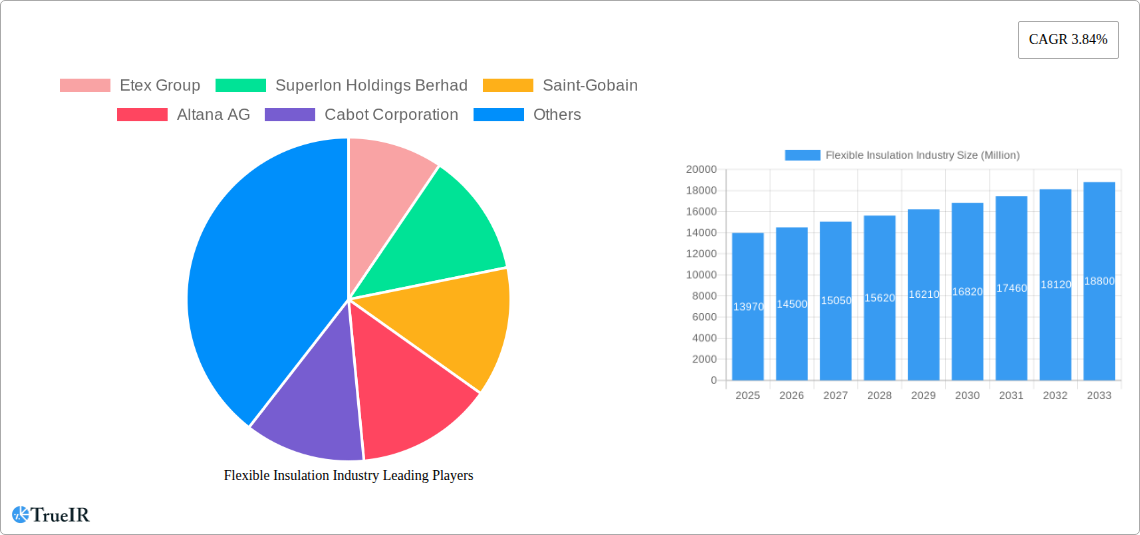

Key Insights

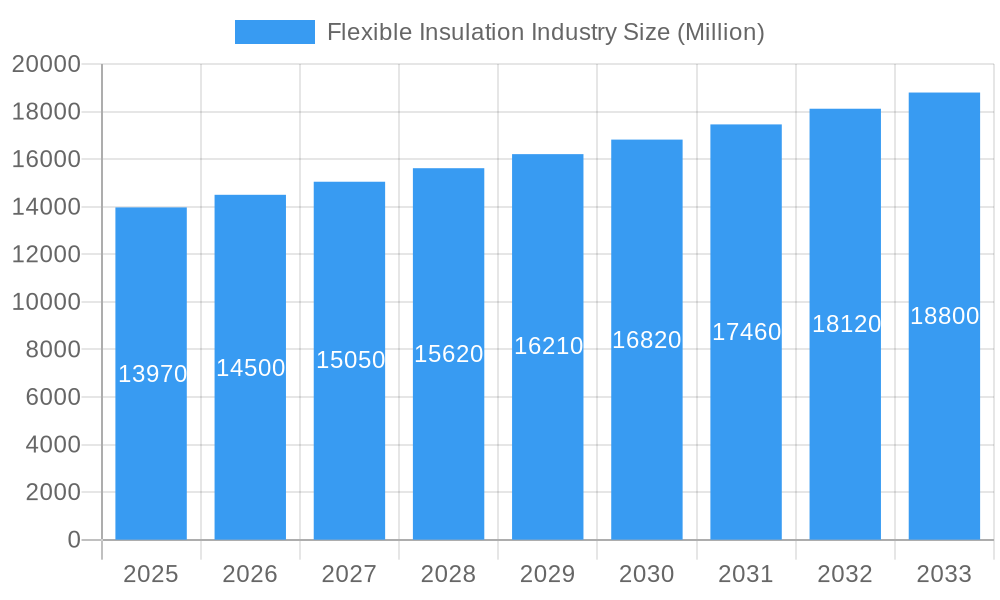

The flexible insulation market, valued at $13.97 billion in 2025, is projected to experience robust growth, driven by the increasing demand for energy efficiency in buildings and industrial applications. A Compound Annual Growth Rate (CAGR) of 3.84% from 2025 to 2033 indicates a significant expansion, fueled by several key factors. The rising adoption of sustainable building practices, stricter energy regulations globally, and the growth of the construction and industrial sectors are major contributors to this market expansion. Furthermore, advancements in material science, leading to the development of lighter, more efficient, and durable insulation materials like aerogel and cross-linked polyethylene, are further stimulating market growth. The segments showing the most promise are thermal insulation, owing to its wide application across various sectors, and the Asia-Pacific region, particularly China and India, due to rapid infrastructure development and industrialization. Competition is fierce, with major players like Saint-Gobain, Owens Corning, and Kingspan Group constantly innovating and expanding their product portfolios to maintain market share. However, fluctuating raw material prices and potential supply chain disruptions pose challenges to sustained growth.

Flexible Insulation Industry Market Size (In Billion)

Despite the positive outlook, certain restraints exist. The high initial cost associated with installing flexible insulation might deter some consumers, particularly in developing economies. Moreover, concerns regarding the environmental impact of certain insulation materials, and the need for skilled labor during installation, may present hurdles. To overcome these challenges, manufacturers are focusing on developing eco-friendly, cost-effective solutions and investing in comprehensive training programs for installers. The market segmentation by material (aerogel, cross-linked polyethylene, elastomer, fiberglass, and others) and insulation type (acoustic, electrical, and thermal) provides valuable insights for targeted market penetration. This detailed understanding, coupled with continuous innovation and strategic partnerships, will be crucial for businesses aiming to thrive in this dynamic market.

Flexible Insulation Industry Company Market Share

This comprehensive report provides a detailed analysis of the flexible insulation market, projecting a robust growth trajectory from 2025 to 2033. Valued at $XX Million in 2025 (estimated year), the market is poised for significant expansion, driven by technological advancements, burgeoning infrastructure development, and stringent energy efficiency regulations. The report covers the historical period (2019-2024), base year (2025), and forecast period (2025-2033), offering invaluable insights for industry stakeholders. Key players like Etex Group, Saint-Gobain, and Owens Corning are analyzed, alongside emerging trends and market segmentation.

Flexible Insulation Industry Market Structure & Competitive Landscape

The flexible insulation market exhibits a moderately consolidated structure, with a handful of major players holding significant market share. The Herfindahl-Hirschman Index (HHI) for 2025 is estimated at XX, indicating a moderately concentrated market. Innovation is a key driver, with companies investing heavily in R&D to develop advanced materials with improved thermal, acoustic, and electrical insulation properties. Stringent environmental regulations, particularly concerning greenhouse gas emissions, are influencing the adoption of eco-friendly insulation materials. Product substitution is a factor, with some consumers opting for alternative solutions depending on application and cost considerations. The market is segmented primarily by end-user industry (building & construction, automotive, industrial, etc.) and geographic region.

- Market Concentration: The HHI for 2025 is estimated at XX, indicating a moderately concentrated market.

- Innovation Drivers: Companies are focusing on developing sustainable, high-performance materials like Aerogel and Cross-Linked Polyethylene.

- Regulatory Impacts: Stringent energy efficiency standards and environmental regulations are driving demand for sustainable insulation solutions.

- Product Substitutes: Alternative materials like spray foam are competing for market share in certain segments.

- End-User Segmentation: Building and construction is currently the largest end-user segment.

- M&A Trends: The past five years have seen XX Million in M&A activity within the flexible insulation sector, indicating consolidation and expansion strategies among major players.

Flexible Insulation Industry Market Trends & Opportunities

The global flexible insulation market is experiencing robust growth, projected to reach $XX Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period. This expansion is fueled by several key factors. Technological advancements are leading to the development of superior insulation materials with enhanced performance characteristics. Increasing consumer awareness of energy efficiency and environmental sustainability is driving demand for eco-friendly insulation products. The expansion of the building and construction sector, particularly in developing economies, is creating significant growth opportunities. Competitive dynamics are shaping the market, with companies constantly striving to improve product offerings and enhance their market position through innovation, strategic partnerships, and mergers & acquisitions. Market penetration rates are high in developed nations but still offer significant growth potential in emerging markets.

Dominant Markets & Segments in Flexible Insulation Industry

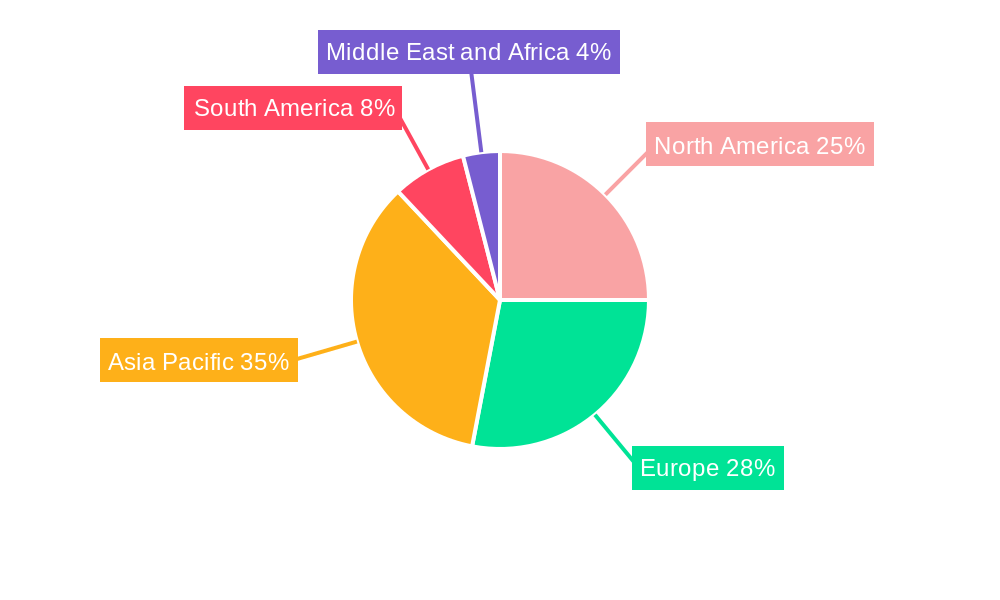

The Asia-Pacific region is currently the dominant market for flexible insulation, driven by rapid urbanization, infrastructure development, and increasing industrialization. Within the material segments, Fiberglass maintains the largest market share, owing to its cost-effectiveness and wide range of applications. However, Aerogel and Cross-Linked Polyethylene are experiencing rapid growth due to their superior performance characteristics. In terms of insulation type, Thermal Insulation dominates, reflecting the growing need for energy efficiency across various sectors.

- Key Growth Drivers in Asia-Pacific:

- Rapid urbanization and infrastructure development.

- Stringent building codes and energy efficiency standards.

- Growing industrial sector.

- Fiberglass Segment Dominance:

- Cost-effectiveness and wide applicability.

- Established manufacturing infrastructure.

- Growth of Aerogel and Cross-Linked Polyethylene:

- Superior thermal performance and eco-friendly properties.

- Increasing adoption in specialized applications.

- Thermal Insulation Leadership:

- Growing focus on energy conservation and reducing carbon footprint.

- Demand across various sectors, including building & construction and industrial applications.

Flexible Insulation Industry Product Analysis

Recent innovations have focused on developing lighter, more durable, and eco-friendly flexible insulation materials. These advancements enhance performance, improve installation ease, and reduce environmental impact. Key areas of innovation include incorporating nanomaterials to improve thermal performance, developing recyclable materials, and improving the fire resistance of flexible insulation products. These products cater to a wide range of applications across various sectors, offering tailored solutions based on specific needs. Competitive advantages are achieved through enhanced performance, sustainable attributes, and superior customer support.

Key Drivers, Barriers & Challenges in Flexible Insulation Industry

Key Drivers:

Technological advancements, including the development of high-performance materials like aerogel and cross-linked polyethylene, are significantly boosting market growth. Government regulations aimed at improving energy efficiency and reducing greenhouse gas emissions are creating favorable market conditions. The expansion of construction and industrial sectors provides a significant impetus to the market.

Key Challenges:

Fluctuations in raw material prices pose a major challenge. Supply chain disruptions, particularly in the wake of recent global events, can impact production and availability. Intense competition amongst established players is leading to price wars and compressed margins.

Growth Drivers in the Flexible Insulation Industry Market

The flexible insulation market is propelled by several key factors, including stringent energy efficiency regulations, the expanding construction sector in emerging economies, and technological advancements leading to higher-performing and sustainable insulation materials. Furthermore, increasing environmental concerns are driving demand for eco-friendly solutions.

Challenges Impacting Flexible Insulation Industry Growth

Major challenges include fluctuating raw material costs, supply chain vulnerabilities, and intense competition leading to price pressure. These factors can significantly affect profitability and market growth.

Key Players Shaping the Flexible Insulation Industry Market

- Etex Group

- Superlon Holdings Berhad

- Saint-Gobain

- Altana AG

- Cabot Corporation

- Armacell

- Fletcher Insulation

- Thermaxx Jackets

- Owens Corning

- Kingspan Group

- Knauf Insulation

- Johns Manville

Significant Flexible Insulation Industry Industry Milestones

- 2022: Saint-Gobain launched a new line of eco-friendly flexible insulation.

- 2021: Armacell acquired a smaller competitor, expanding its market share.

- 2020: Owens Corning introduced a new high-performance insulation material with improved thermal efficiency.

- 2019: Kingspan Group invested heavily in R&D to develop new sustainable insulation technologies. (Further milestones from "The recent developments pertaining to the major players in the market are covered in the complete study" would be listed here)

Future Outlook for Flexible Insulation Industry Market

The flexible insulation market is projected to experience sustained growth over the next decade, driven by ongoing technological advancements, increasing demand from emerging markets, and favorable government policies promoting energy efficiency. Strategic acquisitions and partnerships will continue to shape the market landscape, with companies focusing on developing innovative, sustainable, and high-performance insulation solutions. The market presents significant opportunities for established players and new entrants alike.

Flexible Insulation Industry Segmentation

-

1. Material

- 1.1. Aerogel

- 1.2. Cross-Linked Polyethylene

- 1.3. Elastomer

- 1.4. Fiberglass

- 1.5. Other Materials

-

2. Insulation Type

- 2.1. Acoustic Insulation

- 2.2. Electrical Insulation

- 2.3. Thermal Insulation

Flexible Insulation Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Flexible Insulation Industry Regional Market Share

Geographic Coverage of Flexible Insulation Industry

Flexible Insulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Aerogel

- 5.1.2. Cross-Linked Polyethylene

- 5.1.3. Elastomer

- 5.1.4. Fiberglass

- 5.1.5. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Insulation Type

- 5.2.1. Acoustic Insulation

- 5.2.2. Electrical Insulation

- 5.2.3. Thermal Insulation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Flexible Insulation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Aerogel

- 6.1.2. Cross-Linked Polyethylene

- 6.1.3. Elastomer

- 6.1.4. Fiberglass

- 6.1.5. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Insulation Type

- 6.2.1. Acoustic Insulation

- 6.2.2. Electrical Insulation

- 6.2.3. Thermal Insulation

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Asia Pacific Flexible Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Aerogel

- 7.1.2. Cross-Linked Polyethylene

- 7.1.3. Elastomer

- 7.1.4. Fiberglass

- 7.1.5. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Insulation Type

- 7.2.1. Acoustic Insulation

- 7.2.2. Electrical Insulation

- 7.2.3. Thermal Insulation

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. North America Flexible Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Aerogel

- 8.1.2. Cross-Linked Polyethylene

- 8.1.3. Elastomer

- 8.1.4. Fiberglass

- 8.1.5. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Insulation Type

- 8.2.1. Acoustic Insulation

- 8.2.2. Electrical Insulation

- 8.2.3. Thermal Insulation

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Europe Flexible Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Aerogel

- 9.1.2. Cross-Linked Polyethylene

- 9.1.3. Elastomer

- 9.1.4. Fiberglass

- 9.1.5. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Insulation Type

- 9.2.1. Acoustic Insulation

- 9.2.2. Electrical Insulation

- 9.2.3. Thermal Insulation

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. South America Flexible Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Aerogel

- 10.1.2. Cross-Linked Polyethylene

- 10.1.3. Elastomer

- 10.1.4. Fiberglass

- 10.1.5. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by Insulation Type

- 10.2.1. Acoustic Insulation

- 10.2.2. Electrical Insulation

- 10.2.3. Thermal Insulation

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Middle East and Africa Flexible Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Aerogel

- 11.1.2. Cross-Linked Polyethylene

- 11.1.3. Elastomer

- 11.1.4. Fiberglass

- 11.1.5. Other Materials

- 11.2. Market Analysis, Insights and Forecast - by Insulation Type

- 11.2.1. Acoustic Insulation

- 11.2.2. Electrical Insulation

- 11.2.3. Thermal Insulation

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Etex Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Superlon Holdings Berhad

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Saint-Gobain

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Altana AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cabot Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Armacell

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Fletcher Insulation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Thermaxx Jackets

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Owens Corning

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Kingspan Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Knauf Insulation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Johns Manville

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Etex Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Flexible Insulation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Flexible Insulation Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Flexible Insulation Industry Revenue (Million), by Material 2025 & 2033

- Figure 4: Asia Pacific Flexible Insulation Industry Volume (K Tons), by Material 2025 & 2033

- Figure 5: Asia Pacific Flexible Insulation Industry Revenue Share (%), by Material 2025 & 2033

- Figure 6: Asia Pacific Flexible Insulation Industry Volume Share (%), by Material 2025 & 2033

- Figure 7: Asia Pacific Flexible Insulation Industry Revenue (Million), by Insulation Type 2025 & 2033

- Figure 8: Asia Pacific Flexible Insulation Industry Volume (K Tons), by Insulation Type 2025 & 2033

- Figure 9: Asia Pacific Flexible Insulation Industry Revenue Share (%), by Insulation Type 2025 & 2033

- Figure 10: Asia Pacific Flexible Insulation Industry Volume Share (%), by Insulation Type 2025 & 2033

- Figure 11: Asia Pacific Flexible Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: Asia Pacific Flexible Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 13: Asia Pacific Flexible Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Flexible Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Flexible Insulation Industry Revenue (Million), by Material 2025 & 2033

- Figure 16: North America Flexible Insulation Industry Volume (K Tons), by Material 2025 & 2033

- Figure 17: North America Flexible Insulation Industry Revenue Share (%), by Material 2025 & 2033

- Figure 18: North America Flexible Insulation Industry Volume Share (%), by Material 2025 & 2033

- Figure 19: North America Flexible Insulation Industry Revenue (Million), by Insulation Type 2025 & 2033

- Figure 20: North America Flexible Insulation Industry Volume (K Tons), by Insulation Type 2025 & 2033

- Figure 21: North America Flexible Insulation Industry Revenue Share (%), by Insulation Type 2025 & 2033

- Figure 22: North America Flexible Insulation Industry Volume Share (%), by Insulation Type 2025 & 2033

- Figure 23: North America Flexible Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: North America Flexible Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: North America Flexible Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Flexible Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Flexible Insulation Industry Revenue (Million), by Material 2025 & 2033

- Figure 28: Europe Flexible Insulation Industry Volume (K Tons), by Material 2025 & 2033

- Figure 29: Europe Flexible Insulation Industry Revenue Share (%), by Material 2025 & 2033

- Figure 30: Europe Flexible Insulation Industry Volume Share (%), by Material 2025 & 2033

- Figure 31: Europe Flexible Insulation Industry Revenue (Million), by Insulation Type 2025 & 2033

- Figure 32: Europe Flexible Insulation Industry Volume (K Tons), by Insulation Type 2025 & 2033

- Figure 33: Europe Flexible Insulation Industry Revenue Share (%), by Insulation Type 2025 & 2033

- Figure 34: Europe Flexible Insulation Industry Volume Share (%), by Insulation Type 2025 & 2033

- Figure 35: Europe Flexible Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe Flexible Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 37: Europe Flexible Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Flexible Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Flexible Insulation Industry Revenue (Million), by Material 2025 & 2033

- Figure 40: South America Flexible Insulation Industry Volume (K Tons), by Material 2025 & 2033

- Figure 41: South America Flexible Insulation Industry Revenue Share (%), by Material 2025 & 2033

- Figure 42: South America Flexible Insulation Industry Volume Share (%), by Material 2025 & 2033

- Figure 43: South America Flexible Insulation Industry Revenue (Million), by Insulation Type 2025 & 2033

- Figure 44: South America Flexible Insulation Industry Volume (K Tons), by Insulation Type 2025 & 2033

- Figure 45: South America Flexible Insulation Industry Revenue Share (%), by Insulation Type 2025 & 2033

- Figure 46: South America Flexible Insulation Industry Volume Share (%), by Insulation Type 2025 & 2033

- Figure 47: South America Flexible Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: South America Flexible Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 49: South America Flexible Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Flexible Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Flexible Insulation Industry Revenue (Million), by Material 2025 & 2033

- Figure 52: Middle East and Africa Flexible Insulation Industry Volume (K Tons), by Material 2025 & 2033

- Figure 53: Middle East and Africa Flexible Insulation Industry Revenue Share (%), by Material 2025 & 2033

- Figure 54: Middle East and Africa Flexible Insulation Industry Volume Share (%), by Material 2025 & 2033

- Figure 55: Middle East and Africa Flexible Insulation Industry Revenue (Million), by Insulation Type 2025 & 2033

- Figure 56: Middle East and Africa Flexible Insulation Industry Volume (K Tons), by Insulation Type 2025 & 2033

- Figure 57: Middle East and Africa Flexible Insulation Industry Revenue Share (%), by Insulation Type 2025 & 2033

- Figure 58: Middle East and Africa Flexible Insulation Industry Volume Share (%), by Insulation Type 2025 & 2033

- Figure 59: Middle East and Africa Flexible Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Flexible Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 61: Middle East and Africa Flexible Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Flexible Insulation Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 3: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 4: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 5: Global Flexible Insulation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Flexible Insulation Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 8: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 9: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 10: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 11: Global Flexible Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Flexible Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: China Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: China Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: India Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: India Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Japan Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: South Korea Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: South Korea Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 24: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 25: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 26: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 27: Global Flexible Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Global Flexible Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 29: United States Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: United States Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Canada Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Canada Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 33: Mexico Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Mexico Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 36: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 37: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 38: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 39: Global Flexible Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Flexible Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 41: Germany Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Germany Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: France Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: France Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: Italy Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Italy Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 52: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 53: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 54: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 55: Global Flexible Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Flexible Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: Brazil Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Brazil Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: Argentina Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Argentina Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 61: Rest of South America Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of South America Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 63: Global Flexible Insulation Industry Revenue Million Forecast, by Material 2020 & 2033

- Table 64: Global Flexible Insulation Industry Volume K Tons Forecast, by Material 2020 & 2033

- Table 65: Global Flexible Insulation Industry Revenue Million Forecast, by Insulation Type 2020 & 2033

- Table 66: Global Flexible Insulation Industry Volume K Tons Forecast, by Insulation Type 2020 & 2033

- Table 67: Global Flexible Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 68: Global Flexible Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 69: Saudi Arabia Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: Saudi Arabia Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 71: South Africa Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: South Africa Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 73: Rest of Middle East and Africa Flexible Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Rest of Middle East and Africa Flexible Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flexible Insulation Industry?

The projected CAGR is approximately 3.84%.

2. Which companies are prominent players in the Flexible Insulation Industry?

Key companies in the market include Etex Group, Superlon Holdings Berhad, Saint-Gobain, Altana AG, Cabot Corporation, Armacell, Fletcher Insulation, Thermaxx Jackets, Owens Corning, Kingspan Group, Knauf Insulation, Johns Manville.

3. What are the main segments of the Flexible Insulation Industry?

The market segments include Material, Insulation Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.97 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Energy Efficiency from the Construction Industry; Increasing Application of Flexible Piping Insulation; Other Drivers.

6. What are the notable trends driving market growth?

Rising Demand for Fiberglass Insulation.

7. Are there any restraints impacting market growth?

Availability of Alternatives; Other Restraints.

8. Can you provide examples of recent developments in the market?

The recent developments pertaining to the major players in the market are covered in the complete study.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flexible Insulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flexible Insulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flexible Insulation Industry?

To stay informed about further developments, trends, and reports in the Flexible Insulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence