Key Insights

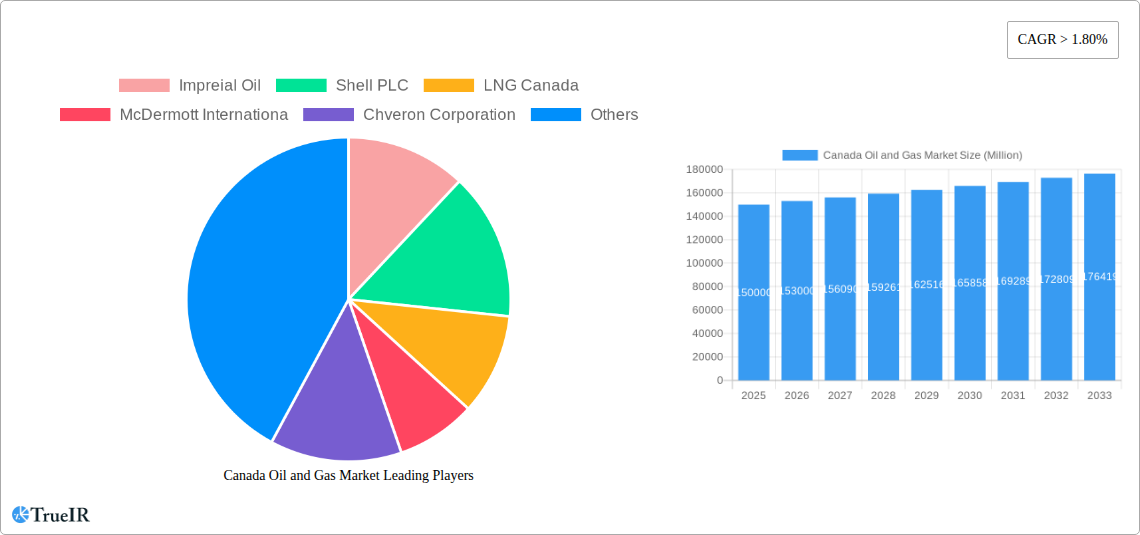

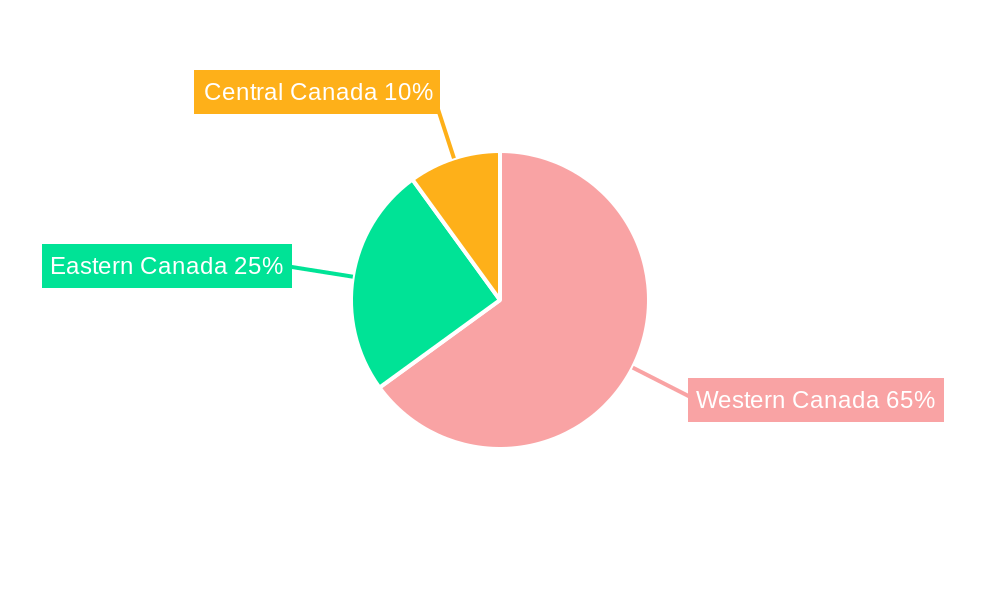

The Canadian oil and gas market, valued at approximately $150 billion in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) exceeding 1.80% from 2025 to 2033. This expansion is fueled by several key drivers. Firstly, consistent global demand for energy, particularly natural gas, continues to support production and investment. Secondly, advancements in extraction technologies, such as enhanced oil recovery techniques, are boosting production efficiency and profitability in established fields. Finally, government initiatives aimed at responsible resource development and energy security contribute to a supportive regulatory environment. The market is segmented into upstream (exploration and production), midstream (transportation and storage), and downstream (refining and marketing) sectors. The upstream sector, driven by substantial oil sands reserves in Alberta, and growing offshore exploration activity in Newfoundland and Labrador, is a significant contributor to overall market value. Western Canada, possessing the bulk of oil sands resources, holds the largest regional market share, followed by Eastern Canada and Central Canada. However, environmental concerns and the increasing adoption of renewable energy sources present notable restraints. Further, fluctuations in global energy prices and geopolitical instability represent considerable challenges to sustained growth. Key players like Imperial Oil, Shell PLC, LNG Canada, and ExxonMobil Corporation are shaping the market through strategic investments and technological innovation. The forecast period (2025-2033) anticipates continued expansion, though at a rate moderated by the aforementioned constraints and the evolving energy landscape.

The competitive landscape is characterized by both large multinational corporations and smaller independent producers. Competition is intense, particularly in the upstream sector, where companies compete for access to resources and production rights. The midstream and downstream segments are also competitive, with companies vying for market share through pipeline infrastructure, refining capacity, and product distribution networks. The evolving energy mix, including the growing importance of renewable energy sources and carbon capture technologies, is shaping the future of the Canadian oil and gas industry. Companies are adapting their strategies to integrate sustainable practices and explore opportunities in carbon-neutral energy solutions. The long-term outlook remains positive, albeit subject to considerable uncertainties associated with global energy demand, climate change policies, and technological advancements. Continued investment in innovation and diversification will be crucial for navigating the challenges and capitalizing on opportunities within this dynamic market.

Canada Oil and Gas Market: A Comprehensive Report (2019-2033)

This dynamic report provides an in-depth analysis of the Canadian oil and gas market, offering invaluable insights for investors, industry professionals, and strategic decision-makers. With a focus on market trends, competitive landscapes, and future projections, this study covers the period from 2019 to 2033, using 2025 as the base and estimated year. The report leverages extensive data analysis to deliver a comprehensive understanding of this crucial sector.

Canada Oil and Gas Market Structure & Competitive Landscape

This section analyzes the market concentration, innovation drivers, regulatory landscape, product substitutes, end-user segmentation, and merger and acquisition (M&A) activity within the Canadian oil and gas industry. The market is characterized by a relatively concentrated structure, with a few major players dominating the upstream, midstream, and downstream segments. However, the presence of numerous smaller players, particularly in specialized areas and niche markets, contributes to a dynamic competitive landscape.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) for the Canadian oil and gas market is estimated at xx in 2025, indicating a moderately concentrated market. This is influenced by the significant presence of integrated energy companies and national oil companies.

- Innovation Drivers: Technological advancements in extraction technologies (e.g., hydraulic fracturing, enhanced oil recovery), pipeline infrastructure, and refining processes are key drivers of innovation. The pursuit of environmental sustainability is also spurring innovation in carbon capture, utilization, and storage (CCUS) technologies.

- Regulatory Impacts: Government regulations concerning emissions, environmental protection, and resource management significantly influence industry operations and investment decisions. These regulations are constantly evolving, creating both challenges and opportunities for market players.

- Product Substitutes: The growing adoption of renewable energy sources poses a significant challenge to the traditional oil and gas industry. However, natural gas is increasingly positioned as a transition fuel, benefiting from its lower carbon emissions compared to coal and oil.

- End-User Segmentation: The end-user segments for oil and gas products include transportation, power generation, industrial processes, and residential heating. Demand variations across these segments influence overall market dynamics.

- M&A Trends: The Canadian oil and gas market has experienced a moderate level of M&A activity in recent years, driven by factors such as consolidation, cost optimization, and access to new resources. The total value of M&A transactions in the sector during the historical period (2019-2024) was approximately xx Million.

Canada Oil and Gas Market Trends & Opportunities

The Canadian oil and gas market exhibits a complex interplay of trends and opportunities. Market size has experienced fluctuating growth, influenced by global energy demand, commodity prices, and environmental concerns. Technological advancements, particularly in unconventional resource extraction, are transforming the industry. Consumer preferences, shifting towards cleaner energy sources, necessitate a strategic adaptation by oil and gas companies. Competitive dynamics are characterized by both cooperation and competition, with companies engaging in strategic partnerships and acquisitions to enhance their market positions.

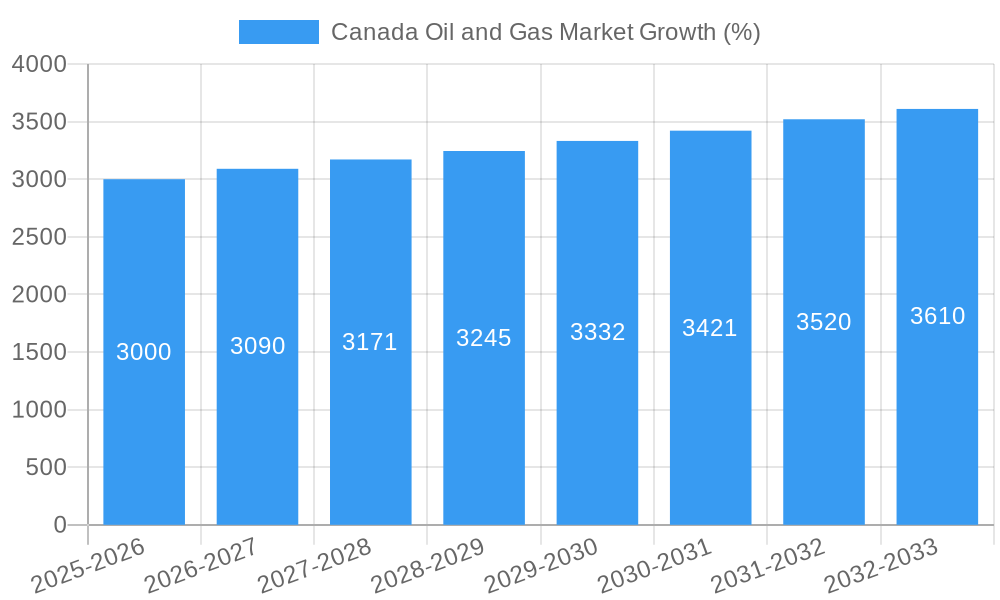

The Compound Annual Growth Rate (CAGR) for the market is projected at xx% during the forecast period (2025-2033). Market penetration rates for various products and services vary significantly depending on factors such as regional variations, technological adoption, and policy incentives. The market is also seeing increased investment in technologies that reduce greenhouse gas emissions, such as carbon capture and storage.

Dominant Markets & Segments in Canada Oil and Gas Market

The Canadian oil and gas market exhibits regional variations in activity and dominance across its upstream, midstream, and downstream segments.

- Upstream: Alberta continues to be the dominant province in upstream activities, accounting for the largest share of oil and gas production. Key growth drivers include:

- Extensive oil sands reserves.

- Ongoing technological advancements in extraction techniques.

- Government policies supporting resource development (although this is subject to change and increasing scrutiny).

- Midstream: The midstream sector, encompassing pipelines, processing plants, and storage facilities, is geographically distributed, reflecting the location of upstream production and downstream demand centers.

- Strategic pipeline infrastructure expansions are key to growth in this segment.

- Regulatory approvals and environmental considerations play a significant role in project development.

- Downstream: Refining and petrochemical production are primarily concentrated in Ontario and Quebec, serving Eastern Canadian markets.

- Proximity to major population centers drives demand.

- Investments in refinery upgrades and expansion are impacting the sector's growth.

Canada Oil and Gas Market Product Analysis

The Canadian oil and gas market encompasses a diverse range of products, from crude oil and natural gas to refined petroleum products and petrochemicals. Recent technological advancements have improved extraction efficiency, enhanced product quality, and enabled the development of new applications. For example, the increasing use of natural gas in power generation and the development of advanced biofuels are significant examples of product innovation and market fit. Competition in this area is intense, with companies constantly seeking to differentiate their offerings through innovation and efficiency improvements.

Key Drivers, Barriers & Challenges in Canada Oil and Gas Market

Key Drivers:

- Increasing global energy demand, particularly in developing economies, provides a significant driver.

- Technological advancements in extraction, processing, and transportation enhance efficiency and reduce costs.

- Government policies supporting resource development (although this support is becoming increasingly conditional).

Challenges:

- Fluctuating global energy prices pose substantial risks to the industry's profitability and investment decisions.

- Stringent environmental regulations necessitate significant capital expenditure on emission reduction technologies, potentially impacting profitability.

- The growing adoption of renewable energy sources is increasing competitive pressure and challenging the long-term viability of fossil fuels. The projected impact of this is estimated at xx Million in lost revenue by 2033.

Growth Drivers in the Canada Oil and Gas Market Market

The Canadian oil and gas market growth is propelled by several factors, including sustained global energy demand, technological advancements leading to cost-effective extraction from unconventional sources, and government support, though increasingly conditional on environmental performance. Increased investment in pipeline infrastructure, aimed at diversifying export routes, also contributes to growth.

Challenges Impacting Canada Oil and Gas Market Growth

Significant challenges hinder the growth of the Canadian oil and gas market. These include volatile global commodity prices, stringent environmental regulations leading to higher operational costs and project delays, and increasing competitive pressures from renewable energy sources. Supply chain disruptions, exacerbated by geopolitical instability, also contribute to uncertainties in production and investment.

Key Players Shaping the Canada Oil and Gas Market Market

- Imperial Oil

- Shell PLC

- LNG Canada

- McDermott International

- Chevron Corporation

- Halliburton

- Petroliam Nasional Berhad (PETRONAS)

- ExxonMobil Corporation

- Total Energies SE

Significant Canada Oil and Gas Market Industry Milestones

- March 2022: Pembina Pipeline Corp. and KKR formed a joint venture for western Canadian natural gas processing assets. This signifies consolidation and increased investment in midstream infrastructure.

- November 2021: Woodfibre LNG awarded an EPFC contract to McDermott International, marking a significant step forward in LNG project development. This demonstrates confidence in future LNG demand and the expansion of export capabilities.

Future Outlook for Canada Oil and Gas Market Market

The Canadian oil and gas market faces a period of significant transformation. While continued global energy demand will support production, the sector must adapt to increasing pressure to reduce emissions and enhance environmental performance. Strategic investments in CCUS technologies, diversification of energy sources, and a focus on operational efficiency will be crucial for sustainable growth. The market's future potential depends on its ability to navigate the challenges posed by climate change policies and competition from renewable energy.

Canada Oil and Gas Market Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

Canada Oil and Gas Market Segmentation By Geography

- 1. Canada

Canada Oil and Gas Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 1.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Modernization and Upgrades of Existing Military Aircraft Fleets4.; Increasing Defense Budgets

- 3.3. Market Restrains

- 3.3.1. 4.; Shift Toward Unmanned Aircraft

- 3.4. Market Trends

- 3.4.1. Upstream Sector to be the Fastest Growing Sector

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Oil and Gas Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Eastern Canada Canada Oil and Gas Market Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Oil and Gas Market Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Oil and Gas Market Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Impreial Oil

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Shell PLC

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 LNG Canada

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 McDermott Internationa

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Chveron Corporation

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Halliburton

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Petroliam Nasional Berhad (PETRONAS)

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Exxonmobil Corporation

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Total Energies SE

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.1 Impreial Oil

List of Figures

- Figure 1: Canada Oil and Gas Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Oil and Gas Market Share (%) by Company 2024

List of Tables

- Table 1: Canada Oil and Gas Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Oil and Gas Market Volume Tonnes Forecast, by Region 2019 & 2032

- Table 3: Canada Oil and Gas Market Revenue Million Forecast, by Sector 2019 & 2032

- Table 4: Canada Oil and Gas Market Volume Tonnes Forecast, by Sector 2019 & 2032

- Table 5: Canada Oil and Gas Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Canada Oil and Gas Market Volume Tonnes Forecast, by Region 2019 & 2032

- Table 7: Canada Oil and Gas Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Canada Oil and Gas Market Volume Tonnes Forecast, by Country 2019 & 2032

- Table 9: Eastern Canada Canada Oil and Gas Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Eastern Canada Canada Oil and Gas Market Volume (Tonnes) Forecast, by Application 2019 & 2032

- Table 11: Western Canada Canada Oil and Gas Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Western Canada Canada Oil and Gas Market Volume (Tonnes) Forecast, by Application 2019 & 2032

- Table 13: Central Canada Canada Oil and Gas Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Central Canada Canada Oil and Gas Market Volume (Tonnes) Forecast, by Application 2019 & 2032

- Table 15: Canada Oil and Gas Market Revenue Million Forecast, by Sector 2019 & 2032

- Table 16: Canada Oil and Gas Market Volume Tonnes Forecast, by Sector 2019 & 2032

- Table 17: Canada Oil and Gas Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Canada Oil and Gas Market Volume Tonnes Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Oil and Gas Market?

The projected CAGR is approximately > 1.80%.

2. Which companies are prominent players in the Canada Oil and Gas Market?

Key companies in the market include Impreial Oil, Shell PLC, LNG Canada, McDermott Internationa, Chveron Corporation, Halliburton, Petroliam Nasional Berhad (PETRONAS), Exxonmobil Corporation, Total Energies SE.

3. What are the main segments of the Canada Oil and Gas Market?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Modernization and Upgrades of Existing Military Aircraft Fleets4.; Increasing Defense Budgets.

6. What are the notable trends driving market growth?

Upstream Sector to be the Fastest Growing Sector.

7. Are there any restraints impacting market growth?

4.; Shift Toward Unmanned Aircraft.

8. Can you provide examples of recent developments in the market?

In March 2022, Pembina Pipeline Corp. announced a deal with private equity firm KKR to combine their western Canadian natural gas processing assets into a new joint venture. Pembina will own a 60% stake in the joint venture and serve as the operator and manager. KKR's global infrastructure funds will hold 40%.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Oil and Gas Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Oil and Gas Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Oil and Gas Market?

To stay informed about further developments, trends, and reports in the Canada Oil and Gas Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence