Key Insights

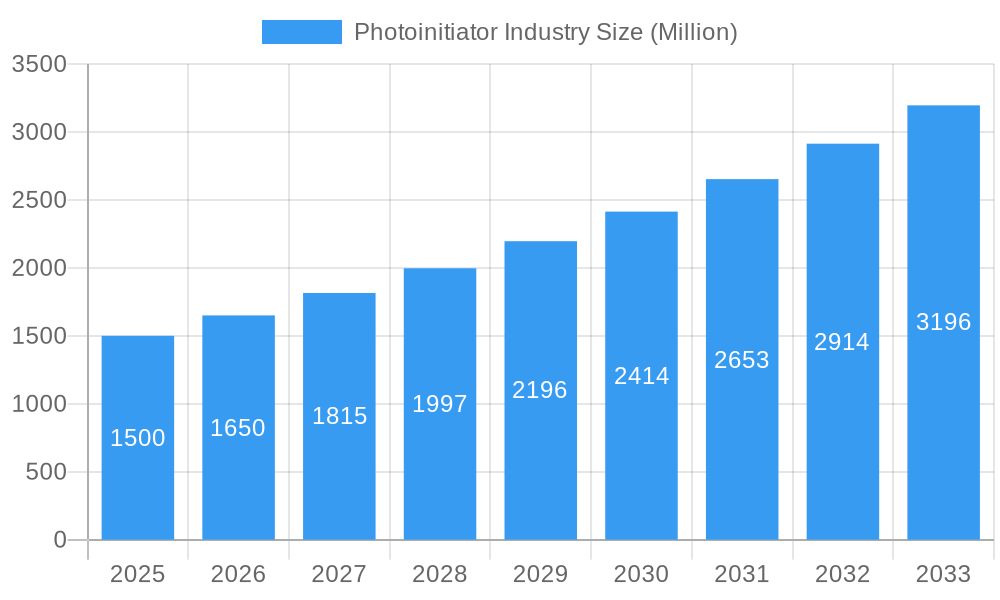

The photoinitiator market, valued at approximately $XX million in 2025, is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 10% from 2025 to 2033. This expansion is driven by several key factors. The increasing demand for high-performance adhesives, inks, and coatings across diverse industries like packaging, electronics, and construction fuels market growth. Advancements in photoinitiator technology, focusing on improved efficiency, reduced toxicity, and enhanced UV curing capabilities, further contribute to market expansion. The shift towards sustainable and environmentally friendly materials is also impacting the market, with manufacturers focusing on developing bio-based and less hazardous photoinitiators. While regulatory changes regarding the use of certain chemicals pose a potential restraint, the overall market outlook remains positive due to the continued growth of end-use industries and ongoing technological innovations.

Photoinitiator Industry Market Size (In Billion)

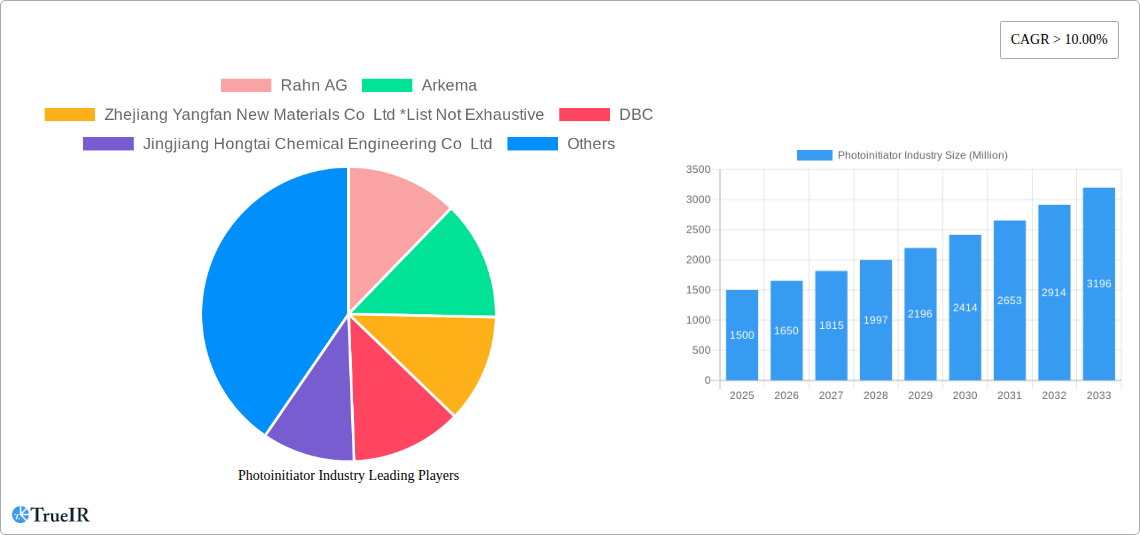

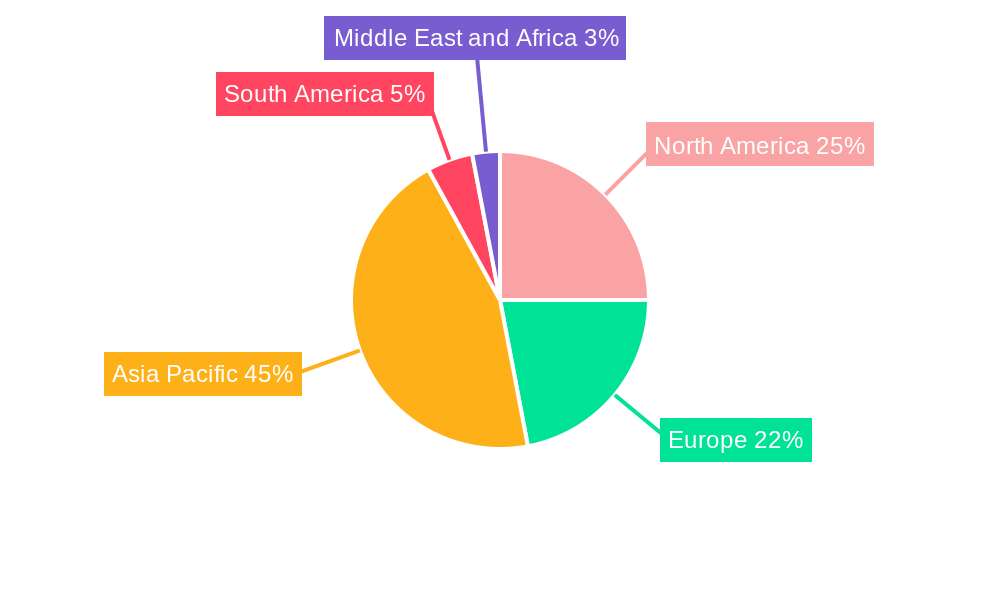

Segmentation analysis reveals a dynamic market landscape. Free radical photoinitiators currently dominate the market due to their widespread applications and cost-effectiveness. However, cationic photoinitiators are experiencing significant growth owing to their ability to cure specific polymers and their use in niche applications. Geographically, the Asia-Pacific region, particularly China and India, represents a major market due to its burgeoning manufacturing sectors and increasing demand for coatings and adhesives. North America and Europe also maintain significant market shares, driven by established industries and stringent regulatory compliance. Key players like Rahn AG, Arkema, and several prominent Asian manufacturers are actively shaping the market through product innovation, strategic partnerships, and geographical expansion. The competitive landscape is characterized by a mix of established global players and regional manufacturers, leading to intense competition and continuous product development.

Photoinitiator Industry Company Market Share

Dynamic Photoinitiator Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the global photoinitiator market, offering invaluable insights for stakeholders across the value chain. From market size and segmentation to competitive dynamics and future trends, this report equips you with the knowledge to navigate this dynamic industry and make informed strategic decisions. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

Photoinitiator Industry Market Structure & Competitive Landscape

The global photoinitiator market is characterized by a moderately concentrated structure, with a few major players holding significant market share. However, the presence of numerous smaller companies and regional players fosters a competitive landscape driven by innovation and product differentiation. The market concentration ratio (CR4) is estimated at xx%, indicating a moderately consolidated market. Mergers and acquisitions (M&A) activity has been notable, particularly in the recent past. For instance, the xx Million acquisition of Litian by IGM Resins in July 2022 significantly reshaped the competitive dynamics within the energy-curing resins segment. The total M&A volume in the photoinitiator industry during the historical period (2019-2024) was approximately xx Million.

- Key Market Segments: The market is segmented by type (Free Radical, Cationic) and application (Adhesives, Ink, Coatings, Other Applications). The Free Radical segment currently holds the largest market share, driven by its widespread use in various applications.

- Innovation Drivers: Continuous research and development efforts focus on enhancing the efficiency, photoreactivity, and sustainability of photoinitiators, particularly in line with stricter environmental regulations.

- Regulatory Impacts: Stringent environmental regulations regarding volatile organic compounds (VOCs) and hazardous substances are driving the demand for eco-friendly photoinitiators.

- Product Substitutes: While some alternatives exist, the unique properties of photoinitiators, particularly in curing processes, limit the availability of effective substitutes.

- End-User Segmentation: The key end-use industries include printing inks, coatings, adhesives, and 3D printing, each with specific demands and preferences.

- M&A Trends: Consolidation is expected to continue, driven by the need for enhanced scale, technological capabilities, and geographical reach. Strategic acquisitions are likely to accelerate innovation and market penetration.

Photoinitiator Industry Market Trends & Opportunities

The global photoinitiator market is experiencing robust growth, fueled by increasing demand across various end-use sectors. The market size is projected to reach xx Million by 2033, driven by several key factors. Technological advancements, especially in energy-curing technologies like UV and EB curing, are boosting the adoption of photoinitiators in various applications. The rising demand for high-performance, eco-friendly materials in packaging, coatings, and adhesives is a key growth driver. Consumer preference for sustainable and environmentally friendly products is also influencing the demand for photoinitiators that meet these criteria. The competitive dynamics are characterized by continuous innovation and product differentiation strategies. Key players are investing heavily in R&D to develop novel photoinitiators with improved performance characteristics and sustainability profiles. The market penetration rate is projected to increase from xx% in 2025 to xx% by 2033.

Dominant Markets & Segments in Photoinitiator Industry

The Asia-Pacific region is currently the dominant market for photoinitiators, driven by robust economic growth, expanding manufacturing sectors, and increasing infrastructure development. China and India are particularly significant contributors. Within the type segment, Free Radical photoinitiators dominate, fueled by their versatility and cost-effectiveness. The coatings segment accounts for a significant portion of the market, driven by growing demand for high-performance coatings in various applications.

- Key Growth Drivers in Asia-Pacific:

- Rapid industrialization and urbanization.

- Growing demand for high-quality coatings and adhesives.

- Increasing investments in infrastructure projects.

- Favorable government policies promoting industrial growth.

- Dominant Segment Analysis: The Free Radical segment's dominance stems from its compatibility with various curing methods and its cost-effectiveness compared to Cationic photoinitiators. The Coatings application segment's strong performance reflects the widespread use of photoinitiators in diverse coating applications, including automotive, wood, and industrial coatings.

Photoinitiator Industry Product Analysis

Photoinitiator product innovation focuses on enhanced performance characteristics, including improved efficiency, reactivity, and curing speed. Manufacturers are developing specialized photoinitiators for specific applications, addressing unique needs in terms of viscosity, color, and other properties. The competitive advantage lies in developing high-performance, eco-friendly products with superior cost-effectiveness and efficient curing capabilities. Advances in formulations, focusing on lower VOC content and reduced toxicity, are also crucial.

Key Drivers, Barriers & Challenges in Photoinitiator Industry

Key Drivers: The increasing demand for high-performance coatings, inks, and adhesives across diverse industries is the primary driver. Technological advancements in UV and EB curing technologies are also significantly boosting market growth. Furthermore, stringent environmental regulations favoring eco-friendly alternatives are fueling innovation and market expansion.

Key Challenges: Supply chain disruptions, particularly in the sourcing of raw materials, pose a significant challenge. The volatility of raw material prices also impacts profitability. Intense competition among established players and new entrants creates pricing pressure. Finally, evolving environmental regulations require continuous adaptation and investment in R&D for compliant products. These challenges could collectively limit market growth by an estimated xx% by 2033 if not effectively addressed.

Growth Drivers in the Photoinitiator Industry Market

The primary growth drivers include the expanding applications of UV and EB curing technologies in various industries, the increasing demand for high-performance and eco-friendly coatings and adhesives, and the supportive government regulations encouraging sustainable material usage. The rising investments in R&D for developing advanced photoinitiators with improved efficiency and sustainability are also significant contributors.

Challenges Impacting Photoinitiator Industry Growth

Key challenges include fluctuating raw material prices, stringent environmental regulations, intense competition, and potential supply chain disruptions. These factors can impact the overall market growth, particularly affecting pricing strategies and the availability of key components.

Key Players Shaping the Photoinitiator Industry Market

- Rahn AG

- Arkema

- Zhejiang Yangfan New Materials Co Ltd

- DBC

- Jingjiang Hongtai Chemical Engineering Co Ltd

- Eutec

- Changzhou Tronly New Electronic Materials Co Ltd

- TCI Chemicals

- ADEKA Corporation

- Lambson

- Jiuri Chemical

- Environ Speciality Chemicals Ltd

- New Sun Poly Tec Co Ltd

- Tianjin Jiuri New Materials Co Ltd

- Polynaisse

- IGM Resins

Significant Photoinitiator Industry Milestones

- July 2022: IGM Resins acquired Litian, expanding its product portfolio significantly.

- May 2022: Arkema showcased sustainable solutions at RadTech UV+EB 2022, highlighting innovation in energy-cured materials.

Future Outlook for Photoinitiator Industry Market

The future of the photoinitiator market appears bright, driven by continuous innovation, expanding applications, and growing demand for sustainable solutions. Strategic investments in R&D and partnerships will be crucial for sustained growth. The market is expected to experience significant expansion, particularly in emerging economies with robust industrial growth and infrastructure development. The development and adoption of increasingly sustainable photoinitiator technologies will further accelerate market expansion in the coming years.

Photoinitiator Industry Segmentation

-

1. Type

- 1.1. Free Radical

- 1.2. Cationic

-

2. Application

- 2.1. Adhesives

- 2.2. Ink

- 2.3. Coating

- 2.4. Other Applications

Photoinitiator Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Photoinitiator Industry Regional Market Share

Geographic Coverage of Photoinitiator Industry

Photoinitiator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 10.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Free Radical

- 5.1.2. Cationic

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Adhesives

- 5.2.2. Ink

- 5.2.3. Coating

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Photoinitiator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Free Radical

- 6.1.2. Cationic

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Adhesives

- 6.2.2. Ink

- 6.2.3. Coating

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Photoinitiator Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Free Radical

- 7.1.2. Cationic

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Adhesives

- 7.2.2. Ink

- 7.2.3. Coating

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America Photoinitiator Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Free Radical

- 8.1.2. Cationic

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Adhesives

- 8.2.2. Ink

- 8.2.3. Coating

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Photoinitiator Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Free Radical

- 9.1.2. Cationic

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Adhesives

- 9.2.2. Ink

- 9.2.3. Coating

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Photoinitiator Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Free Radical

- 10.1.2. Cationic

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Adhesives

- 10.2.2. Ink

- 10.2.3. Coating

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Photoinitiator Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Free Radical

- 11.1.2. Cationic

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Adhesives

- 11.2.2. Ink

- 11.2.3. Coating

- 11.2.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Rahn AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arkema

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zhejiang Yangfan New Materials Co Ltd *List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DBC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Jingjiang Hongtai Chemical Engineering Co Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Eutec

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Changzhou Tronly New Electronic Materials Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 TCI Chemicals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ADEKA Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Lambson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Jiuri Chemical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Environ Speciality Chemicals Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 New Sun Poly Tec Co Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Tianjin Jiuri New Materials Co Ltd

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Polynaisse

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 IGM Resins

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Rahn AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Photoinitiator Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Photoinitiator Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: Asia Pacific Photoinitiator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Photoinitiator Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: Asia Pacific Photoinitiator Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Photoinitiator Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: Asia Pacific Photoinitiator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Photoinitiator Industry Revenue (Million), by Type 2025 & 2033

- Figure 9: North America Photoinitiator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Photoinitiator Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: North America Photoinitiator Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: North America Photoinitiator Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America Photoinitiator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Photoinitiator Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Europe Photoinitiator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Photoinitiator Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: Europe Photoinitiator Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Photoinitiator Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Photoinitiator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Photoinitiator Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: South America Photoinitiator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Photoinitiator Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: South America Photoinitiator Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Photoinitiator Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Photoinitiator Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Photoinitiator Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East and Africa Photoinitiator Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Photoinitiator Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Photoinitiator Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Photoinitiator Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Photoinitiator Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Photoinitiator Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Photoinitiator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: China Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: India Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Japan Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: South Korea Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 13: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Photoinitiator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United States Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Mexico Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 19: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Photoinitiator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Germany Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: France Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Italy Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Spain Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Europe Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 28: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 29: Global Photoinitiator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Brazil Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Argentina Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of South America Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Global Photoinitiator Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Photoinitiator Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 35: Global Photoinitiator Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: South Africa Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Saudi Arabia Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Photoinitiator Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photoinitiator Industry?

The projected CAGR is approximately > 10.00%.

2. Which companies are prominent players in the Photoinitiator Industry?

Key companies in the market include Rahn AG, Arkema, Zhejiang Yangfan New Materials Co Ltd *List Not Exhaustive, DBC, Jingjiang Hongtai Chemical Engineering Co Ltd, Eutec, Changzhou Tronly New Electronic Materials Co Ltd, TCI Chemicals, ADEKA Corporation, Lambson, Jiuri Chemical, Environ Speciality Chemicals Ltd, New Sun Poly Tec Co Ltd, Tianjin Jiuri New Materials Co Ltd, Polynaisse, IGM Resins.

3. What are the main segments of the Photoinitiator Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Promising Growth in End-use Industries such as Adhesive. Coating. Ink. and Paint; Eco-friendly Alternatives for Volatile Organic Compounds (VOCs).

6. What are the notable trends driving market growth?

Coatings Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Safety Concerns and Highest Costs; Other Restriants.

8. Can you provide examples of recent developments in the market?

July 2022: IGM Resins acquired Litian, a Chinese manufacturer of energy-curing resins. After the acquisition, IGM now includes three distinct product lines, a wide range of photoinitiators, a strong offering of energy-curing resins, and a good selection of additives.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photoinitiator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photoinitiator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photoinitiator Industry?

To stay informed about further developments, trends, and reports in the Photoinitiator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence