Key Insights

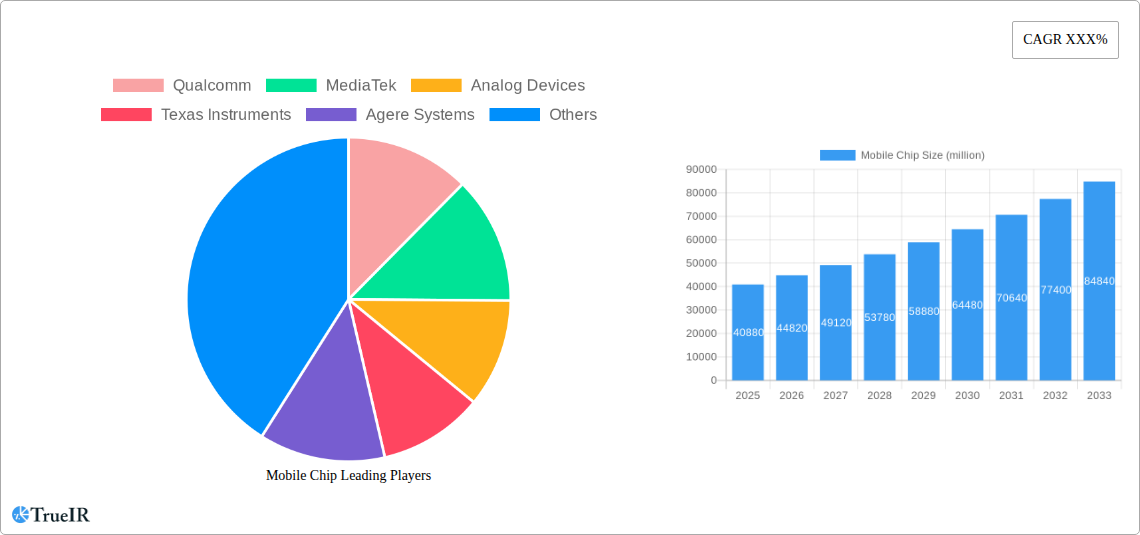

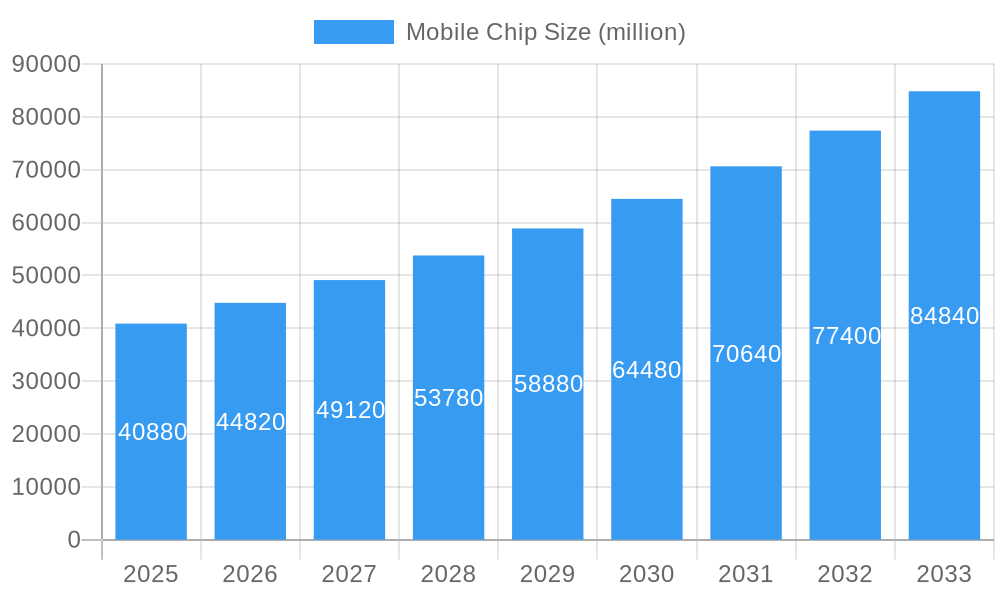

The mobile chip market is poised for substantial growth, projected to reach a market size of $40.88 billion in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 9.9% anticipated throughout the forecast period of 2025-2033. This robust expansion is primarily fueled by the insatiable demand for advanced mobile communication devices, driven by the proliferation of 5G technology, the increasing adoption of smartphones with sophisticated features, and the growing need for enhanced processing power and energy efficiency in mobile applications. The evolution of chip manufacturing processes, particularly the widespread adoption of smaller node technologies like 7nm and 14nm chips, is a significant enabler of this growth, allowing for more powerful and power-efficient mobile chipsets. Emerging applications, such as the Internet of Things (IoT) and augmented/virtual reality (AR/VR) experiences on mobile devices, are also contributing to the market's upward trajectory by demanding specialized and high-performance mobile silicon.

Mobile Chip Market Size (In Billion)

Despite the optimistic outlook, the market faces certain challenges that could temper its growth. Intense competition among leading players, including Qualcomm, MediaTek, and Analog Devices, necessitates continuous innovation and price adjustments, potentially impacting profit margins. Furthermore, the complex and capital-intensive nature of semiconductor manufacturing, coupled with supply chain vulnerabilities and geopolitical factors, can lead to production delays and cost fluctuations. Nevertheless, the enduring consumer appetite for cutting-edge mobile technology, the ongoing advancements in AI and machine learning capabilities integrated into mobile chips, and the expansion of mobile connectivity into new verticals are expected to outweigh these restraints, ensuring a dynamic and expanding market landscape for mobile chips.

Mobile Chip Company Market Share

This comprehensive report delves into the dynamic and rapidly evolving mobile chip market. With an estimated market size projected to reach hundreds of billions by 2033, this analysis leverages high-volume SEO keywords to provide actionable insights for industry stakeholders. We cover key segments, dominant players, and future trends, offering a deep dive into the technological innovations and market forces shaping the global mobile semiconductor industry. This report is your definitive guide to understanding the current landscape and future trajectory of mobile chip technology.

Mobile Chip Market Structure & Competitive Landscape

The global mobile chip market is characterized by a high degree of concentration, with a few dominant players controlling a significant market share, estimated at over 80%. This concentration is driven by substantial R&D investments, proprietary technologies, and economies of scale. Key innovation drivers include the relentless pursuit of enhanced performance, reduced power consumption, and the integration of artificial intelligence (AI) capabilities within mobile devices. Regulatory impacts are increasingly shaping the market, with governments worldwide implementing policies related to semiconductor manufacturing, data privacy, and fair competition. Product substitutes, while emerging, currently struggle to match the integrated performance and ecosystem support offered by dedicated mobile chips. End-user segmentation is primarily driven by the smartphone market, followed by tablets, wearables, and emerging IoT devices. Mergers and acquisitions (M&A) trends have been significant, with an estimated tens of billions in M&A volumes over the historical period, aimed at consolidating market share, acquiring critical intellectual property, and expanding product portfolios. Key M&A activities aim to secure supply chains and bolster R&D capabilities in areas such as 5G, AI acceleration, and advanced process nodes.

- Market Concentration: Dominated by a few key players, signifying high barriers to entry.

- Innovation Drivers: AI integration, 5G/6G advancements, power efficiency, miniaturization, and advanced manufacturing processes.

- Regulatory Impacts: Geopolitical factors, trade policies, and government incentives for domestic semiconductor production.

- Product Substitutes: Limited, primarily in specialized applications rather than general-purpose mobile processing.

- End-User Segmentation: Smartphones (dominant), tablets, wearables, automotive, and industrial IoT.

- M&A Trends: Strategic acquisitions to gain market share, technology access, and talent.

Mobile Chip Market Trends & Opportunities

The mobile chip market is experiencing robust growth, projected to expand significantly from its historical base of hundreds of billions to trillions by the end of the forecast period in 2033. This surge is fueled by the ever-increasing demand for sophisticated mobile devices, the proliferation of 5G and the upcoming 6G networks, and the rapid adoption of AI and machine learning (ML) in mobile applications. The market size growth is expected to witness a Compound Annual Growth Rate (CAGR) of over 10% from the base year 2025. Technological shifts are at the forefront, with a strong emphasis on advanced process nodes like 7nm chips and the continuous development of 14nm chips and 22nm chips, offering superior performance and energy efficiency. The transition to smaller, more powerful chips is critical for enabling next-generation mobile experiences, including augmented reality (AR), virtual reality (VR), and advanced gaming. Consumer preferences are evolving rapidly, with users demanding faster processing speeds, longer battery life, enhanced camera capabilities, and seamless connectivity. This drives semiconductor manufacturers to innovate aggressively. Competitive dynamics are intensifying, with companies constantly vying for market leadership through technological differentiation, strategic partnerships, and aggressive pricing strategies. The integration of specialized AI accelerators and dedicated graphics processing units (GPUs) within mobile chipsets is becoming a standard feature, catering to the growing demand for on-device AI processing. The expansion of the Internet of Things (IoT) ecosystem, encompassing smart homes, connected vehicles, and industrial automation, presents a substantial long-term opportunity for mobile chip vendors to diversify their product offerings beyond traditional mobile communication devices. Furthermore, the increasing focus on sustainable technology and energy-efficient designs will play a pivotal role in shaping product development and consumer choice. Opportunities also lie in developing chips for emerging markets with rapidly growing smartphone penetration and for niche applications requiring high-performance mobile computing. The continuous evolution of mobile operating systems and applications also necessitates frequent upgrades and innovations in mobile chip architectures to support new functionalities and improve user experiences.

Dominant Markets & Segments in Mobile Chip

The Mobile Communication application segment remains the undisputed leader in the mobile chip market, driven by the colossal global smartphone and tablet user base. Within this segment, the demand for advanced chipsets that support high-speed 5G and future 6G connectivity is a primary growth catalyst, projected to account for over 70% of the market share by 2033. Countries like China, the United States, and South Korea are leading the charge in 5G infrastructure deployment and smartphone adoption, significantly influencing regional market dominance. The 7nm chip technology currently holds a dominant position due to its balance of performance, power efficiency, and manufacturing maturity, followed closely by the rapidly advancing 14nm chip segment. While 22nm chips still represent a considerable portion of the market, especially in cost-sensitive segments and older device generations, the trend is clearly towards more advanced process nodes. The "Other" application segment, encompassing wearables, automotive infotainment systems, and industrial IoT devices, is experiencing exponential growth, albeit from a smaller base. Infrastructure development, including the build-out of 5G base stations and enterprise networks, indirectly fuels demand for mobile chips used in networking equipment and connected devices. Favorable government policies, such as semiconductor manufacturing incentives and digital transformation initiatives, are crucial for fostering growth in key regions. The growing adoption of mobile devices in emerging economies, driven by increasing disposable incomes and the need for digital connectivity, presents a significant opportunity for market expansion.

- Dominant Application: Mobile Communication, driven by smartphone and tablet demand.

- Leading Regions: Asia-Pacific (especially China, South Korea, India), North America, and Europe.

- Key Segments by Type:

- 7nm Chip: Leading in high-end smartphones and performance-critical applications.

- 14nm Chip: Significant market share, particularly in mid-range devices and broader IoT applications.

- 22nm Chip: Still relevant for cost-sensitive devices and specific industrial applications.

- Other Types: Emerging technologies like 5nm and 3nm chips, driving future innovation.

- Growth Drivers: 5G/6G deployment, AI/ML integration, IoT expansion, increasing smartphone penetration in emerging markets.

- Policy Impact: Government incentives for R&D and manufacturing, trade agreements, and intellectual property protection.

Mobile Chip Product Analysis

Mobile chip product innovations are centered on enhancing processing power, improving energy efficiency, and integrating advanced functionalities. Leading companies are focusing on developing System-on-Chips (SoCs) that combine CPUs, GPUs, AI accelerators, and connectivity modems on a single die. Competitive advantages are derived from proprietary architectures, cutting-edge manufacturing processes (e.g., 7nm chips and beyond), and robust software ecosystems. For instance, advanced AI capabilities enable on-device machine learning for features like real-time language translation, enhanced photography, and personalized user experiences. The integration of 5G modems directly into SoCs is a critical advancement, simplifying device design and reducing power consumption.

Key Drivers, Barriers & Challenges in Mobile Chip

The mobile chip market is propelled by several key drivers, including the relentless global demand for smarter, faster, and more connected devices. Technological advancements, such as the maturation of 7nm chip technology and the ongoing development of 14nm chips and beyond, continue to push performance boundaries. The expanding Internet of Things (IoT) ecosystem and the widespread adoption of 5G networks represent significant growth catalysts. Economic factors, including rising disposable incomes in emerging markets and increased enterprise investment in mobile solutions, also play a crucial role. Policy-driven factors, such as government incentives for domestic semiconductor manufacturing and digital transformation initiatives, further bolster market growth.

Key challenges impacting mobile chip growth include the immense capital expenditure required for leading-edge manufacturing facilities, estimated at billions per fab. Supply chain vulnerabilities, as highlighted by recent global disruptions, pose a significant risk, leading to extended lead times and increased costs. Regulatory hurdles, including trade restrictions and intellectual property disputes, can impede market access and innovation. Competitive pressures are intense, with companies constantly striving to outpace rivals in performance and features, often leading to rapid product obsolescence. Furthermore, the increasing complexity of chip design and manufacturing at advanced process nodes requires substantial investment in highly specialized talent and R&D.

Key Drivers:

- Technological Advancements: Maturation of 7nm chip and development of 14nm chips, AI/ML integration.

- Market Demand: Proliferation of smartphones, wearables, and IoT devices.

- Connectivity: Rollout of 5G and future 6G networks.

- Economic Factors: Growing middle class, enterprise mobility investments.

- Government Support: Incentives for domestic manufacturing.

Key Barriers & Challenges:

- High Capital Expenditure: Billions required for advanced fabrication.

- Supply Chain Disruptions: Geopolitical risks and material shortages.

- Regulatory Complexity: Trade wars, IP disputes, and data privacy laws.

- Intense Competition: Rapid product cycles and pricing pressures.

- Talent Shortage: Demand for specialized engineers.

- Environmental Concerns: Energy consumption and e-waste.

Growth Drivers in the Mobile Chip Market

The mobile chip market's growth is primarily fueled by the escalating global demand for advanced mobile devices, encompassing smartphones, tablets, and wearables. The ongoing widespread deployment of 5G infrastructure and the anticipated advent of 6G networks are critical drivers, necessitating higher-performance and more integrated chipsets. The rapid integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities into mobile applications, from enhanced camera features to on-device data processing, is creating new avenues for chip innovation and demand. Furthermore, the burgeoning Internet of Things (IoT) ecosystem, spanning smart homes, connected vehicles, and industrial automation, presents substantial growth opportunities for specialized mobile chips. Government initiatives, including incentives for domestic semiconductor manufacturing and digital transformation agendas, are also playing a significant role in fostering market expansion.

Challenges Impacting Mobile Chip Growth

Despite robust growth, the mobile chip market faces significant challenges. The immense capital required for designing and manufacturing cutting-edge chips, especially those utilizing advanced nodes like 7nm chips and beyond, can be a substantial barrier to entry and sustainability. Global supply chain vulnerabilities, exacerbated by geopolitical tensions and natural disasters, can lead to production delays and increased costs, impacting market availability and pricing. Stringent regulatory environments, including evolving trade policies and intellectual property protection laws, can create uncertainties and hinder global market access. Intense competition among major players, characterized by rapid product cycles and the constant need for innovation, can also put pressure on profit margins and market share.

Key Players Shaping the Mobile Chip Market

- Qualcomm

- MediaTek

- Analog Devices

- Texas Instruments

- Agere Systems

- Koninklijke Philips N.V.

- Infineon Technologies AG

- Skyworks Solutions, Inc.

- Spreadtrum Communications

Significant Mobile Chip Industry Milestones

- 2019: Introduction of flagship smartphones featuring 7nm chips, enabling significant performance and efficiency gains.

- 2020: Accelerated rollout of 5G networks globally, driving demand for 5G-enabled mobile chips.

- 2021: Increased focus on AI integration in mobile chipsets for enhanced camera capabilities and on-device processing.

- 2022: Growing awareness and initial development of next-generation chip technologies beyond 7nm.

- 2023: Continued advancements in power efficiency and integration of specialized processors for AI/ML workloads.

- 2024: Strengthening supply chains and strategic partnerships to mitigate global semiconductor shortages.

Future Outlook for Mobile Chip Market

The future outlook for the mobile chip market is exceptionally promising, driven by several key growth catalysts. The continued expansion of 5G and the emergence of 6G technologies will necessitate even more sophisticated and powerful chipsets, creating sustained demand. The burgeoning Internet of Things (IoT) sector, with its vast array of connected devices, will offer substantial diversification opportunities. Furthermore, the pervasive integration of AI and machine learning into everyday mobile applications will drive innovation in specialized processing units. Strategic opportunities lie in developing ultra-low-power chips for wearables and the expanding edge computing landscape. The market is poised for significant growth, projected to reach trillions by the end of the forecast period, offering immense potential for companies that can innovate and adapt to the rapidly evolving technological and consumer demands.

Mobile Chip Segmentation

-

1. Application

- 1.1. Mobile Communication

- 1.2. Other

-

2. Type

- 2.1. 7nm Chip

- 2.2. 14nm Chip

- 2.3. 22nm Chip

- 2.4. Other

Mobile Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

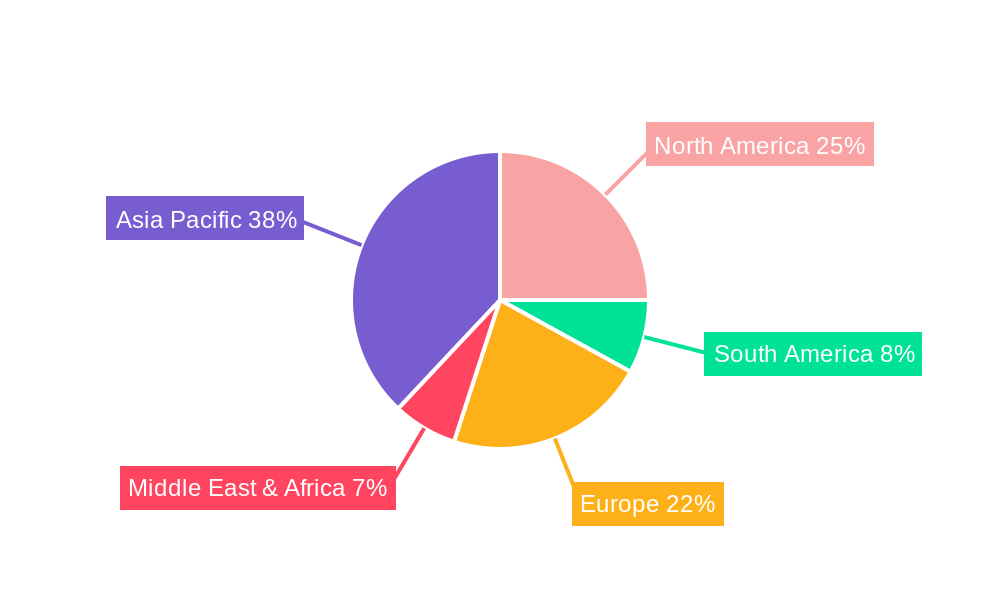

Mobile Chip Regional Market Share

Geographic Coverage of Mobile Chip

Mobile Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mobile Communication

- 5.1.2. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 7nm Chip

- 5.2.2. 14nm Chip

- 5.2.3. 22nm Chip

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mobile Communication

- 6.1.2. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 7nm Chip

- 6.2.2. 14nm Chip

- 6.2.3. 22nm Chip

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mobile Communication

- 7.1.2. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 7nm Chip

- 7.2.2. 14nm Chip

- 7.2.3. 22nm Chip

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mobile Communication

- 8.1.2. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 7nm Chip

- 8.2.2. 14nm Chip

- 8.2.3. 22nm Chip

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mobile Communication

- 9.1.2. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 7nm Chip

- 9.2.2. 14nm Chip

- 9.2.3. 22nm Chip

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Mobile Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mobile Communication

- 10.1.2. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 7nm Chip

- 10.2.2. 14nm Chip

- 10.2.3. 22nm Chip

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Qualcomm

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 MediaTek

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Analog Devices

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Texas Instruments

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Agere Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Koninklijke Philips N.V.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Infineon Technologies AG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Skyworks Solutions Inc.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Spreadtrum Communications

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Qualcomm

List of Figures

- Figure 1: Global Mobile Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Mobile Chip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Mobile Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Mobile Chip Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Mobile Chip Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Mobile Chip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Mobile Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Mobile Chip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Mobile Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Mobile Chip Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Mobile Chip Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Mobile Chip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Mobile Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Mobile Chip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Mobile Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Mobile Chip Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Mobile Chip Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Mobile Chip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Mobile Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Mobile Chip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Mobile Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Mobile Chip Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Mobile Chip Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Mobile Chip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Mobile Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Mobile Chip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Mobile Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Mobile Chip Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Mobile Chip Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Mobile Chip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Mobile Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Mobile Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Mobile Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Mobile Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Mobile Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Mobile Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Mobile Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Mobile Chip Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Mobile Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Mobile Chip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Chip?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Mobile Chip?

Key companies in the market include Qualcomm, MediaTek, Analog Devices, Texas Instruments, Agere Systems, Koninklijke Philips N.V., Infineon Technologies AG, Skyworks Solutions, Inc., Spreadtrum Communications.

3. What are the main segments of the Mobile Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Chip?

To stay informed about further developments, trends, and reports in the Mobile Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence