Key Insights

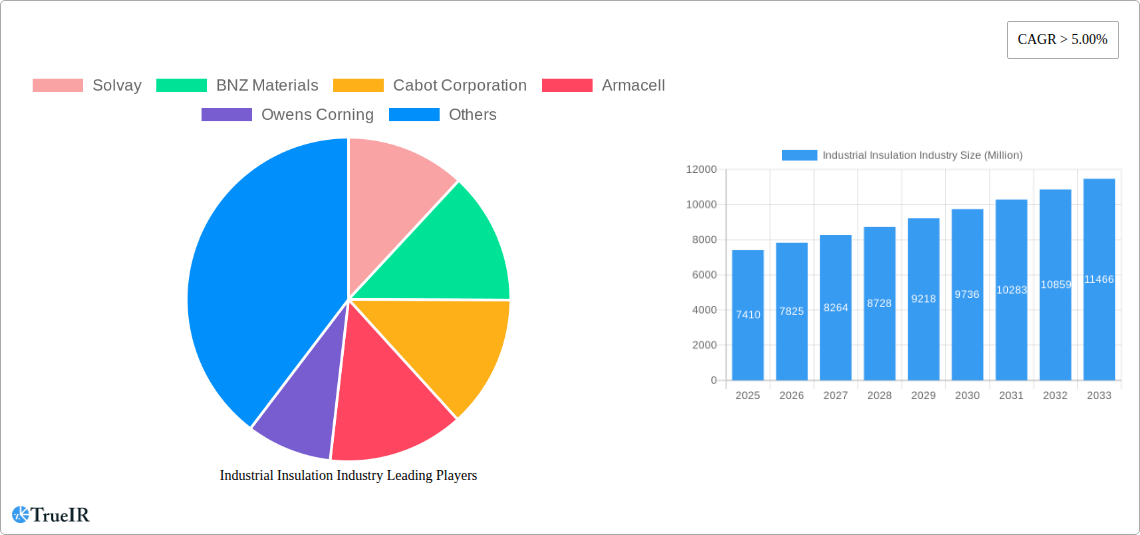

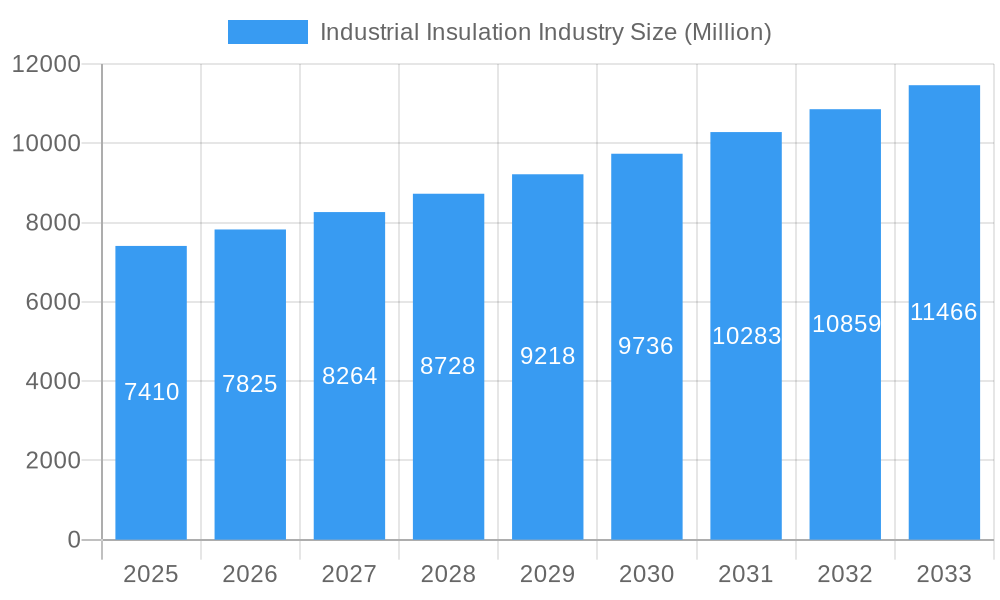

The industrial insulation market, valued at $7.41 billion in 2025, is projected for robust growth, exceeding a 5% compound annual growth rate (CAGR) through 2033. This expansion is fueled by several key drivers. Increasing energy efficiency regulations across various sectors, particularly in construction, power generation, and oil & gas, are mandating the use of insulation materials to minimize energy loss and reduce carbon footprints. Furthermore, the burgeoning construction industry globally, coupled with rising demand for energy-efficient buildings, is a significant catalyst for market growth. Advances in insulation technology, including the development of more efficient and sustainable materials like aerogel and vacuum insulation panels, are also contributing to market expansion. Growth is further supported by the increasing adoption of insulation in high-temperature applications within the chemical and petrochemical industries. While pricing pressures and material availability can present challenges, the long-term outlook remains positive due to the overarching need for energy conservation and the inherent value proposition of industrial insulation in reducing operational costs.

Industrial Insulation Industry Market Size (In Billion)

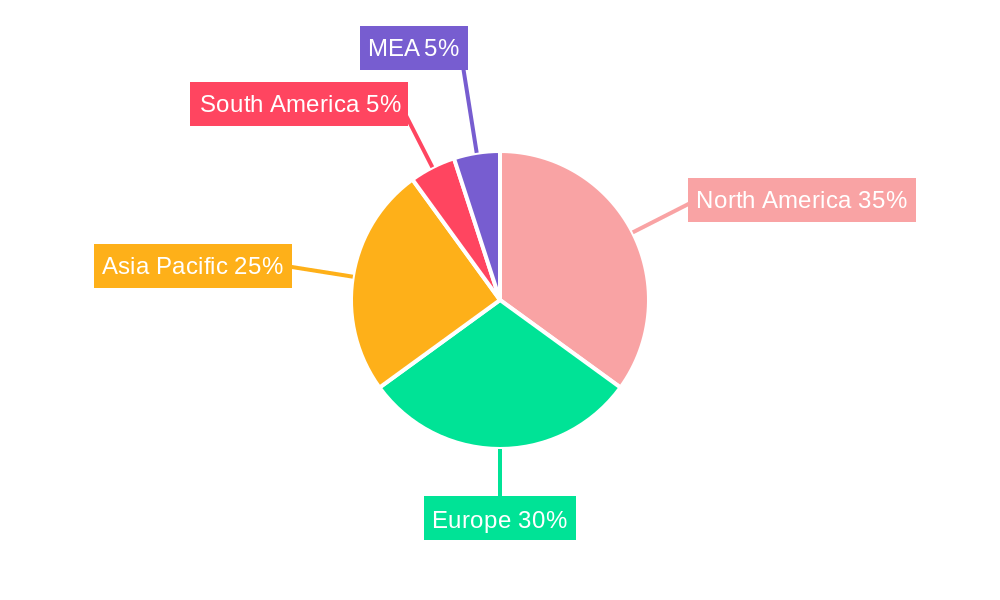

Segment-wise, mineral wool and fiberglass continue to dominate the insulation material market due to their established presence and cost-effectiveness. However, the demand for advanced materials like foamed plastics and calcium silicate is steadily growing due to their superior performance characteristics in specific applications. In terms of product type, blankets and boards maintain a significant share, driven by their versatility and widespread use across diverse sectors. Geographically, North America and Europe currently hold substantial market share, reflecting established infrastructure and robust regulatory frameworks. However, the Asia-Pacific region is expected to witness the fastest growth in the forecast period, driven by rapid industrialization and infrastructure development in countries like China and India. Key players like Owens Corning, Rockwool, and BASF are strategically investing in R&D and expanding their geographical footprint to capitalize on these market opportunities. The competitive landscape is characterized by a mix of established multinational corporations and regional players, fostering innovation and ensuring a wide range of product offerings catering to specific application needs.

Industrial Insulation Industry Company Market Share

Industrial Insulation Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the global industrial insulation market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report covers the period 2019-2033, with a focus on the forecast period 2025-2033 and a base year of 2025. Expect in-depth analysis of market size (in Millions), key players such as Solvay, BNZ Materials, Cabot Corporation, Armacell, Owens Corning, BASF SE, Rockwool A/S, Knauf Insulation, Temati Group, INSUL-FAB, Johns Manville-Berkshire Hathaway Company, and Jays Refractory Specialists, and emerging trends shaping this dynamic sector. The report segments the market by insulation material (mineral wool, fiberglass, foamed plastics, calcium silicate, and others), product type (blanket, board, pipe, and others), and end-user industry (automotive, chemical & petrochemical, construction, electrical & electronics, oil & gas, power generation, and others).

Industrial Insulation Industry Market Structure & Competitive Landscape

The industrial insulation market is characterized by a moderately concentrated landscape, with a few major players commanding significant market share. The industry's concentration ratio (CR4) is estimated to be around xx%, reflecting the presence of large multinational corporations alongside smaller, specialized companies. Innovation is a key driver, with companies continuously developing advanced materials and technologies to improve insulation performance, energy efficiency, and sustainability. Stringent environmental regulations, particularly concerning greenhouse gas emissions and hazardous materials, significantly impact industry practices and product development. Substitutes for industrial insulation materials include alternative construction techniques and energy-saving technologies, posing a potential competitive challenge. The market exhibits strong end-user segmentation, with the construction, oil & gas, and power generation sectors being major consumers. Mergers and acquisitions (M&A) activity is relatively frequent, driven by companies seeking to expand their product portfolios, geographic reach, and technological capabilities. The total value of M&A transactions in the period 2019-2024 is estimated at approximately $xx Million.

- Market Concentration: CR4 estimated at xx%

- Innovation Drivers: Development of advanced materials, energy efficiency improvements, sustainability focus

- Regulatory Impacts: Stringent environmental regulations impacting material choices and production processes

- Product Substitutes: Alternative construction methods, energy-saving technologies

- End-User Segmentation: Construction, Oil & Gas, Power Generation as key segments

- M&A Trends: Significant activity driven by expansion and technological acquisition

Industrial Insulation Industry Market Trends & Opportunities

The global industrial insulation market is experiencing robust growth, propelled by the twin engines of increasing urbanization and widespread infrastructure development. A significant contributing factor is the imposition of increasingly stringent energy efficiency regulations across a diverse array of end-use sectors. Analysts project the market size to reach an impressive $XX Million by 2033, demonstrating a compound annual growth rate (CAGR) of XX% during the forecast period spanning from 2025 to 2033. This upward trajectory is further amplified by continuous technological advancements, which are yielding high-performance insulation materials characterized by enhanced thermal resistance, superior durability, and improved fire safety. A notable shift in consumer preferences is the growing emphasis on eco-friendly and sustainable insulation solutions, presenting lucrative opportunities for manufacturers that prioritize products with a reduced environmental impact. The competitive landscape is intensifying, with both established industry titans and agile new entrants actively vying for greater market share. Moreover, technological paradigm shifts, such as the integration of smart insulation systems and the optimization of manufacturing processes, are consistently driving efficiency gains. It's important to note that market penetration rates exhibit considerable variation across different geographical regions and end-use industries, with higher adoption rates typically observed in developed economies and sectors subject to stringent energy efficiency mandates.

Dominant Markets & Segments in Industrial Insulation Industry

The construction sector continues to be the primary driver of demand for industrial insulation materials, commanding an estimated XX% of the market share in 2025. This dominance is largely attributed to ongoing and expanding infrastructure projects worldwide, with a particular surge observed in developing economies. Among the various insulation materials, mineral wool retains the largest market share, closely followed by fiberglass. From a product perspective, pipe insulation represents a significant and consistently in-demand segment, stemming from the pervasive need for effective thermal management across a multitude of industrial applications.

- Leading Region/Country: [Insert leading region/country based on comprehensive market analysis and recent data]

- Key Growth Drivers:

- Expansion of critical infrastructure projects, especially in rapidly developing economies.

- The implementation and enforcement of increasingly stringent energy efficiency regulations.

- A rising demand for sustainable and environmentally conscious building materials.

- Sustained growth in industrial production across a broad spectrum of sectors.

Dominant Segments Analysis:

- Insulation Material: Mineral wool continues to lead due to its exceptional thermal performance, cost-effectiveness, and inherent sustainability benefits.

- Product Type: Pipe insulation remains a cornerstone of the market, driven by its indispensable role and consistent demand in diverse industrial applications requiring precise thermal control.

- End-User Industry: The construction sector retains its leading position, fueled by substantial infrastructure investments and the ongoing evolution of building codes and energy performance standards.

Industrial Insulation Industry Product Analysis

The industrial insulation market is characterized by a dynamic landscape of continuous product innovation, primarily driven by the persistent demand for enhanced thermal performance, improved long-term durability, and a growing preference for environmentally responsible materials. Cutting-edge innovations include the development of advanced mineral wool formulations that boast superior thermal resistance and exceptional acoustic dampening properties. Furthermore, lightweight and highly flexible fiberglass insulation solutions are emerging, significantly simplifying installation processes. A notable advancement is the introduction of high-performance vacuum insulation panels (VIPs), which offer an unparalleled level of thermal efficiency. These groundbreaking innovations are meticulously designed to cater to the diverse and specific application needs across various end-user industries. They not only deliver superior performance but also proactively address critical sustainability concerns, contributing to significant energy savings and a reduced carbon footprint. The competitive edge in this market is often forged through proprietary material formulations, the adoption of innovative and efficient manufacturing processes, and the delivery of demonstrably superior thermal efficiency, all of which translate into tangible cost savings and reduced energy consumption for end-users.

Key Drivers, Barriers & Challenges in Industrial Insulation Industry

Key Drivers:

- Growing demand for energy efficiency: Driven by rising energy costs and environmental concerns, leading to increased adoption of insulation in buildings and industrial processes.

- Stringent building codes and regulations: Government regulations promoting energy efficiency in construction and industrial sectors are boosting the demand.

- Technological advancements: Innovations in materials and manufacturing processes are enhancing performance, durability, and cost-effectiveness.

Challenges:

- Fluctuating raw material prices: Prices of key raw materials, such as glass, minerals, and polymers, can impact profitability and pricing strategies. The impact is estimated to be around xx% on the overall market value in the historical period.

- Supply chain disruptions: Global events can disrupt the supply of raw materials and finished products, leading to delays and increased costs.

- Intense competition: The presence of numerous established players and new entrants creates a competitive landscape, pressuring margins and requiring continuous innovation.

Growth Drivers in the Industrial Insulation Industry Market

The sustained growth of the industrial insulation market is primarily propelled by a confluence of factors: an escalating demand for enhanced energy efficiency across all sectors, the implementation of more rigorous building codes and standards, and the relentless pace of technological advancements in material science and manufacturing. The continuous rise in energy costs, coupled with growing global awareness of environmental concerns, is a powerful catalyst for the widespread adoption of insulation in both buildings and complex industrial processes. Government mandates and incentives promoting energy efficiency further bolster this demand. Innovations in insulation materials, encompassing novel compositions and advanced manufacturing techniques, are consistently improving performance, extending product lifespans, and making these solutions more accessible and affordable. Collectively, these interwoven factors are significantly contributing to the market's robust expansion.

Challenges Impacting Industrial Insulation Industry Growth

Several factors hinder the industrial insulation market's growth, including fluctuating raw material prices impacting profitability. Supply chain disruptions caused by global events lead to production delays and higher costs. Intense competition among established and new players pressures margins and necessitates continuous product innovation. These factors pose challenges to sustained market growth.

Key Players Shaping the Industrial Insulation Industry Market

- Solvay

- BNZ Materials

- Cabot Corporation

- Armacell

- Owens Corning

- BASF SE

- Rockwool A/S

- Knauf Insulation

- Temati Group

- INSUL-FAB

- Johns Manville-Berkshire Hathaway Company

- Jays Refractory Specialists

Significant Industrial Insulation Industry Milestones

- October 2022: Knauf Group's significant investment (~USD 133.4 Million) in expanding mineral wool production capacity in Romania signals a major commitment to this market segment. This will enhance their supply capabilities and potentially impact market pricing.

- November 2022: BEWI's acquisition of Aislamientos y Envases SL expands their market presence in Spain and strengthens their EPS-based insulation product portfolio. This strategic move enhances competitive positioning within a key geographic market.

Future Outlook for Industrial Insulation Industry Market

The industrial insulation market is poised for continued growth, driven by long-term trends toward energy efficiency, sustainable building practices, and industrial expansion. Strategic opportunities exist for companies focused on innovation, particularly in areas such as sustainable materials, smart insulation technologies, and improved installation methods. The market’s potential is substantial, particularly in emerging economies where infrastructure development is rapid, and demand for energy-efficient solutions is rising.

Industrial Insulation Industry Segmentation

-

1. Insulation Material

- 1.1. Mineral Wool

- 1.2. Fiber Glass

- 1.3. Foamed Plastics

- 1.4. Calcium Silicate

- 1.5. Other Insulation Materials

-

2. Product

- 2.1. Blanket

- 2.2. Board

- 2.3. Pipe

- 2.4. Other Products

-

3. End-user Industry

- 3.1. Automotive

- 3.2. Chemical and Petrochemical

- 3.3. Construction

- 3.4. Electrical and Electronics

- 3.5. Oil and Gas

- 3.6. Power Generation

- 3.7. Other End-user Industries

Industrial Insulation Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. South Africa

- 6.2. Rest of Middle East

Industrial Insulation Industry Regional Market Share

Geographic Coverage of Industrial Insulation Industry

Industrial Insulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 5.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insulation Material

- 5.1.1. Mineral Wool

- 5.1.2. Fiber Glass

- 5.1.3. Foamed Plastics

- 5.1.4. Calcium Silicate

- 5.1.5. Other Insulation Materials

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Blanket

- 5.2.2. Board

- 5.2.3. Pipe

- 5.2.4. Other Products

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Automotive

- 5.3.2. Chemical and Petrochemical

- 5.3.3. Construction

- 5.3.4. Electrical and Electronics

- 5.3.5. Oil and Gas

- 5.3.6. Power Generation

- 5.3.7. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East

- 5.4.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Insulation Material

- 6. Global Industrial Insulation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insulation Material

- 6.1.1. Mineral Wool

- 6.1.2. Fiber Glass

- 6.1.3. Foamed Plastics

- 6.1.4. Calcium Silicate

- 6.1.5. Other Insulation Materials

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Blanket

- 6.2.2. Board

- 6.2.3. Pipe

- 6.2.4. Other Products

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Automotive

- 6.3.2. Chemical and Petrochemical

- 6.3.3. Construction

- 6.3.4. Electrical and Electronics

- 6.3.5. Oil and Gas

- 6.3.6. Power Generation

- 6.3.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Insulation Material

- 7. Asia Pacific Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Insulation Material

- 7.1.1. Mineral Wool

- 7.1.2. Fiber Glass

- 7.1.3. Foamed Plastics

- 7.1.4. Calcium Silicate

- 7.1.5. Other Insulation Materials

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Blanket

- 7.2.2. Board

- 7.2.3. Pipe

- 7.2.4. Other Products

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Automotive

- 7.3.2. Chemical and Petrochemical

- 7.3.3. Construction

- 7.3.4. Electrical and Electronics

- 7.3.5. Oil and Gas

- 7.3.6. Power Generation

- 7.3.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Insulation Material

- 8. North America Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Insulation Material

- 8.1.1. Mineral Wool

- 8.1.2. Fiber Glass

- 8.1.3. Foamed Plastics

- 8.1.4. Calcium Silicate

- 8.1.5. Other Insulation Materials

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Blanket

- 8.2.2. Board

- 8.2.3. Pipe

- 8.2.4. Other Products

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Automotive

- 8.3.2. Chemical and Petrochemical

- 8.3.3. Construction

- 8.3.4. Electrical and Electronics

- 8.3.5. Oil and Gas

- 8.3.6. Power Generation

- 8.3.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Insulation Material

- 9. Europe Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Insulation Material

- 9.1.1. Mineral Wool

- 9.1.2. Fiber Glass

- 9.1.3. Foamed Plastics

- 9.1.4. Calcium Silicate

- 9.1.5. Other Insulation Materials

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Blanket

- 9.2.2. Board

- 9.2.3. Pipe

- 9.2.4. Other Products

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Automotive

- 9.3.2. Chemical and Petrochemical

- 9.3.3. Construction

- 9.3.4. Electrical and Electronics

- 9.3.5. Oil and Gas

- 9.3.6. Power Generation

- 9.3.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Insulation Material

- 10. South America Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Insulation Material

- 10.1.1. Mineral Wool

- 10.1.2. Fiber Glass

- 10.1.3. Foamed Plastics

- 10.1.4. Calcium Silicate

- 10.1.5. Other Insulation Materials

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Blanket

- 10.2.2. Board

- 10.2.3. Pipe

- 10.2.4. Other Products

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Automotive

- 10.3.2. Chemical and Petrochemical

- 10.3.3. Construction

- 10.3.4. Electrical and Electronics

- 10.3.5. Oil and Gas

- 10.3.6. Power Generation

- 10.3.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Insulation Material

- 11. Middle East Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Insulation Material

- 11.1.1. Mineral Wool

- 11.1.2. Fiber Glass

- 11.1.3. Foamed Plastics

- 11.1.4. Calcium Silicate

- 11.1.5. Other Insulation Materials

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Blanket

- 11.2.2. Board

- 11.2.3. Pipe

- 11.2.4. Other Products

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Automotive

- 11.3.2. Chemical and Petrochemical

- 11.3.3. Construction

- 11.3.4. Electrical and Electronics

- 11.3.5. Oil and Gas

- 11.3.6. Power Generation

- 11.3.7. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Insulation Material

- 12. Saudi Arabia Industrial Insulation Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Insulation Material

- 12.1.1. Mineral Wool

- 12.1.2. Fiber Glass

- 12.1.3. Foamed Plastics

- 12.1.4. Calcium Silicate

- 12.1.5. Other Insulation Materials

- 12.2. Market Analysis, Insights and Forecast - by Product

- 12.2.1. Blanket

- 12.2.2. Board

- 12.2.3. Pipe

- 12.2.4. Other Products

- 12.3. Market Analysis, Insights and Forecast - by End-user Industry

- 12.3.1. Automotive

- 12.3.2. Chemical and Petrochemical

- 12.3.3. Construction

- 12.3.4. Electrical and Electronics

- 12.3.5. Oil and Gas

- 12.3.6. Power Generation

- 12.3.7. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Insulation Material

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Solvay

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 BNZ Materials

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Cabot Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Armacell

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Owens Corning

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 BASF SE

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Rockwool A/S

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Knauf Insulation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Temati Group

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 INSUL-FAB

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Johns Manville-Berkshire Hathway Company

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Jays Refractory Specialists

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.1 Solvay

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Industrial Insulation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Industrial Insulation Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 4: Asia Pacific Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 5: Asia Pacific Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 6: Asia Pacific Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 7: Asia Pacific Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 8: Asia Pacific Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 9: Asia Pacific Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: Asia Pacific Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 11: Asia Pacific Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 12: Asia Pacific Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 13: Asia Pacific Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: Asia Pacific Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: Asia Pacific Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: Asia Pacific Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 17: Asia Pacific Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: North America Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 20: North America Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 21: North America Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 22: North America Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 23: North America Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 24: North America Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 25: North America Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 26: North America Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 27: North America Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 28: North America Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 29: North America Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: North America Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: North America Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: North America Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 33: North America Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: North America Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Europe Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 36: Europe Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 37: Europe Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 38: Europe Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 39: Europe Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 40: Europe Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 41: Europe Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 42: Europe Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 43: Europe Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 44: Europe Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 45: Europe Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Europe Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Europe Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Europe Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 49: Europe Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Europe Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 52: South America Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 53: South America Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 54: South America Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 55: South America Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 56: South America Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 57: South America Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 58: South America Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 59: South America Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 60: South America Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 61: South America Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 62: South America Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 63: South America Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: South America Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 65: South America Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: South America Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: Middle East Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 68: Middle East Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 69: Middle East Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 70: Middle East Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 71: Middle East Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 72: Middle East Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 73: Middle East Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 74: Middle East Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 75: Middle East Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 76: Middle East Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 77: Middle East Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 78: Middle East Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 79: Middle East Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: Middle East Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 81: Middle East Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

- Figure 83: Saudi Arabia Industrial Insulation Industry Revenue (Million), by Insulation Material 2025 & 2033

- Figure 84: Saudi Arabia Industrial Insulation Industry Volume (K Tons), by Insulation Material 2025 & 2033

- Figure 85: Saudi Arabia Industrial Insulation Industry Revenue Share (%), by Insulation Material 2025 & 2033

- Figure 86: Saudi Arabia Industrial Insulation Industry Volume Share (%), by Insulation Material 2025 & 2033

- Figure 87: Saudi Arabia Industrial Insulation Industry Revenue (Million), by Product 2025 & 2033

- Figure 88: Saudi Arabia Industrial Insulation Industry Volume (K Tons), by Product 2025 & 2033

- Figure 89: Saudi Arabia Industrial Insulation Industry Revenue Share (%), by Product 2025 & 2033

- Figure 90: Saudi Arabia Industrial Insulation Industry Volume Share (%), by Product 2025 & 2033

- Figure 91: Saudi Arabia Industrial Insulation Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 92: Saudi Arabia Industrial Insulation Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 93: Saudi Arabia Industrial Insulation Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 94: Saudi Arabia Industrial Insulation Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 95: Saudi Arabia Industrial Insulation Industry Revenue (Million), by Country 2025 & 2033

- Figure 96: Saudi Arabia Industrial Insulation Industry Volume (K Tons), by Country 2025 & 2033

- Figure 97: Saudi Arabia Industrial Insulation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 98: Saudi Arabia Industrial Insulation Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 2: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 3: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 4: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 5: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Industrial Insulation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Industrial Insulation Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 10: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 11: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 12: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 13: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: China Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: India Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: India Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Japan Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: South Korea Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: South Korea Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 28: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 29: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 30: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 31: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 32: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 33: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 35: United States Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: United States Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 37: Canada Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Canada Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 39: Mexico Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Mexico Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 41: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 42: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 43: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 44: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 45: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 46: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 47: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 49: Germany Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Germany Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: United Kingdom Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: United Kingdom Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 53: France Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: France Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 55: Italy Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Italy Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 57: Rest of Europe Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Rest of Europe Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 60: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 61: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 62: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 63: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 64: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 65: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 66: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 67: Brazil Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: Brazil Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 69: Argentina Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: Argentina Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 71: Rest of South America Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Rest of South America Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 73: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 74: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 75: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 76: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 77: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 78: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 79: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 80: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 81: Global Industrial Insulation Industry Revenue Million Forecast, by Insulation Material 2020 & 2033

- Table 82: Global Industrial Insulation Industry Volume K Tons Forecast, by Insulation Material 2020 & 2033

- Table 83: Global Industrial Insulation Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 84: Global Industrial Insulation Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 85: Global Industrial Insulation Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 86: Global Industrial Insulation Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 87: Global Industrial Insulation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 88: Global Industrial Insulation Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 89: South Africa Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: South Africa Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 91: Rest of Middle East Industrial Insulation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Middle East Industrial Insulation Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Insulation Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the Industrial Insulation Industry?

Key companies in the market include Solvay, BNZ Materials, Cabot Corporation, Armacell, Owens Corning, BASF SE, Rockwool A/S, Knauf Insulation, Temati Group, INSUL-FAB, Johns Manville-Berkshire Hathway Company, Jays Refractory Specialists.

3. What are the main segments of the Industrial Insulation Industry?

The market segments include Insulation Material, Product, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.41 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Construction and Power Generation Industry; Regulatory Support to Increase Energy Efficiency.

6. What are the notable trends driving market growth?

Power Generation Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

Environmental Hazards; Other Restraints.

8. Can you provide examples of recent developments in the market?

November 2022: BEWI acquired Aislamientos y Envases SL, a Spanish insulation company that provides EPS-based products for packaging and industrial applications, to expand its geographic footprint and strengthen its insulation solutions product portfolio in Spain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Insulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Insulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Insulation Industry?

To stay informed about further developments, trends, and reports in the Industrial Insulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence