Key Insights

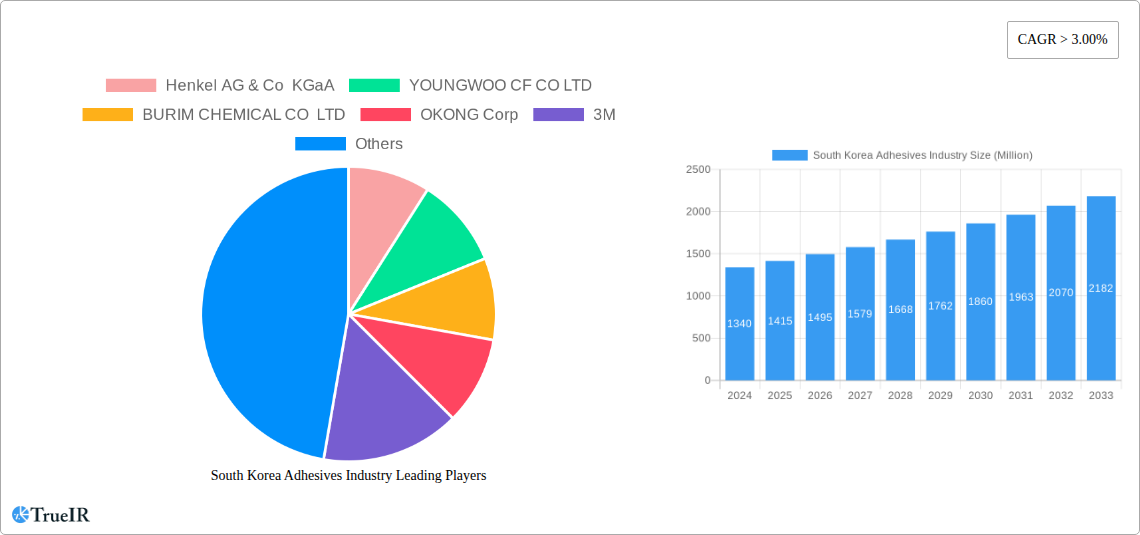

The South Korean adhesives industry is poised for robust expansion, projecting a market size of USD 1.34 billion in 2024, driven by a Compound Annual Growth Rate (CAGR) of 5.62% through 2033. This significant growth is fueled by escalating demand across key end-user industries. The automotive sector, a cornerstone of South Korea's economy, continues to be a primary consumer of advanced adhesives for lightweighting and structural bonding, enhancing fuel efficiency and safety. Similarly, the burgeoning aerospace industry is adopting sophisticated adhesive solutions for assembly and composite manufacturing, seeking lighter and stronger alternatives to traditional fastening methods. The construction industry's focus on energy-efficient buildings and infrastructure development also contributes substantially to this demand, with adhesives playing a crucial role in insulation, sealing, and bonding applications. Furthermore, the expanding packaging sector, driven by e-commerce and consumer goods, necessitates a continuous supply of reliable and specialized adhesives.

South Korea Adhesives Industry Market Size (In Billion)

The technological landscape of the South Korean adhesives market is dynamic, with significant adoption of Hot Melt, Reactive, and UV Cured adhesives. These technologies offer distinct advantages, ranging from rapid bonding and high strength to environmental friendliness and specialized performance characteristics. Water-borne adhesives are gaining traction due to increasing regulatory emphasis on reduced volatile organic compounds (VOCs). In terms of resin technology, Polyurethane and Epoxy resins are dominant due to their superior mechanical properties and versatility, finding applications in demanding environments. Acrylics and Cyanoacrylates cater to a broad spectrum of applications requiring quick setting times and strong adhesion. The industry is characterized by the presence of major global players alongside strong domestic manufacturers, fostering innovation and competitive pricing. The forecast period anticipates sustained growth, with strategic investments in research and development and a continued focus on sustainability and performance enhancement expected to shape market dynamics.

South Korea Adhesives Industry Company Market Share

Unlock unparalleled insights into the dynamic South Korean adhesives market. This comprehensive report delves into market structure, competitive landscapes, emerging trends, dominant segments, and future projections from 2019 to 2033. Leveraging high-volume keywords, this analysis provides a deep dive into technology, resin, and end-user industry segmentation, offering actionable intelligence for stakeholders in the global adhesives sector.

South Korea Adhesives Industry Market Structure & Competitive Landscape

The South Korean adhesives market exhibits a moderately concentrated structure, with a blend of multinational giants and robust domestic players vying for market share. Innovation remains a critical driver, fueled by intense R&D investments aimed at developing high-performance, sustainable, and specialized adhesive solutions. Regulatory impacts, particularly concerning environmental standards and safety regulations, are progressively shaping product development and market entry strategies. Product substitutes, while present, often struggle to match the tailored performance characteristics offered by advanced adhesives, especially in demanding industrial applications. End-user segmentation reveals a diverse demand landscape, with the automotive, packaging, and building and construction sectors emerging as key growth engines. Merger and acquisition (M&A) activity, while not currently at a fever pitch, presents opportunities for strategic consolidation and market expansion. The overall market concentration is estimated at approximately 65% by the top five players, with M&A deals valued in the hundreds of millions of dollars in recent years, indicating strategic acquisitions for technology or market access.

South Korea Adhesives Industry Market Trends & Opportunities

The South Korean adhesives industry is poised for substantial growth, projected to reach a market size exceeding fifty billion dollars by 2033. This expansion is propelled by a consistent Compound Annual Growth Rate (CAGR) of approximately 6.5% throughout the forecast period. Technological shifts are a significant trend, with an increasing demand for advanced adhesive technologies such as UV-cured, reactive, and water-borne adhesives, driven by their superior performance, reduced environmental impact, and suitability for automation. Consumer preferences are increasingly gravitating towards eco-friendly and low-VOC (Volatile Organic Compound) solutions, influencing product formulation and marketing strategies. The competitive dynamics are characterized by continuous product innovation, strategic partnerships, and a focus on providing customized solutions to diverse end-user industries. Emerging opportunities lie in the development of bio-based and recyclable adhesives, the expansion of smart adhesives with embedded functionalities, and the penetration of niche applications within the rapidly growing electronics and renewable energy sectors. Market penetration for high-performance adhesives in specialized industries is estimated to be over 70%, with significant room for growth in emerging sectors. The rise of the electric vehicle (EV) market alone is expected to drive a ten billion dollar surge in demand for specialized automotive adhesives by 2030. Furthermore, the burgeoning healthcare industry's demand for biocompatible and high-strength medical adhesives presents another promising avenue for market expansion, with an estimated growth of five billion dollars in this segment. The increasing adoption of advanced manufacturing techniques and the government's focus on high-tech industries are also significant tailwinds.

Dominant Markets & Segments in South Korea Adhesives Industry

The Automotive sector stands out as a dominant market within the South Korean adhesives industry, driven by the nation's robust automotive manufacturing base and its leadership in electric vehicle (EV) production. The increasing need for lightweighting, structural integrity, and enhanced safety features in vehicles directly translates to a higher demand for advanced adhesives. Key growth drivers include the stringent fuel efficiency regulations and the continuous innovation in EV battery technology, requiring specialized thermal management and structural bonding adhesives.

- Automotive: Expected to account for over 25% of the total market share by 2033, driven by EV production and advanced driver-assistance systems (ADAS) integration.

- Packaging: A consistently strong segment, projected to hold around 20% market share, fueled by the e-commerce boom and demand for sustainable packaging solutions. Growth drivers include the demand for food-grade and recyclable adhesives.

- Building and Construction: This segment is experiencing steady growth, estimated at 15% market share, propelled by government infrastructure projects and the demand for energy-efficient building materials, including high-performance sealants and bonding agents.

Technology Segmentation:

- Hot Melt Adhesives: A significant segment, valued at over seven billion dollars, widely used in packaging and assembly due to their fast setting times and ease of application.

- Reactive Adhesives: This category, including epoxy and polyurethane, is experiencing rapid growth, particularly in automotive and aerospace, due to their high strength, durability, and chemical resistance. The market for reactive adhesives is projected to reach twelve billion dollars by 2033.

- Water-borne Adhesives: Driven by environmental regulations and a push for sustainability, this segment is gaining traction, especially in consumer goods and packaging.

Resin Segmentation:

- Polyurethane: A leading resin type, crucial for its versatility in applications ranging from automotive interiors to construction sealants, with an estimated market value of nine billion dollars.

- Acrylic: Dominant in various industrial applications, including automotive and electronics, due to its excellent UV resistance and bonding capabilities. The acrylic resin market is valued at approximately six billion dollars.

- Epoxy: Essential for high-strength structural bonding in aerospace, automotive, and electronics, the epoxy resin segment is expected to continue its robust growth trajectory.

South Korea Adhesives Industry Product Analysis

Product innovation in the South Korean adhesives market centers on high-performance formulations catering to evolving industry demands. Innovations include the development of advanced structural adhesives for automotive lightweighting, high-temperature resistant adhesives for electronics, and eco-friendly, low-VOC options for packaging and construction. The competitive advantage lies in developing solutions that offer enhanced bonding strength, faster curing times, superior durability, and improved sustainability profiles. Applications are expanding beyond traditional uses, encompassing specialized bonding in renewable energy components and advanced medical devices.

Key Drivers, Barriers & Challenges in South Korea Adhesives Industry

Key Drivers: The South Korean adhesives industry is propelled by robust growth in key end-user sectors such as automotive (especially EVs), electronics, and construction. Technological advancements driving demand for high-performance, specialized adhesives (e.g., for battery assembly, lightweighting) are significant growth catalysts. Supportive government policies promoting advanced manufacturing and sustainable technologies further bolster the market.

Key Barriers & Challenges: Stringent environmental regulations and a growing emphasis on sustainability present both opportunities and challenges, requiring significant R&D investment for compliance. Supply chain volatility for raw materials, including petrochemical derivatives, can impact production costs and availability. Intense competition from both domestic and international players necessitates continuous innovation and cost optimization. Regulatory hurdles for new product approvals in sectors like healthcare can also pose a restraint. Supply chain disruptions have led to an estimated 10-15% increase in raw material costs over the historical period, impacting profit margins.

Growth Drivers in the South Korea Adhesives Industry Market

Key growth drivers for the South Korean adhesives industry include the booming automotive sector, particularly the rapid expansion of electric vehicle (EV) manufacturing, which requires specialized and high-performance adhesives for battery packs and lightweight components. The burgeoning electronics industry, with its demand for micro-assembly and thermal management solutions, is another significant driver. Furthermore, government initiatives promoting green building and infrastructure development are fueling the demand for advanced adhesives in construction. Technological innovation, focusing on sustainable, high-strength, and functional adhesives, is also a critical growth catalyst.

Challenges Impacting South Korea Adhesives Industry Growth

Challenges impacting the growth of the South Korean adhesives industry include stringent environmental regulations that necessitate significant investment in eco-friendly product development and compliance. Volatility in raw material prices, particularly petrochemical-derived components, can lead to unpredictable cost fluctuations and impact profitability. Intense competition within the market, both from established global players and agile domestic manufacturers, demands continuous innovation and competitive pricing strategies. Furthermore, the skilled labor shortage in specialized adhesive application and R&D can also present a constraint on expansion.

Key Players Shaping the South Korea Adhesives Industry Market

- Henkel AG & Co KGaA

- YOUNGWOO CF CO LTD

- BURIM CHEMICAL CO LTD

- OKONG Corp

- 3M

- H B Fuller Company

- Industrial Adhesives Company MCS

- SAMYOUNG INK&PAINT INDUSTRIAL CO LTD

- AVERY DENNISON CORPORATION

- Unitech Co Ltd

Significant South Korea Adhesives Industry Industry Milestones

- October 2021: 3M introduced a new generation of acrylic adhesives, including 3M Scotch-Weld Low Odor Acrylic Adhesive 8700NS Series, 3M Scotch-Weld Flexible Acrylic Adhesive 8600NS Series, and 3M Scotch-Weld Nylon Bonder Structural Adhesive DP8910NS, enhancing their product portfolio for industrial bonding.

- September 2021: Henkel launched its newly developed solvent-free and zero-VOC adhesive range for rubber lining, demonstrating a commitment to sustainable solutions and addressing growing environmental concerns.

- July 2021: H.B. Fuller announced a strategic agreement with Covestro to offer sustainable adhesives in the market, indicating a collaborative approach to advancing green chemistry in the adhesives sector.

Future Outlook for South Korea Adhesives Industry Market

The future outlook for the South Korean adhesives industry is exceptionally bright, with sustained growth driven by ongoing technological advancements and the expansion of key end-user industries. The increasing adoption of electric vehicles, advancements in electronics manufacturing, and the government's focus on smart infrastructure will continue to fuel demand for high-performance, specialized adhesives. Opportunities for innovation in bio-based and recyclable adhesives, along with the development of smart adhesives with embedded functionalities, will shape market trends. Strategic collaborations and a focus on sustainability will be crucial for companies aiming to maintain a competitive edge in this dynamic and evolving market. The market is projected to surpass seventy billion dollars by 2033, driven by these robust growth catalysts.

South Korea Adhesives Industry Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Footwear and Leather

- 1.5. Healthcare

- 1.6. Packaging

- 1.7. Woodworking and Joinery

- 1.8. Other End-user Industries

-

2. Technology

- 2.1. Hot Melt

- 2.2. Reactive

- 2.3. Solvent-borne

- 2.4. UV Cured Adhesives

- 2.5. Water-borne

-

3. Resin

- 3.1. Acrylic

- 3.2. Cyanoacrylate

- 3.3. Epoxy

- 3.4. Polyurethane

- 3.5. Silicone

- 3.6. VAE/EVA

- 3.7. Other Resins

South Korea Adhesives Industry Segmentation By Geography

- 1. South Korea

South Korea Adhesives Industry Regional Market Share

Geographic Coverage of South Korea Adhesives Industry

South Korea Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Footwear and Leather

- 5.1.5. Healthcare

- 5.1.6. Packaging

- 5.1.7. Woodworking and Joinery

- 5.1.8. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Hot Melt

- 5.2.2. Reactive

- 5.2.3. Solvent-borne

- 5.2.4. UV Cured Adhesives

- 5.2.5. Water-borne

- 5.3. Market Analysis, Insights and Forecast - by Resin

- 5.3.1. Acrylic

- 5.3.2. Cyanoacrylate

- 5.3.3. Epoxy

- 5.3.4. Polyurethane

- 5.3.5. Silicone

- 5.3.6. VAE/EVA

- 5.3.7. Other Resins

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. South Korea

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. South Korea Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Aerospace

- 6.1.2. Automotive

- 6.1.3. Building and Construction

- 6.1.4. Footwear and Leather

- 6.1.5. Healthcare

- 6.1.6. Packaging

- 6.1.7. Woodworking and Joinery

- 6.1.8. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Hot Melt

- 6.2.2. Reactive

- 6.2.3. Solvent-borne

- 6.2.4. UV Cured Adhesives

- 6.2.5. Water-borne

- 6.3. Market Analysis, Insights and Forecast - by Resin

- 6.3.1. Acrylic

- 6.3.2. Cyanoacrylate

- 6.3.3. Epoxy

- 6.3.4. Polyurethane

- 6.3.5. Silicone

- 6.3.6. VAE/EVA

- 6.3.7. Other Resins

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Henkel AG & Co KGaA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 YOUNGWOO CF CO LTD

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BURIM CHEMICAL CO LTD

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 OKONG Corp

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 3M

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 H B Fuller Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Industrial Adhesives Company MCS

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 SAMYOUNG INK&PAINT INDUSTRIAL CO LTD

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AVERY DENNISON CORPORATION

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Unitech Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Henkel AG & Co KGaA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Korea Adhesives Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South Korea Adhesives Industry Share (%) by Company 2025

List of Tables

- Table 1: South Korea Adhesives Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: South Korea Adhesives Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: South Korea Adhesives Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 4: South Korea Adhesives Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: South Korea Adhesives Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 6: South Korea Adhesives Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 7: South Korea Adhesives Industry Revenue billion Forecast, by Resin 2020 & 2033

- Table 8: South Korea Adhesives Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Korea Adhesives Industry?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the South Korea Adhesives Industry?

Key companies in the market include Henkel AG & Co KGaA, YOUNGWOO CF CO LTD, BURIM CHEMICAL CO LTD, OKONG Corp, 3M, H B Fuller Company, Industrial Adhesives Company MCS, SAMYOUNG INK&PAINT INDUSTRIAL CO LTD, AVERY DENNISON CORPORATION, Unitech Co Ltd.

3. What are the main segments of the South Korea Adhesives Industry?

The market segments include End User Industry, Technology, Resin.

4. Can you provide details about the market size?

The market size is estimated to be USD 86.62 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand from Metal and Steel Industries; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

; Environmental Constraints; Unfavorable Conditions Arising Due to COVID-19 Outbreak.

8. Can you provide examples of recent developments in the market?

October 2021: 3M introduced a new generation of acrylic adhesives, including 3M Scotch-Weld Low Odor Acrylic Adhesive 8700NS Series, 3M Scotch-Weld Flexible Acrylic Adhesive 8600NS Series, and 3M Scotch-Weld Nylon Bonder Structural Adhesive DP8910NS.September 2021: Henkel launched its newly developed solvent-free and zero-VOC adhesive range for rubber lining.July 2021: H.B. Fuller announced a strategic agreement with Covestro to offer sustainable adhesives in the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Korea Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Korea Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Korea Adhesives Industry?

To stay informed about further developments, trends, and reports in the South Korea Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence