Key Insights

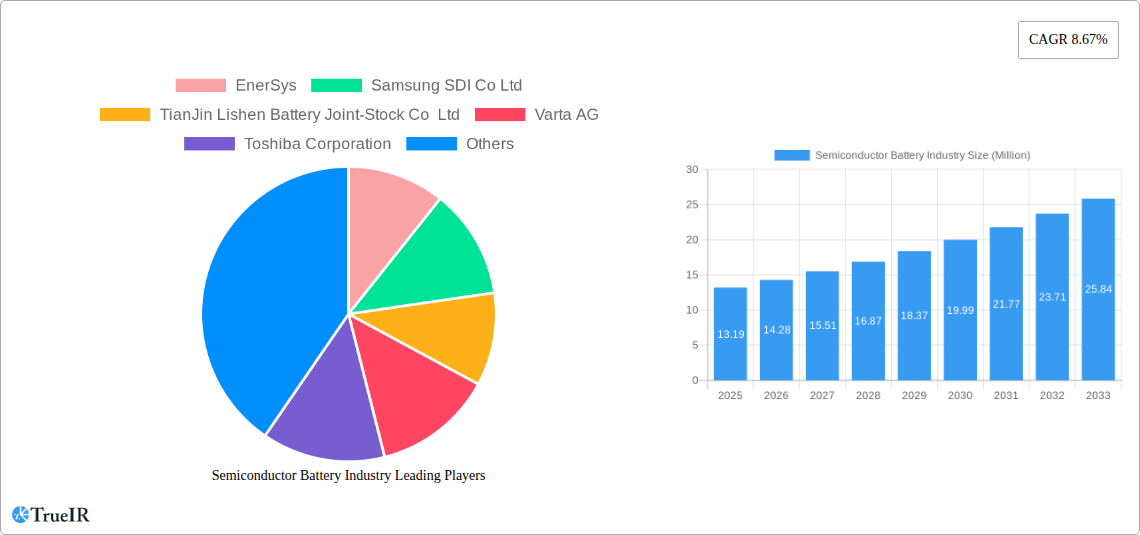

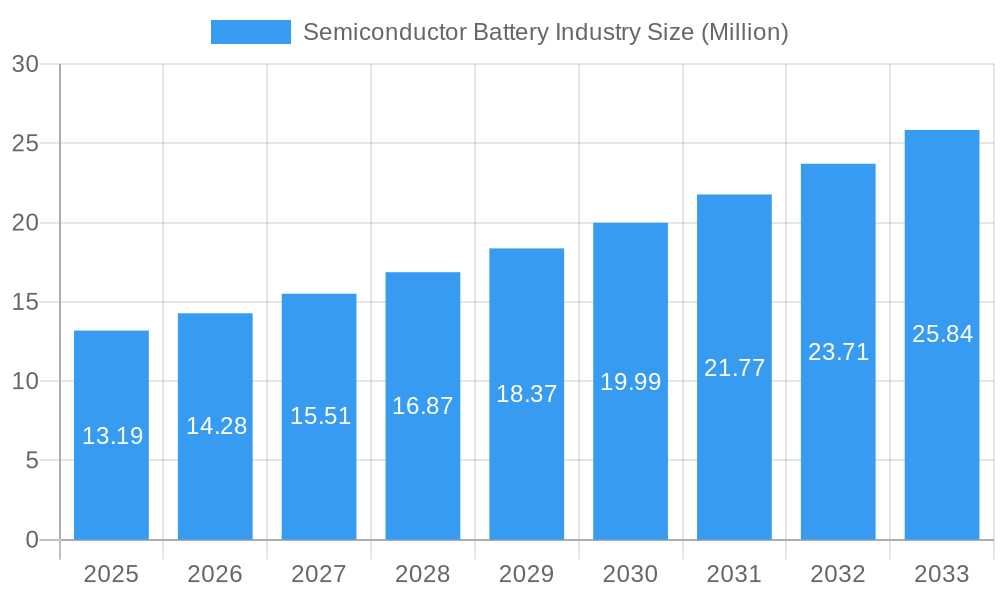

The global Semiconductor Battery market is poised for substantial growth, projected to reach $13.19 million with a robust Compound Annual Growth Rate (CAGR) of 8.67% from 2025 to 2033. This expansion is primarily fueled by the insatiable demand from the consumer electronics sector, where advanced battery technologies are critical for powering everything from smartphones and wearables to laptops and gaming devices. Furthermore, the burgeoning electric vehicle (EV) market represents a significant growth catalyst, with increasing consumer adoption and government incentives driving the need for high-performance, long-lasting batteries. Energy storage systems, crucial for renewable energy integration and grid stability, also contribute significantly to this market's upward trajectory. Emerging trends like the development of next-generation battery chemistries such as Sodium-Ion batteries, offering cost-effectiveness and sustainability advantages, are expected to further shape the market landscape. Innovations in battery management systems and enhanced safety features are also key drivers, addressing consumer concerns and enabling wider application.

Semiconductor Battery Industry Market Size (In Million)

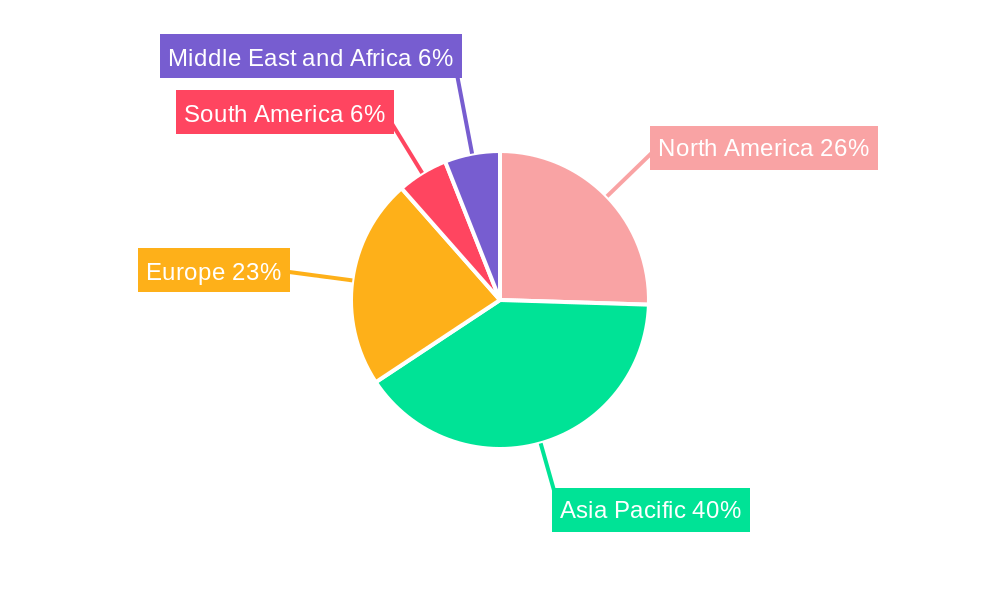

While the market is characterized by strong growth, certain restraints could influence the pace of expansion. These include the fluctuating raw material costs, particularly for lithium, and the complexities associated with battery recycling and disposal, which pose environmental and economic challenges. The high initial investment required for advanced manufacturing facilities and ongoing research and development also presents a barrier to entry for smaller players. Geographically, the Asia Pacific region, led by China, is anticipated to dominate the market due to its established manufacturing capabilities and a substantial consumer base for electronics and EVs. North America and Europe are also key markets, driven by technological advancements and supportive government policies for sustainable energy solutions. The competitive landscape features established players like Samsung SDI, Panasonic, and Sony, alongside emerging innovators focusing on new battery chemistries and sustainable manufacturing processes.

Semiconductor Battery Industry Company Market Share

Unlocking the Future: A Comprehensive Report on the Semiconductor Battery Industry (2019–2033)

This in-depth report provides a critical analysis of the global Semiconductor Battery Industry, encompassing market dynamics, technological advancements, and future projections from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study offers actionable insights into the evolving landscape of semiconductor-powered battery technologies. Leverage high-volume keywords such as "semiconductor battery market," "advanced battery technology," "lithium-ion battery innovations," "electric vehicle batteries," and "energy storage solutions" to enhance search visibility and engage a broad industry audience. This report is meticulously crafted for immediate use without requiring any further modifications.

Semiconductor Battery Industry Market Structure & Competitive Landscape

The Semiconductor Battery Industry is characterized by a moderately concentrated market structure, driven by significant R&D investments and the presence of well-established players. Innovation is a paramount driver, with continuous advancements in material science and manufacturing processes pushing the boundaries of energy density, charging speed, and safety. Regulatory impacts, particularly concerning environmental standards and safety protocols for advanced battery chemistries, play a crucial role in shaping market entry and product development. Product substitutes, such as conventional battery technologies and alternative energy sources, exist but are increasingly challenged by the superior performance and specialized applications of semiconductor batteries. End-user segmentation is diverse, with strong demand from consumer electronics, electric vehicles (EVs), and energy storage systems (ESS). Mergers and acquisitions (M&A) are prevalent, driven by the pursuit of technological superiority, market share expansion, and vertical integration. For instance, in the historical period, M&A volumes are estimated to have reached approximately $500 Million, signifying strategic consolidation. Key competitive factors include intellectual property, cost-effectiveness, supply chain robustness, and the ability to scale production. The industry's competitive landscape is shaped by the constant race for breakthroughs in battery performance and the development of next-generation semiconductor materials for enhanced battery functionality.

Semiconductor Battery Industry Market Trends & Opportunities

The global Semiconductor Battery Industry is poised for substantial growth, driven by escalating demand for high-performance energy storage solutions across a multitude of applications. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 15% during the forecast period, reaching an estimated value of over $100 Billion by 2033. Technological shifts are at the forefront of this expansion, with continuous innovation in material science and manufacturing leading to batteries with higher energy densities, faster charging capabilities, extended lifecycles, and enhanced safety features. The integration of semiconductor components within battery management systems (BMS) is becoming increasingly sophisticated, enabling smarter and more efficient energy utilization. Consumer preferences are evolving, with a growing demand for compact, lightweight, and long-lasting power sources for portable devices and a strong inclination towards sustainable energy solutions. This trend is particularly evident in the electric vehicle sector, where battery performance directly influences vehicle range and charging convenience. Competitive dynamics are intensifying as new entrants and established players alike invest heavily in research and development to secure a leading position. Key opportunities lie in the development of solid-state semiconductor batteries, which promise superior safety and energy density compared to traditional lithium-ion chemistries. Furthermore, the burgeoning market for Internet of Things (IoT) devices, wearable technology, and advanced medical devices presents significant growth avenues for miniaturized and high-efficiency semiconductor batteries. The increasing global focus on decarbonization and renewable energy integration also fuels demand for advanced energy storage systems, creating a substantial market for grid-scale and residential semiconductor battery solutions. The market penetration rates for semiconductor batteries in consumer electronics are already high, exceeding 80%, while the EV sector is experiencing rapid adoption with penetration rates projected to reach over 60% by 2033. The development of cost-effective manufacturing processes and robust supply chains will be critical to capitalize on these expanding market opportunities.

Dominant Markets & Segments in Semiconductor Battery Industry

The Semiconductor Battery Industry is witnessing dominant growth in several key regions and segments, driven by specific market dynamics and policy support.

Leading Region: Asia-Pacific

- This region, particularly China, South Korea, and Japan, holds a dominant position due to its robust manufacturing infrastructure, significant investments in battery R&D, and the presence of major players in both semiconductor and battery manufacturing.

- Government initiatives promoting electric vehicle adoption and renewable energy deployment are key growth drivers. For example, China's ambitious EV production targets and supportive policies have propelled demand for advanced battery technologies.

- The concentration of consumer electronics manufacturing also contributes significantly to regional market dominance.

Dominant Segment by Type: Lithium-Ion Battery

- Lithium-ion batteries continue to be the workhorse of the semiconductor battery market, benefiting from decades of technological refinement and economies of scale.

- Innovations in cathode and anode materials, as well as electrolyte formulations, are constantly enhancing their performance for a wide range of applications.

- The cost-competitiveness and proven reliability of lithium-ion batteries make them the preferred choice for electric vehicles and portable electronics.

Dominant Segment by End-User Application: Electric Vehicles (EVs)

- The electric vehicle sector represents the most significant growth driver for the semiconductor battery industry.

- The increasing global push towards sustainable transportation, coupled with declining battery costs and improving EV performance, is accelerating adoption rates.

- Key growth drivers include supportive government policies, expanding charging infrastructure, and growing consumer awareness regarding environmental benefits.

- The demand for higher energy density and faster charging solutions in EVs directly translates to a need for advanced semiconductor battery technologies.

Emerging Segment: Sodium-Ion Battery

- While currently a smaller segment, sodium-ion batteries are gaining traction due to the abundance and low cost of sodium, presenting a promising alternative for grid-scale energy storage and certain EV applications, especially where cost is a primary concern.

- Technological advancements are steadily improving their performance and energy density, making them a viable contender for future market share.

Semiconductor Battery Industry Product Analysis

Product innovations in the semiconductor battery industry are primarily focused on enhancing energy density, improving charge/discharge rates, extending cycle life, and ensuring superior safety. The integration of advanced semiconductor materials, such as silicon-based anodes and solid-state electrolytes, is leading to batteries that are lighter, more powerful, and inherently safer than their predecessors. These advancements unlock new application possibilities, from ultra-long-lasting consumer electronics to high-performance electric vehicles and robust grid-scale energy storage systems. Competitive advantages stem from proprietary material formulations, optimized battery management system (BMS) designs leveraging embedded semiconductors, and highly efficient manufacturing processes that reduce costs and environmental impact.

Key Drivers, Barriers & Challenges in Semiconductor Battery Industry

Key Drivers:

- Technological Advancements: Continuous innovation in materials science and semiconductor technology drives higher energy density, faster charging, and improved safety in semiconductor batteries. This includes breakthroughs in solid-state electrolytes and advanced anode materials.

- Growing Demand for Electric Vehicles (EVs): The global shift towards sustainable transportation is a major catalyst, necessitating high-performance and long-lasting EV batteries.

- Expansion of Energy Storage Systems (ESS): The increasing integration of renewable energy sources requires reliable and efficient battery storage solutions, bolstering demand for semiconductor batteries.

- Miniaturization in Consumer Electronics: The demand for smaller, lighter, and more powerful devices in the consumer electronics sector fuels innovation in compact semiconductor battery designs.

Barriers & Challenges:

- High Manufacturing Costs: The sophisticated processes and specialized materials required for semiconductor battery production can lead to higher initial costs compared to conventional batteries. For instance, the cost per kWh can be up to 20% higher for nascent technologies.

- Supply Chain Volatility: Reliance on rare earth elements and specific semiconductor materials can lead to supply chain disruptions and price fluctuations, impacting production and cost-effectiveness.

- Regulatory Hurdles and Safety Standards: Evolving and stringent safety regulations for advanced battery chemistries require significant investment in R&D and compliance.

- Competitive Landscape: Intense competition from established battery technologies and the rapid pace of innovation necessitate continuous investment to maintain market position.

- Scalability of Production: Transitioning from laboratory-scale development to mass production of advanced semiconductor battery technologies can be challenging, impacting widespread adoption.

Growth Drivers in the Semiconductor Battery Industry Market

The semiconductor battery industry's growth is propelled by a confluence of technological, economic, and policy-driven factors. Technologically, relentless advancements in materials science are unlocking higher energy densities and faster charging capabilities, making semiconductor batteries indispensable for next-generation applications. Economically, the declining cost of manufacturing and the increasing demand from burgeoning sectors like electric vehicles and renewable energy storage are creating significant market opportunities. Policy support, particularly from governments worldwide advocating for decarbonization and the adoption of clean energy solutions, provides a robust framework for sustained growth. For example, subsidies for EV purchases and mandates for renewable energy integration directly translate into increased demand for advanced battery technologies. The increasing proliferation of smart devices and the Internet of Things (IoT) also drives the need for compact, efficient, and long-lasting power sources.

Challenges Impacting Semiconductor Battery Industry Growth

Despite its promising trajectory, the semiconductor battery industry faces several significant barriers to sustained growth. The high capital expenditure required for advanced manufacturing facilities and the complex supply chains for critical raw materials pose substantial economic challenges, often leading to higher per-unit costs compared to established battery technologies. Regulatory complexities surrounding the safe disposal and recycling of advanced battery components, coupled with evolving international standards, can create development delays and compliance burdens. Competitive pressures are fierce, with established battery manufacturers constantly innovating and traditional technologies offering lower initial costs. Furthermore, ensuring the scalability of cutting-edge semiconductor battery production to meet the rapidly increasing global demand for EVs and energy storage systems remains a critical hurdle. Supply chain disruptions, exacerbated by geopolitical factors and limited sourcing options for specialized materials, can impact production volumes and cost stability.

Key Players Shaping the Semiconductor Battery Industry Market

- EnerSys

- Samsung SDI Co Ltd

- TianJin Lishen Battery Joint-Stock Co Ltd

- Varta AG

- Toshiba Corporation

- Faradion Limited

- GS Yuasa Corporation

- Routejade

- Panasonic Corporation

- Sony Corporation

Significant Semiconductor Battery Industry Industry Milestones

- February 2022: ROHM Semiconductor announced the development of a new evaluation board for ultra-efficient semiconductor battery operations, specifically designed for newly developed Internet of Things (IoT) devices, named REFLVBMS001-EVK-001. This development signifies a push towards more efficient power management in smaller electronic devices.

- February 2022: Solus Advanced Material announced its strategic decision to diversify its business operations by establishing overseer production facilities for developing semiconductor batteries and battery foils. The company anticipated a significant increase in sales by the end of 2026, highlighting confidence in the market's growth potential and a strategic move towards capturing market share in this emerging sector.

Future Outlook for Semiconductor Battery Industry Market

The future outlook for the Semiconductor Battery Industry is exceptionally bright, driven by escalating demand for sustainable energy solutions and advanced portable electronics. Strategic opportunities lie in the widespread adoption of solid-state semiconductor batteries, which promise a step-change in safety and energy density, making them ideal for next-generation electric vehicles and aerospace applications. The continued miniaturization of electronic devices will fuel demand for highly efficient and compact semiconductor battery solutions. Furthermore, the expansion of smart grids and the integration of renewable energy sources will create substantial market potential for large-scale energy storage systems powered by advanced semiconductor battery technology. The industry is poised for continued innovation, cost reduction through advanced manufacturing techniques, and significant market penetration across various end-user applications, solidifying its role as a cornerstone of the global energy transition and technological advancement.

Semiconductor Battery Industry Segmentation

-

1. Type

- 1.1. Lithium-Ion

- 1.2. Nickel-Metal Hydride

- 1.3. Lithium-Ion Polymer

- 1.4. Sodium-Ion Battery

-

2. End-User Application

- 2.1. Consumer Electronics

- 2.2. Electric Vehicles

- 2.3. Energy Storage System

- 2.4. Other End-User Applications

Semiconductor Battery Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Asia Pacific

- 2.1. China

- 2.2. India

- 2.3. Japan

- 2.4. South Korea

- 2.5. Rest of Asia Pacific

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Chile

- 4.2. Brazil

- 4.3. Argentina

- 4.4. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. United Arab Emirates

- 5.3. South Africa

- 5.4. Egypt

- 5.5. Rest of Middle East and Africa

Semiconductor Battery Industry Regional Market Share

Geographic Coverage of Semiconductor Battery Industry

Semiconductor Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lithium-Ion

- 5.1.2. Nickel-Metal Hydride

- 5.1.3. Lithium-Ion Polymer

- 5.1.4. Sodium-Ion Battery

- 5.2. Market Analysis, Insights and Forecast - by End-User Application

- 5.2.1. Consumer Electronics

- 5.2.2. Electric Vehicles

- 5.2.3. Energy Storage System

- 5.2.4. Other End-User Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Semiconductor Battery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Lithium-Ion

- 6.1.2. Nickel-Metal Hydride

- 6.1.3. Lithium-Ion Polymer

- 6.1.4. Sodium-Ion Battery

- 6.2. Market Analysis, Insights and Forecast - by End-User Application

- 6.2.1. Consumer Electronics

- 6.2.2. Electric Vehicles

- 6.2.3. Energy Storage System

- 6.2.4. Other End-User Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Semiconductor Battery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Lithium-Ion

- 7.1.2. Nickel-Metal Hydride

- 7.1.3. Lithium-Ion Polymer

- 7.1.4. Sodium-Ion Battery

- 7.2. Market Analysis, Insights and Forecast - by End-User Application

- 7.2.1. Consumer Electronics

- 7.2.2. Electric Vehicles

- 7.2.3. Energy Storage System

- 7.2.4. Other End-User Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Semiconductor Battery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Lithium-Ion

- 8.1.2. Nickel-Metal Hydride

- 8.1.3. Lithium-Ion Polymer

- 8.1.4. Sodium-Ion Battery

- 8.2. Market Analysis, Insights and Forecast - by End-User Application

- 8.2.1. Consumer Electronics

- 8.2.2. Electric Vehicles

- 8.2.3. Energy Storage System

- 8.2.4. Other End-User Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Semiconductor Battery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Lithium-Ion

- 9.1.2. Nickel-Metal Hydride

- 9.1.3. Lithium-Ion Polymer

- 9.1.4. Sodium-Ion Battery

- 9.2. Market Analysis, Insights and Forecast - by End-User Application

- 9.2.1. Consumer Electronics

- 9.2.2. Electric Vehicles

- 9.2.3. Energy Storage System

- 9.2.4. Other End-User Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Semiconductor Battery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Lithium-Ion

- 10.1.2. Nickel-Metal Hydride

- 10.1.3. Lithium-Ion Polymer

- 10.1.4. Sodium-Ion Battery

- 10.2. Market Analysis, Insights and Forecast - by End-User Application

- 10.2.1. Consumer Electronics

- 10.2.2. Electric Vehicles

- 10.2.3. Energy Storage System

- 10.2.4. Other End-User Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Semiconductor Battery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Lithium-Ion

- 11.1.2. Nickel-Metal Hydride

- 11.1.3. Lithium-Ion Polymer

- 11.1.4. Sodium-Ion Battery

- 11.2. Market Analysis, Insights and Forecast - by End-User Application

- 11.2.1. Consumer Electronics

- 11.2.2. Electric Vehicles

- 11.2.3. Energy Storage System

- 11.2.4. Other End-User Applications

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 EnerSys

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung SDI Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 TianJin Lishen Battery Joint-Stock Co Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Varta AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Toshiba Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Faradion Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 GS Yuasa Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Routejade

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Panasonic Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sony Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 EnerSys

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Battery Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Semiconductor Battery Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Semiconductor Battery Industry Revenue (Million), by Type 2025 & 2033

- Figure 4: North America Semiconductor Battery Industry Volume (K Unit), by Type 2025 & 2033

- Figure 5: North America Semiconductor Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Semiconductor Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Semiconductor Battery Industry Revenue (Million), by End-User Application 2025 & 2033

- Figure 8: North America Semiconductor Battery Industry Volume (K Unit), by End-User Application 2025 & 2033

- Figure 9: North America Semiconductor Battery Industry Revenue Share (%), by End-User Application 2025 & 2033

- Figure 10: North America Semiconductor Battery Industry Volume Share (%), by End-User Application 2025 & 2033

- Figure 11: North America Semiconductor Battery Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Semiconductor Battery Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Semiconductor Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Semiconductor Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Asia Pacific Semiconductor Battery Industry Revenue (Million), by Type 2025 & 2033

- Figure 16: Asia Pacific Semiconductor Battery Industry Volume (K Unit), by Type 2025 & 2033

- Figure 17: Asia Pacific Semiconductor Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Asia Pacific Semiconductor Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Asia Pacific Semiconductor Battery Industry Revenue (Million), by End-User Application 2025 & 2033

- Figure 20: Asia Pacific Semiconductor Battery Industry Volume (K Unit), by End-User Application 2025 & 2033

- Figure 21: Asia Pacific Semiconductor Battery Industry Revenue Share (%), by End-User Application 2025 & 2033

- Figure 22: Asia Pacific Semiconductor Battery Industry Volume Share (%), by End-User Application 2025 & 2033

- Figure 23: Asia Pacific Semiconductor Battery Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Asia Pacific Semiconductor Battery Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Asia Pacific Semiconductor Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Semiconductor Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Semiconductor Battery Industry Revenue (Million), by Type 2025 & 2033

- Figure 28: Europe Semiconductor Battery Industry Volume (K Unit), by Type 2025 & 2033

- Figure 29: Europe Semiconductor Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Europe Semiconductor Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Europe Semiconductor Battery Industry Revenue (Million), by End-User Application 2025 & 2033

- Figure 32: Europe Semiconductor Battery Industry Volume (K Unit), by End-User Application 2025 & 2033

- Figure 33: Europe Semiconductor Battery Industry Revenue Share (%), by End-User Application 2025 & 2033

- Figure 34: Europe Semiconductor Battery Industry Volume Share (%), by End-User Application 2025 & 2033

- Figure 35: Europe Semiconductor Battery Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe Semiconductor Battery Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Europe Semiconductor Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Semiconductor Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Semiconductor Battery Industry Revenue (Million), by Type 2025 & 2033

- Figure 40: South America Semiconductor Battery Industry Volume (K Unit), by Type 2025 & 2033

- Figure 41: South America Semiconductor Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 42: South America Semiconductor Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 43: South America Semiconductor Battery Industry Revenue (Million), by End-User Application 2025 & 2033

- Figure 44: South America Semiconductor Battery Industry Volume (K Unit), by End-User Application 2025 & 2033

- Figure 45: South America Semiconductor Battery Industry Revenue Share (%), by End-User Application 2025 & 2033

- Figure 46: South America Semiconductor Battery Industry Volume Share (%), by End-User Application 2025 & 2033

- Figure 47: South America Semiconductor Battery Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: South America Semiconductor Battery Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: South America Semiconductor Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Semiconductor Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Semiconductor Battery Industry Revenue (Million), by Type 2025 & 2033

- Figure 52: Middle East and Africa Semiconductor Battery Industry Volume (K Unit), by Type 2025 & 2033

- Figure 53: Middle East and Africa Semiconductor Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Middle East and Africa Semiconductor Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Middle East and Africa Semiconductor Battery Industry Revenue (Million), by End-User Application 2025 & 2033

- Figure 56: Middle East and Africa Semiconductor Battery Industry Volume (K Unit), by End-User Application 2025 & 2033

- Figure 57: Middle East and Africa Semiconductor Battery Industry Revenue Share (%), by End-User Application 2025 & 2033

- Figure 58: Middle East and Africa Semiconductor Battery Industry Volume Share (%), by End-User Application 2025 & 2033

- Figure 59: Middle East and Africa Semiconductor Battery Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Semiconductor Battery Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: Middle East and Africa Semiconductor Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Semiconductor Battery Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 4: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 5: Global Semiconductor Battery Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Semiconductor Battery Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 9: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 10: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 11: Global Semiconductor Battery Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Semiconductor Battery Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Rest of North America Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of North America Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 21: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 22: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 23: Global Semiconductor Battery Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Semiconductor Battery Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: China Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: China Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: India Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: India Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Japan Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Japan Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: South Korea Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Korea Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Rest of Asia Pacific Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Asia Pacific Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 36: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 37: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 38: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 39: Global Semiconductor Battery Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Semiconductor Battery Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Germany Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Germany Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: France Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: France Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Italy Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Italy Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 52: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 53: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 54: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 55: Global Semiconductor Battery Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Semiconductor Battery Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 57: Chile Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Chile Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: Brazil Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Brazil Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Argentina Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Argentina Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Rest of South America Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Rest of South America Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Global Semiconductor Battery Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 66: Global Semiconductor Battery Industry Volume K Unit Forecast, by Type 2020 & 2033

- Table 67: Global Semiconductor Battery Industry Revenue Million Forecast, by End-User Application 2020 & 2033

- Table 68: Global Semiconductor Battery Industry Volume K Unit Forecast, by End-User Application 2020 & 2033

- Table 69: Global Semiconductor Battery Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Semiconductor Battery Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: Saudi Arabia Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Saudi Arabia Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: United Arab Emirates Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: United Arab Emirates Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: South Africa Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: South Africa Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Egypt Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Egypt Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 79: Rest of Middle East and Africa Semiconductor Battery Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: Rest of Middle East and Africa Semiconductor Battery Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Battery Industry?

The projected CAGR is approximately 8.67%.

2. Which companies are prominent players in the Semiconductor Battery Industry?

Key companies in the market include EnerSys, Samsung SDI Co Ltd, TianJin Lishen Battery Joint-Stock Co Ltd, Varta AG, Toshiba Corporation, Faradion Limited, GS Yuasa Corporation, Routejade, Panasonic Corporation, Sony Corporation.

3. What are the main segments of the Semiconductor Battery Industry?

The market segments include Type, End-User Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.19 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand for Mobile Devices4.; Rising Adaption of Electric Vehicles.

6. What are the notable trends driving market growth?

The Electric Vehicle Segment is Expected to Witness Significant Demand.

7. Are there any restraints impacting market growth?

4.; Availability of Technical Challenges.

8. Can you provide examples of recent developments in the market?

February 2022: ROHM Semiconductor announced that the company developed a new evaluation board for ultra-efficient semiconductor battery operations for the newly developed Internet of Things devices called REFLVBMS001-EVK-001.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Battery Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence