Key Insights

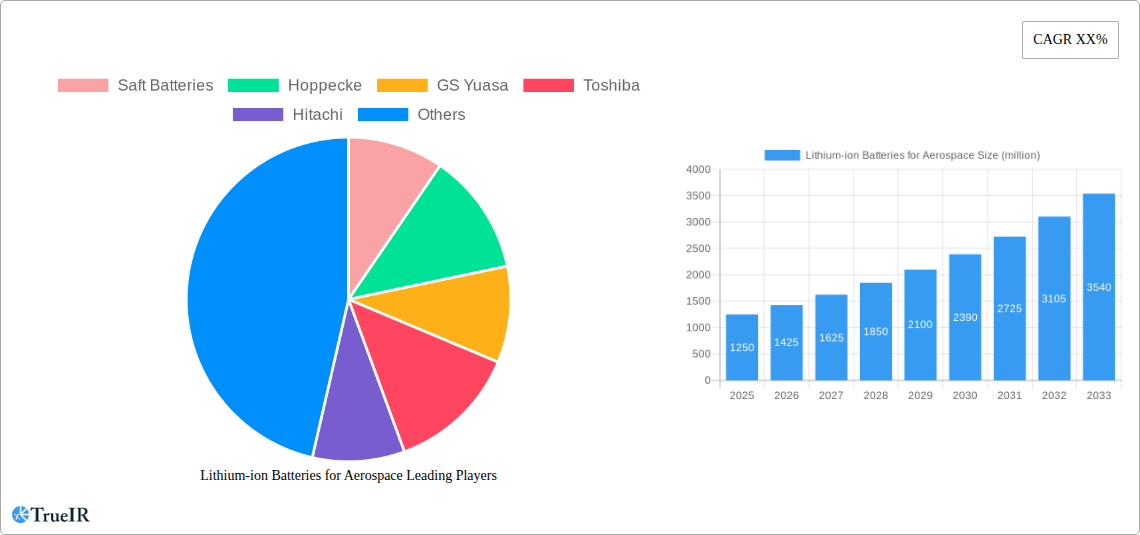

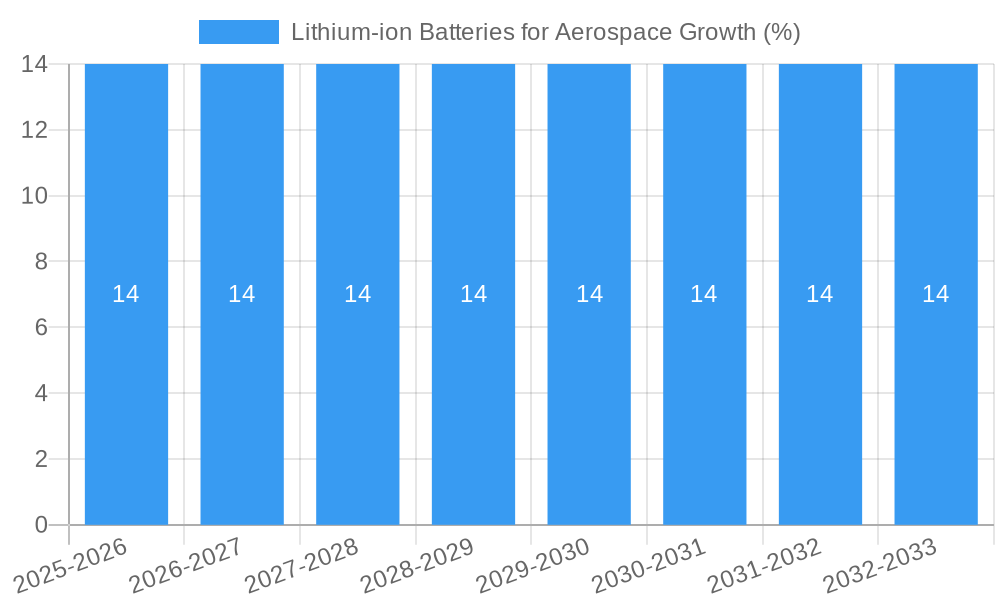

The global Lithium-ion Batteries for Aerospace market is poised for significant expansion, projected to reach an estimated market size of $1,250 million by 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 14% through 2033. This upward trajectory is primarily fueled by the increasing demand for advanced battery solutions in commercial aviation, driven by the need for lighter, more efficient, and powerful energy storage systems to support enhanced payload capacity and extended flight ranges. General aviation is also witnessing a surge in adoption, with a growing interest in electric and hybrid-electric aircraft, pushing the boundaries of sustainable flight. Military aviation, a historically significant segment, continues to drive innovation through the requirement for reliable and high-performance batteries in drones, electronic warfare systems, and other critical defense applications. The market is also benefiting from the continuous technological advancements in battery chemistry, particularly in the development of LFP (Lithium Iron Phosphate) and Li-NMC (Lithium Nickel Manganese Cobalt) battery technologies, offering improved safety, energy density, and lifecycle.

The market's growth is further propelled by several key drivers. The increasing focus on reducing aviation's environmental impact and achieving net-zero emissions is a major catalyst for the adoption of electric and hybrid-electric propulsion systems, which heavily rely on advanced lithium-ion battery technology. Technological innovation, leading to higher energy density and longer operational lifespans, directly addresses the performance demands of the aerospace sector. Furthermore, government initiatives and investments supporting the development of sustainable aviation technologies are creating a favorable market landscape. However, the market faces certain restraints, including the high initial cost of advanced battery systems and stringent regulatory approvals required for aviation applications, which can slow down the adoption rate. Despite these challenges, the persistent drive for innovation and the undeniable benefits of lithium-ion batteries in enhancing aircraft performance and sustainability are expected to ensure sustained market growth.

Lithium-ion Batteries for Aerospace: Market Analysis and Forecast (2019-2033)

This comprehensive report delves into the dynamic global market for Lithium-ion Batteries in Aerospace. Leveraging extensive primary and secondary research, this analysis provides deep insights into market structure, key trends, dominant segments, product innovations, and the competitive landscape. The report is meticulously crafted for aerospace manufacturers, battery suppliers, investors, and policymakers seeking to understand and capitalize on the evolving opportunities within this critical sector.

Lithium-ion Batteries for Aerospace Market Structure & Competitive Landscape

The Lithium-ion Batteries for Aerospace market exhibits a moderately concentrated structure, with a few key players accounting for a significant share of the market. Innovation drivers are primarily fueled by the relentless demand for higher energy density, improved safety standards, and longer cycle life to meet the stringent requirements of aerospace applications. Regulatory impacts from aviation authorities worldwide, such as the FAA and EASA, play a crucial role in dictating battery design, testing, and certification, influencing market entry and product development. The threat of product substitutes, while currently limited, is a consideration, with ongoing research into alternative battery chemistries. End-user segmentation is clearly defined by Commercial Aviation, General Aviation, and Military Aviation, each with distinct operational demands and procurement cycles. Mergers and acquisitions (M&A) trends are observed as larger, established battery manufacturers seek to expand their aerospace capabilities and smaller, innovative firms aim for scalability and market access. In 2023, approximately 15-20% of aerospace battery market transactions were M&A related, demonstrating active consolidation.

Lithium-ion Batteries for Aerospace Market Trends & Opportunities

The global Lithium-ion Batteries for Aerospace market is poised for significant expansion, projected to reach an estimated $5,000 million by 2025 and further grow to $9,500 million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period (2025–2033). This growth is underpinned by several transformative trends and emerging opportunities.

A pivotal trend is the increasing adoption of electric and hybrid-electric propulsion systems in both commercial and general aviation. As aircraft manufacturers push the boundaries of sustainable aviation, the demand for lightweight, high-performance lithium-ion batteries intensifies. This includes advancements in battery management systems (BMS) for enhanced safety and operational efficiency, as well as the development of advanced thermal management solutions to ensure reliable performance across extreme operating temperatures encountered during flight.

Technological shifts are primarily focused on improving energy density and specific energy, allowing for longer flight ranges and increased payload capacities. Innovations in cell chemistries, such as solid-state batteries and advanced Li-NMC variations, are gaining traction, promising higher safety margins and faster charging capabilities. The market penetration rate for these advanced chemistries in new aircraft designs is expected to rise from approximately 15% in 2025 to over 35% by 2033.

Consumer preferences, driven by the airline industry's focus on operational cost reduction and environmental sustainability, are steering towards battery solutions that offer lower total cost of ownership and reduced emissions. This translates to a demand for batteries with extended lifecycles, higher reliability, and reduced maintenance requirements. The market penetration for LFP (Lithium Iron Phosphate) batteries, known for their inherent safety and long cycle life, is also increasing, particularly for auxiliary power units and less demanding applications.

Competitive dynamics are intensifying, with established players investing heavily in research and development while new entrants vie for market share with specialized solutions. Strategic partnerships between battery manufacturers, aircraft OEMs, and research institutions are becoming crucial for accelerating innovation and navigating the complex certification processes. The pursuit of lighter, more powerful, and safer battery solutions will continue to define the competitive landscape, with opportunities arising in custom battery pack design, specialized charging infrastructure, and end-of-life battery management.

Dominant Markets & Segments in Lithium-ion Batteries for Aerospace

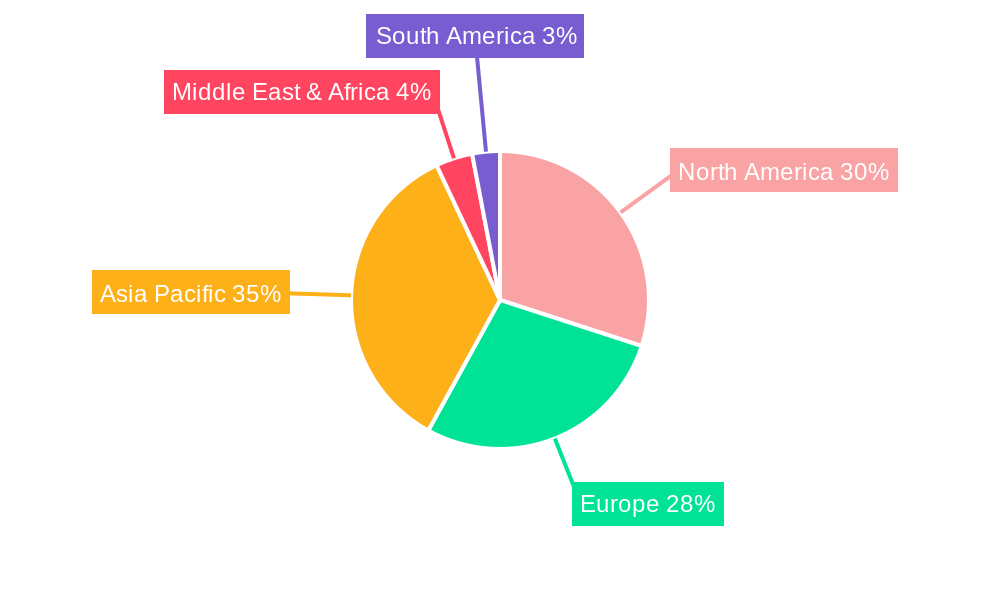

The Commercial Aviation segment is the leading market for Lithium-ion Batteries in Aerospace, driven by the sheer volume of aircraft production and the increasing integration of advanced battery technologies for auxiliary power, cabin systems, and emerging electric/hybrid propulsion initiatives. The United States and Europe currently represent the dominant regional markets, owing to the presence of major aircraft manufacturers and robust regulatory frameworks supporting technological advancement.

Within the Application segmentation:

- Commercial Aviation: This segment's dominance is fueled by the demand for lighter, more energy-dense batteries to improve fuel efficiency and enable new aircraft designs, including single-aisle aircraft and regional jets with hybrid-electric capabilities. The installed battery capacity in this segment is expected to grow by over 50% from 2025 to 2033. Key growth drivers include airline fleet modernization programs and the push for reduced operational costs.

- Military Aviation: This segment, while smaller in volume, represents a high-value market. The need for reliable power for critical systems, electronic warfare, and unmanned aerial vehicles (UAVs) drives demand. Military applications often require batteries with superior endurance, extreme temperature tolerance, and enhanced security features, contributing to their higher per-unit value. Government defense spending and the increasing use of drones for surveillance and logistics are key growth factors.

- General Aviation: This segment, encompassing smaller aircraft and private jets, is experiencing a growing interest in battery-powered solutions for lighter aircraft and as backup power sources. Regulatory changes supporting smaller electric aircraft and the increasing affordability of advanced battery technologies are contributing to its growth.

Within the Types segmentation:

- Li-NMC Battery (Lithium Nickel Manganese Cobalt Oxide): This type currently dominates due to its high energy density and power output, making it ideal for applications where weight and performance are paramount. Its market share is projected to remain strong, accounting for approximately 60% of the market by 2025, with further innovation enhancing its safety profiles.

- LFP Battery (Lithium Iron Phosphate): While historically less prevalent due to lower energy density, LFP batteries are experiencing a resurgence and projected significant growth, especially for applications where safety and long cycle life are prioritized over ultimate energy density. Their inherent thermal stability and reduced risk of thermal runaway make them increasingly attractive for auxiliary power and specific military applications. Their market share is expected to grow from approximately 25% in 2025 to over 40% by 2033.

- Others: This category includes emerging chemistries and next-generation battery technologies like solid-state batteries. While currently a smaller segment, it holds immense potential for future disruption as technological advancements mature and production scales. The market share for "Others" is projected to increase from around 15% in 2025 to 25% by 2033, driven by breakthroughs in research and development.

Lithium-ion Batteries for Aerospace Product Analysis

Lithium-ion batteries for aerospace are characterized by continuous product innovation focused on enhancing energy density, improving safety mechanisms, and extending operational lifecycles. Key applications range from primary power sources for electric and hybrid-electric aircraft to critical backup power systems, avionics, and specialized military equipment. Manufacturers like Saft Batteries and Kokam are at the forefront of developing custom battery packs that integrate advanced thermal management and sophisticated Battery Management Systems (BMS) to ensure peak performance and reliability across extreme environmental conditions. The competitive advantage lies in achieving superior specific energy (Wh/kg) and volumetric energy density (Wh/L) while adhering to stringent aviation safety certifications, offering a compelling blend of reduced weight, extended flight range, and enhanced system redundancy.

Key Drivers, Barriers & Challenges in Lithium-ion Batteries for Aerospace

Key Drivers: The primary forces propelling the Lithium-ion Batteries for Aerospace market are the global push for sustainable aviation and the electrification of aircraft. Technological advancements leading to higher energy density and improved safety features are critical enablers. Government initiatives and regulatory support for green aviation are also significant drivers. For example, the European Union's "Green Deal" aims to reduce aviation emissions, directly impacting battery demand. Economic drivers include the pursuit of lower operating costs for airlines through improved fuel efficiency and reduced maintenance.

Barriers & Challenges: Key challenges impacting growth include stringent and complex regulatory certification processes for aerospace batteries, which can significantly prolong time-to-market. Supply chain vulnerabilities, particularly for critical raw materials like lithium and cobalt, pose a risk, potentially leading to price volatility and production delays. The high initial investment cost for developing and manufacturing aerospace-grade lithium-ion batteries remains a barrier. Furthermore, managing the thermal runaway risk in highly demanding aviation environments requires continuous innovation and robust safety protocols, with incidents, though rare, having significant implications. The competition from established battery technologies and the need for extensive ground testing and validation add to the complexity.

Growth Drivers in the Lithium-ion Batteries for Aerospace Market

The growth of the Lithium-ion Batteries for Aerospace market is fundamentally driven by the accelerating transition towards electrification and hybrid-electric propulsion systems in all segments of aviation. This is further amplified by the increasing demand for enhanced aircraft performance, specifically in terms of longer flight ranges and higher payload capacities, which directly benefits from the superior energy density offered by advanced lithium-ion chemistries. Government mandates and incentives promoting sustainable aviation and reduced carbon emissions, alongside airline industry efforts to optimize operational costs and improve fuel efficiency, are crucial economic and policy-driven factors. Continuous technological advancements in battery chemistry, thermal management, and Battery Management Systems (BMS) are making lithium-ion solutions increasingly viable and reliable for the demanding aerospace environment.

Challenges Impacting Lithium-ion Batteries for Aerospace Growth

The primary challenges impacting the growth of the Lithium-ion Batteries for Aerospace market revolve around the rigorous and time-consuming regulatory certification processes mandated by aviation authorities worldwide. These stringent safety and performance requirements necessitate extensive testing and validation, significantly increasing development timelines and costs. Supply chain complexities and the potential for raw material price volatility for key components like lithium, nickel, and cobalt also present significant risks, potentially impacting production schedules and overall cost-effectiveness. Furthermore, inherent safety concerns associated with lithium-ion technology, particularly the risk of thermal runaway under extreme operating conditions, require continuous innovation and robust fail-safe mechanisms to ensure passenger and crew safety, leading to higher manufacturing and material costs. Competitive pressures from established battery technologies and the need for substantial capital investment in specialized manufacturing facilities also act as barriers.

Key Players Shaping the Lithium-ion Batteries for Aerospace Market

- Saft Batteries

- Hoppecke

- GS Yuasa

- Toshiba

- Hitachi

- Leclanché

- AKASOL AG

- Kokam

Significant Lithium-ion Batteries for Aerospace Industry Milestones

- 2019: Saft Batteries introduces its advanced aviation battery solutions, emphasizing safety and performance for commercial aircraft.

- 2020: GS Yuasa announces significant advancements in its high-energy density lithium-ion cells for aviation applications.

- 2021: Kokam partners with an aerospace OEM for the development of a novel battery system for a next-generation electric aircraft prototype.

- 2022: The EASA approves new battery certification standards, influencing the design and testing requirements for lithium-ion batteries in commercial aviation.

- 2022: Hoppecke expands its aerospace battery portfolio, focusing on improved thermal management for enhanced reliability.

- 2023: AKASOL AG showcases its high-power battery systems designed for hybrid-electric aircraft demonstrator programs.

- 2023: Leclanché announces breakthroughs in LFP battery technology for increased safety and cycle life in aviation.

- 2024: Toshiba unveils its new generation of lithium-ion battery technology with a focus on higher energy density and extended lifespan for aerospace.

Future Outlook for Lithium-ion Batteries for Aerospace Market

The future outlook for the Lithium-ion Batteries for Aerospace market is exceptionally promising, driven by the unwavering global commitment to sustainable aviation and the rapid advancement of electric and hybrid-electric aircraft technologies. Strategic opportunities lie in the development of next-generation battery chemistries, such as solid-state batteries, which promise enhanced safety, higher energy density, and faster charging capabilities, potentially revolutionizing aircraft design and performance. Increased investment in advanced Battery Management Systems (BMS) and sophisticated thermal management solutions will be critical for ensuring operational reliability and safety. Furthermore, the establishment of robust recycling and end-of-life management frameworks for aerospace batteries will be crucial for sustainability and resource efficiency. The market is poised for sustained growth, with significant potential for innovation and market expansion as aircraft manufacturers increasingly integrate these advanced power solutions.

Lithium-ion Batteries for Aerospace Segmentation

-

1. Application

- 1.1. Commercial Aviation

- 1.2. General Aviation

- 1.3. Military Aviation

-

2. Types

- 2.1. LFP Battery

- 2.2. Li-NMC Battery

- 2.3. Others

Lithium-ion Batteries for Aerospace Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Lithium-ion Batteries for Aerospace REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Aviation

- 5.1.2. General Aviation

- 5.1.3. Military Aviation

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. LFP Battery

- 5.2.2. Li-NMC Battery

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Aviation

- 6.1.2. General Aviation

- 6.1.3. Military Aviation

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. LFP Battery

- 6.2.2. Li-NMC Battery

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Aviation

- 7.1.2. General Aviation

- 7.1.3. Military Aviation

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. LFP Battery

- 7.2.2. Li-NMC Battery

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Aviation

- 8.1.2. General Aviation

- 8.1.3. Military Aviation

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. LFP Battery

- 8.2.2. Li-NMC Battery

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Aviation

- 9.1.2. General Aviation

- 9.1.3. Military Aviation

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. LFP Battery

- 9.2.2. Li-NMC Battery

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Lithium-ion Batteries for Aerospace Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Aviation

- 10.1.2. General Aviation

- 10.1.3. Military Aviation

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. LFP Battery

- 10.2.2. Li-NMC Battery

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Saft Batteries

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Hoppecke

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GS Yuasa

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Toshiba

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hitachi

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Leclanché

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AKASOL AG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kokam

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Saft Batteries

List of Figures

- Figure 1: Global Lithium-ion Batteries for Aerospace Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Lithium-ion Batteries for Aerospace Revenue (million), by Application 2024 & 2032

- Figure 3: North America Lithium-ion Batteries for Aerospace Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Lithium-ion Batteries for Aerospace Revenue (million), by Types 2024 & 2032

- Figure 5: North America Lithium-ion Batteries for Aerospace Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Lithium-ion Batteries for Aerospace Revenue (million), by Country 2024 & 2032

- Figure 7: North America Lithium-ion Batteries for Aerospace Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Lithium-ion Batteries for Aerospace Revenue (million), by Application 2024 & 2032

- Figure 9: South America Lithium-ion Batteries for Aerospace Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Lithium-ion Batteries for Aerospace Revenue (million), by Types 2024 & 2032

- Figure 11: South America Lithium-ion Batteries for Aerospace Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Lithium-ion Batteries for Aerospace Revenue (million), by Country 2024 & 2032

- Figure 13: South America Lithium-ion Batteries for Aerospace Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Lithium-ion Batteries for Aerospace Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Lithium-ion Batteries for Aerospace Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Lithium-ion Batteries for Aerospace Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Lithium-ion Batteries for Aerospace Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Lithium-ion Batteries for Aerospace Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Lithium-ion Batteries for Aerospace Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Lithium-ion Batteries for Aerospace Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Lithium-ion Batteries for Aerospace Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Lithium-ion Batteries for Aerospace Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Lithium-ion Batteries for Aerospace Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Lithium-ion Batteries for Aerospace Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Lithium-ion Batteries for Aerospace Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Lithium-ion Batteries for Aerospace Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Lithium-ion Batteries for Aerospace Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Lithium-ion Batteries for Aerospace Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lithium-ion Batteries for Aerospace?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Lithium-ion Batteries for Aerospace?

Key companies in the market include Saft Batteries, Hoppecke, GS Yuasa, Toshiba, Hitachi, Leclanché, AKASOL AG, Kokam.

3. What are the main segments of the Lithium-ion Batteries for Aerospace?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lithium-ion Batteries for Aerospace," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lithium-ion Batteries for Aerospace report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lithium-ion Batteries for Aerospace?

To stay informed about further developments, trends, and reports in the Lithium-ion Batteries for Aerospace, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence