policies promoting infrastructure development and economic diversification across the region. The market, while exhibiting regional variations, is characterized by strong activity in established economies like Japan, Australia, and Singapore, alongside rapidly expanding opportunities in emerging markets such as India, Indonesia, and Vietnam. These emerging markets are particularly attractive due to their large populations, rising disposable incomes, and relatively underdeveloped financial sectors presenting significant untapped potential for private equity investment. The focus is shifting towards sectors like technology, healthcare, and renewable energy, reflecting global trends and the region's unique growth dynamics. Competition is intensifying amongst both domestic and international private equity firms, leading to innovative deal structuring and a heightened focus on value creation strategies. While economic uncertainties and geopolitical risks present challenges, the long-term outlook remains positive, supported by a favorable demographic profile and ongoing structural reforms across many Asia-Pacific nations.

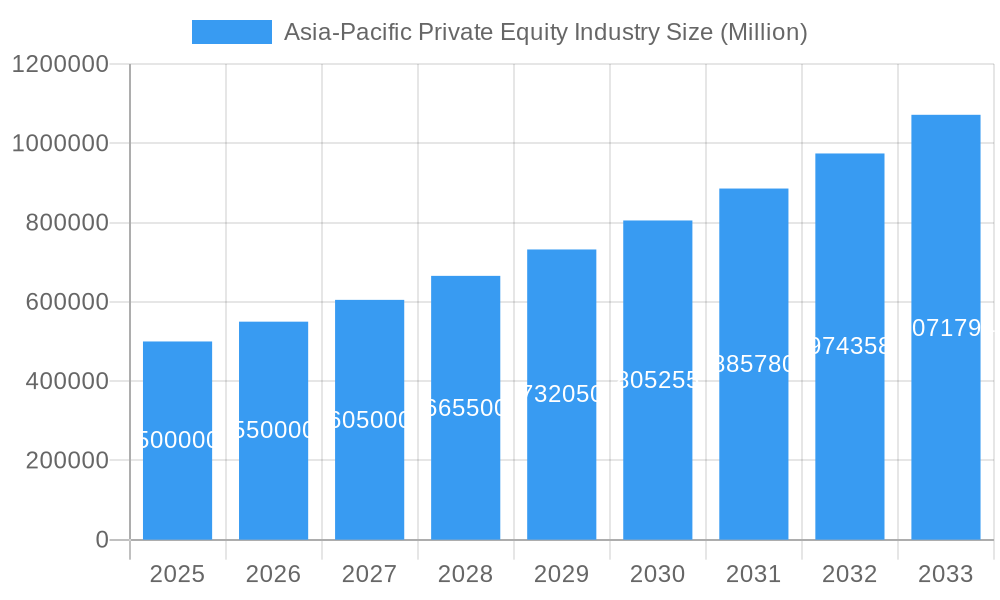

Asia-Pacific Private Equity Industry Market Size (In Billion)

Despite the overall positive trajectory, the Asia-Pacific private equity market faces complexities. Navigating regulatory landscapes varies across the diverse countries within the region, demanding a nuanced understanding of local regulations and investment frameworks. Finding suitable exit strategies also requires careful consideration, as market liquidity can differ substantially between developed and emerging economies. However, the sheer size and diversity of the Asia-Pacific region, combined with its impressive economic growth potential, make it a highly attractive investment destination for private equity firms globally. The industry’s expansion is further fueled by the increasing adoption of technology and data analytics in investment decisions and portfolio management, leading to more efficient and data-driven strategies. This ongoing evolution and adaptation within the industry ensures its sustained growth and influence on the economic landscape of the Asia-Pacific region.

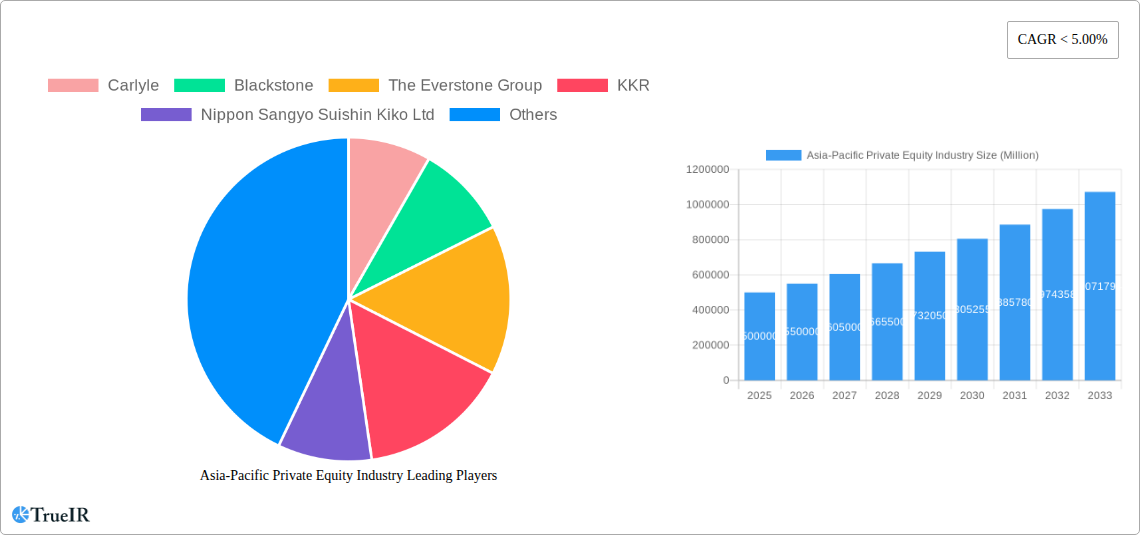

Asia-Pacific Private Equity Industry Company Market Share

Asia-Pacific Private Equity Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Asia-Pacific private equity industry, offering invaluable insights for investors, industry professionals, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report examines market structure, competitive dynamics, growth drivers, and future outlook. The study incorporates extensive quantitative data and qualitative analysis, providing a clear understanding of this dynamic and rapidly evolving market. Key players such as Carlyle, Blackstone, and KKR are analyzed, alongside emerging firms, offering a 360-degree view of the landscape.

Asia-Pacific Private Equity Industry Market Structure & Competitive Landscape

The Asia-Pacific private equity market is characterized by a moderately concentrated structure, with a few dominant players and a large number of smaller firms. The Herfindahl-Hirschman Index (HHI) for the region is estimated at xx in 2025, indicating a moderately competitive market. However, this varies significantly across sub-regions, with some exhibiting higher levels of concentration.

Market Concentration:

- Dominant players such as Carlyle, Blackstone, and KKR hold significant market share, driving M&A activity.

- Regional players and smaller firms actively compete for deals, particularly in niche sectors.

- The concentration ratio for the top 5 firms in 2025 is estimated at xx%.

Innovation Drivers:

- Technological advancements in areas like fintech and AI are creating new investment opportunities.

- Rising demand for sustainable and ESG-compliant investments is driving innovation.

- Government initiatives promoting private equity investment in specific sectors contribute to market innovation.

Regulatory Impacts:

- Varying regulatory environments across the Asia-Pacific region impact investment strategies and deal flow.

- New regulations related to data privacy, antitrust, and foreign investment influence market dynamics.

- Government policies aimed at promoting domestic industries shape the investment landscape.

Product Substitutes:

- Other forms of alternative investment, such as venture capital and real estate investment trusts, offer competitive alternatives.

End-User Segmentation:

- The industry serves a diverse range of end-users including large corporations, SMEs, and government entities.

M&A Trends:

- The volume of M&A transactions in the Asia-Pacific private equity market experienced a significant surge in recent years, reaching xx Million deals in 2024.

- Cross-border transactions are increasing as firms seek diversification and expansion opportunities.

- Consolidation among private equity firms is expected to continue.

Asia-Pacific Private Equity Industry Market Trends & Opportunities

The Asia-Pacific private equity market is experiencing a period of dynamic expansion, propelled by a confluence of powerful growth engines. Market projections indicate a significant upswing, with the market size anticipated to reach [Insert Latest Market Size Value Here] by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of [Insert Latest CAGR Value Here] during the forecast period of 2025-2033. This impressive trajectory is underpinned by a notable increase in sophisticated institutional investor participation, the sustained rise of a burgeoning middle class, and substantial, ongoing infrastructure development initiatives across the diverse landscapes of the region.

Technological innovation is fundamentally transforming the industry's operational fabric. Advanced technologies are streamlining critical processes such as deal sourcing, enhancing portfolio management capabilities, and refining risk assessment methodologies. The pervasive adoption of data analytics and artificial intelligence is instrumental in elevating the rigor of due diligence processes and sharpening the precision of investment decision-making. Simultaneously, evolving consumer preferences are increasingly tilting towards sustainable and ethically conscious investments, consequently fueling a robust demand for private equity funds that are compliant with Environmental, Social, and Governance (ESG) principles. The competitive arena is characterized by its vibrant and ever-changing nature, with a strategic interplay between well-established market veterans and agile new entrants aggressively vying for market share. Market penetration rates exhibit considerable variance, fluctuating significantly across different sectors and geographical sub-regions, with more mature economies and specialized industry segments typically demonstrating higher penetration levels. The overarching market outlook remains overwhelmingly positive, signaling substantial growth potential, particularly within emerging markets and in relation to novel investment themes.

Dominant Markets & Segments in Asia-Pacific Private Equity Industry

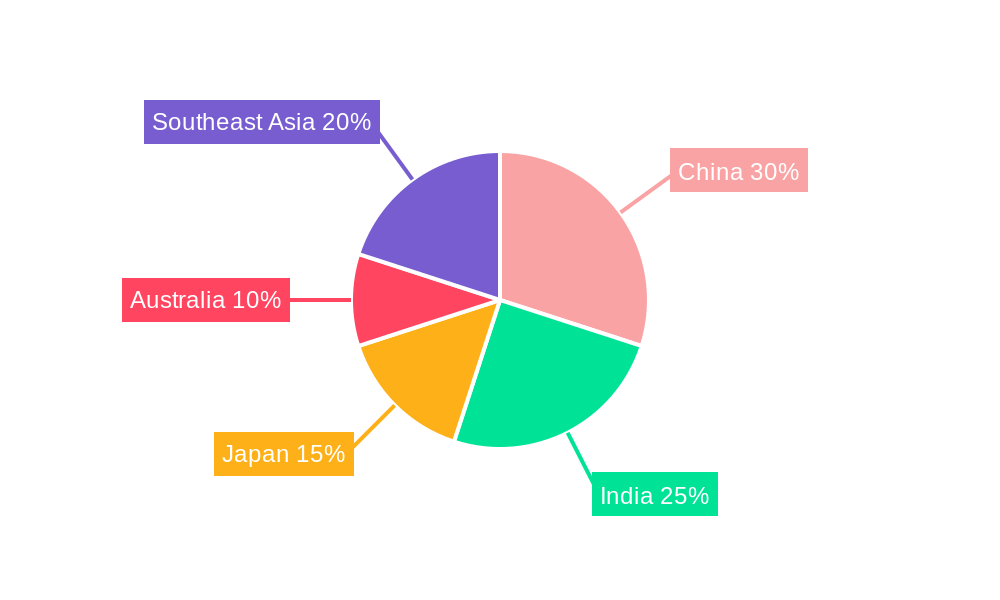

Within the expansive Asia-Pacific private equity ecosystem, China and India continue to assert their dominance, largely due to their immense economic scale, substantial investment allure, and the presence of supportive government frameworks. Concurrently, Southeast Asia is emerging as a rapidly expanding hub, propelled by vigorous economic momentum and the dynamic growth of its consumer markets. Across specific industry segments, technology, healthcare, and infrastructure consistently attract significant capital inflows, highlighting their pivotal roles in regional development and innovation.

-

Key Growth Drivers in China:

- Vast domestic market and sustained, robust economic expansion.

- Strategic government support for key industrial and technological sectors.

- High propensity for groundbreaking technological innovation and disruptive market potential.

-

Key Growth Drivers in India:

- A large and continuously expanding middle class, driving escalating consumer demand across diverse product and service categories.

- Proactive government initiatives, such as 'Make in India,' fostering domestic manufacturing and industrial capabilities.

- Accelerated pace of digitalization and widespread adoption of advanced technologies.

-

Key Growth Drivers in Southeast Asia:

- Strong and consistent economic growth coupled with rising affluence and disposable incomes.

- A young, demographic dividend and a rapidly growing, dynamic population.

- Strategic focus on significant infrastructure development to support economic and social progress.

The sustained leadership of China and India is a testament to their sheer economic magnitude and inherent dynamism. However, the increasing prominence and attractiveness of Southeast Asia present compelling and diversified growth avenues for private equity firms looking to expand their regional footprint.

Asia-Pacific Private Equity Industry Product Analysis

Private equity products in the Asia-Pacific region are increasingly diversified to meet the specific needs of investors and businesses. This ranges from traditional buyout funds to specialized vehicles focused on specific industries or investment strategies like venture capital, growth equity, and infrastructure funds. Technological advancements such as AI-driven deal sourcing platforms and sophisticated portfolio management tools are enhancing the efficiency and returns of these products. The market fit of these new offerings hinges on adapting to local market conditions, regulatory frameworks, and investor preferences.

Key Drivers, Barriers & Challenges in Asia-Pacific Private Equity Industry

Key Drivers:

- The vigorous economic expansion and the upward trend in disposable incomes across numerous Asia-Pacific nations are cultivating exceptionally favorable conditions for investment.

- Forward-thinking government policies designed to encourage private equity investments, coupled with substantial investments in infrastructure development, are acting as significant catalysts for market growth.

- The relentless march of technological advancements is leading to demonstrable improvements in deal sourcing efficiency, portfolio management effectiveness, and the precision of risk assessment, thereby rendering investment processes more streamlined and impactful.

Barriers & Challenges:

- The prevailing geopolitical uncertainties and the fluctuating regulatory landscapes observed across the region can introduce complexities and hesitation into investment decisions and the pipeline of deals. The precise quantifiable impact is challenging to ascertain, but it can lead to a reduction in investment appetite for markets perceived as volatile.

- Disruptions within global supply chains, often exacerbated by unforeseen global events such as pandemics, can adversely affect the financial performance and returns of portfolio companies. A concrete example of a quantifiable impact includes an estimated [Insert Specific Figure, e.g., $5 Million] in lost revenue for a particular portfolio company due to prolonged supply chain disruptions.

- The intensifying competition among both established domestic and international private equity firms is creating upward pressure on investment returns and demanding greater strategic acumen and operational efficiency from all market participants.

Growth Drivers in the Asia-Pacific Private Equity Industry Market

The Asia-Pacific region's robust economic expansion, coupled with supportive government policies and rising consumer spending, fuels significant growth in the private equity industry. Technological advancements are enhancing efficiency and investment returns, while the increasing prominence of ESG investing drives demand for sustainable private equity strategies.

Challenges Impacting Asia-Pacific Private Equity Industry Growth

Regulatory complexities across diverse markets, coupled with geopolitical uncertainties and potential supply chain disruptions, present significant challenges. Intense competition for promising investment opportunities and a need to navigate varying regulatory frameworks further pose obstacles to consistent and predictable growth.

Key Players Shaping the Asia-Pacific Private Equity Industry Market

- Carlyle

- Blackstone

- The Everstone Group

- KKR

- Nippon Sangyo Suishin Kiko Ltd (JIC)

- Bain Capital

- Warburg Pincus

- J-Star

- Ascent Capital

- CVC Capital Partners (This list is representative and not exhaustive)

Significant Asia-Pacific Private Equity Industry Milestones

September 2022: The Asian Development Bank (ADB) signed a USD 15 Million equity investment in KV Asia Capital Fund II LP, expanding investment opportunities in Southeast Asia's healthcare, financial services, education, manufacturing, business services, and consumer sectors. This signifies increased institutional investor confidence and broader access to capital for promising companies.

July 2022: Malaysia-headquartered private equity firm Navis Capital Partners launched an Asia Credit Platform, Navis Asia Credit. This highlights the growing importance of credit investments in the regional market and the diversification of strategies within the private equity industry.

Future Outlook for Asia-Pacific Private Equity Industry Market

The Asia-Pacific private equity market is strategically positioned for sustained and robust growth. This positive trajectory is fueled by the region's dynamic economic expansion, the accelerating pace of technological innovation, and a growing influx of sophisticated institutional investor capital. Significant strategic opportunities are abundant across high-growth sectors such as technology, healthcare, and infrastructure, presenting highly attractive investment prospects for discerning private equity firms. The long-term potential of this market is considerable, promising substantial returns for investors who possess the foresight and agility to successfully navigate the inherent complexities and capitalize on the unique dynamics of this vibrant and evolving landscape.

Asia-Pacific Private Equity Industry Segmentation

-

1. Investment

- 1.1. Real Estate

- 1.2. Private Investment in Public Equity (PIPE)

- 1.3. Buyouts

- 1.4. Exits

Asia-Pacific Private Equity Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Private Equity Industry Regional Market Share

Geographic Coverage of Asia-Pacific Private Equity Industry

Asia-Pacific Private Equity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of < 5.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Investment

- 5.1.1. Real Estate

- 5.1.2. Private Investment in Public Equity (PIPE)

- 5.1.3. Buyouts

- 5.1.4. Exits

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Investment

- 6. Asia-Pacific Private Equity Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Investment

- 6.1.1. Real Estate

- 6.1.2. Private Investment in Public Equity (PIPE)

- 6.1.3. Buyouts

- 6.1.4. Exits

- 6.1. Market Analysis, Insights and Forecast - by Investment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Carlyle

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Blackstone

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Everstone Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 KKR

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nippon Sangyo Suishin Kiko Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bain Capital

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Warburg Pincus

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 J-Star

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ascent Capital

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 CVC Capital Partners**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Carlyle

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Private Equity Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Private Equity Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Investment 2020 & 2033

- Table 2: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Investment 2020 & 2033

- Table 4: Asia-Pacific Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: China Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Japan Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: South Korea Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: India Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Australia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: New Zealand Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Indonesia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Malaysia Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Singapore Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Thailand Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Vietnam Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Philippines Asia-Pacific Private Equity Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Private Equity Industry?

The projected CAGR is approximately < 5.00%.

2. Which companies are prominent players in the Asia-Pacific Private Equity Industry?

Key companies in the market include Carlyle, Blackstone, The Everstone Group, KKR, Nippon Sangyo Suishin Kiko Ltd, Bain Capital, Warburg Pincus, J-Star, Ascent Capital, CVC Capital Partners**List Not Exhaustive.

3. What are the main segments of the Asia-Pacific Private Equity Industry?

The market segments include Investment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Deals Made a Remarkable Rebound in Asia-Pacific Private Equity Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

September 2022: The Asian Development Bank (ADB) signed a USD 15 million equity investment in KV Asia Capital Fund II LP, a private equity fund managed by KV Asia to provide growth capital to companies in the health care, financial services, education, manufacturing, business services, and consumer sectors across Southeast Asia.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Private Equity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Private Equity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Private Equity Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Private Equity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence