Key Insights

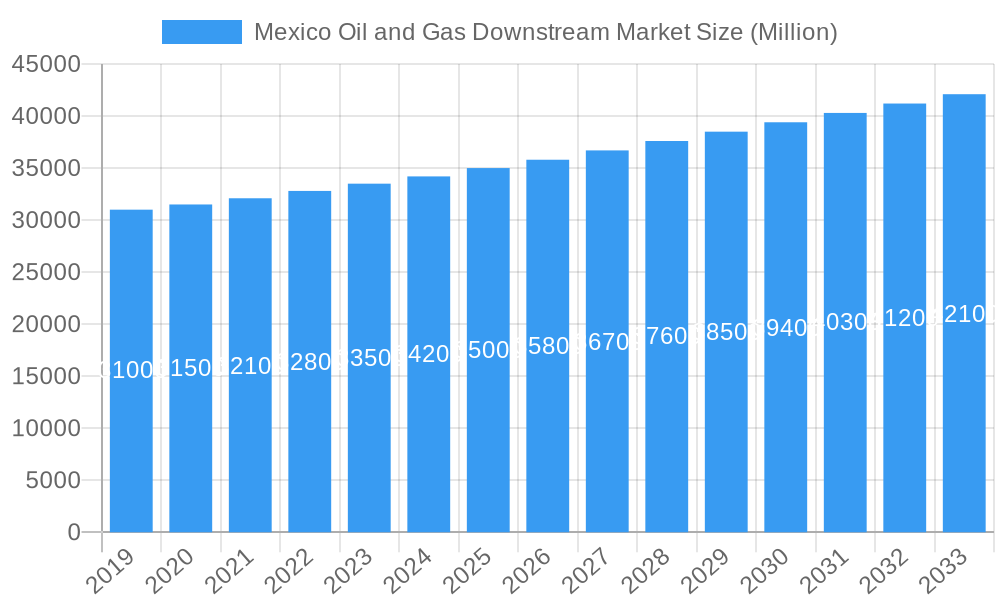

The Mexico Oil and Gas Downstream Market is projected for robust expansion, expected to reach $1.21 billion by 2025, driven by a Compound Annual Growth Rate (CAGR) of 2.35% through 2033. This growth is propelled by escalating demand in the petrochemical sector, supported by Mexico's expanding manufacturing output and rising consumer consumption of essential goods. Strategic investments in refinery modernization for enhanced efficiency and yield, alongside the development of new petrochemical facilities, are key growth catalysts. Government initiatives prioritizing energy security and domestic value addition further bolster the sector. The downstream segment encompasses significant operations within Refineries and Petrochemicals Plants, integral to the industry's value chain.

Mexico Oil and Gas Downstream Market Market Size (In Billion)

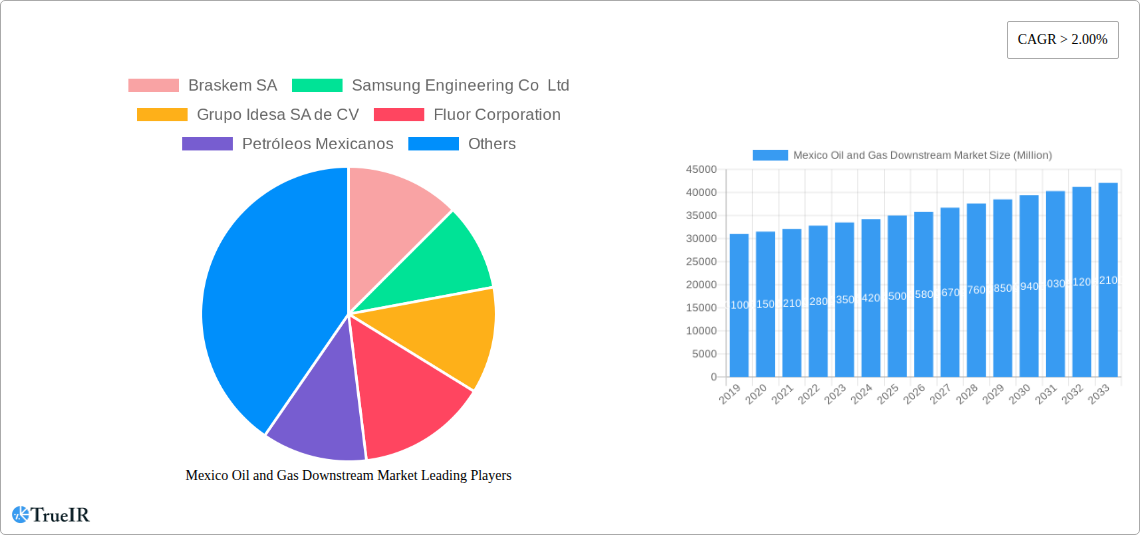

Key market restraints include the substantial capital expenditure required for modernizing aging refinery infrastructure and evolving environmental regulations impacting the transition to cleaner energy sources. Crude oil price volatility presents a challenge to profitability and investment decisions. Despite these, significant investments from industry leaders such as Braskem SA, Samsung Engineering Co Ltd, Grupo Idesa SA de CV, Fluor Corporation, and Petróleos Mexicanos, coupled with consistent demand for refined fuels and petrochemicals, highlight the market's resilience and economic importance. Future strategies will focus on operational optimization, technological adoption, and product portfolio diversification.

Mexico Oil and Gas Downstream Market Company Market Share

This comprehensive report provides a dynamic, SEO-optimized analysis of the Mexico Oil and Gas Downstream Market, utilizing high-volume keywords to improve search visibility and deliver actionable intelligence. Covering the forecast period from 2019 to 2033, with a base year of 2025, the report details market dynamics, trends, dominant segments, product insights, growth drivers, challenges, and future projections.

Mexico Oil and Gas Downstream Market Market Structure & Competitive Landscape

The Mexico Oil and Gas Downstream Market exhibits a moderate to high concentration, with Petróleos Mexicanos (Pemex) holding a significant market share, particularly in refining operations. The competitive landscape is characterized by the presence of both national and international players, including Braskem SA, Samsung Engineering Co Ltd, Grupo Idesa SA de CV, and Fluor Corporation, who are actively involved in infrastructure development, petrochemical production, and technological advancements. Innovation drivers are primarily focused on enhancing operational efficiency, reducing environmental impact through the adoption of cleaner technologies, and meeting the growing demand for refined products and petrochemicals. Regulatory impacts are substantial, with government policies influencing investment decisions, environmental standards, and market access. Product substitutes for traditional fuels are emerging, driven by the global shift towards renewable energy sources, although their penetration remains limited in the current market. End-user segmentation spans the transportation, manufacturing, and chemical industries. Merger and acquisition (M&A) trends are observed as companies seek to expand their operational footprint, acquire technological expertise, and consolidate their market positions. The overall M&A volume is projected to grow as strategic partnerships and consolidations become more prevalent to navigate market complexities and capitalize on emerging opportunities.

Mexico Oil and Gas Downstream Market Market Trends & Opportunities

The Mexico Oil and Gas Downstream Market is poised for robust growth, driven by increasing domestic demand for refined petroleum products and petrochemicals, coupled with strategic investments in infrastructure modernization and expansion. The market size is projected to expand significantly from an estimated USD 150 Billion in 2025 to over USD 200 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 3.5% during the forecast period. Technological shifts are a key trend, with a growing emphasis on upgrading existing refinery capabilities and constructing new, more efficient facilities. The adoption of advanced refining technologies, such as catalytic cracking and hydrocracking, is becoming crucial to produce higher-value products and meet stringent environmental regulations. Consumer preferences are evolving, with a rising demand for cleaner fuels, including ultra-low-sulfur diesel and Euro V compliant gasoline, to mitigate air pollution. This trend is creating opportunities for companies that can invest in and deploy advanced refining processes. Competitive dynamics are intensifying, with both established players and new entrants vying for market share. Opportunities abound in the development of integrated refining and petrochemical complexes, the expansion of storage and distribution networks, and the production of specialty chemicals and high-performance polymers. The increasing focus on energy security and self-sufficiency within Mexico further bolsters the demand for domestic downstream operations. Furthermore, the burgeoning manufacturing sector and the automotive industry's growing needs for a consistent supply of refined products and petrochemicals present significant market penetration opportunities. The government's focus on bolstering energy independence and revitalizing the state-owned oil company, Pemex, is a pivotal factor driving investment and development in this sector.

Dominant Markets & Segments in Mexico Oil and Gas Downstream Market

Within the Mexico Oil and Gas Downstream Market, the Refineries segment holds a dominant position, driven by the foundational role of crude oil processing in supplying a wide array of derived products. The Petrochemicals Plants segment is experiencing rapid growth, fueled by the increasing demand from downstream manufacturing industries such as plastics, textiles, and automotive components.

Refineries:

The refining segment's dominance is underpinned by several key growth drivers:

- Infrastructure Modernization and Expansion: Significant investments are being channeled into upgrading existing refineries and constructing new ones to enhance processing capacity, improve efficiency, and meet evolving product quality standards. The recent announcement regarding Pemex's Olmeca refinery, with an installed capacity of 340,000 barrels per day (BPD), slated to produce 170,000 barrels of petrol and 120,000 barrels of ultra-low-sulfur diesel, exemplifies this strategic expansion. This initiative aims to bolster Mexico's refining capabilities and reduce reliance on imported refined products, thereby consolidating energy security.

- Government Policies and Strategic Importance: The Mexican government's commitment to strengthening its domestic refining sector is a crucial policy-driven factor. The emphasis on achieving energy self-sufficiency and optimizing the utilization of national crude oil reserves directly fuels investment and operational focus within this segment.

- Demand for Transportation Fuels: The continued demand for gasoline and diesel for transportation purposes remains a primary revenue stream for the refining segment. Despite the global push towards electric vehicles, internal combustion engines will continue to be a significant part of the energy mix for the foreseeable future.

Petrochemicals Plants:

The petrochemicals segment, while currently smaller than refining, is exhibiting a higher growth trajectory:

- Growing Industrial Demand: Mexico's expanding manufacturing base, particularly in the automotive, construction, and packaging sectors, is creating a substantial and growing demand for petrochemical derivatives like plastics, resins, and synthetic fibers.

- Value Addition and Diversification: Petrochemical production allows for greater value addition to crude oil and natural gas feedstock. Companies are investing in diversifying their product portfolios to include higher-margin specialty chemicals.

- Technological Advancements and Foreign Investment: Companies like Braskem SA and Grupo Idesa SA de CV are instrumental in driving innovation and expanding production capacities within the petrochemical sector. Their investments in advanced technologies and new plant constructions are critical for meeting the escalating demand.

- Integration Opportunities: The integration of petrochemical plants with refining operations offers significant synergies, enabling efficient feedstock utilization and cost optimization, further enhancing the attractiveness of this segment.

The interplay between these segments, supported by strategic investments and favorable government policies, will shape the overall growth and competitive dynamics of the Mexico Oil and Gas Downstream Market.

Mexico Oil and Gas Downstream Market Product Analysis

The Mexico Oil and Gas Downstream Market is characterized by a diverse product portfolio catering to a wide range of industrial and consumer needs. Key products include various grades of gasoline, diesel fuel (including ultra-low-sulfur diesel), jet fuel, and fuel oil for the transportation and energy sectors. In the petrochemical realm, the market produces essential building blocks such as ethylene, propylene, benzene, and their derivatives, which are critical for the manufacturing of plastics, resins, synthetic fibers, and other industrial chemicals. Technological advancements are enabling the production of higher-purity chemicals and specialized polymers with enhanced performance characteristics. Competitive advantages are being forged through efficient refining processes, innovative catalyst technologies, and the development of integrated value chains that optimize feedstock utilization and product differentiation.

Key Drivers, Barriers & Challenges in Mexico Oil and Gas Downstream Market

Key Drivers:

- Growing Demand for Refined Products: Increasing domestic consumption of gasoline, diesel, and other fuels for transportation and industrial use remains a primary growth catalyst.

- Petrochemical Industry Expansion: The rising demand from manufacturing sectors for plastics, resins, and other chemical intermediates is spurring significant investment in petrochemical facilities.

- Government Support and Investment: The Mexican government's focus on energy security and revitalization of the national oil company, Pemex, is driving substantial investment in downstream infrastructure.

- Technological Advancements: Adoption of modern refining and petrochemical technologies enhances efficiency, product quality, and environmental compliance.

Barriers & Challenges:

- Infrastructure Deficiencies: Aging infrastructure in some refining facilities and logistical bottlenecks in product distribution can hinder operational efficiency.

- Regulatory Complexities: Navigating evolving environmental regulations and obtaining permits can be time-consuming and costly.

- Competition from Imports: While domestic production is growing, competition from imported refined products and petrochemicals can impact market dynamics.

- Volatile Crude Oil Prices: Fluctuations in global crude oil prices can affect profitability and investment decisions in the downstream sector. The supply chain issues stemming from global events also pose significant challenges, impacting the availability and cost of essential materials and equipment.

Growth Drivers in the Mexico Oil and Gas Downstream Market Market

The Mexico Oil and Gas Downstream Market is propelled by a confluence of technological, economic, and regulatory factors. Technologically, the ongoing adoption of advanced refining processes and the modernization of existing facilities are enhancing operational efficiency and enabling the production of higher-value products. Economically, the burgeoning domestic demand for transportation fuels and petrochemical derivatives, driven by Mexico's growing industrial and manufacturing sectors, presents a significant opportunity. Furthermore, the government's strategic emphasis on achieving energy self-sufficiency and revitalizing national oil company, Petróleos Mexicanos (Pemex), translates into substantial investment in downstream infrastructure development and capacity expansion. This governmental support acts as a crucial regulatory tailwind, encouraging both domestic and foreign investment.

Challenges Impacting Mexico Oil and Gas Downstream Market Growth

Despite its growth potential, the Mexico Oil and Gas Downstream Market faces several critical challenges. Regulatory complexities, including the evolving landscape of environmental standards and permitting processes, can create hurdles for new projects and expansions. Supply chain issues, exacerbated by global geopolitical events and logistical constraints, can lead to delays in equipment procurement and impact project timelines and costs. Competitive pressures from both established domestic players and international producers of refined products and petrochemicals necessitate continuous innovation and cost optimization. Furthermore, the substantial capital investment required for modernizing refineries and building new petrochemical plants, coupled with potential currency volatility, presents financial risks that must be carefully managed by industry stakeholders.

Key Players Shaping the Mexico Oil and Gas Downstream Market Market

- Petróleos Mexicanos (Pemex)

- Braskem SA

- Samsung Engineering Co Ltd

- Grupo Idesa SA de CV

- Fluor Corporation

Significant Mexico Oil and Gas Downstream Market Industry Milestones

- December 2022: Ecopetrol Group announces its energy transition investment plan, allocating 7% to downstream activities. These investments will focus on ensuring the reliability, availability, and sustainability of operations at the Barrancabermeja and Cartagena refineries to support energy security, the energy transition, and decarbonization efforts relevant to Mexico.

- December 2022: Mexican NOC Pemex is set to commence production at the country's eighth refinery in mid-2023. Upon completion, the Olmeca refinery will boast an installed capacity of 340,000 BPD and will produce 170,000 barrels of petrol and 120,000 barrels of ultra-low-sulfur diesel, significantly bolstering national refining capabilities.

Future Outlook for Mexico Oil and Gas Downstream Market Market

The future outlook for the Mexico Oil and Gas Downstream Market is optimistic, driven by sustained demand, strategic investments, and a focus on technological advancement. Key growth catalysts include the ongoing expansion of petrochemical production to cater to the burgeoning manufacturing sector and the continued modernization of refining facilities to enhance efficiency and produce cleaner fuels. Opportunities lie in the development of integrated energy complexes, the adoption of digitalization for operational optimization, and the exploration of opportunities in specialty chemicals. The Mexican government's commitment to strengthening its energy infrastructure and the increasing private sector interest in downstream projects are expected to fuel further growth and innovation in the coming years.

Mexico Oil and Gas Downstream Market Segmentation

- 1. Refineries

- 2. Petrochemicals Plants

Mexico Oil and Gas Downstream Market Segmentation By Geography

- 1. Mexico

Mexico Oil and Gas Downstream Market Regional Market Share

Geographic Coverage of Mexico Oil and Gas Downstream Market

Mexico Oil and Gas Downstream Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Mexico

- 6. Mexico Oil and Gas Downstream Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 6.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Braskem SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Samsung Engineering Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Grupo Idesa SA de CV

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fluor Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Petróleos Mexicanos

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Braskem SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Mexico Oil and Gas Downstream Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Mexico Oil and Gas Downstream Market Share (%) by Company 2025

List of Tables

- Table 1: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Refineries 2020 & 2033

- Table 2: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Refineries 2020 & 2033

- Table 3: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 4: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Petrochemicals Plants 2020 & 2033

- Table 5: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Region 2020 & 2033

- Table 7: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Refineries 2020 & 2033

- Table 8: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Refineries 2020 & 2033

- Table 9: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 10: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Petrochemicals Plants 2020 & 2033

- Table 11: Mexico Oil and Gas Downstream Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Mexico Oil and Gas Downstream Market Volume Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mexico Oil and Gas Downstream Market?

The projected CAGR is approximately 2.35%.

2. Which companies are prominent players in the Mexico Oil and Gas Downstream Market?

Key companies in the market include Braskem SA, Samsung Engineering Co Ltd, Grupo Idesa SA de CV, Fluor Corporation, Petróleos Mexicanos.

3. What are the main segments of the Mexico Oil and Gas Downstream Market?

The market segments include Refineries, Petrochemicals Plants.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.21 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

Refineries Segment to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In December 2022, the Ecopetrol Group announced its investment plan for the energy transition. Out of the total share of investment, 7% will be invested in downstream activities. The investments will emphasize maintaining the reliability, availability, and sustainability of the Barrancabermeja and Cartagena refineries' operations to consolidate energy security, energy transition, and decarbonization of Mexico.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mexico Oil and Gas Downstream Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mexico Oil and Gas Downstream Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mexico Oil and Gas Downstream Market?

To stay informed about further developments, trends, and reports in the Mexico Oil and Gas Downstream Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence