Key Insights

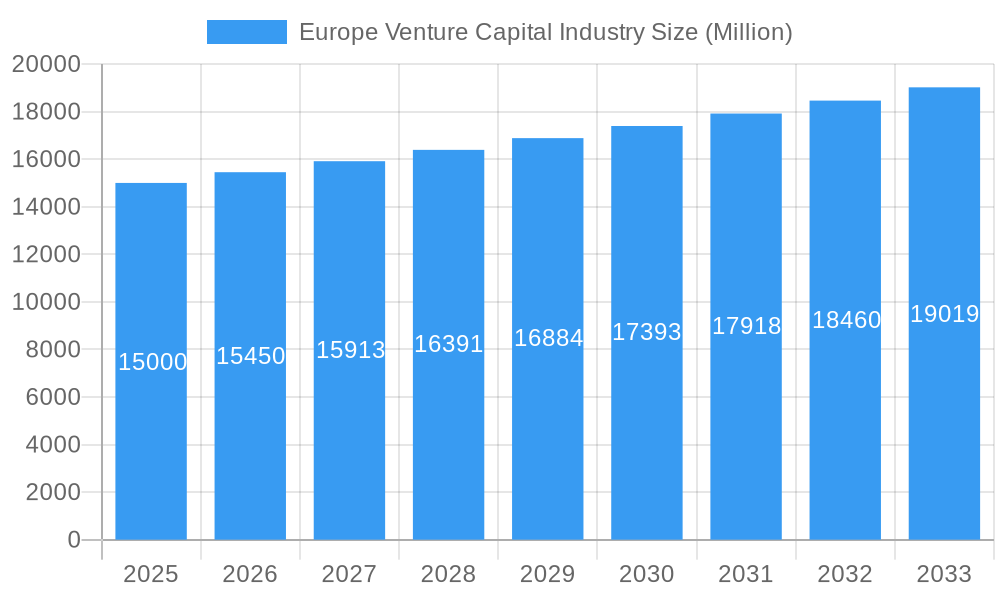

The European Venture Capital (VC) industry is experiencing significant expansion, driven by a dynamic innovation ecosystem and robust investor confidence. The market is projected to achieve a Compound Annual Growth Rate (CAGR) of 13.87%, with an estimated market size of $8.74 billion in the base year 2025. This growth trajectory is expected to continue through 2033, underscoring the region's appeal for venture funding.

Europe Venture Capital Industry Market Size (In Billion)

Key factors fueling this expansion include a flourishing tech sector, particularly in Fintech, Pharma & Biotech, and a supportive regulatory framework across leading European nations such as the UK, Germany, and Finland. These countries attract substantial investment, spanning from angel and seed rounds to later-stage funding, demonstrating a mature and diverse VC landscape. The increasing number of successful startup exits and high-growth ventures creates a virtuous cycle, attracting further capital and fostering continuous innovation.

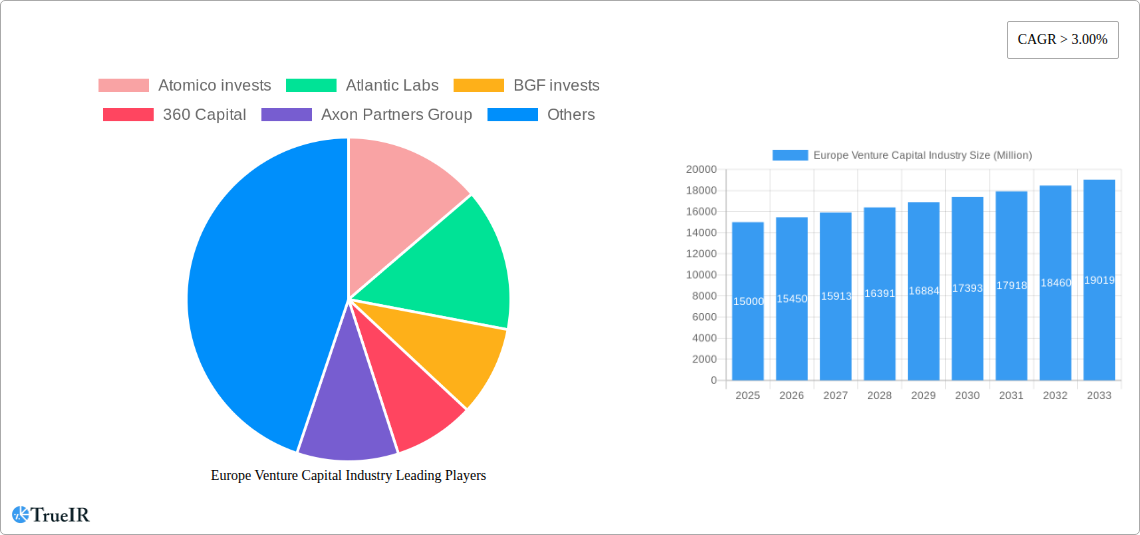

Europe Venture Capital Industry Company Market Share

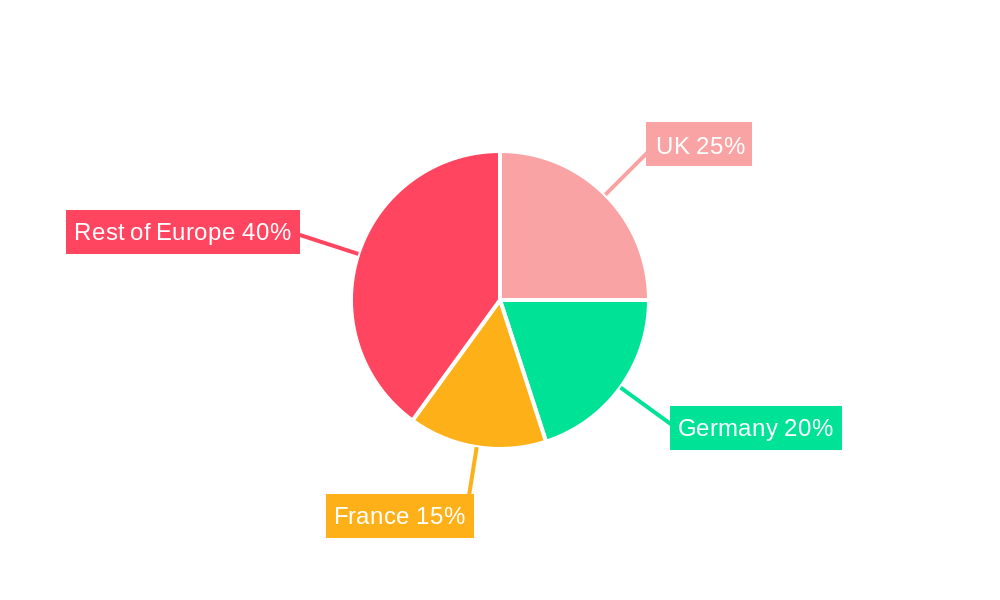

Investment segmentation reveals a diversified approach, with Fintech, Pharma & Biotech, and Consumer Goods anticipated to command significant portions of capital. Early-stage investments are crucial for nurturing new enterprises, while substantial later-stage funding supports the scaling and expansion of established companies. Geographically, investment is distributed across the UK, Germany, Finland, Spain, and other key European markets, reflecting a vibrant and decentralized investment environment. The consistent strong performance from 2019 to 2024 reinforces the positive outlook for continued growth and increased investor confidence in the European startup ecosystem throughout the forecast period (2025-2033).

Europe Venture Capital Industry: A Comprehensive Market Report (2019-2033)

This dynamic report provides a detailed analysis of the European Venture Capital industry, offering invaluable insights for investors, entrepreneurs, and industry professionals. With a focus on key market trends, competitive landscapes, and future growth projections, this report is essential for navigating the complexities of this rapidly evolving sector. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, while the historical period encompasses 2019-2024.

Europe Venture Capital Industry Market Structure & Competitive Landscape

The European Venture Capital market exhibits a moderately concentrated structure, with a few dominant players alongside numerous smaller firms. Key factors influencing market dynamics include continuous innovation driven by technological advancements, evolving regulatory landscapes impacting investment strategies, and the presence of alternative investment options (product substitutes). End-user segmentation is primarily categorized by industry vertical (e.g., Fintech, Biotech) and investment stage (Angel/Seed, Early-stage, Later-stage). Mergers and acquisitions (M&A) activity is significant, with an estimated xx Million deals closed in 2024, reflecting industry consolidation and strategic expansion. The Herfindahl-Hirschman Index (HHI) for the market in 2024 is estimated at xx, indicating a moderately concentrated market.

- Market Concentration: Moderately concentrated, with a few large firms controlling a significant share.

- Innovation Drivers: Technological advancements (AI, biotech), shifting consumer preferences.

- Regulatory Impacts: Evolving regulations on data privacy, fintech, and cross-border investments.

- Product Substitutes: Private equity, angel investors, crowdfunding platforms.

- End-User Segmentation: Fintech, Pharma & Biotech, Consumer Goods, Industrial/Energy, IT Hardware & Services, and Other Industries.

- M&A Trends: Consistent M&A activity, driven by strategic expansion and consolidation.

Europe Venture Capital Industry Market Trends & Opportunities

The European Venture Capital market is experiencing robust growth, driven by several key trends. The market size reached xx Million in 2024 and is projected to reach xx Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period. Technological advancements, particularly in AI and Fintech, are creating new investment opportunities. Changing consumer preferences are influencing investment strategies, with a focus on sustainability and ESG (Environmental, Social, and Governance) factors. Increased competition is driving innovation and efficiency within the industry. Market penetration rates for venture capital in various sectors vary widely, with Fintech and Biotech showing the highest penetration.

Dominant Markets & Segments in Europe Venture Capital Industry

The UK remains the dominant market within Europe for Venture Capital investments, followed by Germany. Within industry segments, Fintech and Pharma & Biotech attract the largest share of investments.

- By Industry of Investment: Fintech shows the highest growth, followed by Pharma & Biotech and IT Hardware & Services.

- Investments - By Country: UK (xx Million), Germany (xx Million), Others (xx Million)

- Deal Size - By Stage of Investment: Early-stage investing constitutes the largest portion of deals, followed by later-stage and Angel/Seed investing.

Key Growth Drivers:

- Strong entrepreneurial ecosystem: A large pool of talented entrepreneurs and innovative startups.

- Government support: Initiatives like the French tech fund contribute to market growth.

- Favorable regulatory environment (in certain sectors): Streamlined processes for investment and startups.

Europe Venture Capital Industry Product Analysis

Venture capital products are primarily focused on funding different stages of startup growth—from seed funding to later-stage growth equity. Recent innovations include specialized funds targeting specific technologies (e.g., AI, GreenTech) and flexible investment structures to better meet the needs of entrepreneurs. Successful products demonstrate a strong alignment with market demands and technological advancements, offering competitive advantages through specialized expertise and networks.

Key Drivers, Barriers & Challenges in Europe Venture Capital Industry

Key Drivers:

- Technological advancements driving innovation and creating new investment opportunities.

- Growing number of high-potential startups.

- Increased government support and initiatives.

Key Challenges and Restraints:

- Regulatory complexities and variations across European countries.

- Competition for funding from other investment sources.

- Economic uncertainties and potential downturns impacting investor confidence.

Growth Drivers in the Europe Venture Capital Industry Market

The European VC market is fueled by technological innovation, a growing number of high-potential startups, and supportive government initiatives like the French tech fund. These factors create a fertile ground for investment and drive significant growth. Economic stability and regulatory clarity will play a significant role.

Challenges Impacting Europe Venture Capital Industry Growth

Regulatory complexities across Europe, competition from other investment vehicles, and potential economic downturns pose challenges. These factors can impact investor confidence and the overall availability of capital. Supply chain disruptions can impact certain sectors and limit growth in associated startups.

Key Players Shaping the Europe Venture Capital Industry Market

- Atomico

- Atlantic Labs

- BGF invests

- 360 Capital

- Axon Partners Group

- Acton Capital

- Bonsai Venture Capital

- Accel Partners

- Active Venture

- AAC Capital

- Adara Ventures

Significant Europe Venture Capital Industry Industry Milestones

- Oct 2021: Sequoia Capital's shift to a singular, permanent fund structure signifies a major strategic change in the industry, aiming to enhance returns and efficiency.

- Feb 2022: The French government's announcement of a new fund to boost the tech sector signals a strong commitment to fostering technological innovation and supporting startups. This initiative aims to create 10 tech companies with a net worth exceeding €100 billion by 2030.

Future Outlook for Europe Venture Capital Industry Market

The European Venture Capital market is poised for continued growth, driven by technological advancements, increasing entrepreneurial activity, and supportive government policies. Strategic investments in promising sectors like Fintech and Biotech, coupled with a focus on sustainability and ESG factors, will shape the future landscape. The market's potential remains substantial, with significant opportunities for investors and entrepreneurs alike.

Europe Venture Capital Industry Segmentation

-

1. Deal Size - Stage of Investment

- 1.1. Angel/Seed Investing

- 1.2. Early-stage Investing

- 1.3. Later-stage Investing

-

2. Industry of Investment

- 2.1. Fintech

- 2.2. Pharma and Biotech

- 2.3. Consumer Goods

- 2.4. Industrial/Energy

- 2.5. IT Hardware and Services

- 2.6. Other Industries of Investment

Europe Venture Capital Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Venture Capital Industry Regional Market Share

Geographic Coverage of Europe Venture Capital Industry

Europe Venture Capital Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.87% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deal Size - Stage of Investment

- 5.1.1. Angel/Seed Investing

- 5.1.2. Early-stage Investing

- 5.1.3. Later-stage Investing

- 5.2. Market Analysis, Insights and Forecast - by Industry of Investment

- 5.2.1. Fintech

- 5.2.2. Pharma and Biotech

- 5.2.3. Consumer Goods

- 5.2.4. Industrial/Energy

- 5.2.5. IT Hardware and Services

- 5.2.6. Other Industries of Investment

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Deal Size - Stage of Investment

- 6. Europe Venture Capital Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deal Size - Stage of Investment

- 6.1.1. Angel/Seed Investing

- 6.1.2. Early-stage Investing

- 6.1.3. Later-stage Investing

- 6.2. Market Analysis, Insights and Forecast - by Industry of Investment

- 6.2.1. Fintech

- 6.2.2. Pharma and Biotech

- 6.2.3. Consumer Goods

- 6.2.4. Industrial/Energy

- 6.2.5. IT Hardware and Services

- 6.2.6. Other Industries of Investment

- 6.1. Market Analysis, Insights and Forecast - by Deal Size - Stage of Investment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Atomico invests

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Atlantic Labs

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BGF invests

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 360 Capital

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Axon Partners Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Acton Capital

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Bonsai Venture Capita

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Accel Partners

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Active Venture

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 AAC Capital

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Adara Ventures

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Atomico invests

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Venture Capital Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Venture Capital Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Venture Capital Industry Revenue billion Forecast, by Deal Size - Stage of Investment 2020 & 2033

- Table 2: Europe Venture Capital Industry Revenue billion Forecast, by Industry of Investment 2020 & 2033

- Table 3: Europe Venture Capital Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Venture Capital Industry Revenue billion Forecast, by Deal Size - Stage of Investment 2020 & 2033

- Table 5: Europe Venture Capital Industry Revenue billion Forecast, by Industry of Investment 2020 & 2033

- Table 6: Europe Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Venture Capital Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Venture Capital Industry?

The projected CAGR is approximately 13.87%.

2. Which companies are prominent players in the Europe Venture Capital Industry?

Key companies in the market include Atomico invests, Atlantic Labs, BGF invests, 360 Capital, Axon Partners Group, Acton Capital, Bonsai Venture Capita, Accel Partners, Active Venture, AAC Capital, Adara Ventures.

3. What are the main segments of the Europe Venture Capital Industry?

The market segments include Deal Size - Stage of Investment, Industry of Investment.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.74 billion as of 2022.

5. What are some drivers contributing to market growth?

Fund Inflows is Driving the ETF Market.

6. What are the notable trends driving market growth?

United States' role in VC rounds in Europe.

7. Are there any restraints impacting market growth?

Underlying Fluctuations and Risks are Restraining the Market.

8. Can you provide examples of recent developments in the market?

February 2022: France's Prime Minister, Bruno Le Maire, announced the plans of creating a new fund to boost the technological sector in Europe. The target of the fund is to establish 10 technological companies having a net worth of more than Euro 100 billion by the end of 2030. Moreover, the fund will be publicly funded to finance new technological startups emerging in Europe.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Venture Capital Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Venture Capital Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Venture Capital Industry?

To stay informed about further developments, trends, and reports in the Europe Venture Capital Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence