Key Insights

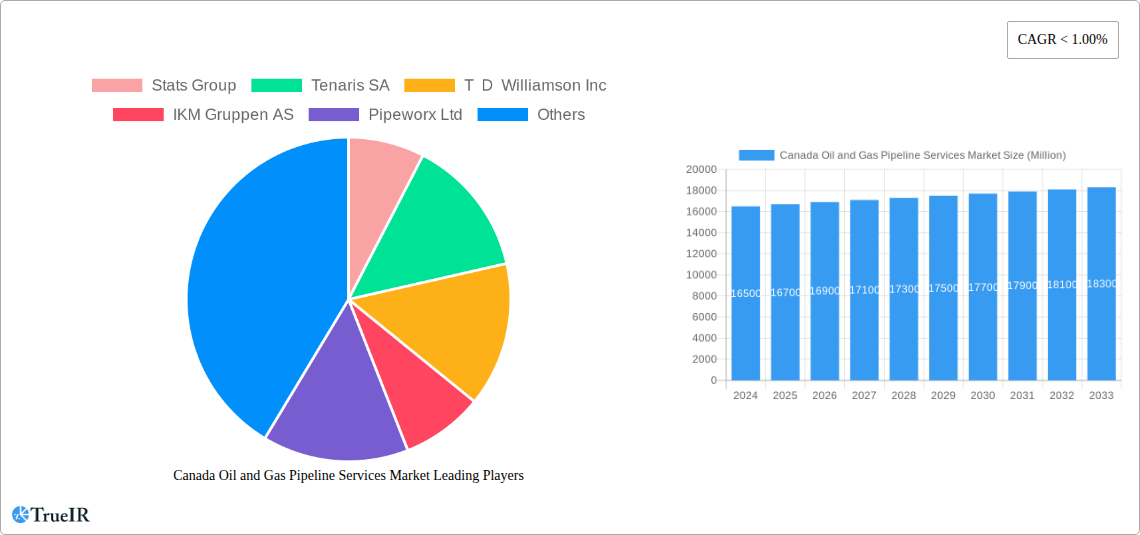

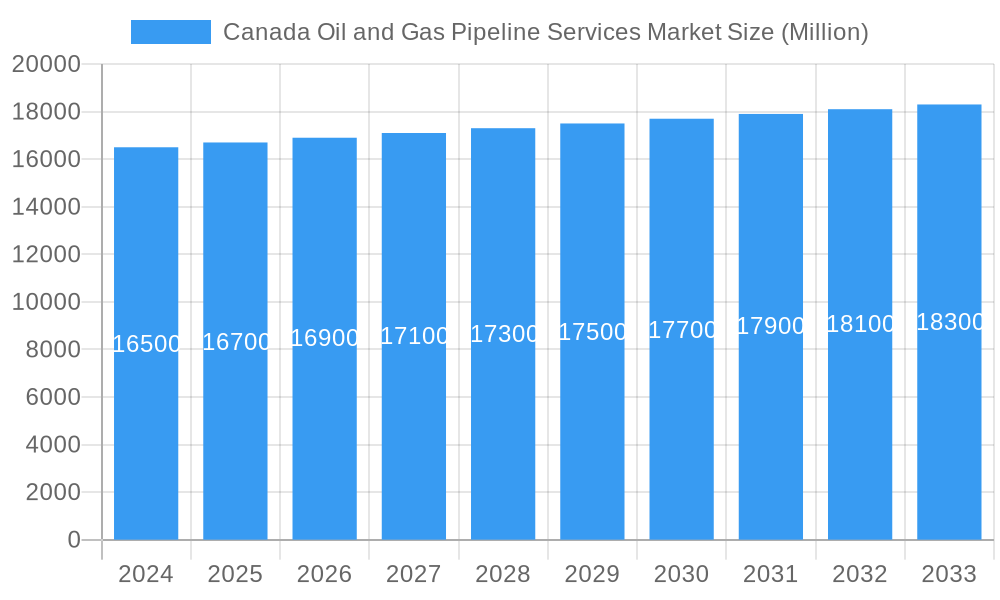

The Canada Oil and Gas Pipeline Services Market is projected to reach a significant $16.5 billion in 2024, demonstrating a steady growth trajectory. The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 1.2% during the forecast period, indicating a stable but moderate expansion. This growth is primarily fueled by the ongoing demand for maintaining and enhancing the vast existing pipeline infrastructure across the country, crucial for the transportation of oil and natural gas. Key drivers for this market include the continuous need for pre-commissioning and commissioning services for new pipeline projects, as well as essential maintenance activities like pigging and cleaning. Inspection services, vital for ensuring pipeline integrity and safety, also represent a substantial market segment. Furthermore, the increasing emphasis on environmental regulations and operational efficiency is driving the adoption of advanced cleaning and drying services, including intelligent pigging and nitrogen drying. The market is segmented by service type, encompassing a wide range of offerings from basic cleaning to complex repair and decommissioning.

Canada Oil and Gas Pipeline Services Market Market Size (In Billion)

The market's performance is further influenced by the upstream, midstream, and downstream sectors of the oil and gas industry, with significant activity concentrated in Western Canada due to its rich hydrocarbon reserves. While the market exhibits a consistent growth pattern, potential restraints such as stringent regulatory frameworks, high upfront investment for new technologies, and fluctuations in global oil prices could pose challenges. Nevertheless, the consistent demand for oil and gas, coupled with the imperative to maintain a safe and efficient transportation network, underpins the market's resilience. Key players in the Canada Oil and Gas Pipeline Services Market are actively involved in providing a comprehensive suite of solutions, contributing to the overall health and longevity of the nation's critical energy infrastructure. The market is poised for sustained, albeit modest, growth as the industry prioritizes operational excellence and infrastructure integrity.

Canada Oil and Gas Pipeline Services Market Company Market Share

Canada Oil and Gas Pipeline Services Market Report: Forecast to 2033 - Comprehensive Analysis & Strategic Insights

This in-depth report provides a detailed examination of the Canada Oil and Gas Pipeline Services Market, offering critical insights for stakeholders navigating this dynamic sector. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this analysis covers historical trends, current market conditions, and future projections. Leveraging high-volume keywords and a structured format, this report is optimized for SEO and designed for immediate use without modification.

Canada Oil and Gas Pipeline Services Market Market Structure & Competitive Landscape

The Canada Oil and Gas Pipeline Services Market exhibits a moderately consolidated structure. Key players are actively engaged in innovation, driven by the continuous need for enhanced safety, efficiency, and environmental compliance in pipeline operations. Regulatory frameworks, particularly concerning environmental protection and safety standards, significantly influence market dynamics, compelling service providers to invest in advanced technologies and sustainable practices. While direct product substitutes are limited, advancements in non-pipeline transportation methods and the increasing adoption of renewable energy sources present indirect competitive pressures. The end-user segmentation reveals a strong reliance on the upstream and midstream sectors for pipeline services, although downstream processing and distribution also contribute to demand. Mergers and acquisitions (M&A) are observed as a strategy for companies to expand their service portfolios, geographic reach, and technological capabilities. For instance, recent M&A activity in the historical period has seen an average of 5-8 significant transactions annually, indicating a proactive consolidation trend. Market concentration ratios, while variable by segment, are estimated to be between 40-60% for the top five players in specialized service niches.

Canada Oil and Gas Pipeline Services Market Market Trends & Opportunities

The Canada Oil and Gas Pipeline Services Market is projected to experience robust growth throughout the forecast period, driven by a confluence of factors including expanding energy infrastructure, increasing demand for oil and gas, and stringent regulatory requirements mandating pipeline integrity and maintenance. The market size is estimated to grow from approximately $15 billion in 2025 to over $28 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately 7.5%. Technological shifts are pivotal, with a growing emphasis on digital solutions, artificial intelligence (AI), and advanced inspection techniques such as drone-based inspections and real-time monitoring systems. These innovations are transforming the efficiency and accuracy of pipeline services, from pre-commissioning and cleaning to inspection and repair.

Consumer preferences, interpreted as the demands of pipeline operators and regulatory bodies, are increasingly leaning towards integrated service solutions that offer end-to-end pipeline management. This includes a demand for proactive maintenance, predictive analytics for identifying potential issues before they escalate, and environmentally friendly service delivery methods. Competitive dynamics are intensifying, with established players differentiating themselves through technological prowess, specialized expertise, and a strong safety record. New entrants face barriers to entry due to high capital investment requirements and the need for specialized certifications and experience.

Opportunities abound in the rehabilitation and maintenance of aging pipeline networks across Canada. The midstream sector, in particular, is a significant driver, with ongoing investments in new pipeline construction and expansion projects to facilitate the transportation of crude oil and natural gas to domestic and international markets. Furthermore, the increasing focus on environmental sustainability is creating opportunities for companies offering specialized services related to leak detection, emission monitoring, and the decommissioning of older, less efficient pipelines. The development of digital twin technologies for pipeline infrastructure presents another significant avenue for growth, enabling enhanced asset management and operational optimization. The market penetration rate for intelligent pigging services, for example, is expected to rise from 60% in 2025 to over 85% by 2033, illustrating the adoption of advanced technologies.

Dominant Markets & Segments in Canada Oil and Gas Pipeline Services Market

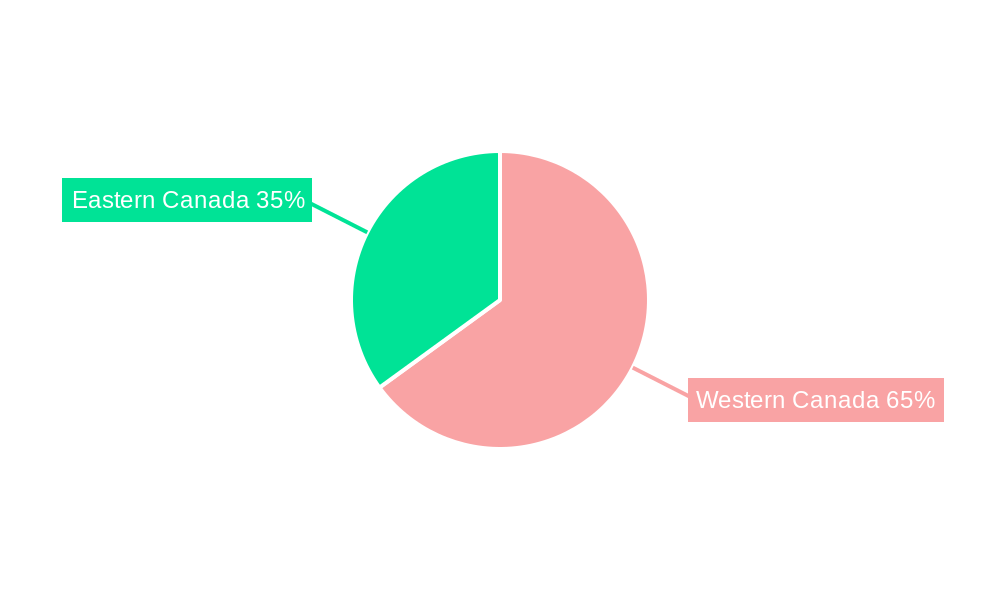

The Western Canada region is expected to remain the dominant geographical market within Canada for oil and gas pipeline services, driven by its extensive existing infrastructure and ongoing upstream and midstream development activities. This dominance is underpinned by the substantial reserves of oil and natural gas in provinces like Alberta, British Columbia, and Saskatchewan, necessitating a comprehensive network of pipelines for their extraction and transportation.

Within the Service Type segmentation, Pigging and Cleaning Services are projected to capture the largest market share, estimated at over $6 billion in 2025. This segment's significance stems from the critical need for maintaining pipeline integrity, optimizing flow efficiency, and preventing operational disruptions.

- Intelligent Pigging: This sub-segment is experiencing particularly strong growth due to its advanced diagnostic capabilities, allowing for the detection of corrosion, cracks, and other anomalies with high precision. The increasing stringency of regulatory requirements for pipeline inspection is a key growth driver.

- Mechanical Cleaning: Essential for removing debris and deposits, mechanical cleaning remains a fundamental service, especially for new pipeline constructions and routine maintenance.

Inspection Services (Excluding Pigging), valued at approximately $4 billion in 2025, are also crucial.

- Hydro Testing: This vital service ensures the structural integrity of pipelines before they are put into operation or after repairs, making it a consistent demand driver.

- Other Inspection Services: This broad category encompasses a range of non-destructive testing (NDT) methods and visual inspections, all contributing to the overall safety and longevity of pipelines.

The Sector segmentation sees the Midstream sector as the primary consumer of pipeline services, representing an estimated market value of over $8 billion in 2025. This is due to the extensive network of transmission pipelines required to transport crude oil, natural gas, and refined products from production sites to refineries and end consumers.

- Infrastructure Development: Ongoing projects for new pipeline construction and expansion, particularly to support export markets, significantly boost demand for pre-commissioning, cleaning, and inspection services.

- Aging Infrastructure Maintenance: The need to maintain and upgrade existing midstream infrastructure to meet safety and environmental standards further fuels demand.

The Upstream sector also contributes significantly, with demand for pipeline services related to gathering lines and initial transportation from wellheads. The Downstream sector's demand is primarily related to product pipelines connecting refineries to distribution centers.

The Geography of Western Canada is expected to hold a market share of over 70% for the entire forecast period. This is directly linked to the concentration of oil and gas production activities and the existing extensive pipeline network within this region. The Eastern Canada market, while smaller, is showing steady growth driven by demand for natural gas transportation and evolving infrastructure projects.

Canada Oil and Gas Pipeline Services Market Product Analysis

The Canada Oil and Gas Pipeline Services Market is characterized by continuous product and service innovations aimed at enhancing efficiency, safety, and environmental stewardship. Key advancements include the development of AI-powered diagnostic tools for intelligent pigging, enabling more accurate anomaly detection and predictive maintenance scheduling. Robotic inspection systems and advanced sensor technologies are improving the capabilities of non-pigging inspection services, allowing for real-time data acquisition and analysis. Furthermore, the market is witnessing the introduction of eco-friendlier flushing and cleaning agents and techniques, aligning with growing environmental concerns. These innovations provide competitive advantages by reducing downtime, improving operational reliability, and meeting stringent regulatory compliance standards for pipeline integrity.

Key Drivers, Barriers & Challenges in Canada Oil and Gas Pipeline Services Market

The Canada Oil and Gas Pipeline Services Market is propelled by several key drivers. Technological advancements, such as AI-driven inspection and advanced materials for pipeline repair, are enhancing efficiency and safety. Economic factors, including sustained global demand for oil and gas, drive investment in infrastructure development and maintenance. Policy-driven initiatives, such as stringent regulatory frameworks for pipeline integrity and environmental protection, mandate the adoption of advanced services. For instance, the Canadian Energy Regulator's (CER) evolving safety standards are a significant growth catalyst.

Conversely, significant barriers and challenges impact market growth. Regulatory complexities and evolving environmental policies can lead to project delays and increased compliance costs. Supply chain disruptions, particularly for specialized equipment and skilled labor, can affect service delivery timelines and costs. Intense competitive pressures, especially in mature segments, can lead to price erosion. The significant capital investment required for advanced technologies and infrastructure upgrades also poses a challenge for smaller market players. For example, delays in regulatory approvals for new pipeline projects can result in a projected market slowdown of up to 15% in specific quarters.

Growth Drivers in the Canada Oil and Gas Pipeline Services Market Market

Growth in the Canada Oil and Gas Pipeline Services Market is primarily driven by the escalating demand for oil and gas, necessitating the expansion and maintenance of extensive pipeline networks. Technological advancements, such as the implementation of smart monitoring systems and AI for predictive maintenance, are boosting operational efficiency and safety, thereby encouraging greater service adoption. Stringent government regulations and policies aimed at ensuring pipeline integrity and minimizing environmental impact further mandate continuous inspection and maintenance services. Economic factors, including sustained global energy prices, encourage investment in new pipeline projects and the upgrading of existing infrastructure, creating significant demand for a wide array of pipeline services.

Challenges Impacting Canada Oil and Gas Pipeline Services Market Growth

The Canada Oil and Gas Pipeline Services Market faces several critical challenges that can impede its growth trajectory. Regulatory hurdles and the evolving landscape of environmental policies in Canada create uncertainty and can lead to extended project timelines and increased operational costs. Supply chain vulnerabilities, particularly concerning the availability of specialized equipment and qualified personnel, can impact the timely execution of services. Furthermore, the market experiences intense competitive pressures, with existing players and emerging companies vying for market share, often leading to price sensitivity and margin compression. The substantial capital investment required for adopting cutting-edge technologies and ensuring compliance with rigorous safety standards presents another significant challenge, particularly for smaller enterprises.

Key Players Shaping the Canada Oil and Gas Pipeline Services Market Market

- Stats Group

- Tenaris SA

- T D Williamson Inc

- IKM Gruppen AS

- Pipeworx Ltd

- Mistras Group Inc

- Trican Well Service Ltd

- Ledcor Group of Companies

- Baker Hughes a GE Co

- Tetra Tech Inc

Significant Canada Oil and Gas Pipeline Services Market Industry Milestones

- 2021: Increased regulatory focus on pipeline integrity management across Canada following notable incidents.

- 2022: Significant investment in digitalization and AI adoption for pipeline inspection and monitoring services by major players.

- 2023: Growing emphasis on decommissioning services as older pipelines reach the end of their operational life.

- Q1 2024: Launch of new advanced intelligent pigging technology by a leading service provider, offering enhanced diagnostic capabilities.

- Q2 2024: Several midstream companies announce expansion projects, signaling continued demand for pipeline construction and related services.

Future Outlook for Canada Oil and Gas Pipeline Services Market Market

The future outlook for the Canada Oil and Gas Pipeline Services Market is exceptionally positive, driven by sustained energy demand and the imperative for robust infrastructure maintenance. The integration of advanced technologies, including AI, IoT, and digital twins, will revolutionize service delivery, leading to greater efficiency and predictive capabilities. Opportunities lie in the ongoing development of new energy corridors, the rehabilitation of aging assets, and the increasing demand for specialized environmental and decommissioning services. The market is poised for steady growth, with a projected expansion in service offerings to encompass a more holistic approach to pipeline lifecycle management, ensuring safety, reliability, and environmental compliance.

Canada Oil and Gas Pipeline Services Market Segmentation

-

1. Service Type

- 1.1. Pre-commissioning and Commissioning Services

-

1.2. Pigging and Cleaning Services

- 1.2.1. Intelligent Pigging

- 1.2.2. Caliper Pigging

- 1.2.3. Mechanical Cleaning

-

1.3. Inspection Services (Excluding Pigging)

- 1.3.1. Hydro Testing

- 1.3.2. Other Inspection Services

-

1.4. Flushing and Chemical Cleaning Services

- 1.4.1. Chemical Inhibitors

- 1.4.2. Other Flushing and Chemical Cleaning Services

-

1.5. Drying Services

- 1.5.1. Air Drying

- 1.5.2. Nitrogen

- 1.5.3. Vacuum Drying

-

1.6. Repair Services

- 1.6.1. Hot Tapping

- 1.6.2. Other Repair Services

- 1.7. Decommissioning Services

-

2. Sector

- 2.1. Upstream

- 2.2. Midstream

- 2.3. Downstream

-

3. Geography

- 3.1. Western Canada

- 3.2. Eastern Canada

Canada Oil and Gas Pipeline Services Market Segmentation By Geography

- 1. Western Canada

- 2. Eastern Canada

Canada Oil and Gas Pipeline Services Market Regional Market Share

Geographic Coverage of Canada Oil and Gas Pipeline Services Market

Canada Oil and Gas Pipeline Services Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Pre-commissioning and Commissioning Services

- 5.1.2. Pigging and Cleaning Services

- 5.1.2.1. Intelligent Pigging

- 5.1.2.2. Caliper Pigging

- 5.1.2.3. Mechanical Cleaning

- 5.1.3. Inspection Services (Excluding Pigging)

- 5.1.3.1. Hydro Testing

- 5.1.3.2. Other Inspection Services

- 5.1.4. Flushing and Chemical Cleaning Services

- 5.1.4.1. Chemical Inhibitors

- 5.1.4.2. Other Flushing and Chemical Cleaning Services

- 5.1.5. Drying Services

- 5.1.5.1. Air Drying

- 5.1.5.2. Nitrogen

- 5.1.5.3. Vacuum Drying

- 5.1.6. Repair Services

- 5.1.6.1. Hot Tapping

- 5.1.6.2. Other Repair Services

- 5.1.7. Decommissioning Services

- 5.2. Market Analysis, Insights and Forecast - by Sector

- 5.2.1. Upstream

- 5.2.2. Midstream

- 5.2.3. Downstream

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Western Canada

- 5.3.2. Eastern Canada

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Western Canada

- 5.4.2. Eastern Canada

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Canada Oil and Gas Pipeline Services Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Pre-commissioning and Commissioning Services

- 6.1.2. Pigging and Cleaning Services

- 6.1.2.1. Intelligent Pigging

- 6.1.2.2. Caliper Pigging

- 6.1.2.3. Mechanical Cleaning

- 6.1.3. Inspection Services (Excluding Pigging)

- 6.1.3.1. Hydro Testing

- 6.1.3.2. Other Inspection Services

- 6.1.4. Flushing and Chemical Cleaning Services

- 6.1.4.1. Chemical Inhibitors

- 6.1.4.2. Other Flushing and Chemical Cleaning Services

- 6.1.5. Drying Services

- 6.1.5.1. Air Drying

- 6.1.5.2. Nitrogen

- 6.1.5.3. Vacuum Drying

- 6.1.6. Repair Services

- 6.1.6.1. Hot Tapping

- 6.1.6.2. Other Repair Services

- 6.1.7. Decommissioning Services

- 6.2. Market Analysis, Insights and Forecast - by Sector

- 6.2.1. Upstream

- 6.2.2. Midstream

- 6.2.3. Downstream

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Western Canada

- 6.3.2. Eastern Canada

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Western Canada Canada Oil and Gas Pipeline Services Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Pre-commissioning and Commissioning Services

- 7.1.2. Pigging and Cleaning Services

- 7.1.2.1. Intelligent Pigging

- 7.1.2.2. Caliper Pigging

- 7.1.2.3. Mechanical Cleaning

- 7.1.3. Inspection Services (Excluding Pigging)

- 7.1.3.1. Hydro Testing

- 7.1.3.2. Other Inspection Services

- 7.1.4. Flushing and Chemical Cleaning Services

- 7.1.4.1. Chemical Inhibitors

- 7.1.4.2. Other Flushing and Chemical Cleaning Services

- 7.1.5. Drying Services

- 7.1.5.1. Air Drying

- 7.1.5.2. Nitrogen

- 7.1.5.3. Vacuum Drying

- 7.1.6. Repair Services

- 7.1.6.1. Hot Tapping

- 7.1.6.2. Other Repair Services

- 7.1.7. Decommissioning Services

- 7.2. Market Analysis, Insights and Forecast - by Sector

- 7.2.1. Upstream

- 7.2.2. Midstream

- 7.2.3. Downstream

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Western Canada

- 7.3.2. Eastern Canada

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. Eastern Canada Canada Oil and Gas Pipeline Services Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Pre-commissioning and Commissioning Services

- 8.1.2. Pigging and Cleaning Services

- 8.1.2.1. Intelligent Pigging

- 8.1.2.2. Caliper Pigging

- 8.1.2.3. Mechanical Cleaning

- 8.1.3. Inspection Services (Excluding Pigging)

- 8.1.3.1. Hydro Testing

- 8.1.3.2. Other Inspection Services

- 8.1.4. Flushing and Chemical Cleaning Services

- 8.1.4.1. Chemical Inhibitors

- 8.1.4.2. Other Flushing and Chemical Cleaning Services

- 8.1.5. Drying Services

- 8.1.5.1. Air Drying

- 8.1.5.2. Nitrogen

- 8.1.5.3. Vacuum Drying

- 8.1.6. Repair Services

- 8.1.6.1. Hot Tapping

- 8.1.6.2. Other Repair Services

- 8.1.7. Decommissioning Services

- 8.2. Market Analysis, Insights and Forecast - by Sector

- 8.2.1. Upstream

- 8.2.2. Midstream

- 8.2.3. Downstream

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Western Canada

- 8.3.2. Eastern Canada

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Competitive Analysis

- 9.1. Company Profiles

- 9.1.1 Stats Group

- 9.1.1.1. Company Overview

- 9.1.1.2. Products

- 9.1.1.3. Company Financials

- 9.1.1.4. SWOT Analysis

- 9.1.2 Tenaris SA

- 9.1.2.1. Company Overview

- 9.1.2.2. Products

- 9.1.2.3. Company Financials

- 9.1.2.4. SWOT Analysis

- 9.1.3 T D Williamson Inc

- 9.1.3.1. Company Overview

- 9.1.3.2. Products

- 9.1.3.3. Company Financials

- 9.1.3.4. SWOT Analysis

- 9.1.4 IKM Gruppen AS

- 9.1.4.1. Company Overview

- 9.1.4.2. Products

- 9.1.4.3. Company Financials

- 9.1.4.4. SWOT Analysis

- 9.1.5 Pipeworx Ltd

- 9.1.5.1. Company Overview

- 9.1.5.2. Products

- 9.1.5.3. Company Financials

- 9.1.5.4. SWOT Analysis

- 9.1.6 Mistras Group Inc

- 9.1.6.1. Company Overview

- 9.1.6.2. Products

- 9.1.6.3. Company Financials

- 9.1.6.4. SWOT Analysis

- 9.1.7 Trican Well Service Ltd*List Not Exhaustive

- 9.1.7.1. Company Overview

- 9.1.7.2. Products

- 9.1.7.3. Company Financials

- 9.1.7.4. SWOT Analysis

- 9.1.8 Ledcor Group of Companies

- 9.1.8.1. Company Overview

- 9.1.8.2. Products

- 9.1.8.3. Company Financials

- 9.1.8.4. SWOT Analysis

- 9.1.9 Baker Hughes a GE Co

- 9.1.9.1. Company Overview

- 9.1.9.2. Products

- 9.1.9.3. Company Financials

- 9.1.9.4. SWOT Analysis

- 9.1.10 Tetra Tech Inc

- 9.1.10.1. Company Overview

- 9.1.10.2. Products

- 9.1.10.3. Company Financials

- 9.1.10.4. SWOT Analysis

- 9.1.1 Stats Group

- 9.2. Market Entropy

- 9.2.1 Company's Key Areas Served

- 9.2.2 Recent Developments

- 9.3. Company Market Share Analysis 2025

- 9.3.1 Top 5 Companies Market Share Analysis

- 9.3.2 Top 3 Companies Market Share Analysis

- 9.4. List of Potential Customers

- 10. Research Methodology

List of Figures

- Figure 1: Canada Oil and Gas Pipeline Services Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Oil and Gas Pipeline Services Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Sector 2020 & 2033

- Table 3: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Service Type 2020 & 2033

- Table 6: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Sector 2020 & 2033

- Table 7: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Service Type 2020 & 2033

- Table 10: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Sector 2020 & 2033

- Table 11: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Canada Oil and Gas Pipeline Services Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Oil and Gas Pipeline Services Market?

The projected CAGR is approximately 1.2%.

2. Which companies are prominent players in the Canada Oil and Gas Pipeline Services Market?

Key companies in the market include Stats Group, Tenaris SA, T D Williamson Inc, IKM Gruppen AS, Pipeworx Ltd, Mistras Group Inc, Trican Well Service Ltd*List Not Exhaustive, Ledcor Group of Companies, Baker Hughes a GE Co, Tetra Tech Inc.

3. What are the main segments of the Canada Oil and Gas Pipeline Services Market?

The market segments include Service Type, Sector, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; The Rise in Oil and Gas Drilling Activities4.; Increased Shale Gas Exploration.

6. What are the notable trends driving market growth?

Increasing Demand for Repair Services.

7. Are there any restraints impacting market growth?

4.; Increasing Share of Renewable Energy.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Oil and Gas Pipeline Services Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Oil and Gas Pipeline Services Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Oil and Gas Pipeline Services Market?

To stay informed about further developments, trends, and reports in the Canada Oil and Gas Pipeline Services Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence