Key Insights

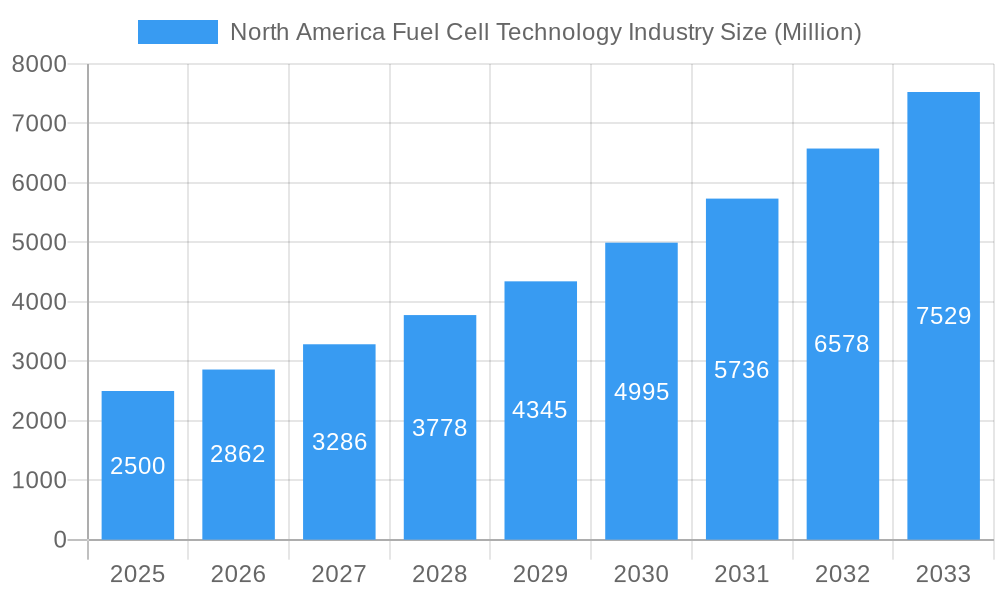

The North American fuel cell technology market is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 14.97% from 2025 to 2033. This expansion is driven primarily by increasing government support for clean energy initiatives, the rising demand for efficient and reliable power solutions in various sectors, and advancements in fuel cell technology leading to improved performance and cost reductions. The portable fuel cell segment is witnessing significant traction due to its applications in portable electronic devices and backup power systems, while the stationary segment is benefiting from the growing adoption of fuel cells in distributed generation and microgrids. The transportation segment, encompassing fuel cell electric vehicles (FCEVs), is expected to experience substantial growth fueled by investments in infrastructure development and ongoing technological improvements addressing range and refueling time limitations. Polymer Electrolyte Membrane Fuel Cells (PEMFCs) currently dominate the market due to their suitability for diverse applications, but Solid Oxide Fuel Cells (SOFCs) are gaining traction owing to their higher efficiency at high temperatures. Leading players such as FuelCell Energy Inc., Ballard Power Systems Inc., and Plug Power Inc. are actively shaping the market landscape through strategic partnerships, technological innovations, and expansion of manufacturing capacities. The United States, being a key player in fuel cell research and development, holds a significant market share within North America.

North America Fuel Cell Technology Industry Market Size (In Billion)

Growth is not without challenges. High initial investment costs, limited refueling infrastructure for FCEVs, and the need for continuous technological advancements to enhance durability and reduce production costs remain key restraints to widespread adoption. However, ongoing research and development, coupled with supportive government policies and increasing consumer awareness of environmental concerns, are expected to mitigate these limitations. The market is segmented based on application (portable, stationary, transportation) and fuel cell technology (PEMFC, SOFC, others). While precise market sizing for 2025 is not provided, extrapolating from the CAGR and considering industry reports indicating a significant market size, a reasonable estimate for the North American market in 2025 would be in the range of several billion dollars, reflecting the substantial investments and growth projections. Continued growth in all segments is anticipated throughout the forecast period (2025-2033), with PEMFCs maintaining a dominant position, yet SOFCs steadily gaining market share due to their superior efficiency in certain applications.

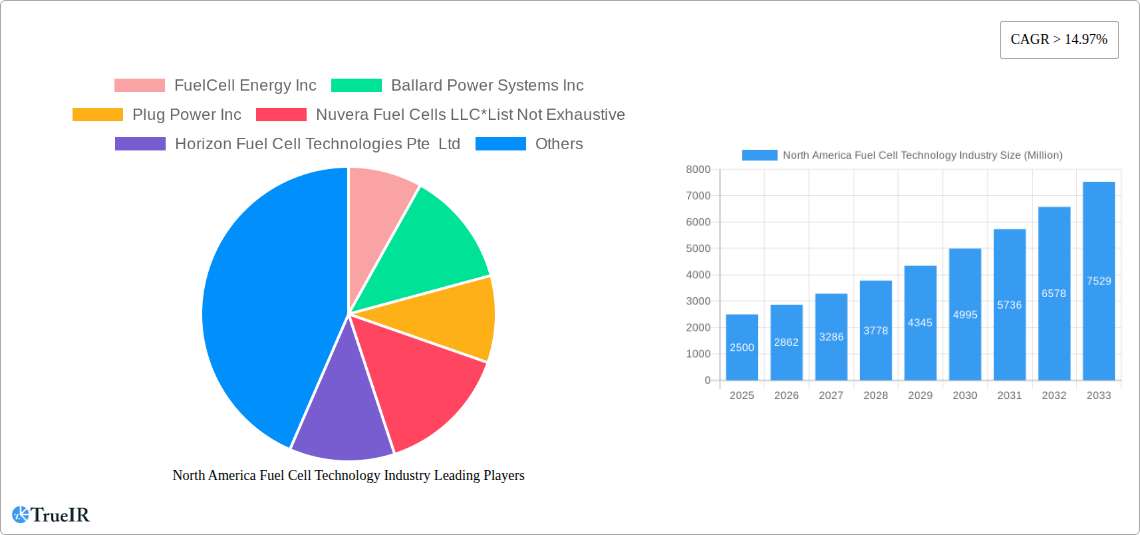

North America Fuel Cell Technology Industry Company Market Share

North America Fuel Cell Technology Industry: 2019-2033 Market Report

This comprehensive report delivers an in-depth analysis of the North American fuel cell technology industry, providing critical insights for stakeholders across the value chain. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages extensive primary and secondary research to offer a granular view of market size, segmentation, competitive dynamics, and future growth prospects. Expect detailed analysis of key players such as FuelCell Energy Inc, Ballard Power Systems Inc, Plug Power Inc, Nuvera Fuel Cells LLC, Horizon Fuel Cell Technologies Pte Ltd, and Hydrogenics Corporation. This report is essential for investors, industry professionals, and strategic decision-makers seeking to navigate the complexities and capitalize on the opportunities within this rapidly evolving sector.

North America Fuel Cell Technology Industry Market Structure & Competitive Landscape

The North American fuel cell technology market exhibits a moderately concentrated structure, with a few major players holding significant market share. However, the landscape is dynamic, characterized by ongoing innovation, strategic partnerships, and mergers and acquisitions (M&A). The Herfindahl-Hirschman Index (HHI) for 2024 is estimated at xx, indicating a moderately concentrated market. Regulatory frameworks, particularly those incentivizing clean energy adoption, play a significant role in shaping market dynamics. Product substitutes, such as battery technologies, pose a competitive threat, driving innovation within the fuel cell sector.

- Market Concentration: The top 5 players account for approximately xx% of the market in 2024.

- Innovation Drivers: Government funding, R&D investments, and the demand for clean energy solutions are key drivers of innovation.

- Regulatory Impacts: Policies supporting renewable energy and emission reduction targets significantly influence market growth.

- Product Substitutes: Battery electric vehicles and other energy storage technologies pose a competitive challenge.

- End-User Segmentation: The market is segmented by application (portable, stationary, transportation) and fuel cell technology (PEMFC, SOFC, others).

- M&A Trends: The past five years have witnessed xx major M&A deals, primarily focused on consolidating market share and expanding technological capabilities. The total value of these deals is estimated at USD xx Million.

North America Fuel Cell Technology Industry Market Trends & Opportunities

The North American fuel cell technology market is experiencing robust growth, driven by increasing environmental concerns, advancements in fuel cell technology, and supportive government policies. The market size is projected to reach USD xx Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration rates for fuel cell vehicles are expected to increase from xx% in 2025 to xx% by 2033, driven by technological advancements and decreasing costs. Key trends include the growing adoption of PEMFCs in transportation applications, the increasing interest in SOFCs for stationary power generation, and the emergence of niche applications in portable devices. Competitive dynamics are shaped by technological innovation, pricing strategies, and strategic partnerships.

Dominant Markets & Segments in North America Fuel Cell Technology Industry

The transportation segment is currently the dominant application area for fuel cell technology in North America, driven by the growing demand for clean transportation solutions. California and other states with stringent emission regulations are leading regional markets. Within fuel cell technologies, Polymer Electrolyte Membrane Fuel Cells (PEMFCs) hold the largest market share due to their suitability for transportation and portable applications.

- Key Growth Drivers for Transportation Segment:

- Increasing stringency of emission regulations.

- Government incentives and subsidies for fuel cell vehicles.

- Development of hydrogen refueling infrastructure.

- Key Growth Drivers for Stationary Segment:

- Growing demand for backup power and distributed generation.

- Cost competitiveness compared to diesel generators.

- Increasing adoption of SOFCs for high-efficiency power generation.

- Key Growth Drivers for Portable Segment:

- Growing demand for portable power solutions in various applications.

- Miniaturization of fuel cell technology.

The United States is the leading national market, owing to its robust economy, supportive government policies, and a strong focus on technological advancement. Canada also demonstrates significant market potential, fueled by its investments in clean energy technologies.

North America Fuel Cell Technology Industry Product Analysis

Significant advancements in fuel cell technology are driving product innovation. PEMFCs are becoming more efficient and cost-effective, while SOFCs are gaining traction in stationary power generation due to their higher efficiency. The focus is on improving durability, reducing costs, and enhancing performance to expand market penetration across various applications. Companies are also developing fuel cell systems integrated with energy management solutions to provide optimized and reliable power.

Key Drivers, Barriers & Challenges in North America Fuel Cell Technology Industry

Key Drivers: Government support through subsidies and tax credits, growing environmental concerns, advancements in fuel cell technology leading to improved efficiency and cost reduction, increasing demand for clean energy, and strategic partnerships are all driving market expansion.

Key Challenges: High initial investment costs, limited hydrogen refueling infrastructure, lack of widespread public awareness and acceptance of fuel cell technology, and competition from other clean energy technologies (like battery electric vehicles) pose significant challenges. Supply chain disruptions for critical materials and skilled labor shortages are also impacting growth. Regulatory uncertainty in some regions adds to the complexity of market development.

Growth Drivers in the North America Fuel Cell Technology Industry Market

Technological advancements resulting in higher efficiency and lower costs, supportive government policies and regulations promoting clean energy, increasing demand for clean transportation solutions, and the expanding applications of fuel cells in various sectors contribute to the market growth. The increasing investment in research and development further accelerates innovation and market expansion.

Challenges Impacting North America Fuel Cell Technology Industry Growth

High initial capital costs, the limited availability of hydrogen refueling infrastructure, the lack of consumer awareness about fuel cell technology, intense competition from alternative energy technologies, and potential supply chain disruptions are significant hurdles. Regulatory uncertainties and the complexity of integrating fuel cell technology into existing energy systems pose additional challenges.

Key Players Shaping the North America Fuel Cell Technology Industry Market

- FuelCell Energy Inc

- Ballard Power Systems Inc

- Plug Power Inc

- Nuvera Fuel Cells LLC

- Horizon Fuel Cell Technologies Pte Ltd

- Hydrogenics Corporation

Significant North America Fuel Cell Technology Industry Industry Milestones

- September 2022: Loop Energy unveils a 120 kW fuel cell system with a 20% efficiency gain. This signifies advancements in fuel cell technology, potentially leading to wider adoption.

- August 2022: Bosch announces a USD 200 Million investment in its South Carolina fuel cell production facility, indicating increased confidence in the North American market and further expansion.

Future Outlook for North America Fuel Cell Technology Industry Market

The North American fuel cell technology market is poised for significant growth, driven by technological advancements, supportive government policies, and the increasing demand for clean energy solutions. Strategic investments in research and development, coupled with the expansion of hydrogen refueling infrastructure, are key catalysts for future market expansion. The continuous improvement in fuel cell efficiency and cost reduction will further drive market penetration across diverse applications, creating substantial opportunities for industry players and investors.

North America Fuel Cell Technology Industry Segmentation

-

1. Application

- 1.1. Portable

- 1.2. Stationary

- 1.3. Transportation

-

2. Fuel Cell Technology

- 2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 2.2. Solid Oxide Fuel Cell (SOFC)

- 2.3. Other Fuel Cell Technologies

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America Fuel Cell Technology Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Fuel Cell Technology Industry Regional Market Share

Geographic Coverage of North America Fuel Cell Technology Industry

North America Fuel Cell Technology Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Portable

- 5.1.2. Stationary

- 5.1.3. Transportation

- 5.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 5.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 5.2.2. Solid Oxide Fuel Cell (SOFC)

- 5.2.3. Other Fuel Cell Technologies

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fuel Cell Technology Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Portable

- 6.1.2. Stationary

- 6.1.3. Transportation

- 6.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 6.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 6.2.2. Solid Oxide Fuel Cell (SOFC)

- 6.2.3. Other Fuel Cell Technologies

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. United States North America Fuel Cell Technology Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Portable

- 7.1.2. Stationary

- 7.1.3. Transportation

- 7.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 7.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 7.2.2. Solid Oxide Fuel Cell (SOFC)

- 7.2.3. Other Fuel Cell Technologies

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Canada North America Fuel Cell Technology Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Portable

- 8.1.2. Stationary

- 8.1.3. Transportation

- 8.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 8.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 8.2.2. Solid Oxide Fuel Cell (SOFC)

- 8.2.3. Other Fuel Cell Technologies

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Rest of North America North America Fuel Cell Technology Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Portable

- 9.1.2. Stationary

- 9.1.3. Transportation

- 9.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 9.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 9.2.2. Solid Oxide Fuel Cell (SOFC)

- 9.2.3. Other Fuel Cell Technologies

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 FuelCell Energy Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Ballard Power Systems Inc

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Plug Power Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Nuvera Fuel Cells LLC*List Not Exhaustive

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Horizon Fuel Cell Technologies Pte Ltd

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Hydrogenics Corporation

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.1 FuelCell Energy Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Fuel Cell Technology Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Fuel Cell Technology Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Fuel Cell Technology Industry Revenue million Forecast, by Application 2020 & 2033

- Table 2: North America Fuel Cell Technology Industry Revenue million Forecast, by Fuel Cell Technology 2020 & 2033

- Table 3: North America Fuel Cell Technology Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 4: North America Fuel Cell Technology Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: North America Fuel Cell Technology Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: North America Fuel Cell Technology Industry Revenue million Forecast, by Fuel Cell Technology 2020 & 2033

- Table 7: North America Fuel Cell Technology Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 8: North America Fuel Cell Technology Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: North America Fuel Cell Technology Industry Revenue million Forecast, by Application 2020 & 2033

- Table 10: North America Fuel Cell Technology Industry Revenue million Forecast, by Fuel Cell Technology 2020 & 2033

- Table 11: North America Fuel Cell Technology Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 12: North America Fuel Cell Technology Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: North America Fuel Cell Technology Industry Revenue million Forecast, by Application 2020 & 2033

- Table 14: North America Fuel Cell Technology Industry Revenue million Forecast, by Fuel Cell Technology 2020 & 2033

- Table 15: North America Fuel Cell Technology Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 16: North America Fuel Cell Technology Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Fuel Cell Technology Industry?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the North America Fuel Cell Technology Industry?

Key companies in the market include FuelCell Energy Inc, Ballard Power Systems Inc, Plug Power Inc, Nuvera Fuel Cells LLC*List Not Exhaustive, Horizon Fuel Cell Technologies Pte Ltd, Hydrogenics Corporation.

3. What are the main segments of the North America Fuel Cell Technology Industry?

The market segments include Application, Fuel Cell Technology, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.8 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Falling Costs of Green And Blue Hydrogen Generation4.; Rising Demand from The Automotive Sector.

6. What are the notable trends driving market growth?

Polymer Electrolyte Membrane Fuel Cell (PEM) to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Competition for Alternative Energy Source.

8. Can you provide examples of recent developments in the market?

In September 2022, Loop Energy unveiled a 120 kW fuel cell system that reportedly provides an additional efficiency gain of 20% when it generates electricity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Fuel Cell Technology Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Fuel Cell Technology Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Fuel Cell Technology Industry?

To stay informed about further developments, trends, and reports in the North America Fuel Cell Technology Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence