Key Insights

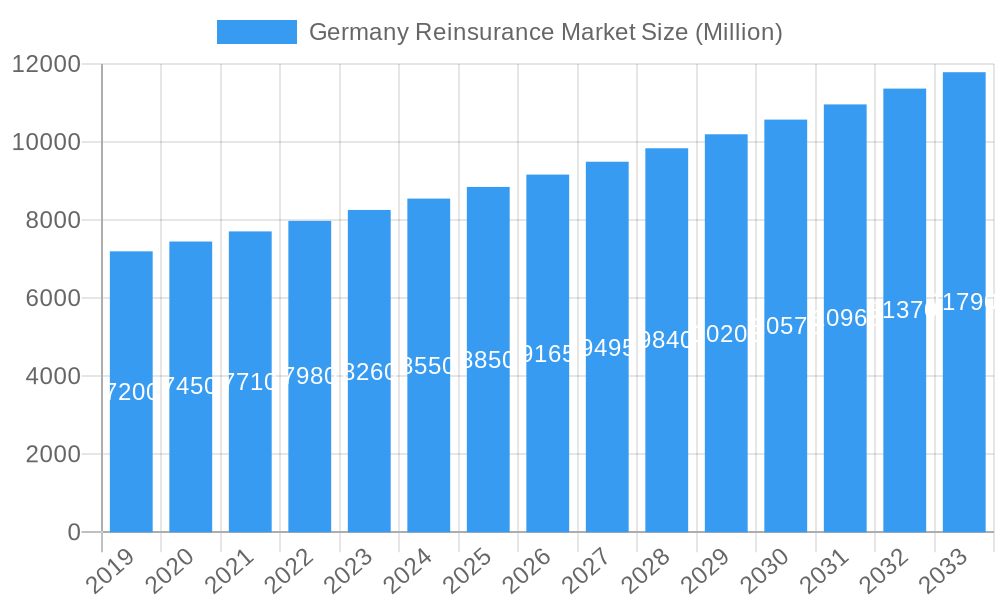

The German reinsurance market is projected for significant growth, with an estimated market size of $689.74 billion by 2025. The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 10.2% through 2033. This expansion is driven by increasing demand for advanced risk management solutions in property & casualty and life & health sectors. Key factors include heightened awareness of financial risks from natural catastrophes, evolving regulatory requirements, and the complexity of modern business operations. The demand for complex insurance products and insurers' need to diversify risk portfolios are also crucial, necessitating reinsurance for capacity and solvency. An aging population and rising chronic diseases are boosting the life and health reinsurance segment, while climate change impacts are increasing demand for property and casualty reinsurance. Technological advancements, including the digitalization of underwriting and claims, are enhancing efficiency and data analytics, supporting market growth.

Germany Reinsurance Market Market Size (In Billion)

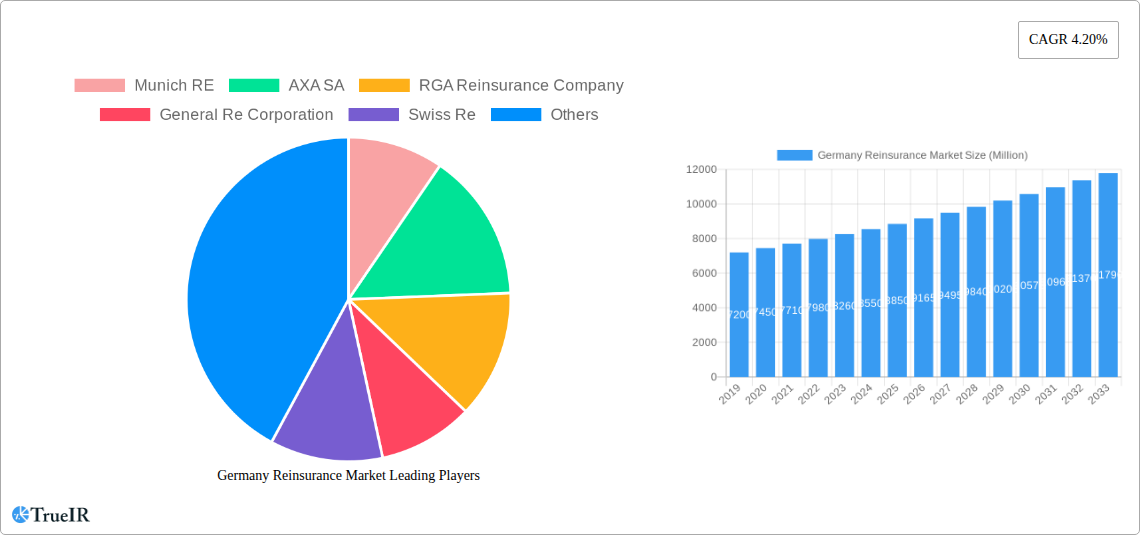

Market segmentation indicates that Treaty Reinsurance holds a leading position due to its comprehensive risk transfer capabilities, followed by Facultative Reinsurance for specific risks. Property & Casualty Reinsurance is expected to dominate applications, driven by heightened exposure to diverse perils, while Life & Health Reinsurance shows strong growth potential. The Broker segment is a primary distribution channel, facilitating connections between reinsurers and primary insurers. However, the Direct channel is growing as large insurers develop in-house reinsurance capabilities. Online engagement is increasing for faster transactions, though offline interactions remain vital for relationship building and complex negotiations. Leading players such as Munich RE, AXA SA, and Swiss Re are investing in innovation and expanding service portfolios to capitalize on these trends within the German reinsurance ecosystem.

Germany Reinsurance Market Company Market Share

Germany Reinsurance Market: Strategic Analysis, Trends, and Future Outlook (2019-2033)

This report offers an in-depth analysis of the German Reinsurance Market, providing actionable insights for stakeholders. The study covers the period from 2019 to 2033, with a base and estimated year of 2025. It explores key market dynamics, dominant segments, emerging opportunities, and the strategic landscape shaped by leading global reinsurers. Optimized with high-volume SEO keywords, this report is designed for enhanced discoverability within the reinsurance industry.

Germany Reinsurance Market Market Structure & Competitive Landscape

The Germany Reinsurance Market is characterized by a moderately concentrated structure, dominated by a few global powerhouses alongside specialized local players. Innovation is a key differentiator, with companies continuously developing sophisticated risk management solutions and embracing digital transformation. Regulatory frameworks play a pivotal role, influencing solvency requirements, capital adequacy, and product offerings, thereby shaping competitive strategies. The presence of product substitutes, while limited in core reinsurance offerings, can manifest in alternative risk transfer mechanisms and capital markets solutions. End-user segmentation by industry and risk type dictates the demand for specialized reinsurance products. Mergers and Acquisitions (M&A) remain a significant aspect of market consolidation and expansion, with recent years witnessing strategic deals aimed at bolstering market share and diversifying portfolios. For instance, the transfer of a significant life and annuity portfolio by AXA Germany in July 2022, valued at an estimated 20.5 Billion USD, underscores the ongoing M&A activity and portfolio rebalancing within the sector. Concentration ratios are closely monitored, and the competitive intensity is driven by both price and service innovation.

- Market Concentration: Dominated by a few large global reinsurers, with significant regional players also present.

- Innovation Drivers: Technological advancements (AI, Big Data), evolving risk landscapes (climate change, cyber threats), and regulatory changes.

- Regulatory Impacts: Stringent Solvency II requirements, data protection laws, and national insurance supervision.

- Product Substitutes: Alternative Risk Transfer (ART) mechanisms, capital markets instruments, and captive insurance.

- End-User Segmentation: Driven by sectors such as automotive, manufacturing, construction, life insurance, and health insurance.

- M&A Trends: Strategic acquisitions, divestitures of non-core assets, and consolidations to achieve economies of scale and market penetration.

Germany Reinsurance Market Market Trends & Opportunities

The Germany Reinsurance Market is poised for robust growth, driven by an increasing demand for sophisticated risk management solutions in a complex and evolving global environment. The market size is projected to expand significantly over the forecast period (2025–2033), fueled by factors such as growing industrialization, rising awareness of insurability for emerging risks, and stringent regulatory mandates that necessitate adequate reinsurance coverage. Technological shifts are profoundly reshaping the industry, with the adoption of artificial intelligence (AI), machine learning, and big data analytics becoming crucial for underwriting, claims processing, and risk modeling. Munich Re's "CertAI" validation service, introduced in May 2022, exemplifies this trend, enabling enhanced client service and market share gains through AI integration. Consumer preferences are also evolving, with a growing demand for tailored and parametric insurance solutions that respond swiftly to specific perils. Competitive dynamics are intense, with established reinsurers focusing on specialization and innovation, while new entrants may leverage digital platforms to offer niche products. The increasing frequency and severity of natural catastrophes, coupled with emerging risks like cyberattacks and pandemics, are creating substantial opportunities for reinsurers to develop innovative products and expand their underwriting capacity. The demand for life and health reinsurance is also expected to rise, driven by an aging population and increased awareness of health-related risks. Furthermore, the ongoing digital transformation presents opportunities for enhanced efficiency, improved customer experience, and the development of new distribution channels. The market penetration rates for advanced reinsurance products are expected to increase as primary insurers seek to optimize their capital allocation and risk appetites.

Dominant Markets & Segments in Germany Reinsurance Market

The Germany Reinsurance Market exhibits distinct dominance across various segments, reflecting the country's economic structure and risk landscape. In terms of Type, Treaty Reinsurance holds a commanding position, driven by the need for broad, ongoing coverage for primary insurers' portfolios. This segment benefits from its ability to provide stable capacity and streamline risk transfer for a wide range of policies, especially within the Property & Casualty sector. Property & Casualty Reinsurance is a cornerstone of the German market, largely due to the country's strong industrial base, extensive infrastructure, and significant exposure to natural perils such as floods and storms. The growth in this segment is directly linked to investments in infrastructure, manufacturing, and the automotive industry, which generate substantial insurable risks.

Dominant Type: Treaty Reinsurance

- Key Growth Drivers: Efficiency in risk management for primary insurers, continuous portfolio coverage, and economies of scale.

- Detailed Analysis: Treaty reinsurance offers automatic coverage for a defined portion of an insurer's business, providing predictable capacity and cost-effectiveness. This is crucial for German insurers seeking to manage the volatility of their extensive property and casualty portfolios, particularly in sectors like manufacturing and engineering where risks are substantial.

Dominant Application: Property & Casualty Reinsurance

- Key Growth Drivers: Robust industrial sector, extensive infrastructure development, increasing frequency of extreme weather events, and evolving cyber risk landscape.

- Detailed Analysis: Germany's position as an industrial powerhouse creates significant exposure to risks like business interruption, product liability, and construction defects. The heightened impact of climate change, leading to more frequent and severe weather events, further amplifies the demand for property and casualty reinsurance. The growing sophistication of cyber threats also necessitates robust reinsurance solutions.

Dominant Distribution Channel: Broker

- Key Growth Drivers: Expertise in complex risk assessment, access to global reinsurance markets, and established relationships with primary insurers.

- Detailed Analysis: Reinsurance brokers play a vital role in navigating the complexities of the reinsurance market. They possess specialized knowledge to identify the optimal reinsurance solutions for primary insurers and negotiate terms with reinsurers, facilitating access to capacity and expertise that might otherwise be unavailable.

Dominant Mode: Offline

- Key Growth Drivers: High degree of personal interaction, complex risk negotiations, and established business practices.

- Detailed Analysis: While online channels are growing, the traditional offline mode, characterized by face-to-face meetings and detailed contractual negotiations, remains dominant due to the intricate nature of reinsurance contracts and the emphasis on building strong, trust-based relationships between brokers, insurers, and reinsurers.

Germany Reinsurance Market Product Analysis

The Germany Reinsurance Market is defined by a range of sophisticated products designed to address diverse risk profiles. Facultative reinsurance provides customized coverage for individual risks, often for large or unusual exposures, offering flexibility to both cedents and reinsurers. Treaty reinsurance, conversely, offers automatic coverage for entire portfolios, providing efficiency and predictable capacity. In terms of application, Property & Casualty Reinsurance is a major segment, encompassing coverage for perils like natural catastrophes, liability, and marine risks, adapting to emerging threats such as cyber and climate change. Life & Health Reinsurance is also significant, catering to demographic shifts, increasing healthcare costs, and the demand for innovative protection products. Technological advancements are driving the development of parametric insurance products, which trigger payouts based on predefined parameters, offering faster claim settlements. Competitive advantages are increasingly derived from data analytics capabilities, risk modeling expertise, and the ability to offer integrated risk management solutions.

Key Drivers, Barriers & Challenges in Germany Reinsurance Market

The Germany Reinsurance Market is propelled by several key drivers. Technological innovation, particularly in AI and data analytics, enhances underwriting accuracy and operational efficiency. Economic growth and industrial expansion create higher insurable values and increased demand for protection. Favorable regulatory environments, while stringent, can also drive the need for adequate reinsurance capacity. Emerging risks, such as climate change and cyber threats, necessitate innovative reinsurance solutions.

Conversely, several barriers and challenges impact market growth. Intense competition among global and regional reinsurers can lead to pricing pressures. Regulatory complexities and evolving compliance requirements demand significant investment in infrastructure and expertise. Supply chain disruptions, particularly those affecting critical industries, can indirectly impact reinsurance demand and claims. The economic climate, including inflation and interest rate fluctuations, also influences investment returns and pricing strategies.

Growth Drivers in the Germany Reinsurance Market Market

The growth of the Germany Reinsurance Market is underpinned by a confluence of critical factors. Technological advancements, especially the adoption of AI and advanced data analytics, are revolutionizing risk assessment, underwriting precision, and claims management, leading to greater efficiency and profitability. Economic resilience and sustained industrial output in Germany create a consistent demand for property and casualty reinsurance to protect significant assets and ongoing operations. The increasing frequency and severity of climate-related events, such as floods and storms, are driving demand for catastrophe reinsurance and innovative weather-risk solutions. Furthermore, evolving regulatory landscapes, while challenging, often necessitate enhanced risk transfer mechanisms, boosting the need for comprehensive reinsurance coverage.

Challenges Impacting Germany Reinsurance Market Growth

Several formidable challenges are impacting the growth trajectory of the Germany Reinsurance Market. The increasing complexity of global risks, including geopolitical instability, pandemics, and escalating cyber threats, presents significant underwriting challenges and can lead to substantial, unpredictable losses. Regulatory burdens, particularly the stringent requirements of Solvency II, necessitate substantial capital allocation and compliance efforts, impacting profitability and operational flexibility. Intense competition from both established global players and agile regional insurers exerts downward pressure on premium rates, potentially squeezing margins. Moreover, the current economic climate, characterized by inflationary pressures and fluctuating interest rates, creates uncertainty for investment returns, a crucial component of reinsurers' profitability. Supply chain vulnerabilities in key German industries can also indirectly affect the volume and nature of insurable risks.

Key Players Shaping the Germany Reinsurance Market Market

- Munich RE

- AXA SA

- RGA Reinsurance Company

- General Re Corporation

- Swiss Re

- Lloyd's

- MAPFRE

- Hannover Re

- Everest Re Group Ltd

- Other Key Players

Significant Germany Reinsurance Market Industry Milestones

- July 2022: AXA Germany agreed to transfer a portfolio of around 900,000 conventional life and annuity insurance contracts worth Euro 19 Billion (20.5 Billion USD) in assets under administration to Athora Germany for a purchase price of Euro 610 million (658.71 Million USD). This strategic divestiture highlights portfolio optimization and M&A activity within the life reinsurance segment.

- May 2022: Munich Re enhanced the acceptance of artificial intelligence (AI) with its new "CertAI" validation service. This initiative aims to improve risk assessment accuracy and efficiency, enabling the company to better cater to clients and gain more market share by offering cutting-edge technological solutions.

Future Outlook for Germany Reinsurance Market Market

The Germany Reinsurance Market is projected for continued growth, driven by an increasing need for sophisticated risk management in the face of evolving global uncertainties. Strategic opportunities lie in the expansion of coverage for emerging risks such as cyber threats, climate change impacts, and supply chain vulnerabilities. The ongoing digital transformation, coupled with the adoption of AI and advanced analytics, will enable reinsurers to offer more tailored products, improve underwriting accuracy, and enhance operational efficiency. The demand for life and health reinsurance is expected to remain robust, influenced by demographic trends and rising healthcare costs. Furthermore, the market will likely witness continued consolidation and strategic partnerships as key players seek to bolster their competitive positions and expand their global reach. The emphasis on sustainability and ESG (Environmental, Social, and Governance) factors will also increasingly shape product development and investment strategies, creating new avenues for growth and innovation.

Germany Reinsurance Market Segmentation

-

1. Type

- 1.1. Facultative Reinsurance

- 1.2. Treaty Reinsurance

-

2. Application

- 2.1. Property & Casualty Reinsurance

- 2.2. Life & Health Reinsurance

-

3. Distribution Channel

- 3.1. Direct

- 3.2. Broker

-

4. Mode

- 4.1. Online

- 4.2. Offline

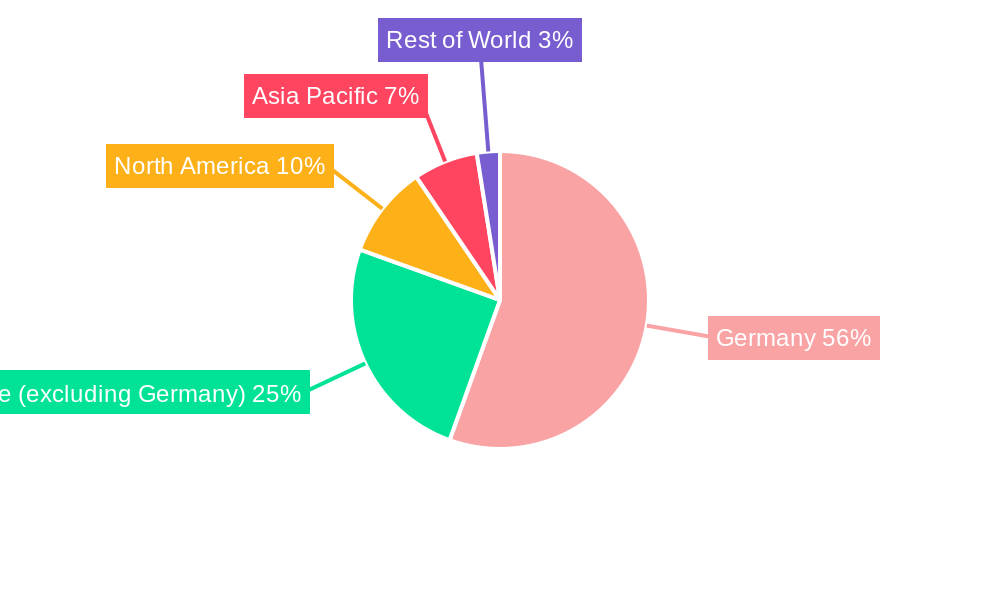

Germany Reinsurance Market Segmentation By Geography

- 1. Germany

Germany Reinsurance Market Regional Market Share

Geographic Coverage of Germany Reinsurance Market

Germany Reinsurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Facultative Reinsurance

- 5.1.2. Treaty Reinsurance

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Property & Casualty Reinsurance

- 5.2.2. Life & Health Reinsurance

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct

- 5.3.2. Broker

- 5.4. Market Analysis, Insights and Forecast - by Mode

- 5.4.1. Online

- 5.4.2. Offline

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Reinsurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Facultative Reinsurance

- 6.1.2. Treaty Reinsurance

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Property & Casualty Reinsurance

- 6.2.2. Life & Health Reinsurance

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Direct

- 6.3.2. Broker

- 6.4. Market Analysis, Insights and Forecast - by Mode

- 6.4.1. Online

- 6.4.2. Offline

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Munich RE

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 AXA SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 RGA Reinsurance Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 General Re Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Swiss Re

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Lloyd's

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MAPFRE

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hannover Re

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Everest Re Group Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Other Key Players**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Munich RE

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Reinsurance Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Germany Reinsurance Market Share (%) by Company 2025

List of Tables

- Table 1: Germany Reinsurance Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Germany Reinsurance Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Germany Reinsurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Germany Reinsurance Market Revenue billion Forecast, by Mode 2020 & 2033

- Table 5: Germany Reinsurance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Germany Reinsurance Market Revenue billion Forecast, by Type 2020 & 2033

- Table 7: Germany Reinsurance Market Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Germany Reinsurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Germany Reinsurance Market Revenue billion Forecast, by Mode 2020 & 2033

- Table 10: Germany Reinsurance Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Reinsurance Market?

The projected CAGR is approximately 10.2%.

2. Which companies are prominent players in the Germany Reinsurance Market?

Key companies in the market include Munich RE, AXA SA, RGA Reinsurance Company, General Re Corporation, Swiss Re, Lloyd's, MAPFRE, Hannover Re, Everest Re Group Ltd, Other Key Players**List Not Exhaustive.

3. What are the main segments of the Germany Reinsurance Market?

The market segments include Type, Application, Distribution Channel, Mode.

4. Can you provide details about the market size?

The market size is estimated to be USD 689.74 billion as of 2022.

5. What are some drivers contributing to market growth?

High Susceptibility for Natural Disasters; High Demand for Specialized Coverage in Insurance.

6. What are the notable trends driving market growth?

Increasing Insurance Claim Across the Region is Driving The Market.

7. Are there any restraints impacting market growth?

High Susceptibility for Natural Disasters; High Demand for Specialized Coverage in Insurance.

8. Can you provide examples of recent developments in the market?

July 2022: AXA Germany agreed to transfer a portfolio of around 900,000 conventional life and annuity insurance contracts worth Euro 19 Billion (20.5 USD billion) in assets under administration to Athora Germany for a purchase price of Euro 610 million (658.71 USD million).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Reinsurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Reinsurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Reinsurance Market?

To stay informed about further developments, trends, and reports in the Germany Reinsurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence