Key Insights

The North Africa battery market is projected for substantial expansion, with a projected market size of $4.97 billion by 2025, and is expected to grow at a robust Compound Annual Growth Rate (CAGR) of 6.55%. This growth is primarily driven by increasing demand for energy storage solutions across key sectors. The automotive industry, especially the adoption of electric vehicles (EVs), and industrial applications like backup power and renewable energy storage, are significant growth drivers. The consumer electronics sector and the integration of smart grid technologies further augment demand for advanced battery solutions.

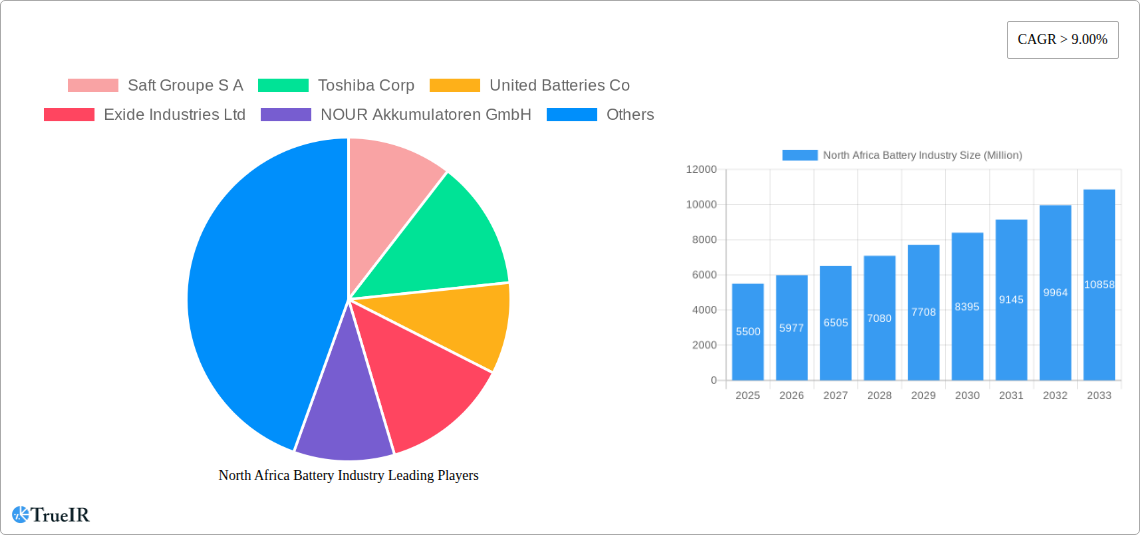

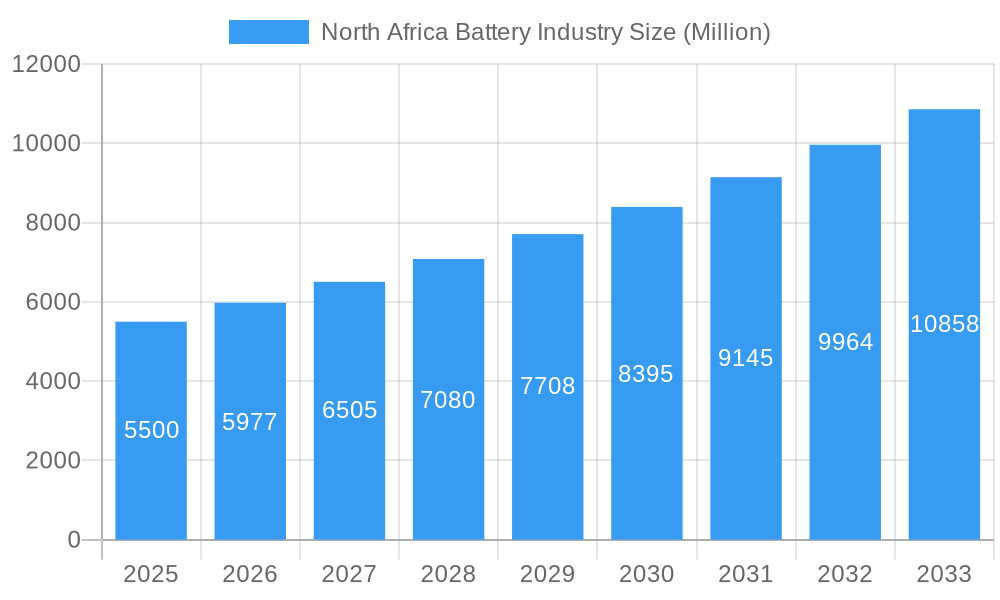

North Africa Battery Industry Market Size (In Billion)

Technological advancements and evolving consumer preferences are shaping market dynamics. Lithium-ion batteries are expected to dominate due to their superior performance, while lead-acid batteries will maintain a significant share in cost-sensitive applications. The "Rest of North Africa" segment is anticipated to experience the highest growth, supported by economic development and infrastructure investments. Potential restraints include raw material supply chain volatility, regulatory shifts, and capital investment needs for manufacturing and recycling. Key market players are focusing on expanding production and R&D to meet market demands.

North Africa Battery Industry Company Market Share

North Africa Battery Industry Market: Comprehensive Analysis and Future Outlook (2019-2033)

Unlock unparalleled insights into the burgeoning North African battery market with this in-depth report. Spanning the historical period of 2019-2024 and projecting through to 2033, this analysis provides a granular view of market dynamics, key players, technological advancements, and emerging opportunities. Leveraging high-volume SEO keywords like "North Africa battery market," "automotive batteries North Africa," "lithium-ion battery Egypt," and "lead-acid battery Algeria," this report is designed to elevate your understanding and strategic positioning in this critical sector. With a base and estimated year of 2025, and a forecast period from 2025-2033, this report delves into the core components driving growth, including a detailed examination of primary and secondary battery types, lithium-ion and lead-acid technologies, and critical applications across automotive, industrial, and portable segments. Explore the competitive landscape featuring industry giants such as Saft Groupe S.A., Toshiba Corp, and Panasonic Corporation, alongside regional specialists like United Batteries Co. and EL-Nisr Company.

North Africa Battery Industry Market Structure & Competitive Landscape

The North African battery industry exhibits a dynamic and evolving market structure, characterized by a moderate concentration of key players alongside a growing number of regional manufacturers. Innovation drivers are primarily fueled by increasing demand for renewable energy storage solutions and advancements in electric vehicle (EV) adoption. Regulatory impacts are becoming increasingly significant, with governments in countries like Egypt and Algeria implementing policies to encourage local manufacturing and investment in battery technologies. Product substitutes, while present, are gradually being outpaced by the superior performance and lifecycle of advanced battery chemistries, particularly lithium-ion. End-user segmentation reveals a strong emphasis on the automotive sector, driven by both traditional internal combustion engine vehicles and the nascent EV market, followed by the industrial segment for power backup and renewable energy integration. Mergers and acquisitions (M&A) trends are anticipated to accelerate as larger international players seek to establish a stronger foothold in this high-growth region. Current M&A volumes are estimated at $100 Million historically, with projections for significant increases. The competitive landscape is shaped by the interplay of global technological leaders and localized production capabilities, creating a complex but opportunity-rich environment for market participants.

North Africa Battery Industry Market Trends & Opportunities

The North Africa battery industry is on an upward trajectory, projected to witness substantial market size growth driven by a confluence of technological advancements, evolving consumer preferences, and evolving competitive dynamics. The market is anticipated to expand from a current estimated value of $1,500 Million in 2025 to $4,000 Million by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of approximately 13%. This growth is intrinsically linked to the increasing adoption of electric vehicles across the region, a trend that is gaining momentum due to government incentives and growing environmental consciousness. Simultaneously, the burgeoning renewable energy sector, particularly solar power, is creating significant demand for energy storage systems, further propelling the market forward. Consumer preferences are shifting towards more efficient, longer-lasting, and environmentally friendly battery solutions. This has led to a surge in demand for lithium-ion batteries, which offer superior energy density and lifespan compared to traditional lead-acid batteries. However, lead-acid batteries continue to hold a significant market share, especially in the automotive and backup power segments, due to their cost-effectiveness and established infrastructure. The competitive landscape is becoming more intense, with both global manufacturers and local players vying for market dominance. This competition is fostering innovation, driving down prices, and increasing the availability of diverse battery products across the region. Opportunities abound for companies that can leverage these trends, including localized manufacturing, development of advanced battery recycling infrastructure, and the provision of integrated energy storage solutions for both grid-scale and residential applications. The penetration rate of advanced battery technologies is expected to rise from 30% in 2025 to over 65% by 2033.

Dominant Markets & Segments in North Africa Battery Industry

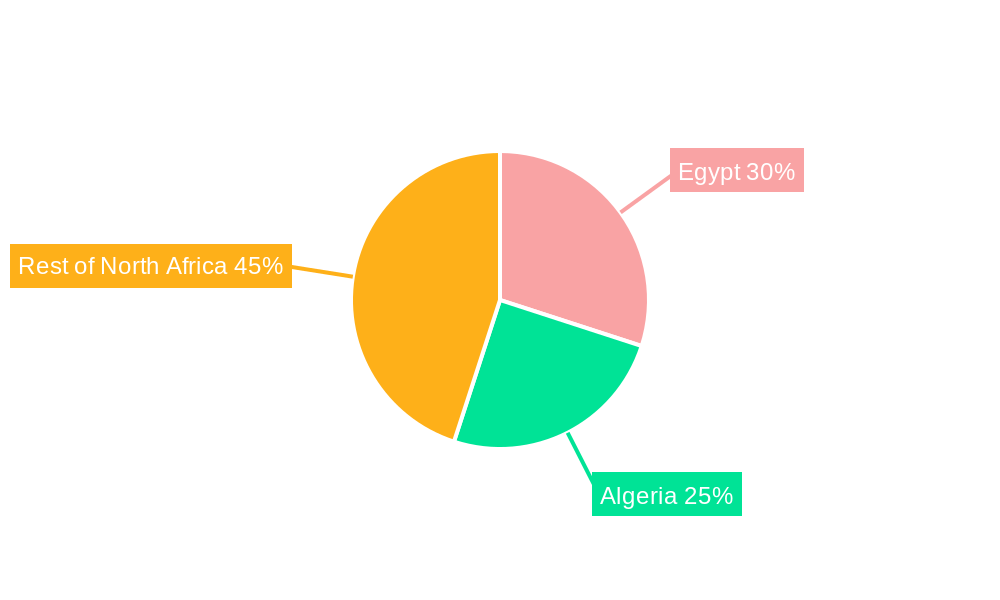

Within the North African battery industry, Egypt emerges as a dominant market, accounting for an estimated 40% of the total market share. This dominance is driven by a combination of a large population, a rapidly expanding automotive sector, and significant government initiatives to promote renewable energy and industrial development. Algeria follows as a key market, representing approximately 25% of the regional share, with strong demand from its oil and gas industry and a growing interest in automotive battery solutions. The "Rest of North Africa" segment, encompassing countries like Morocco, Tunisia, and Libya, collectively contributes the remaining 35%, with varied growth potentials influenced by individual economic conditions and policy frameworks.

Geographically, while Egypt and Algeria lead, the Automotive Batteries application segment holds the largest market share across the entire North African region, capturing an estimated 45%. This is fueled by a consistent demand for replacement batteries and the gradual but increasing adoption of electric and hybrid vehicles. The Industrial Batteries segment, crucial for powering telecommunications, data centers, and renewable energy storage (as exemplified by the KarmSolar project), represents approximately 30% of the market. Portable Batteries, serving consumer electronics and portable power tools, contribute around 20%, with the "Others" segment, including specialized batteries for defense and medical devices, making up the remaining 5%.

Technologically, Lead-acid Battery technology continues to be a significant force, holding an estimated 55% of the market share due to its cost-effectiveness and established presence in automotive applications. However, Lithium-ion Battery technology is witnessing rapid growth, projected to capture 40% of the market by 2033, driven by its superior performance in EVs and renewable energy storage. The "Others" technology segment, including emerging chemistries, accounts for the remaining 5%.

Across the "Type" segmentation, Secondary Battery dominates with an estimated 70% market share, owing to their rechargeability and wide application in automotive and industrial uses. Primary Battery, used in single-use applications like remote controls and some portable devices, accounts for the remaining 30%.

Key growth drivers in these dominant markets and segments include:

- Government Policies: Favorable regulations and incentives for EV adoption, renewable energy deployment, and local manufacturing of batteries.

- Infrastructure Development: Expansion of charging infrastructure for EVs and increased grid modernization efforts.

- Industrial Growth: Continued expansion of key industries like telecommunications, oil and gas, and manufacturing requiring reliable power backup.

- Consumer Demand: Rising consumer awareness of energy efficiency and the desire for advanced portable electronics.

- Technological Advancements: Improvements in battery energy density, lifespan, and safety, particularly in lithium-ion technologies.

North Africa Battery Industry Product Analysis

Product innovation in the North African battery industry is primarily focused on enhancing energy density, improving cycle life, and ensuring safety across various chemistries. Lithium-ion battery technologies, particularly NMC (Nickel Manganese Cobalt) and LFP (Lithium Iron Phosphate), are gaining traction due to their suitability for electric vehicles and large-scale energy storage. Lead-acid batteries are seeing incremental improvements in performance and lifespan, catering to cost-sensitive applications. Competitive advantages lie in localized manufacturing capabilities, cost-efficiency for bulk applications, and the development of robust battery management systems for enhanced safety and performance. The market is increasingly demanding batteries that offer a balance of performance, cost, and sustainability.

Key Drivers, Barriers & Challenges in North Africa Battery Industry

Key Drivers:

The North African battery industry is propelled by several key drivers. Technological advancements, particularly in lithium-ion battery chemistries, are offering enhanced performance and longer lifespans, making them increasingly viable for diverse applications. Government initiatives and supportive policies aimed at promoting electric mobility and renewable energy integration are creating significant market opportunities. The growing automotive sector, both for internal combustion engine vehicles and the nascent electric vehicle market, is a primary demand generator. Furthermore, the expansion of industrial sectors requiring reliable power backup and the increasing adoption of renewable energy sources necessitate robust energy storage solutions.

Barriers & Challenges:

Despite the growth potential, several barriers and challenges impact the North African battery industry. Supply chain disruptions, both for raw materials and finished products, can lead to price volatility and production delays. Regulatory complexities and the absence of harmonized standards across different North African countries can hinder market entry and expansion. High initial investment costs for establishing advanced manufacturing facilities, especially for lithium-ion battery production, pose a significant challenge. Intense competition from established global players and the risk of intellectual property infringement are also key concerns. The limited availability of skilled labor for advanced battery manufacturing and maintenance further restrains growth. The estimated impact of supply chain disruptions on market growth is 5% reduction in potential output.

Growth Drivers in the North Africa Battery Industry Market

Key growth drivers in the North Africa battery industry market include the accelerating adoption of electric vehicles across the region, incentivized by government policies and increasing consumer awareness of environmental benefits. The significant investments in renewable energy projects, particularly solar power, are creating a substantial demand for energy storage systems to ensure grid stability and reliable power supply. Technological advancements leading to more efficient, longer-lasting, and cost-effective battery solutions, especially in lithium-ion technology, are expanding application possibilities. Furthermore, the ongoing industrialization and infrastructure development across North Africa necessitate robust battery solutions for backup power and operational continuity. The growing demand for portable electronics also contributes to market expansion.

Challenges Impacting North Africa Battery Industry Growth

Challenges impacting North Africa battery industry growth include the underdeveloped state of raw material sourcing and refining capabilities for battery production within the region, leading to import dependency and increased costs. Regulatory hurdles and the lack of standardized safety and environmental regulations across different North African countries can create market fragmentation and compliance complexities. High initial capital expenditure required for setting up advanced battery manufacturing facilities, particularly for lithium-ion battery production, remains a significant barrier. Supply chain volatility for critical battery components and materials can lead to production delays and price fluctuations. Furthermore, a scarcity of skilled labor and technical expertise in advanced battery technologies can impede the development and expansion of the industry.

Key Players Shaping the North Africa Battery Industry Market

- Saft Groupe S A

- Toshiba Corp

- United Batteries Co

- Exide Industries Ltd

- NOUR Akkumulatoren GmbH

- Duracell Inc

- Murata Manufacturing Co Ltd

- EL-Nisr Company

- Panasonic Corporation

- Chloride Egypt S A E

Significant North Africa Battery Industry Industry Milestones

- October 2022: KarmSolar secured $2.4 Million in bank financing for a solar-plus-storage project in Egypt.

- Impact: This milestone highlights the growing investment in renewable energy storage solutions in Egypt and underscores the critical role of battery technology in supporting sustainable energy initiatives. The project's expansion phase, involving a 1MW/3.957MWh storage system, demonstrates the increasing scale of battery deployment in the region.

Future Outlook for North Africa Battery Industry Market

The future outlook for the North Africa battery industry market is exceptionally promising, driven by sustained growth catalysts. Strategic opportunities lie in capitalizing on the burgeoning demand for electric vehicles and the widespread adoption of renewable energy sources, which are increasingly reliant on advanced battery storage. Localized manufacturing of batteries, supported by government incentives and foreign direct investment, is expected to gain significant traction, fostering job creation and technological transfer. Furthermore, the development of battery recycling infrastructure will become crucial to ensure sustainability and mitigate the environmental impact of battery disposal. The market is poised for continued expansion, driven by innovation in battery technology, favorable policy environments, and a growing consumer and industrial demand for reliable and efficient energy storage solutions. The market is projected to reach $4,000 Million by 2033.

North Africa Battery Industry Segmentation

-

1. Type

- 1.1. Primary Battery

- 1.2. Secondary Battery

-

2. Technology

- 2.1. Lithium-ion Battery

- 2.2. Lead-acid Battery

- 2.3. Others

-

3. Application

- 3.1. Automotive Batteries

- 3.2. Industrial Batteries

- 3.3. Portable Batteries

- 3.4. Others

-

4. Geography

- 4.1. Egypt

- 4.2. Algeria

- 4.3. Rest of North Africa

North Africa Battery Industry Segmentation By Geography

- 1. Egypt

- 2. Algeria

- 3. Rest of North Africa

North Africa Battery Industry Regional Market Share

Geographic Coverage of North Africa Battery Industry

North Africa Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Primary Battery

- 5.1.2. Secondary Battery

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Lithium-ion Battery

- 5.2.2. Lead-acid Battery

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Automotive Batteries

- 5.3.2. Industrial Batteries

- 5.3.3. Portable Batteries

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. Egypt

- 5.4.2. Algeria

- 5.4.3. Rest of North Africa

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Egypt

- 5.5.2. Algeria

- 5.5.3. Rest of North Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North Africa Battery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Primary Battery

- 6.1.2. Secondary Battery

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Lithium-ion Battery

- 6.2.2. Lead-acid Battery

- 6.2.3. Others

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Automotive Batteries

- 6.3.2. Industrial Batteries

- 6.3.3. Portable Batteries

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. Egypt

- 6.4.2. Algeria

- 6.4.3. Rest of North Africa

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Egypt North Africa Battery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Primary Battery

- 7.1.2. Secondary Battery

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Lithium-ion Battery

- 7.2.2. Lead-acid Battery

- 7.2.3. Others

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Automotive Batteries

- 7.3.2. Industrial Batteries

- 7.3.3. Portable Batteries

- 7.3.4. Others

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. Egypt

- 7.4.2. Algeria

- 7.4.3. Rest of North Africa

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Algeria North Africa Battery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Primary Battery

- 8.1.2. Secondary Battery

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Lithium-ion Battery

- 8.2.2. Lead-acid Battery

- 8.2.3. Others

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Automotive Batteries

- 8.3.2. Industrial Batteries

- 8.3.3. Portable Batteries

- 8.3.4. Others

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. Egypt

- 8.4.2. Algeria

- 8.4.3. Rest of North Africa

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of North Africa North Africa Battery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Primary Battery

- 9.1.2. Secondary Battery

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Lithium-ion Battery

- 9.2.2. Lead-acid Battery

- 9.2.3. Others

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Automotive Batteries

- 9.3.2. Industrial Batteries

- 9.3.3. Portable Batteries

- 9.3.4. Others

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. Egypt

- 9.4.2. Algeria

- 9.4.3. Rest of North Africa

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Saft Groupe S A

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Toshiba Corp

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 United Batteries Co

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Exide Industries Ltd

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 NOUR Akkumulatoren GmbH

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Duracell Inc*List Not Exhaustive

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Murata Manufacturing Co Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 EL-Nisr Company

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Panasonic Corporation

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Chloride Egypt S A E

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 Saft Groupe S A

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North Africa Battery Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North Africa Battery Industry Share (%) by Company 2025

List of Tables

- Table 1: North Africa Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North Africa Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: North Africa Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 4: North Africa Battery Industry Volume K Tons Forecast, by Technology 2020 & 2033

- Table 5: North Africa Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: North Africa Battery Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 7: North Africa Battery Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North Africa Battery Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 9: North Africa Battery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 10: North Africa Battery Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 11: North Africa Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 12: North Africa Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 13: North Africa Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: North Africa Battery Industry Volume K Tons Forecast, by Technology 2020 & 2033

- Table 15: North Africa Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: North Africa Battery Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 17: North Africa Battery Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 18: North Africa Battery Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 19: North Africa Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: North Africa Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 21: North Africa Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: North Africa Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 23: North Africa Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 24: North Africa Battery Industry Volume K Tons Forecast, by Technology 2020 & 2033

- Table 25: North Africa Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 26: North Africa Battery Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 27: North Africa Battery Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 28: North Africa Battery Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 29: North Africa Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: North Africa Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 31: North Africa Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 32: North Africa Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 33: North Africa Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 34: North Africa Battery Industry Volume K Tons Forecast, by Technology 2020 & 2033

- Table 35: North Africa Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 36: North Africa Battery Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 37: North Africa Battery Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 38: North Africa Battery Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 39: North Africa Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: North Africa Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North Africa Battery Industry?

The projected CAGR is approximately 6.55%.

2. Which companies are prominent players in the North Africa Battery Industry?

Key companies in the market include Saft Groupe S A, Toshiba Corp, United Batteries Co, Exide Industries Ltd, NOUR Akkumulatoren GmbH, Duracell Inc*List Not Exhaustive, Murata Manufacturing Co Ltd, EL-Nisr Company, Panasonic Corporation, Chloride Egypt S A E.

3. What are the main segments of the North Africa Battery Industry?

The market segments include Type, Technology, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.97 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Uses of Natural Gas in Various Sectors.

6. What are the notable trends driving market growth?

Lithium-ion Batteries to Dominate the Market Growth.

7. Are there any restraints impacting market growth?

4.; Volatile Natural Gas Prices.

8. Can you provide examples of recent developments in the market?

October 2022: KarmSolar has secured USD 2.4 million in bank financing for a solar-plus-storage project in Egypt. The funds will be used for Phase 2 expansion of the company's existing solar microgrid system for Cairo 3A Poultry's farm in the Bahareya Oasis in Giza, Egypt. The energy storage system will comprise a 2.576MWp PV inverter and 1MW/3.957MWh storage.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North Africa Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North Africa Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North Africa Battery Industry?

To stay informed about further developments, trends, and reports in the North Africa Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence