Key Insights

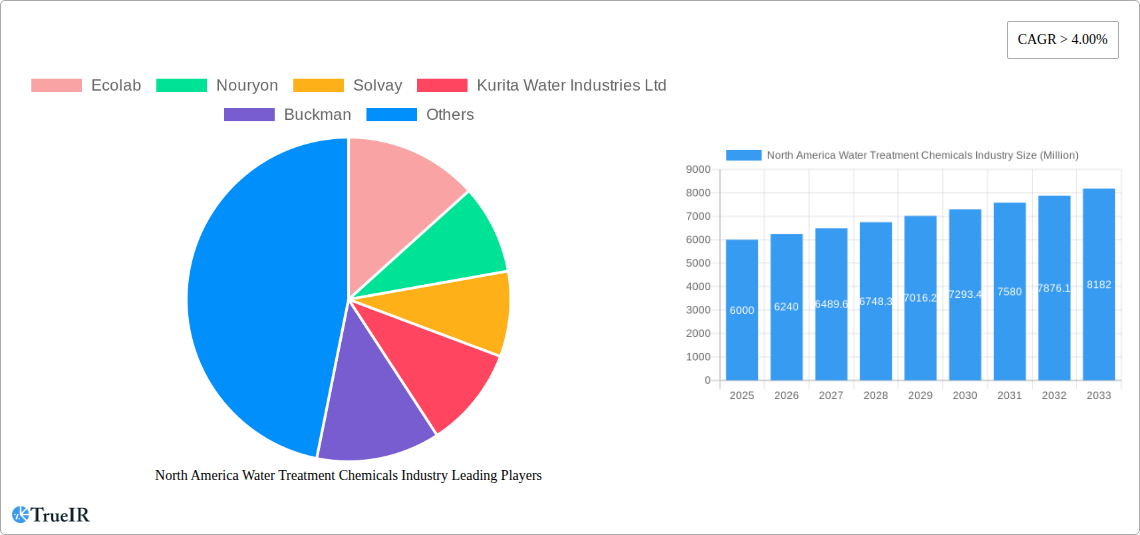

The North American water treatment chemicals market, valued at approximately $39.8 billion in the base year 2025, is projected to grow at a compound annual growth rate (CAGR) of 6.3% through 2033. This growth is propelled by increasing industrialization, urbanization, and stringent water quality regulations. Growing awareness of water scarcity and the imperative for sustainable water management also stimulate demand for efficient and eco-friendly chemical solutions. The market segments include biocides & disinfectants, coagulants & flocculants, and corrosion & scale inhibitors, serving end-user industries such as power, oil & gas, and chemical manufacturing. Established players like Ecolab, Nouryon, and Solvay define the competitive landscape, while opportunities exist for specialized firms focusing on innovation. The mature regulatory environment and robust infrastructure in North America make it an attractive market for water treatment chemical suppliers, with advancements in formulations and digital water management tools further supporting sustained growth.

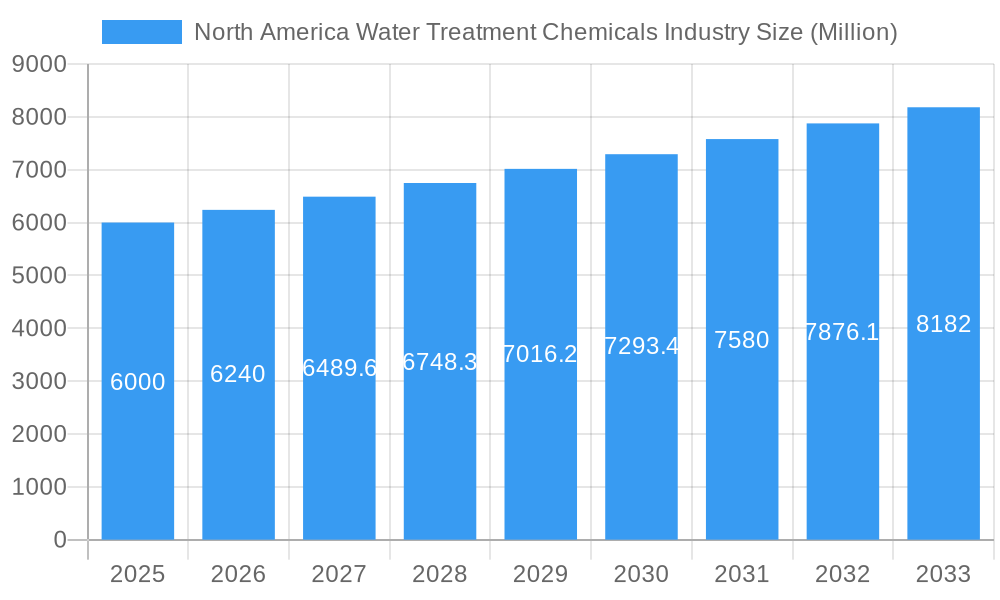

North America Water Treatment Chemicals Industry Market Size (In Billion)

Significant expansion in key end-user industries including power generation, oil & gas extraction, and food & beverage processing is a primary driver for the North American water treatment chemicals market. These sectors' substantial water requirements, coupled with strict regulatory compliance for water quality and effluent discharge, amplify demand. Rising environmental concerns and the need for optimized water usage further bolster this trend. Biocides & disinfectants, vital for addressing waterborne pathogens, and coagulants & flocculants, essential for effective water purification, are anticipated to exhibit the strongest growth. Despite challenges like raw material price volatility and potential economic slowdowns, the long-term market outlook remains positive, supported by ongoing development of innovative, environmentally friendly chemical solutions, supportive government policies, and increasing industrial activity.

North America Water Treatment Chemicals Industry Company Market Share

North America Water Treatment Chemicals Industry Market Report: 2019-2033

This comprehensive report delivers an in-depth analysis of the North America water treatment chemicals market, projecting robust growth from 2025 to 2033. Valued at $XX Million in 2025, the market is poised for significant expansion, driven by increasing industrialization, stringent environmental regulations, and growing demand for clean water across various sectors. This report provides crucial insights for industry stakeholders, including manufacturers, investors, and regulatory bodies.

North America Water Treatment Chemicals Industry Market Structure & Competitive Landscape

The North American water treatment chemicals market exhibits a moderately concentrated structure, with several multinational corporations holding significant market share. The Herfindahl-Hirschman Index (HHI) is estimated at XX, indicating a moderately consolidated market. Key players like Ecolab, Ecolab, Nouryon, Nouryon, Solvay, Solvay, and Kurita Water Industries Ltd. drive innovation through continuous product development and strategic acquisitions. Regulatory pressures, particularly concerning environmental compliance and chemical safety, significantly impact market dynamics. The market also witnesses competition from product substitutes, such as membrane filtration technologies, driving manufacturers to enhance product efficacy and cost-effectiveness.

- Market Concentration: HHI estimated at XX in 2025.

- Innovation Drivers: R&D investments in sustainable and high-performance chemicals.

- Regulatory Impacts: Stringent environmental regulations influencing product formulations and disposal methods.

- Product Substitutes: Membrane filtration systems and other advanced treatment technologies pose competitive pressure.

- End-User Segmentation: Diversification across power generation, industrial manufacturing, and municipal water treatment.

- M&A Trends: A moderate level of mergers and acquisitions activity aimed at expanding market reach and product portfolios; XX M&A deals recorded between 2019-2024.

North America Water Treatment Chemicals Industry Market Trends & Opportunities

The North America water treatment chemicals market is experiencing significant growth, driven by escalating demand from various end-user industries. The market size is estimated at $XX Million in 2025 and is projected to reach $XX Million by 2033, exhibiting a CAGR of XX% during the forecast period (2025-2033). This growth is fueled by several factors, including increasing industrial activities, stringent environmental regulations pushing for improved water quality, and rising consumer awareness regarding water scarcity and pollution. Technological advancements in water treatment techniques are leading to the development of more efficient and eco-friendly chemicals. Furthermore, changing consumer preferences towards sustainable and environmentally responsible products are creating new opportunities for manufacturers to introduce innovative, green solutions. The competitive landscape is characterized by both established players and new entrants, fostering innovation and driving market expansion. Market penetration rates vary across different segments, with the highest penetration observed in the power and industrial sectors.

Dominant Markets & Segments in North America Water Treatment Chemicals Industry

The municipal and power generation segments dominate the North American water treatment chemicals market, accounting for XX% and XX% of the total market value respectively in 2025. Within product types, biocides & disinfectants, coagulants & flocculants, and corrosion & scale inhibitors constitute the largest segments.

Leading Segments:

- End-user Industry: Municipal, Power.

- Product Type: Biocides & Disinfectants, Coagulants & Flocculants, Corrosion & Scale Inhibitors.

Key Growth Drivers:

- Municipal Segment: Increasing urbanization and stringent regulations mandating improved water quality.

- Power Segment: Growing electricity demand and emphasis on efficient cooling water treatment.

- Biocides & Disinfectants: Concerns over waterborne pathogens and need for effective disinfection.

- Coagulants & Flocculants: Expanding application in wastewater treatment to remove suspended solids.

- Corrosion & Scale Inhibitors: Preventative measures to maintain pipeline integrity and reduce operational costs.

North America Water Treatment Chemicals Industry Product Analysis

Technological advancements are driving the development of next-generation water treatment chemicals, emphasizing sustainability and enhanced performance. Bio-based and biodegradable products are gaining traction, along with advanced formulations providing improved efficacy at lower concentrations. This focus on efficiency and eco-friendliness directly addresses the market's growing demand for environmentally responsible solutions. The competitive advantage lies in offering superior performance, reduced environmental impact, and cost-effectiveness while adhering to stringent regulatory requirements.

Key Drivers, Barriers & Challenges in North America Water Treatment Chemicals Industry

Key Drivers:

Stringent environmental regulations, increasing industrial water usage, and rising awareness of water scarcity are major drivers. Advances in nanotechnology and biotechnology are also contributing to product innovation.

Challenges and Restraints:

Fluctuating raw material prices, stringent regulatory compliance requirements, and potential supply chain disruptions pose significant challenges. Competitive pressures also impact profitability, forcing manufacturers to focus on differentiation and cost optimization. The estimated impact of supply chain disruptions on market growth is approximately XX% in 2025.

Growth Drivers in the North America Water Treatment Chemicals Industry Market

Technological advancements, particularly in biocides and nanotechnology-based solutions, are driving market growth. Stringent environmental regulations are pushing for the adoption of sustainable and environmentally friendly products. Increased industrial activity and infrastructure development also contribute to demand expansion.

Challenges Impacting North America Water Treatment Chemicals Industry Growth

Regulatory complexities and compliance costs are significant barriers. Supply chain volatility and the price fluctuations of raw materials can impact profitability. Intense competition from both established players and new entrants creates price pressures.

Significant North America Water Treatment Chemicals Industry Industry Milestones

- 2020: Ecolab launched a new line of sustainable biocides.

- 2021: Nouryon acquired a smaller water treatment chemicals company, expanding its portfolio.

- 2022: New EPA regulations came into effect, impacting product formulations.

- 2023: Solvay invested heavily in R&D for next-generation water treatment technologies. (Note: Specific dates and details may need verification.)

Future Outlook for North America Water Treatment Chemicals Industry Market

The North American water treatment chemicals market is poised for continued growth, driven by a combination of factors, including increasing demand from various sectors, technological innovations focusing on sustainability, and stringent environmental regulations. Strategic partnerships and collaborations among industry players will be crucial for driving innovation and market expansion. The market is projected to witness substantial growth over the forecast period (2025-2033).

North America Water Treatment Chemicals Industry Segmentation

-

1. Product Type

- 1.1. Biocides & Disinfectants

- 1.2. Coagulants & Flocculants

- 1.3. Corrosion & Scale Inhibitors

- 1.4. Defoamers & Defoaming Agents

- 1.5. pH & Adjuster & Softener

- 1.6. Other Product Types

-

2. End-user Industry

- 2.1. Power

- 2.2. Oil & Gas

- 2.3. Chemical Manufacturing

- 2.4. Mining & Mineral Processing

- 2.5. Municipal

- 2.6. Food & Beverage

- 2.7. Pulp & Paper

- 2.8. Other End-user Industries

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Water Treatment Chemicals Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

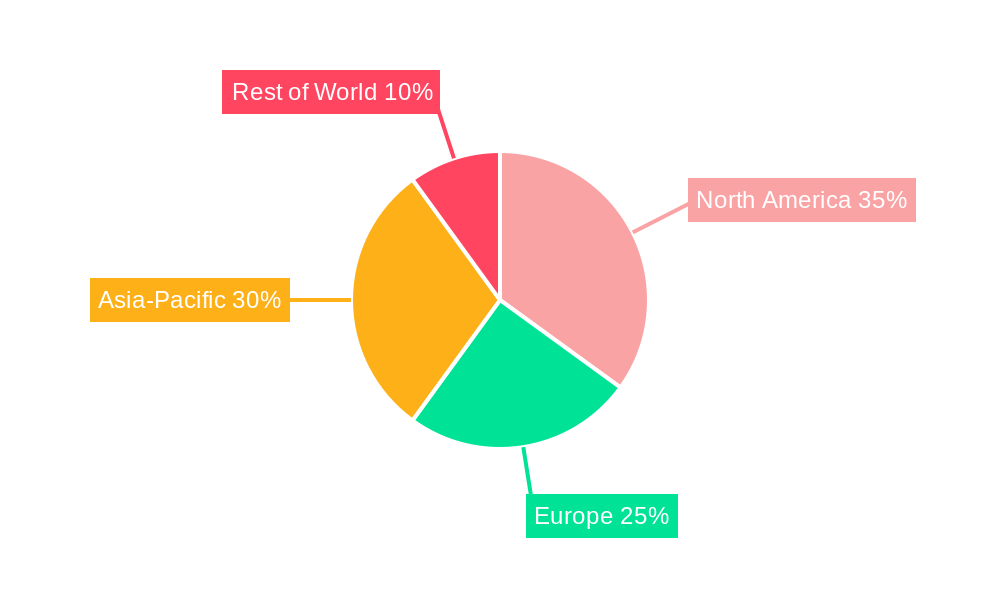

North America Water Treatment Chemicals Industry Regional Market Share

Geographic Coverage of North America Water Treatment Chemicals Industry

North America Water Treatment Chemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Biocides & Disinfectants

- 5.1.2. Coagulants & Flocculants

- 5.1.3. Corrosion & Scale Inhibitors

- 5.1.4. Defoamers & Defoaming Agents

- 5.1.5. pH & Adjuster & Softener

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Power

- 5.2.2. Oil & Gas

- 5.2.3. Chemical Manufacturing

- 5.2.4. Mining & Mineral Processing

- 5.2.5. Municipal

- 5.2.6. Food & Beverage

- 5.2.7. Pulp & Paper

- 5.2.8. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Biocides & Disinfectants

- 6.1.2. Coagulants & Flocculants

- 6.1.3. Corrosion & Scale Inhibitors

- 6.1.4. Defoamers & Defoaming Agents

- 6.1.5. pH & Adjuster & Softener

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Power

- 6.2.2. Oil & Gas

- 6.2.3. Chemical Manufacturing

- 6.2.4. Mining & Mineral Processing

- 6.2.5. Municipal

- 6.2.6. Food & Beverage

- 6.2.7. Pulp & Paper

- 6.2.8. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. United States North America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Biocides & Disinfectants

- 7.1.2. Coagulants & Flocculants

- 7.1.3. Corrosion & Scale Inhibitors

- 7.1.4. Defoamers & Defoaming Agents

- 7.1.5. pH & Adjuster & Softener

- 7.1.6. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Power

- 7.2.2. Oil & Gas

- 7.2.3. Chemical Manufacturing

- 7.2.4. Mining & Mineral Processing

- 7.2.5. Municipal

- 7.2.6. Food & Beverage

- 7.2.7. Pulp & Paper

- 7.2.8. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Canada North America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Biocides & Disinfectants

- 8.1.2. Coagulants & Flocculants

- 8.1.3. Corrosion & Scale Inhibitors

- 8.1.4. Defoamers & Defoaming Agents

- 8.1.5. pH & Adjuster & Softener

- 8.1.6. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Power

- 8.2.2. Oil & Gas

- 8.2.3. Chemical Manufacturing

- 8.2.4. Mining & Mineral Processing

- 8.2.5. Municipal

- 8.2.6. Food & Beverage

- 8.2.7. Pulp & Paper

- 8.2.8. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Mexico North America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Biocides & Disinfectants

- 9.1.2. Coagulants & Flocculants

- 9.1.3. Corrosion & Scale Inhibitors

- 9.1.4. Defoamers & Defoaming Agents

- 9.1.5. pH & Adjuster & Softener

- 9.1.6. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Power

- 9.2.2. Oil & Gas

- 9.2.3. Chemical Manufacturing

- 9.2.4. Mining & Mineral Processing

- 9.2.5. Municipal

- 9.2.6. Food & Beverage

- 9.2.7. Pulp & Paper

- 9.2.8. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Ecolab

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Nouryon

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Solvay

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Kurita Water Industries Ltd

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Buckman

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Italmatch Chemicals SpA

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 SUEZ

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Kemira

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Dow

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 ChemTreat Inc

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Solenis

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Albemarle Corporation

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 Veolia Water Technologies

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.1 Ecolab

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Water Treatment Chemicals Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Water Treatment Chemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: North America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 5: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 7: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 10: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 11: North America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 13: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 15: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 19: North America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 21: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 23: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 26: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 27: North America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 29: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 30: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 31: North America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: North America Water Treatment Chemicals Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Water Treatment Chemicals Industry?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the North America Water Treatment Chemicals Industry?

Key companies in the market include Ecolab, Nouryon, Solvay, Kurita Water Industries Ltd, Buckman, Italmatch Chemicals SpA, SUEZ, Kemira, Dow, ChemTreat Inc, Solenis, Albemarle Corporation, Veolia Water Technologies.

3. What are the main segments of the North America Water Treatment Chemicals Industry?

The market segments include Product Type, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.3 billion as of 2022.

5. What are some drivers contributing to market growth?

; Stringent Regulatory Requirements to Control the Wastewater Disposal from both Municipal and Industrial sources; Growing Demand from the Power Industry.

6. What are the notable trends driving market growth?

Municipal Segment to Dominate the Market Demand.

7. Are there any restraints impacting market growth?

; Increasing Popularity for Chlorine Alternatives for Cooling Water Treatment Serves as one of the Stumbling Blocks in the Growth of the Market Studied.; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3,950, USD 4,950, and USD 6,950 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Water Treatment Chemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Water Treatment Chemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Water Treatment Chemicals Industry?

To stay informed about further developments, trends, and reports in the North America Water Treatment Chemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence