Key Insights

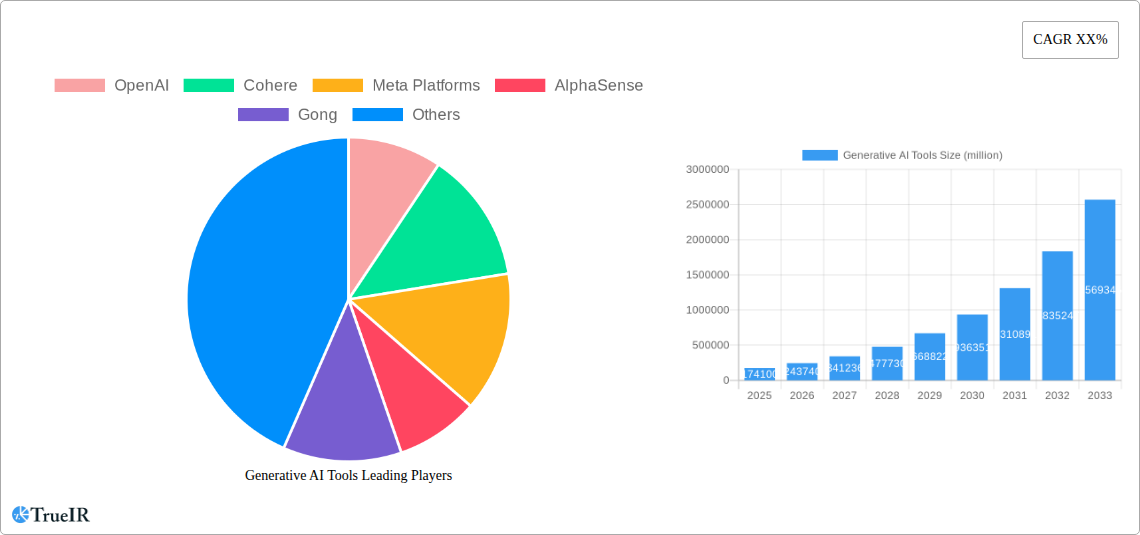

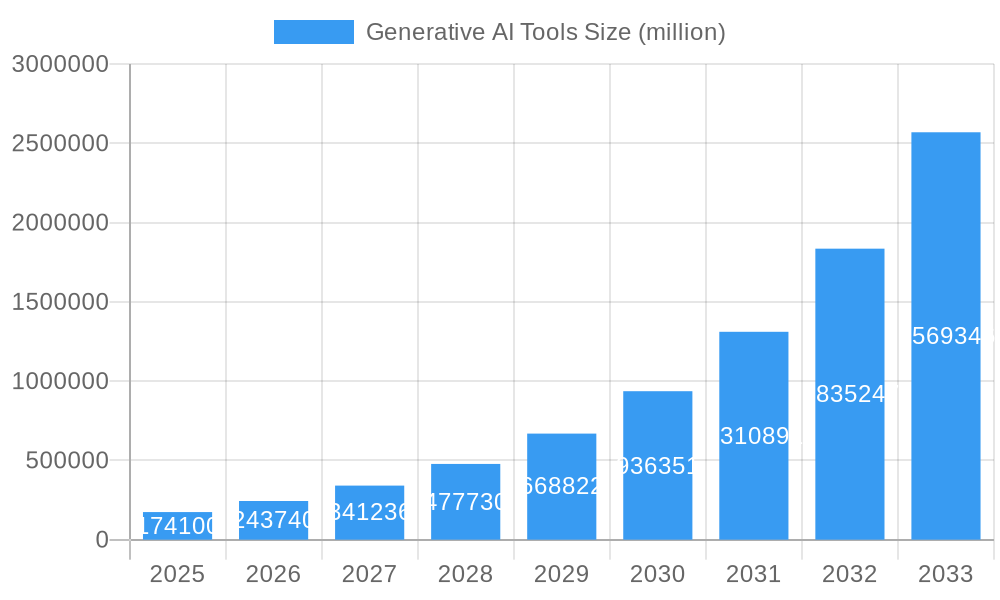

The Generative AI Tools market is poised for explosive growth, with an estimated market size of $174.1 billion in 2025 and projected to expand at a compound annual growth rate (CAGR) of 40% over the forecast period of 2025-2033. This remarkable expansion is fueled by a confluence of powerful drivers, including the increasing demand for personalized content creation, the democratization of advanced AI capabilities, and the growing adoption across diverse enterprise functions such as marketing, software development, and customer service. The ability of generative AI to automate complex tasks, accelerate innovation, and unlock new creative possibilities is fundamentally reshaping industries, making it an indispensable technology for businesses seeking a competitive edge. Key trends underpinning this surge include the proliferation of sophisticated text, image, and code generation models, alongside advancements in music and audio synthesis, all of which are becoming more accessible and powerful. The integration of these tools into existing workflows is becoming seamless, further accelerating their adoption and market penetration.

Generative AI Tools Market Size (In Billion)

Despite the overwhelmingly positive outlook, certain restraints could influence the pace and nature of market expansion. These include potential concerns around data privacy and security, the ethical implications of AI-generated content, and the need for robust regulatory frameworks. Additionally, the significant investment required for developing and deploying advanced generative AI solutions could present a barrier for smaller organizations. However, the sheer potential for efficiency gains, cost reductions, and novel revenue streams strongly incentivizes overcoming these challenges. The market is segmented into distinct applications, with both private and enterprise sectors actively embracing generative AI. Within types, Text Generators, Image Generators, and Code Generators are leading the charge, with Music and Audio Generators also showing significant promise. Major players like OpenAI, Google, Microsoft, and Meta are at the forefront of innovation, alongside a rapidly growing ecosystem of specialized companies, indicating a highly competitive and dynamic market landscape.

Generative AI Tools Company Market Share

Generative AI Tools Market Report: Unlocking Billion-Dollar Opportunities (2019-2033)

Report Description:

Dive deep into the rapidly evolving Generative AI Tools market with this comprehensive, SEO-optimized report. Covering the Study Period of 2019–2033, with a Base Year and Estimated Year of 2025, and a Forecast Period from 2025–2033, this analysis provides unparalleled insights into a sector poised for exponential growth. We meticulously examine the market structure, competitive landscape, emerging trends, dominant segments, product innovations, and the critical drivers, barriers, and challenges shaping this billion-dollar industry. Leveraging high-volume keywords such as "Generative AI," "AI tools," "text generation," "image generation," "code generation," "enterprise AI," and "private AI," this report is designed to enhance search rankings and engage key industry audiences, including technology strategists, investors, researchers, and business leaders. The report meticulously analyzes the market's trajectory, offering actionable intelligence for strategic decision-making.

Generative AI Tools Market Structure & Competitive Landscape

The Generative AI Tools market is characterized by a dynamic and increasingly concentrated competitive landscape, driven by substantial innovation and significant investment. Leading companies like OpenAI, Google (Alphabet), Microsoft, and Meta Platforms are at the forefront, investing billions in research and development, which fuels rapid product advancements and market penetration. The innovation drivers are multifaceted, stemming from breakthroughs in large language models (LLMs), diffusion models, and transformer architectures, enabling increasingly sophisticated text, image, and code generation capabilities. Regulatory impacts, while still nascent, are beginning to emerge, with discussions around data privacy, intellectual property, and ethical AI influencing development and deployment strategies across both private and enterprise segments. Product substitutes are emerging, primarily from traditional content creation software and in-house development efforts, but Generative AI tools offer distinct advantages in speed, scalability, and novel creation. End-user segmentation reveals strong adoption within the enterprise sector for applications ranging from marketing and customer service to software development and scientific research, while the private segment is rapidly growing with consumer-facing applications. Mergers and acquisitions (M&A) trends indicate a consolidation phase, with larger technology giants acquiring innovative startups to bolster their AI portfolios, a trend expected to continue with billions in deal values. Concentration ratios are rising as established players leverage their vast resources, creating significant barriers to entry for smaller entities.

Generative AI Tools Market Trends & Opportunities

The Generative AI Tools market is experiencing an unprecedented surge in growth, projected to reach multi-billion dollar valuations by 2033. This remarkable expansion is fueled by a confluence of technological advancements, evolving consumer preferences, and intensifying competitive dynamics. The market size is set to escalate from tens of billions in the base year of 2025 to hundreds of billions by the end of the forecast period, reflecting a compound annual growth rate (CAGR) of over 30%. Technological shifts are profoundly impacting the landscape, with continuous improvements in model architectures, such as further refinements in LLMs and advancements in multimodal AI, enabling more nuanced and context-aware content generation. The development of more accessible APIs and integrated platforms is democratizing access to these powerful tools, lowering the barrier to entry for businesses of all sizes. Consumer preferences are increasingly leaning towards personalized and on-demand content creation, with Generative AI tools meeting this demand by offering bespoke marketing materials, creative artwork, and tailored communication. The penetration rate of Generative AI tools within the enterprise segment, particularly for applications like content marketing, software development, and customer support, is rapidly increasing, with an estimated penetration of over 60% by 2030.

The competitive dynamics are fierce, with major players like OpenAI, Google, Microsoft, and Meta Platforms continually pushing the boundaries of what's possible. Startups, including Cohere, Anthropic, and Jasper AI, are carving out significant niches by focusing on specialized applications and offering distinct technological advantages. The rise of specialized tools for code generation by companies like Databricks and IBM, alongside image generators from Adobe and image synthesis specialists, is diversifying the market. The demand for real-time, high-quality content is a significant opportunity, with businesses seeking to leverage Generative AI for accelerated product development, enhanced customer engagement, and streamlined operational workflows. The integration of Generative AI into existing software suites and platforms, such as those offered by Microsoft and Adobe, is another key trend, making these technologies more accessible and indispensable. Furthermore, the emergence of specialized enterprise solutions from companies like AlphaSense and Gong, focused on specific industry needs, highlights the growing maturity and segmentation of the market, offering billions in untapped potential. The continuous pursuit of more efficient, cost-effective, and ethically aligned Generative AI models presents ongoing opportunities for innovation and market leadership.

Dominant Markets & Segments in Generative AI Tools

The Generative AI Tools market is exhibiting strong dominance in several key regions and segments, driven by robust infrastructure, supportive policies, and high adoption rates. The Enterprise application segment is currently the most dominant, projected to account for over 70% of the total market revenue by 2030, with billions in value derived from its widespread integration into business processes. This dominance is fueled by enterprises seeking to optimize operations, enhance customer engagement, and drive innovation. Within the Types of Generative AI tools, Text Generators represent the largest and most influential segment, accounting for an estimated 40% of the market share, driven by their applications in content creation, marketing, customer service, and coding assistance. Following closely are Image Generators, which are rapidly gaining traction with billions in market value, driven by their use in digital art, marketing, and design.

Key Growth Drivers for Dominant Segments:

- Enterprise:

- Scalability and Efficiency: Businesses are leveraging AI for automated content generation, code completion, and data analysis, leading to significant cost savings and productivity gains, estimated to save businesses billions annually.

- Personalization: AI-driven tools enable hyper-personalized marketing campaigns and customer interactions, boosting engagement and conversion rates, unlocking billions in new revenue streams.

- Innovation Acceleration: Generative AI is empowering R&D departments to rapidly prototype ideas, design new products, and accelerate scientific discovery, representing billions in future economic impact.

- Text Generators:

- Content Marketing and SEO: The demand for high-quality, SEO-optimized content is insatiable, with text generators providing a cost-effective and scalable solution, generating billions in marketing expenditure.

- Software Development: AI-powered code generation and debugging tools are dramatically increasing developer productivity, saving billions in development time and costs.

- Customer Service Automation: Chatbots and virtual assistants powered by advanced LLMs are revolutionizing customer support, improving response times and customer satisfaction, impacting billions in operational expenditure.

- Image Generators:

- Digital Art and Design: Artists and designers are using AI to create novel visuals, accelerate design workflows, and explore new creative possibilities, opening up billions in the creative economy.

- Marketing and Advertising: The ability to generate unique and compelling visuals for advertising campaigns is a major draw, driving billions in marketing spend.

- Product Visualization: Businesses are using AI to create realistic product mockups and visualizations, improving e-commerce experiences and reducing prototyping costs, adding billions in efficiency.

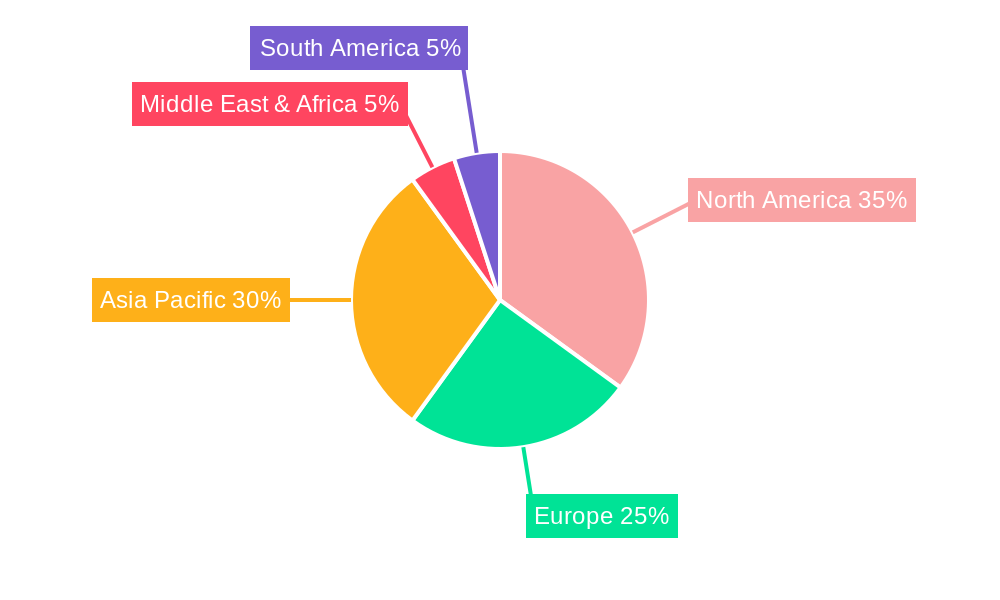

Regionally, North America and Europe are currently leading the Generative AI tools market, driven by strong technological ecosystems, significant venture capital investment, and a high concentration of enterprises adopting these technologies, contributing billions to the global market. However, the Asia-Pacific region is showing the fastest growth trajectory, fueled by government initiatives, increasing digital adoption, and the presence of major tech players like Baidu, indicating billions in future market potential. The increasing accessibility and affordability of Generative AI tools are also expected to drive adoption in emerging markets, further expanding the global reach and impact of this transformative technology.

Generative AI Tools Product Analysis

Generative AI tools are witnessing a rapid evolution characterized by remarkable product innovations that are redefining content creation, code development, and complex problem-solving. Key advancements include the development of larger and more sophisticated language models that exhibit enhanced coherence, creativity, and factual accuracy in text generation, such as those pioneered by OpenAI and Anthropic. Image generation models are achieving unprecedented photorealism and artistic versatility, enabling applications from marketing collateral to scientific visualization. Code generation tools, like those being developed by Databricks and IBM, are significantly accelerating software development cycles by automating boilerplate code, suggesting optimizations, and even assisting in debugging. The competitive advantage lies in the ability of these tools to offer speed, scalability, and novel outputs that were previously unattainable or prohibitively expensive, thereby unlocking billions in new efficiencies and creative potential across industries.

Key Drivers, Barriers & Challenges in Generative AI Tools

Key Drivers:

The Generative AI Tools market is propelled by a powerful combination of technological, economic, and policy-driven factors. Technological advancements, particularly in deep learning, neural networks, and transformer architectures, are the primary catalysts, enabling increasingly sophisticated and human-like content generation. Economically, the promise of significant productivity gains, cost reductions in content creation and software development, and the opening of new revenue streams for businesses are immense, driving billions in investment and adoption. Policy-driven initiatives, though still evolving, are increasingly focused on fostering innovation in AI research and development, while also considering ethical guidelines, which indirectly supports market growth by creating a more structured environment. The insatiable demand for personalized content, efficient code generation, and rapid prototyping across industries further fuels this growth, creating billions in market opportunities.

Barriers & Challenges:

Despite its rapid ascent, the Generative AI Tools market faces substantial barriers and challenges that could impact its trajectory. Regulatory complexities surrounding data privacy, intellectual property rights for AI-generated content, and ethical considerations related to bias and misinformation are significant hurdles, with potential costs running into billions if not addressed proactively. Supply chain issues, particularly concerning the availability of specialized AI hardware (e.g., advanced GPUs) and the talent required to develop and deploy these complex models, can also lead to bottlenecks and increased operational costs. Competitive pressures are intensifying, with established tech giants and a surge of agile startups vying for market share, leading to rapid commoditization of certain functionalities and demanding continuous innovation to maintain a competitive edge. The cost of training and maintaining large AI models remains a significant financial burden for many organizations, potentially limiting widespread adoption, despite the potential for billions in long-term savings.

Growth Drivers in the Generative AI Tools Market

The Generative AI Tools market is experiencing robust growth driven by several interconnected factors. Technologically, continuous advancements in neural network architectures, such as the scaling and refinement of Large Language Models (LLMs) and diffusion models, are enabling more sophisticated and nuanced content generation. Economically, the promise of enhanced productivity, reduced operational costs for content creation and software development, and the creation of novel business models is a significant motivator for investment and adoption, unlocking billions in economic value. Regulatory frameworks, while still evolving, are increasingly supportive of AI innovation, with governments recognizing the strategic importance of this technology, thereby creating a favorable environment for growth. Furthermore, the ever-increasing demand for personalized and engaging digital content across all sectors, coupled with the need for efficient software development processes, creates a substantial market pull. For instance, the demand for marketing content alone represents billions in annual expenditure that Generative AI can help optimize.

Challenges Impacting Generative AI Tools Growth

The rapid growth of the Generative AI Tools market is not without its significant challenges. Regulatory complexities surrounding data privacy, intellectual property rights, and the potential for misuse (e.g., deepfakes, misinformation) pose substantial ethical and legal hurdles that could lead to costly compliance measures or market restrictions, impacting billions in projected revenue. Supply chain issues, particularly concerning the availability of high-performance computing hardware necessary for training and deploying advanced AI models, can create bottlenecks and increase development costs, potentially delaying market expansion. Competitive pressures are intense, with a proliferation of startups and established tech giants vying for dominance, leading to rapid commoditization and a constant need for differentiation. The significant computational resources and expertise required to develop and maintain state-of-the-art Generative AI models present a substantial barrier to entry for smaller players and can lead to ongoing high operational costs, representing billions in R&D and infrastructure expenditure.

Key Players Shaping the Generative AI Tools Market

- OpenAI

- Cohere

- Meta Platforms

- AlphaSense

- Gong

- Anthropic

- Databricks

- C3.ai

- Writer

- Baidu

- IBM

- Intuit

- Advanced Micro Devices

- Adobe

- Microsoft

- Alphabet

- Jasper AI

- Typeface AI

- Keyway

- Glean

Significant Generative AI Tools Industry Milestones

- 2019: Introduction of GPT-2 by OpenAI, demonstrating advanced text generation capabilities, sparking broader interest in LLMs.

- 2020: Release of DALL-E by OpenAI, showcasing impressive text-to-image generation, marking a significant leap in multimodal AI.

- 2021: AlphaSense expands its AI-powered market intelligence platform, integrating advanced NLP for enterprise insights, with billions invested in the sector.

- 2022: Stability AI releases Stable Diffusion, democratizing high-quality image generation and fostering a vibrant open-source community, impacting billions in creative industries.

- 2023 (Early): OpenAI launches ChatGPT, achieving widespread public adoption and demonstrating the power of conversational AI for billions of users.

- 2023 (Mid): Google announces Gemini, its most capable and general AI model, designed to be multimodal and highly efficient, signaling billions in future competition.

- 2023 (Late): Anthropic releases Claude 2, emphasizing safety and helpfulness in its LLM, addressing growing concerns about AI ethics and responsible development, with billions in funding.

- 2024: Adobe integrates advanced Generative AI features into its Creative Cloud suite, offering powerful tools for designers and content creators, impacting billions in creative workflows.

- 2024: Microsoft heavily invests in and integrates OpenAI's models across its product suite, including Azure and Microsoft 365 Copilot, signifying a strategic push into AI-driven productivity, worth billions.

- 2025 (Estimated): Databricks further enhances its AI platform with advanced code generation and LLM deployment capabilities, catering to the growing enterprise demand for AI solutions, unlocking billions in new markets.

Future Outlook for Generative AI Tools Market

The future outlook for the Generative AI Tools market is exceptionally bright, poised for continued exponential growth and transformative impact across virtually every industry. The market is anticipated to expand by hundreds of billions by 2033, driven by ongoing breakthroughs in AI model efficiency, multimodality, and ethical alignment. Key growth catalysts include the increasing demand for personalized content at scale, the acceleration of software development cycles through advanced code generation, and the democratization of creative tools for both professionals and consumers. Strategic opportunities lie in the development of specialized AI solutions tailored to specific industry verticals, such as healthcare, finance, and education, as well as the integration of Generative AI into existing enterprise workflows to unlock unprecedented levels of productivity and innovation. The market potential is immense, with billions in economic value to be unlocked as AI continues to redefine the boundaries of human creativity and problem-solving.

Generative AI Tools Segmentation

-

1. Application

- 1.1. Private

- 1.2. Enterprise

-

2. Types

- 2.1. Text Generators

- 2.2. Image Generators

- 2.3. Code Generators

- 2.4. Music and Audio Generators

- 2.5. Other

Generative AI Tools Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Generative AI Tools Regional Market Share

Geographic Coverage of Generative AI Tools

Generative AI Tools REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 41.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Private

- 5.1.2. Enterprise

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Text Generators

- 5.2.2. Image Generators

- 5.2.3. Code Generators

- 5.2.4. Music and Audio Generators

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Private

- 6.1.2. Enterprise

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Text Generators

- 6.2.2. Image Generators

- 6.2.3. Code Generators

- 6.2.4. Music and Audio Generators

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Private

- 7.1.2. Enterprise

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Text Generators

- 7.2.2. Image Generators

- 7.2.3. Code Generators

- 7.2.4. Music and Audio Generators

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Private

- 8.1.2. Enterprise

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Text Generators

- 8.2.2. Image Generators

- 8.2.3. Code Generators

- 8.2.4. Music and Audio Generators

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Private

- 9.1.2. Enterprise

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Text Generators

- 9.2.2. Image Generators

- 9.2.3. Code Generators

- 9.2.4. Music and Audio Generators

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Generative AI Tools Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Private

- 10.1.2. Enterprise

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Text Generators

- 10.2.2. Image Generators

- 10.2.3. Code Generators

- 10.2.4. Music and Audio Generators

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 OpenAI

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cohere

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Meta Platforms

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 AlphaSense

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Gong

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Anthropic

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Databricks

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 C3.ai

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Writer

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Baidu

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 IBM

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Intuit

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Advanced Micro DeviceS

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Adobe

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Microsoft

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Alphabet

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Jasper AI

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Typeface AI

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Keyway

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Glean

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 OpenAI

List of Figures

- Figure 1: Global Generative AI Tools Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Generative AI Tools Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Generative AI Tools Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Generative AI Tools Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Generative AI Tools Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Generative AI Tools Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Generative AI Tools Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Generative AI Tools Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Generative AI Tools Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Generative AI Tools Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Generative AI Tools Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Generative AI Tools Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Generative AI Tools Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Generative AI Tools Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Generative AI Tools Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Generative AI Tools Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Generative AI Tools Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Generative AI Tools Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Generative AI Tools Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Generative AI Tools Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Generative AI Tools Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Generative AI Tools Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Generative AI Tools Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Generative AI Tools Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Generative AI Tools Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Generative AI Tools Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Generative AI Tools Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Generative AI Tools Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Generative AI Tools Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Generative AI Tools Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Generative AI Tools Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Generative AI Tools Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Generative AI Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Generative AI Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Generative AI Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Generative AI Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Generative AI Tools Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Generative AI Tools Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Generative AI Tools Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Generative AI Tools Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Generative AI Tools?

The projected CAGR is approximately 41.53%.

2. Which companies are prominent players in the Generative AI Tools?

Key companies in the market include OpenAI, Cohere, Meta Platforms, AlphaSense, Gong, Anthropic, Databricks, C3.ai, Writer, Baidu, IBM, Intuit, Advanced Micro DeviceS, Adobe, Microsoft, Alphabet, Jasper AI, Typeface AI, Keyway, Glean.

3. What are the main segments of the Generative AI Tools?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Generative AI Tools," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Generative AI Tools report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Generative AI Tools?

To stay informed about further developments, trends, and reports in the Generative AI Tools, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence