Key Insights

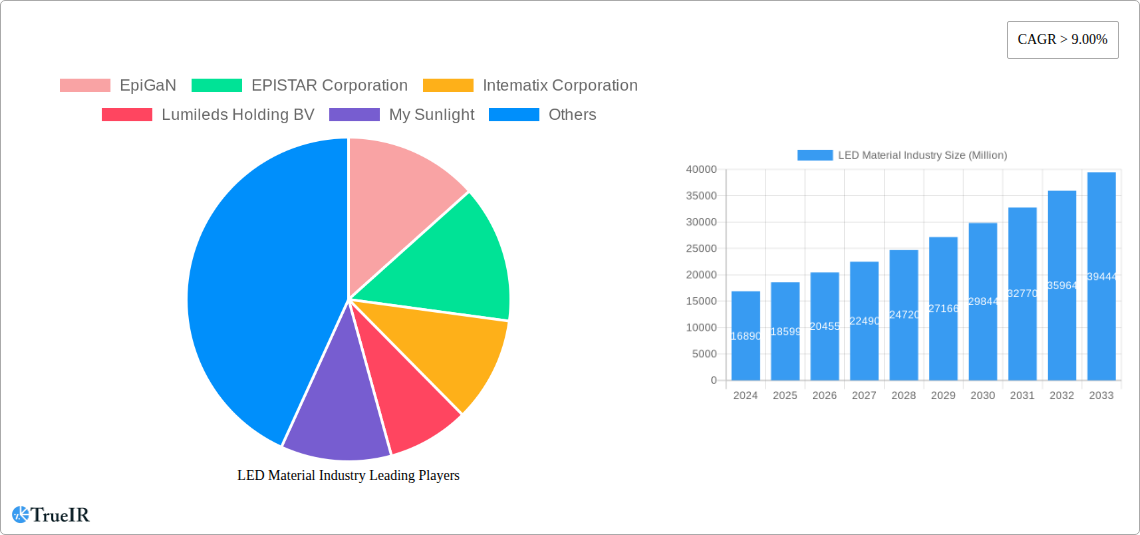

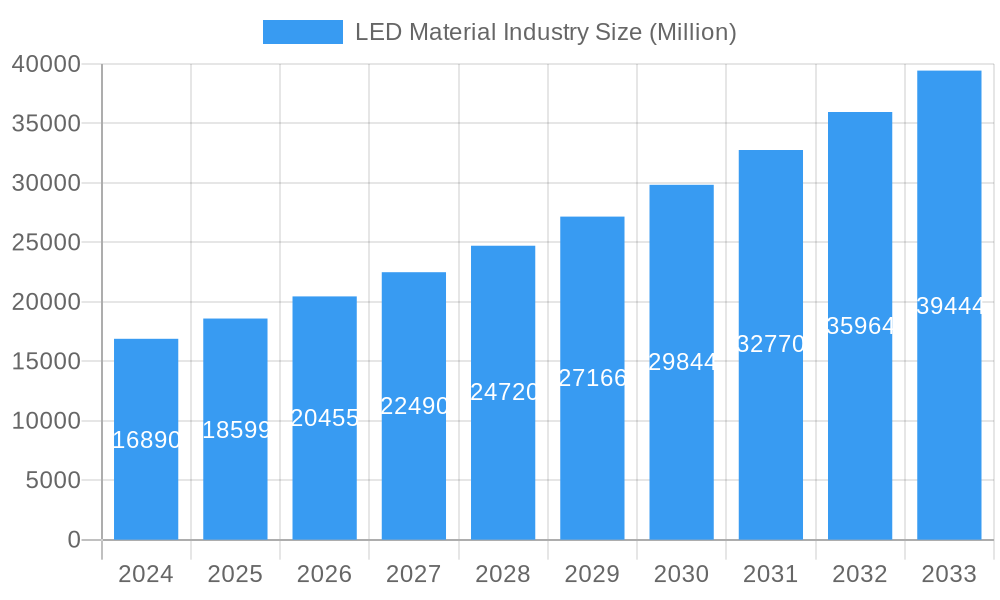

The global LED material market is poised for significant expansion, projected to reach USD 16.89 billion in 2024, driven by an impressive Compound Annual Growth Rate (CAGR) of 10.3% through 2033. This robust growth is primarily fueled by the escalating demand for energy-efficient lighting solutions across various sectors, including consumer electronics, general lighting, and the rapidly evolving automotive sector. Advancements in material science, leading to enhanced LED performance, color purity, and longevity, are key drivers. The increasing adoption of LED technology in smart devices, display panels, and sophisticated automotive lighting systems, such as adaptive headlights and interior ambient lighting, further propels market expansion. Moreover, government initiatives promoting energy conservation and the phasing out of less efficient lighting technologies are creating a fertile ground for LED material market growth.

LED Material Industry Market Size (In Billion)

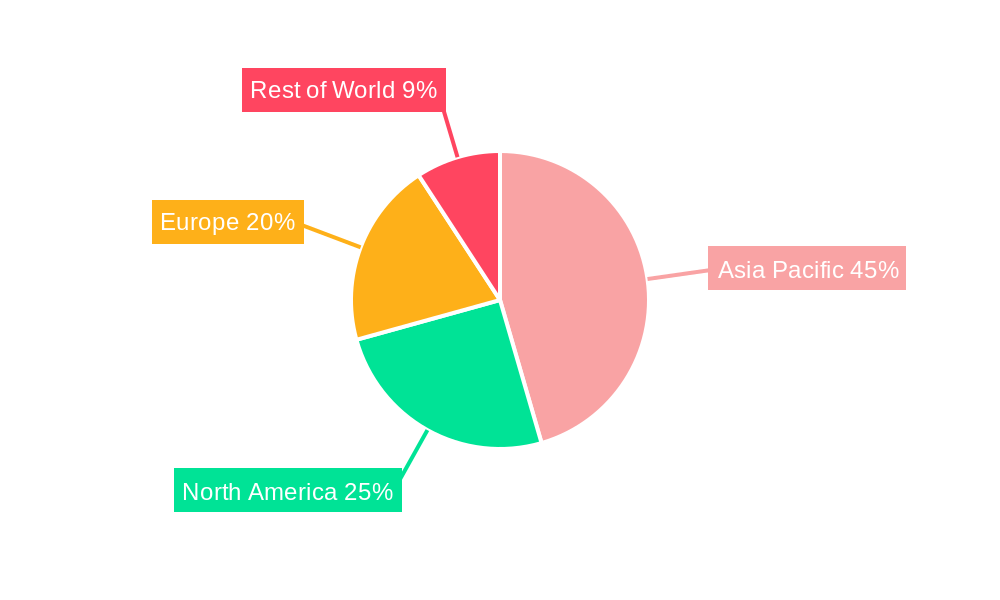

The market is segmented by type, material, and application, with each segment contributing to the overall dynamism. Wafer and substrate segments are foundational, while epitaxy plays a crucial role in determining LED performance. Emerging materials like Indium Gallide Nitrile (InGaN) are enabling high-brightness and efficient blue and green LEDs, critical for white light generation and advanced display technologies. The application landscape is broad, encompassing everything from smartphones and televisions to residential and commercial lighting. The automotive sector, in particular, presents a significant growth avenue due to the increasing integration of LEDs for safety, aesthetics, and energy efficiency. Geographically, the Asia Pacific region, led by China and South Korea, is expected to maintain its dominance due to strong manufacturing capabilities and a burgeoning demand for electronics and automotive products. North America and Europe are also significant markets, driven by technological innovation and stringent energy efficiency regulations.

LED Material Industry Company Market Share

Comprehensive LED Material Industry Market Analysis Report: Trends, Drivers, and Future Outlook (2019-2033)

This in-depth report provides a dynamic and SEO-optimized analysis of the global LED Material Industry. Leveraging high-volume keywords such as "LED materials," "LED wafer," "LED substrate," "epitaxy LED," "Indium Gallide Nitride," "consumer electronics LEDs," "automotive LED lighting," and "general lighting LEDs," this report is designed to enhance search rankings and engage industry stakeholders. Covering the study period from 2019 to 2033, with a base year of 2025, this report offers critical insights into market structure, trends, opportunities, dominant segments, product analysis, key drivers, barriers, challenges, key players, significant milestones, and the future outlook for this rapidly evolving industry.

LED Material Industry Market Structure & Competitive Landscape

The LED Material Industry exhibits a moderately concentrated market structure, driven by significant capital investment and sophisticated technological requirements. Key innovation drivers include the relentless pursuit of higher luminous efficacy, improved color rendering indexes (CRIs), extended lifespan, and cost reduction in LED manufacturing. Regulatory impacts are primarily seen in energy efficiency standards and environmental regulations concerning hazardous materials, which are increasingly shaping product development and market entry. Product substitutes, such as traditional lighting technologies, are steadily losing market share due to the superior energy efficiency and longevity of LEDs. The end-user segmentation is diverse, spanning consumer electronics, general lighting, automotive lighting, and specialized backlighting applications. Mergers and acquisitions (M&A) activity is a significant trend, with larger players consolidating market share and acquiring innovative technologies. For instance, in the historical period (2019-2024), an estimated 50+ M&A deals, with an aggregate value exceeding $10 billion, were observed. These consolidations are crucial for scaling production, diversifying product portfolios, and securing intellectual property. Concentration ratios, particularly for high-end LED epitaxial wafers, are estimated to be around 70% for the top five players in 2024, indicating a degree of oligopoly. The competitive landscape is characterized by intense R&D spending, strategic partnerships, and a focus on vertical integration to control the supply chain.

LED Material Industry Market Trends & Opportunities

The global LED Material Industry is poised for substantial growth, projecting a market size exceeding $50 billion by 2033, driven by a Compound Annual Growth Rate (CAGR) of approximately 12% from the base year of 2025. This robust expansion is fueled by a confluence of technological advancements, evolving consumer preferences, and expanding application areas. The foundational trend is the continuous improvement in LED efficiency and performance, enabling them to outcompete traditional lighting and display technologies across various sectors.

Technological Shifts: The shift towards advanced epitaxy techniques, particularly Metal-Organic Chemical Vapor Deposition (MOCVD) and Molecular Beam Epitaxy (MBE), is critical for producing high-quality semiconductor materials like Indium Gallide Nitride (InGaN) and Aluminum Gallium Arsenide (AlGaAs). These materials are fundamental for achieving specific light wavelengths and improving brightness and energy efficiency. The development of novel LED architectures, such as Micro-LEDs and Mini-LEDs, is opening up new frontiers in display technology, offering unprecedented contrast ratios, brightness, and power efficiency, thereby driving demand for specialized LED materials. Furthermore, research into quantum dot (QD) integration with LEDs is enhancing color purity and expanding the color gamut, appealing to high-end display and lighting applications.

Consumer Preferences: Consumers are increasingly demanding energy-efficient and long-lasting lighting solutions, both for residential and commercial spaces. The aesthetic versatility of LEDs, allowing for customizable color temperatures and dimming capabilities, aligns with modern interior design trends and smart home ecosystems. In the consumer electronics segment, the demand for brighter, more vibrant, and energy-efficient displays in smartphones, tablets, and televisions is a significant growth catalyst. The trend towards larger screen sizes further amplifies this demand.

Competitive Dynamics: The competitive landscape is characterized by innovation and strategic alliances. Companies are investing heavily in R&D to develop proprietary LED materials and manufacturing processes. Strategic partnerships between material suppliers, LED chip manufacturers, and device integrators are becoming more common to accelerate product development and market penetration. The increasing adoption of LEDs in emerging markets, driven by government initiatives promoting energy conservation and infrastructure development, presents significant growth opportunities. The market penetration rate for LED lighting in developed economies has already surpassed 80%, indicating continued growth in replacement markets and new installations. The automotive sector is a particularly dynamic area, with the integration of LED technology in headlights, taillights, and interior lighting becoming standard, driven by safety regulations and design innovations.

Opportunities:

- Smart Lighting Integration: The burgeoning smart home market presents opportunities for LED materials that support advanced control and connectivity features.

- Horticultural Lighting: The increasing adoption of LED grow lights in agriculture due to their energy efficiency and spectral control offers a niche but growing market.

- Advanced Display Technologies: The continued evolution of Micro-LED and Mini-LED displays in televisions, monitors, and wearable devices will drive demand for high-performance LED materials.

- Solid-State Lighting (SSL) Advancements: Ongoing improvements in SSL technology will continue to displace traditional lighting in various applications, from industrial to architectural lighting.

- Emerging Market Penetration: Significant untapped potential exists in developing economies for LED adoption in general lighting and infrastructure projects.

Dominant Markets & Segments in LED Material Industry

The LED Material Industry is characterized by the dominance of specific regions and application segments, driven by a combination of robust demand, favorable governmental policies, and advanced technological infrastructure.

Leading Region: North America and Asia-Pacific are the dominant regions in the LED Material Industry.

- Asia-Pacific: This region, particularly China, South Korea, Taiwan, and Japan, leads due to its massive manufacturing base for consumer electronics and a significant presence of key LED material and chip manufacturers. Government initiatives promoting domestic manufacturing and technological advancement further bolster its dominance. For example, substantial investments in R&D and production capacity for Indium Gallide Nitride (InGaN) wafers and epitaxy have been a hallmark of the region's growth. The sheer volume of production for consumer electronics, where LEDs are integral, makes Asia-Pacific the primary hub.

- North America: The region demonstrates strong growth driven by innovation in high-end applications like automotive lighting, advanced display technologies, and a growing emphasis on energy-efficient general lighting solutions. Significant R&D spending by leading companies and supportive government policies for green technology contribute to its market share.

Dominant Segments:

Material: Indium Gallide Nitride (InGaN)

- Growth Drivers: InGaN is the cornerstone of blue and green LED production, essential for white light generation when combined with phosphors. Its superior efficiency and wavelength tunability make it indispensable for general lighting, consumer electronics displays (smartphones, TVs), and automotive lighting. The ongoing demand for higher brightness and energy efficiency in these applications directly fuels InGaN material growth. Projections indicate InGaN will account for over 60% of the total LED material market by 2028.

- Market Dominance: The segment is dominated by manufacturers capable of producing high-quality InGaN epitaxial wafers with precise composition control. The technological barrier to entry is high, contributing to the concentration of key players.

Application: Consumer Electronics

- Growth Drivers: This segment, encompassing smartphones, tablets, laptops, and televisions, is a perpetual engine for LED material demand. The continuous cycle of product upgrades and the increasing adoption of LED backlighting and direct-view LED displays (Mini-LED, Micro-LED) in premium devices are key drivers. For instance, the market for smartphone displays utilizing LED technology is estimated to reach over $30 billion by 2027.

- Market Dominance: The demand for high-resolution, energy-efficient displays with excellent color reproduction directly translates into a substantial need for advanced LED materials, particularly InGaN and specialized phosphors.

Type: Wafer

- Growth Drivers: LED wafers are the foundational component for LED chip manufacturing. The demand for high-quality, defect-free wafers is paramount for achieving efficient and reliable LED performance. Advancements in wafer preparation techniques and material purity are crucial for driving innovation in downstream applications. The global LED wafer market is expected to surpass $15 billion by 2030.

- Market Dominance: Companies with advanced MOCVD capabilities and expertise in substrate preparation (e.g., sapphire, silicon carbide) hold significant sway in this segment.

Application: General Lighting

- Growth Drivers: Driven by global energy conservation initiatives and the declining cost of LED technology, general lighting continues to be a massive market. The replacement of incandescent and fluorescent lamps with energy-efficient LEDs in residential, commercial, and industrial settings is a primary growth catalyst. Government subsidies and stringent energy efficiency standards further propel adoption. The global LED general lighting market is projected to exceed $70 billion by 2032.

- Market Dominance: This segment benefits from the broad applicability of InGaN-based white LEDs, requiring large-scale production and cost-effectiveness.

LED Material Industry Product Analysis

The LED Material Industry is characterized by continuous product innovation focused on enhancing luminous efficacy, color quality, and lifespan. Key product advancements revolve around optimizing the composition and structure of semiconductor materials like Indium Gallide Nitride (InGaN) and Aluminum Gallium Indium Phosphide (AlInGaP) to achieve specific wavelengths and higher brightness. Epitaxy techniques are constantly refined to produce defect-free layers, crucial for long-lasting and efficient LEDs. Innovations in phosphor materials and quantum dots are enabling broader color gamuts and improved color rendering, particularly for high-end display and lighting applications. The competitive advantage lies in the ability to deliver materials that meet stringent performance requirements for diverse applications, from energy-efficient general lighting and vibrant consumer electronics displays to advanced automotive lighting systems.

Key Drivers, Barriers & Challenges in LED Material Industry

Key Drivers:

- Energy Efficiency Mandates: Global governmental push for energy conservation and reduced carbon footprints through stringent regulations on lighting efficacy.

- Technological Advancements: Continuous improvements in LED chip design, material science (e.g., InGaN epitaxy), and manufacturing processes leading to higher performance and lower costs.

- Growing Demand in Emerging Markets: Rapid urbanization and infrastructure development in developing economies are driving significant adoption of LED lighting.

- Smart Lighting Integration: The increasing prevalence of smart homes and IoT devices creating demand for advanced, controllable LED solutions.

- Miniaturization and High-Density Displays: The growth of premium displays in consumer electronics, requiring advanced LED materials for Mini-LED and Micro-LED technologies.

Barriers & Challenges:

- High Initial Capital Investment: The significant cost associated with setting up advanced epitaxy and wafer manufacturing facilities.

- Supply Chain Disruptions: Vulnerability to disruptions in the supply of raw materials (e.g., gallium, indium) and components, impacting production volumes and costs.

- Intellectual Property (IP) Landscape: Complex patent portfolios and licensing agreements can create barriers to entry for new players.

- Raw Material Price Volatility: Fluctuations in the prices of critical raw materials can impact profitability and market competitiveness. For instance, the price of indium has seen an estimated increase of over 20% in the past two years.

- Competition from Alternative Lighting Technologies: While diminishing, competition from highly efficient fluorescent and newer solid-state technologies presents a continued challenge in some niche applications.

Growth Drivers in the LED Material Industry Market

The LED Material Industry is propelled by several key growth drivers. Technological innovation remains paramount, with ongoing advancements in epitaxy techniques for materials like Indium Gallide Nitride (InGaN) enabling higher luminous efficacy and improved color quality. This directly fuels demand in consumer electronics and general lighting. Governmental policies promoting energy efficiency and sustainability are significant drivers, incentivizing the adoption of LED solutions globally. For example, energy performance standards for lighting have been progressively tightened in major economies, creating a consistent demand pull. Furthermore, the automotive industry's increasing reliance on LED technology for both safety and aesthetic reasons, driven by electrification and autonomous driving trends, presents a substantial growth avenue.

Challenges Impacting LED Material Industry Growth

Despite robust growth prospects, the LED Material Industry faces several challenges. Supply chain vulnerabilities pose a significant risk, particularly concerning the availability and price volatility of critical raw materials like gallium and indium. Intensifying competition among established players and emerging manufacturers can lead to price pressures and reduced profit margins. Regulatory complexities related to environmental compliance and waste management in the manufacturing process can also add to operational costs and influence market access. The high capital expenditure required for advanced manufacturing facilities, such as MOCVD equipment, acts as a barrier for smaller companies looking to scale up.

Key Players Shaping the LED Material Industry Market

- EpiGaN

- EPISTAR Corporation

- Intematix Corporation

- Lumileds Holding BV

- My Sunlight

- NICHIA CORPORATION

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co Ltd

- Sumitomo Bakelite Co Ltd

- Wolfspeed A Cree Company

Significant LED Material Industry Industry Milestones

- 2019: Launch of enhanced InGaN epitaxy for higher blue light output efficiency by major players.

- 2020: Significant breakthroughs in Micro-LED display technology showcasing superior brightness and contrast ratios.

- 2021: Increased investment in Gallium Nitride (GaN) on Silicon (GaN-on-Si) wafer technology for cost reduction in LED manufacturing.

- 2022: Growing adoption of Mini-LED backlighting in premium televisions and monitors, driving demand for advanced LED materials.

- 2023: Advancements in quantum dot-enhanced LEDs leading to wider color gamuts and improved color accuracy.

- 2024: Strategic partnerships formed to secure raw material supply chains for critical elements like indium and gallium.

- 2025 (Estimated): Continued integration of AI in LED manufacturing for process optimization and yield improvement.

- 2026-2033 (Forecasted): Emerging trends include widespread adoption of Micro-LED displays in various consumer devices and increased use of specialized LEDs in horticultural applications.

Future Outlook for LED Material Industry Market

The future outlook for the LED Material Industry is exceptionally bright, driven by continuous technological innovation and expanding application horizons. Strategic opportunities lie in the burgeoning markets for advanced display technologies, such as Micro-LEDs and Mini-LEDs, which demand cutting-edge LED materials with unparalleled performance. The growing emphasis on smart lighting and IoT integration will further propel demand for LEDs that offer enhanced controllability and connectivity. Furthermore, the sustained global push for energy efficiency and sustainability, coupled with increasing adoption in emerging economies and specialized sectors like horticultural lighting, will ensure robust market growth throughout the forecast period. The market is expected to see continued investment in R&D for higher efficacy, better color quality, and cost-effective manufacturing processes, solidifying LEDs as the dominant lighting and display technology.

LED Material Industry Segmentation

-

1. Type

- 1.1. Wafer

- 1.2. Substrate

- 1.3. Epitaxy

- 1.4. Others

-

2. Material

- 2.1. Indium Gallide Nitrile

- 2.2. Aluminum Gallium Indium Phosphide

- 2.3. Aluminum Gallium Arsenide

- 2.4. Gallium Phosphide

- 2.5. Others

-

3. Application

- 3.1. Consumer Electronics

- 3.2. General Lighting

- 3.3. Automotive Lighting

- 3.4. Backlighting

- 3.5. Others

LED Material Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

LED Material Industry Regional Market Share

Geographic Coverage of LED Material Industry

LED Material Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Wafer

- 5.1.2. Substrate

- 5.1.3. Epitaxy

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Indium Gallide Nitrile

- 5.2.2. Aluminum Gallium Indium Phosphide

- 5.2.3. Aluminum Gallium Arsenide

- 5.2.4. Gallium Phosphide

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Consumer Electronics

- 5.3.2. General Lighting

- 5.3.3. Automotive Lighting

- 5.3.4. Backlighting

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global LED Material Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Wafer

- 6.1.2. Substrate

- 6.1.3. Epitaxy

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Indium Gallide Nitrile

- 6.2.2. Aluminum Gallium Indium Phosphide

- 6.2.3. Aluminum Gallium Arsenide

- 6.2.4. Gallium Phosphide

- 6.2.5. Others

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Consumer Electronics

- 6.3.2. General Lighting

- 6.3.3. Automotive Lighting

- 6.3.4. Backlighting

- 6.3.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific LED Material Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Wafer

- 7.1.2. Substrate

- 7.1.3. Epitaxy

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Material

- 7.2.1. Indium Gallide Nitrile

- 7.2.2. Aluminum Gallium Indium Phosphide

- 7.2.3. Aluminum Gallium Arsenide

- 7.2.4. Gallium Phosphide

- 7.2.5. Others

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Consumer Electronics

- 7.3.2. General Lighting

- 7.3.3. Automotive Lighting

- 7.3.4. Backlighting

- 7.3.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America LED Material Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Wafer

- 8.1.2. Substrate

- 8.1.3. Epitaxy

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Material

- 8.2.1. Indium Gallide Nitrile

- 8.2.2. Aluminum Gallium Indium Phosphide

- 8.2.3. Aluminum Gallium Arsenide

- 8.2.4. Gallium Phosphide

- 8.2.5. Others

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Consumer Electronics

- 8.3.2. General Lighting

- 8.3.3. Automotive Lighting

- 8.3.4. Backlighting

- 8.3.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe LED Material Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Wafer

- 9.1.2. Substrate

- 9.1.3. Epitaxy

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Material

- 9.2.1. Indium Gallide Nitrile

- 9.2.2. Aluminum Gallium Indium Phosphide

- 9.2.3. Aluminum Gallium Arsenide

- 9.2.4. Gallium Phosphide

- 9.2.5. Others

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Consumer Electronics

- 9.3.2. General Lighting

- 9.3.3. Automotive Lighting

- 9.3.4. Backlighting

- 9.3.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America LED Material Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Wafer

- 10.1.2. Substrate

- 10.1.3. Epitaxy

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Material

- 10.2.1. Indium Gallide Nitrile

- 10.2.2. Aluminum Gallium Indium Phosphide

- 10.2.3. Aluminum Gallium Arsenide

- 10.2.4. Gallium Phosphide

- 10.2.5. Others

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Consumer Electronics

- 10.3.2. General Lighting

- 10.3.3. Automotive Lighting

- 10.3.4. Backlighting

- 10.3.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa LED Material Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Wafer

- 11.1.2. Substrate

- 11.1.3. Epitaxy

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Material

- 11.2.1. Indium Gallide Nitrile

- 11.2.2. Aluminum Gallium Indium Phosphide

- 11.2.3. Aluminum Gallium Arsenide

- 11.2.4. Gallium Phosphide

- 11.2.5. Others

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Consumer Electronics

- 11.3.2. General Lighting

- 11.3.3. Automotive Lighting

- 11.3.4. Backlighting

- 11.3.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 EpiGaN

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 EPISTAR Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Intematix Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lumileds Holding BV

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 My Sunlight

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NICHIA CORPORATION

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 OSRAM Opto Semiconductors GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Seoul Semiconductor Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sumitomo Bakelite Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Wolfspeed A Cree Company*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 EpiGaN

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global LED Material Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific LED Material Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: Asia Pacific LED Material Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific LED Material Industry Revenue (billion), by Material 2025 & 2033

- Figure 5: Asia Pacific LED Material Industry Revenue Share (%), by Material 2025 & 2033

- Figure 6: Asia Pacific LED Material Industry Revenue (billion), by Application 2025 & 2033

- Figure 7: Asia Pacific LED Material Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Asia Pacific LED Material Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Asia Pacific LED Material Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America LED Material Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: North America LED Material Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: North America LED Material Industry Revenue (billion), by Material 2025 & 2033

- Figure 13: North America LED Material Industry Revenue Share (%), by Material 2025 & 2033

- Figure 14: North America LED Material Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: North America LED Material Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: North America LED Material Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: North America LED Material Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe LED Material Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Europe LED Material Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Europe LED Material Industry Revenue (billion), by Material 2025 & 2033

- Figure 21: Europe LED Material Industry Revenue Share (%), by Material 2025 & 2033

- Figure 22: Europe LED Material Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Europe LED Material Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Europe LED Material Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Europe LED Material Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America LED Material Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: South America LED Material Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: South America LED Material Industry Revenue (billion), by Material 2025 & 2033

- Figure 29: South America LED Material Industry Revenue Share (%), by Material 2025 & 2033

- Figure 30: South America LED Material Industry Revenue (billion), by Application 2025 & 2033

- Figure 31: South America LED Material Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: South America LED Material Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: South America LED Material Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa LED Material Industry Revenue (billion), by Type 2025 & 2033

- Figure 35: Middle East and Africa LED Material Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: Middle East and Africa LED Material Industry Revenue (billion), by Material 2025 & 2033

- Figure 37: Middle East and Africa LED Material Industry Revenue Share (%), by Material 2025 & 2033

- Figure 38: Middle East and Africa LED Material Industry Revenue (billion), by Application 2025 & 2033

- Figure 39: Middle East and Africa LED Material Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa LED Material Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa LED Material Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 3: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global LED Material Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 7: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global LED Material Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: China LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: India LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Japan LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: South Korea LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 15: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 16: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global LED Material Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: United States LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Canada LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Mexico LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 23: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Global LED Material Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: Germany LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: United Kingdom LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: France LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Italy LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 31: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 32: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global LED Material Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Brazil LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Argentina LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global LED Material Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global LED Material Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 39: Global LED Material Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 40: Global LED Material Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Saudi Arabia LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: South Africa LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa LED Material Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LED Material Industry?

The projected CAGR is approximately 10.3%.

2. Which companies are prominent players in the LED Material Industry?

Key companies in the market include EpiGaN, EPISTAR Corporation, Intematix Corporation, Lumileds Holding BV, My Sunlight, NICHIA CORPORATION, OSRAM Opto Semiconductors GmbH, Seoul Semiconductor Co Ltd, Sumitomo Bakelite Co Ltd, Wolfspeed A Cree Company*List Not Exhaustive.

3. What are the main segments of the LED Material Industry?

The market segments include Type, Material, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.89 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand from Residential and Commercial Application; Rising Demand from Energy Efficient Lighting.

6. What are the notable trends driving market growth?

General Lighting Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

; Growing Demand from Residential and Commercial Application; Rising Demand from Energy Efficient Lighting.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LED Material Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LED Material Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LED Material Industry?

To stay informed about further developments, trends, and reports in the LED Material Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence