Key Insights

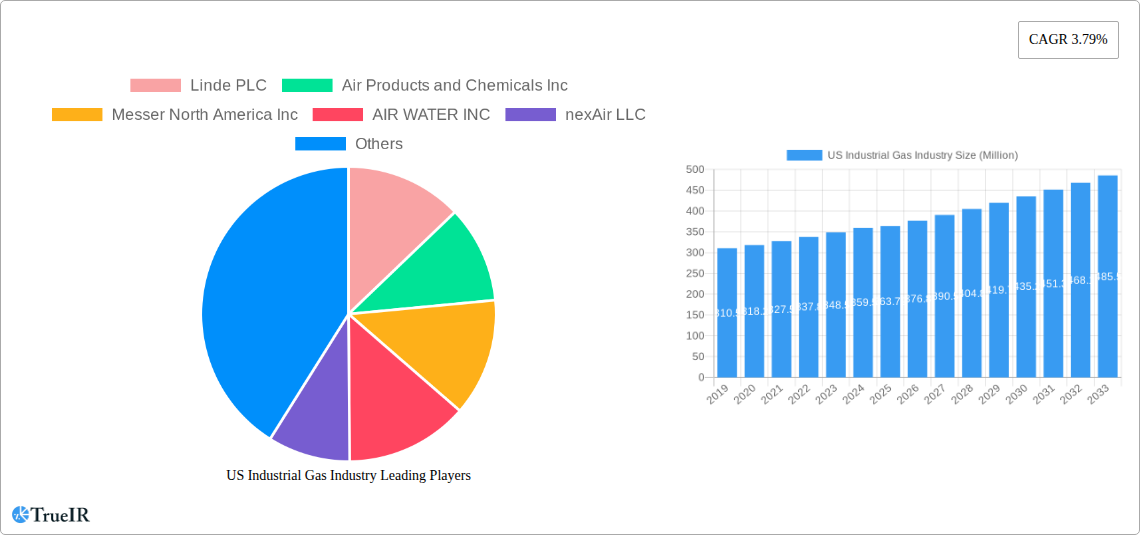

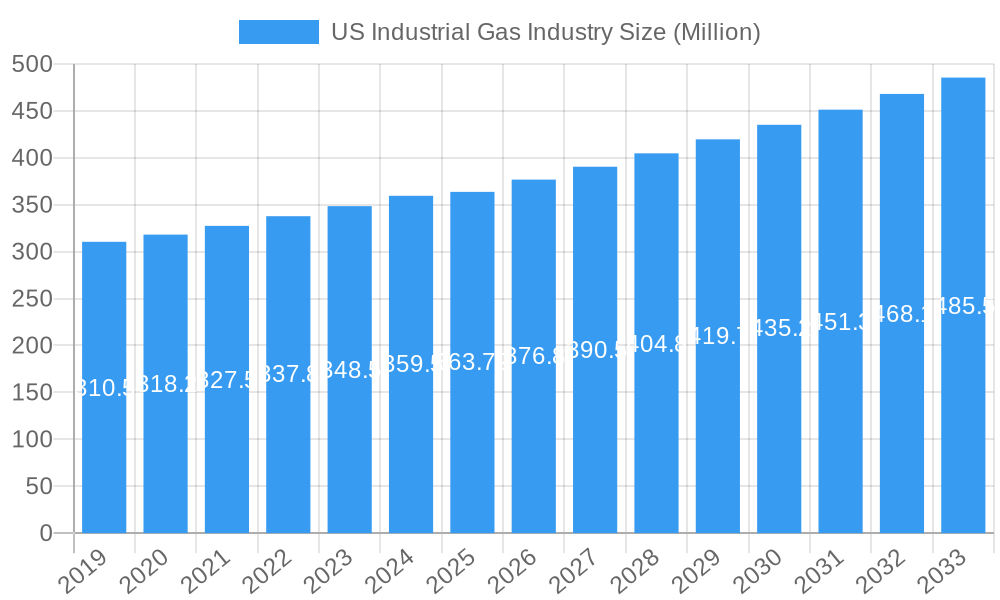

The US Industrial Gas market is poised for steady growth, projected to reach a substantial $363.72 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 3.79% through 2033. This expansion is fueled by robust demand across key sectors, with the oil and gas, petrochemical and chemical manufacturing, and metal manufacturing and fabrication industries serving as significant drivers. The increasing complexity of industrial processes, coupled with the growing need for specialized gases in advanced manufacturing and energy production, underpins this positive trajectory. Furthermore, the healthcare sector's reliance on medical gases like oxygen and nitrogen for life support and pharmaceutical production continues to be a cornerstone of market stability and growth. Innovations in gas production and delivery technologies are also contributing to efficiency gains and cost-effectiveness, further stimulating market adoption.

US Industrial Gas Industry Market Size (In Million)

However, the market faces certain constraints that necessitate strategic navigation by industry players. Fluctuations in raw material costs, particularly those associated with energy, can impact production expenses and, consequently, gas pricing. Stringent environmental regulations and the increasing emphasis on sustainable practices are also prompting a shift towards greener gas production methods, requiring significant investment in new technologies. Despite these challenges, the overarching trend points towards sustained demand, driven by the indispensable role of industrial gases in a wide array of critical economic activities. The ongoing development of new applications, from advanced electronics manufacturing to the burgeoning hydrogen economy, suggests a dynamic and evolving market landscape with ample opportunities for innovation and strategic investment.

US Industrial Gas Industry Company Market Share

US Industrial Gas Industry Market Analysis: Trends, Opportunities, and Future Outlook (2019-2033)

This comprehensive report delivers an in-depth analysis of the US Industrial Gas Industry, forecasting market dynamics from 2019 to 2033. Leveraging high-volume keywords, this report is optimized for search engines and designed to provide actionable insights for industry stakeholders. We delve into market structure, competitive landscapes, emerging trends, dominant segments, product innovations, key drivers, barriers, challenges, and the future outlook. The study encompasses a detailed examination of critical segments including Nitrogen, Oxygen, Carbon Dioxide, Hydrogen, Helium, Argon, Ammonia, Methane, Propane, and Butane, across diverse end-user industries such as Oil and Gas, Energy and Power, Petrochemical and Chemical Manufacturing, Medical and Pharmaceutical, Food and Beverage, Metal Manufacturing and Fabrication, and Transportation.

US Industrial Gas Industry Market Structure & Competitive Landscape

The US Industrial Gas Industry is characterized by a moderately concentrated market structure, dominated by a few major global players and a growing number of regional suppliers. Innovation drivers are primarily fueled by advancements in production technologies, increased demand for specialized gases, and the growing emphasis on sustainability and reduced carbon footprints. Regulatory impacts, particularly concerning environmental standards and safety protocols, play a significant role in shaping market entry and operational strategies. Product substitutes exist for certain applications, but the unique properties of industrial gases often make direct replacement challenging. End-user segmentation reveals a broad spectrum of applications, with significant reliance on the Oil and Gas, Petrochemical, and Medical sectors. Merger and acquisition (M&A) trends indicate a strategic consolidation of market share and expansion of geographical reach. Recent M&A activities, valued in the hundreds of millions of dollars, underscore the competitive drive for vertical integration and diversification. A substantial portion of market share, estimated to be over 70%, is held by the top five players.

US Industrial Gas Industry Market Trends & Opportunities

The US Industrial Gas Industry is poised for robust growth, with an estimated market size of over $45 Billion in the base year of 2025, projected to expand at a Compound Annual Growth Rate (CAGR) exceeding 6% throughout the forecast period of 2025-2033. This expansion is driven by a confluence of technological shifts, evolving consumer preferences, and dynamic competitive landscapes. Technological advancements in gas production, purification, and distribution are enabling greater efficiency and cost-effectiveness. The increasing adoption of on-site gas generation and modular production facilities is transforming supply chain dynamics, offering tailored solutions to end-users. Furthermore, the growing demand for high-purity gases in advanced manufacturing processes, such as semiconductor fabrication and additive manufacturing, presents significant opportunities. Consumer preferences are increasingly leaning towards environmentally friendly and sustainable gas solutions. This is evident in the burgeoning demand for green hydrogen and carbon capture technologies, directly impacting the market for these gases. Competitive dynamics are intensifying, with established players focusing on strategic acquisitions and partnerships to expand their product portfolios and geographical presence. Emerging players are capitalizing on niche markets and specialized applications. The energy transition, with its focus on renewable energy sources and decarbonization efforts, is a major catalyst, driving demand for gases like hydrogen as a clean fuel and for various industrial processes in renewable energy infrastructure development. The pharmaceutical and healthcare sectors continue to be a consistent driver of demand for medical-grade gases like oxygen and nitrogen, with an aging population and advancements in medical treatments further solidifying this segment. The food and beverage industry's demand for gases like carbon dioxide for packaging and beverage carbonation, as well as nitrogen for freezing and preservation, remains a stable and growing market. The ongoing investments in infrastructure projects across the nation also contribute to the steady demand for industrial gases in construction and fabrication. The strategic implementation of advanced separation technologies, coupled with a focus on operational excellence and supply chain resilience, will be crucial for capitalizing on these expanding market opportunities and maintaining a competitive edge in this evolving industry landscape.

Dominant Markets & Segments in US Industrial Gas Industry

Within the US Industrial Gas Industry, Nitrogen consistently emerges as a dominant product type, driven by its widespread applications in the Petrochemical and Chemical Manufacturing and Oil and Gas sectors. Its inert properties are crucial for Blanketing, Purging, and Inerting processes, ensuring safety and product integrity. The Energy and Power sector also represents a significant market for nitrogen, particularly in applications like turbine flushing and power plant maintenance.

Product Type Dominance:

- Nitrogen: Leading market share due to its extensive use in inerting, blanketing, and purging across major industrial sectors. Its demand is intrinsically linked to the health and expansion of the petrochemical, chemical, and oil and gas industries.

- Oxygen: A strong second, primarily driven by its critical role in metal manufacturing and fabrication (welding, cutting), healthcare (medical oxygen), and the energy sector for combustion enhancement and gasification processes.

- Hydrogen: Experiencing rapid growth, fueled by the energy transition and its increasing use in refining, ammonia production, and emerging applications in fuel cells and green hydrogen initiatives. The Oil and Gas and Petrochemical sectors are current major consumers, with significant future potential in Transportation and Energy and Power.

- Carbon Dioxide: Widely used in the Food and Beverage industry for carbonation and preservation, as well as in Metal Manufacturing for welding and in the Chemical industry.

End-User Industry Dominance:

- Petrochemical and Chemical Manufacturing: This segment represents the largest consumer of industrial gases, particularly nitrogen and hydrogen, for various synthesis, processing, and safety applications. Infrastructure development and expansion in this sector directly translate to increased gas demand.

- Oil and Gas: A perennial strong performer, consuming significant volumes of nitrogen for purging, well stimulation, and as a diluent. Hydrogen is also critical for refining processes.

- Medical and Pharmaceutical: A steady and high-value market, driven by the constant need for medical-grade oxygen, nitrogen, and other specialty gases for patient care, research, and pharmaceutical manufacturing. Regulatory mandates for medical gas purity and supply chain reliability reinforce this segment's importance.

- Metal Manufacturing and Fabrication: This sector relies heavily on oxygen for cutting and welding, and on argon for TIG and MIG welding, making it a consistently significant market.

The growth in these dominant segments is supported by substantial investments in infrastructure, favorable government policies promoting industrial development and energy security, and the ongoing pursuit of operational efficiencies and product innovation within these core industries. The geographical distribution of these industries within the US further dictates regional market dominance, with states having a strong presence in petrochemical production or heavy manufacturing leading in overall industrial gas consumption.

US Industrial Gas Industry Product Analysis

Innovations in industrial gas production and application are continuously enhancing efficiency and expanding market reach. Advancements in cryogenic distillation and membrane separation technologies are leading to more cost-effective and environmentally friendly production of key gases like nitrogen and oxygen. In the hydrogen sector, breakthroughs in electrolysis powered by renewable energy are paving the way for green hydrogen, a critical component of decarbonization efforts. Liquid hydrogen storage and transportation solutions are also seeing significant development to support the burgeoning hydrogen mobility market. The application spectrum for industrial gases is also broadening, with increased use of specialty gases in semiconductor manufacturing, advanced materials production, and in the burgeoning biotechnology sector, underscoring the market's adaptability and responsiveness to emerging technological demands.

Key Drivers, Barriers & Challenges in US Industrial Gas Industry

Key Drivers: The US Industrial Gas Industry is propelled by several significant factors. Technologically, advancements in on-site generation and modular production are enhancing efficiency and reducing costs. Economically, robust demand from the manufacturing sector, particularly in petrochemicals and metals, alongside growth in healthcare and energy, provides a stable foundation. Policy-driven factors such as government initiatives supporting decarbonization and renewable energy adoption, particularly for hydrogen, are creating new avenues for growth. The increasing stringency of environmental regulations also drives demand for gases used in emission control and cleaner industrial processes.

Barriers & Challenges: Despite the positive outlook, the industry faces several challenges. Supply chain disruptions, exacerbated by global events, can impact the availability and cost of raw materials and the efficient distribution of gases. Regulatory complexities, particularly around environmental compliance and the transportation of hazardous materials, add to operational overhead. Intense competitive pressures among established players and new entrants necessitate continuous innovation and cost optimization. Furthermore, the capital-intensive nature of building and maintaining production facilities poses a significant financial hurdle, especially for smaller regional players. Fluctuations in energy prices can also impact production costs and, consequently, gas pricing.

Growth Drivers in the US Industrial Gas Industry Market

Key growth drivers in the US Industrial Gas Industry are multifaceted. Technologically, innovations in gas separation and purification, coupled with the development of on-site generation solutions, are significantly improving efficiency and reducing costs for end-users. Economically, the sustained demand from core sectors like petrochemicals, chemicals, metal fabrication, and healthcare, alongside the emerging needs of the renewable energy sector for hydrogen, provides a strong market foundation. Policy-driven factors, such as government incentives for decarbonization and the expansion of clean energy infrastructure, are creating substantial opportunities, particularly for hydrogen production and carbon capture technologies. The increasing adoption of advanced manufacturing techniques also necessitates the use of high-purity specialty gases, further contributing to market expansion.

Challenges Impacting US Industrial Gas Industry Growth

The growth of the US Industrial Gas Industry is not without its impediments. Regulatory complexities, encompassing stringent environmental standards and evolving safety protocols for hazardous gas transport, can increase operational costs and lead times. Supply chain vulnerabilities, as demonstrated by recent global disruptions, pose risks to the consistent availability of feedstocks and the efficient delivery of products. Intense competitive pressures among a consolidated group of major players and emerging regional suppliers demand continuous investment in technology and service to maintain market share. The substantial capital investment required for building and maintaining production facilities and distribution networks also presents a significant barrier to entry and expansion, particularly for smaller entities.

Key Players Shaping the US Industrial Gas Industry Market

- Linde PLC

- Air Products and Chemicals Inc

- Messer North America Inc

- AIR WATER INC

- nexAir LLC

- Matheson Tri-Gas Inc

- BASF SE

- Iwatani Corporation

- NIPPON SANSO HOLDINGS CORPORATION

- Air Liquide

- UIG

Significant US Industrial Gas Industry Industry Milestones

- January 2023: Iwatani Corporation of America, a wholly-owned subsidiary of Iwatani Corporation, announced the acquisition of Aspen Air US, LLC, a leading manufacturer and distributor of bulk liquid industrial gases. This acquisition marks Iwatani's entrance into the United States Industrial Gases sector and highlights the company's expansion focus in this business segment.

- May 2022: Air Liquide established its largest liquid hydrogen production and logistics infrastructure complex in North Las Vegas, Nevada, to cater to the growing hydrogen mobility industry. With a USD 250 million investment, the plant has the capacity to manufacture 30 tons of liquid hydrogen per day, some of which is sourced from renewable natural gas produced using Air Liquide's advanced separation membrane technology, including landfill-sourced renewable natural gas.

Future Outlook for US Industrial Gas Industry Market

The future outlook for the US Industrial Gas Industry is exceptionally promising, driven by the accelerating energy transition and ongoing technological advancements. The burgeoning demand for hydrogen as a clean fuel, supported by significant government investment and corporate commitments, is expected to be a primary growth catalyst. Advancements in carbon capture utilization and storage (CCUS) technologies will also create substantial opportunities for gases like CO2. Furthermore, the continued growth in the pharmaceutical, advanced manufacturing, and semiconductor sectors will sustain the demand for high-purity and specialty gases. Strategic investments in infrastructure, a focus on sustainable production methods, and the expansion into emerging applications will be crucial for market players to capitalize on this robust growth trajectory. The industry is well-positioned to play a pivotal role in supporting decarbonization efforts and enabling technological innovation across a multitude of sectors.

US Industrial Gas Industry Segmentation

-

1. Product Type

- 1.1. Nitrogen

- 1.2. Oxygen

- 1.3. Carbon Dioxide

- 1.4. Hydrogen

- 1.5. Helium

- 1.6. Argon

- 1.7. Ammonia

- 1.8. Methane

- 1.9. Propane

- 1.10. Butane

- 1.11. Other Product Types

-

2. End-User Industry

- 2.1. Oil and Gas

- 2.2. Energy and Power

- 2.3. Petrochemical and Chemical Manufacturing

- 2.4. Medical and Pharmaceutical

- 2.5. Food and Beverage

- 2.6. Metal Manufacturing and Fabrication

- 2.7. Transportation

- 2.8. Other En

US Industrial Gas Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

US Industrial Gas Industry Regional Market Share

Geographic Coverage of US Industrial Gas Industry

US Industrial Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Nitrogen

- 5.1.2. Oxygen

- 5.1.3. Carbon Dioxide

- 5.1.4. Hydrogen

- 5.1.5. Helium

- 5.1.6. Argon

- 5.1.7. Ammonia

- 5.1.8. Methane

- 5.1.9. Propane

- 5.1.10. Butane

- 5.1.11. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Oil and Gas

- 5.2.2. Energy and Power

- 5.2.3. Petrochemical and Chemical Manufacturing

- 5.2.4. Medical and Pharmaceutical

- 5.2.5. Food and Beverage

- 5.2.6. Metal Manufacturing and Fabrication

- 5.2.7. Transportation

- 5.2.8. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global US Industrial Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Nitrogen

- 6.1.2. Oxygen

- 6.1.3. Carbon Dioxide

- 6.1.4. Hydrogen

- 6.1.5. Helium

- 6.1.6. Argon

- 6.1.7. Ammonia

- 6.1.8. Methane

- 6.1.9. Propane

- 6.1.10. Butane

- 6.1.11. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Oil and Gas

- 6.2.2. Energy and Power

- 6.2.3. Petrochemical and Chemical Manufacturing

- 6.2.4. Medical and Pharmaceutical

- 6.2.5. Food and Beverage

- 6.2.6. Metal Manufacturing and Fabrication

- 6.2.7. Transportation

- 6.2.8. Other En

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America US Industrial Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Nitrogen

- 7.1.2. Oxygen

- 7.1.3. Carbon Dioxide

- 7.1.4. Hydrogen

- 7.1.5. Helium

- 7.1.6. Argon

- 7.1.7. Ammonia

- 7.1.8. Methane

- 7.1.9. Propane

- 7.1.10. Butane

- 7.1.11. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by End-User Industry

- 7.2.1. Oil and Gas

- 7.2.2. Energy and Power

- 7.2.3. Petrochemical and Chemical Manufacturing

- 7.2.4. Medical and Pharmaceutical

- 7.2.5. Food and Beverage

- 7.2.6. Metal Manufacturing and Fabrication

- 7.2.7. Transportation

- 7.2.8. Other En

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. South America US Industrial Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Nitrogen

- 8.1.2. Oxygen

- 8.1.3. Carbon Dioxide

- 8.1.4. Hydrogen

- 8.1.5. Helium

- 8.1.6. Argon

- 8.1.7. Ammonia

- 8.1.8. Methane

- 8.1.9. Propane

- 8.1.10. Butane

- 8.1.11. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by End-User Industry

- 8.2.1. Oil and Gas

- 8.2.2. Energy and Power

- 8.2.3. Petrochemical and Chemical Manufacturing

- 8.2.4. Medical and Pharmaceutical

- 8.2.5. Food and Beverage

- 8.2.6. Metal Manufacturing and Fabrication

- 8.2.7. Transportation

- 8.2.8. Other En

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe US Industrial Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Nitrogen

- 9.1.2. Oxygen

- 9.1.3. Carbon Dioxide

- 9.1.4. Hydrogen

- 9.1.5. Helium

- 9.1.6. Argon

- 9.1.7. Ammonia

- 9.1.8. Methane

- 9.1.9. Propane

- 9.1.10. Butane

- 9.1.11. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by End-User Industry

- 9.2.1. Oil and Gas

- 9.2.2. Energy and Power

- 9.2.3. Petrochemical and Chemical Manufacturing

- 9.2.4. Medical and Pharmaceutical

- 9.2.5. Food and Beverage

- 9.2.6. Metal Manufacturing and Fabrication

- 9.2.7. Transportation

- 9.2.8. Other En

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East & Africa US Industrial Gas Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Nitrogen

- 10.1.2. Oxygen

- 10.1.3. Carbon Dioxide

- 10.1.4. Hydrogen

- 10.1.5. Helium

- 10.1.6. Argon

- 10.1.7. Ammonia

- 10.1.8. Methane

- 10.1.9. Propane

- 10.1.10. Butane

- 10.1.11. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by End-User Industry

- 10.2.1. Oil and Gas

- 10.2.2. Energy and Power

- 10.2.3. Petrochemical and Chemical Manufacturing

- 10.2.4. Medical and Pharmaceutical

- 10.2.5. Food and Beverage

- 10.2.6. Metal Manufacturing and Fabrication

- 10.2.7. Transportation

- 10.2.8. Other En

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific US Industrial Gas Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Nitrogen

- 11.1.2. Oxygen

- 11.1.3. Carbon Dioxide

- 11.1.4. Hydrogen

- 11.1.5. Helium

- 11.1.6. Argon

- 11.1.7. Ammonia

- 11.1.8. Methane

- 11.1.9. Propane

- 11.1.10. Butane

- 11.1.11. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by End-User Industry

- 11.2.1. Oil and Gas

- 11.2.2. Energy and Power

- 11.2.3. Petrochemical and Chemical Manufacturing

- 11.2.4. Medical and Pharmaceutical

- 11.2.5. Food and Beverage

- 11.2.6. Metal Manufacturing and Fabrication

- 11.2.7. Transportation

- 11.2.8. Other En

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Linde PLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Air Products and Chemicals Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Messer North America Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AIR WATER INC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 nexAir LLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Matheson Tri-Gas Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BASF SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Iwatani Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 NIPPON SANSO HOLDINGS CORPORATION

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Air Liquide

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 UIG*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Linde PLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Industrial Gas Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global US Industrial Gas Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: North America US Industrial Gas Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America US Industrial Gas Industry Volume (K Tons), by Product Type 2025 & 2033

- Figure 5: North America US Industrial Gas Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America US Industrial Gas Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America US Industrial Gas Industry Revenue (Million), by End-User Industry 2025 & 2033

- Figure 8: North America US Industrial Gas Industry Volume (K Tons), by End-User Industry 2025 & 2033

- Figure 9: North America US Industrial Gas Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 10: North America US Industrial Gas Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 11: North America US Industrial Gas Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America US Industrial Gas Industry Volume (K Tons), by Country 2025 & 2033

- Figure 13: North America US Industrial Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America US Industrial Gas Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: South America US Industrial Gas Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 16: South America US Industrial Gas Industry Volume (K Tons), by Product Type 2025 & 2033

- Figure 17: South America US Industrial Gas Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: South America US Industrial Gas Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 19: South America US Industrial Gas Industry Revenue (Million), by End-User Industry 2025 & 2033

- Figure 20: South America US Industrial Gas Industry Volume (K Tons), by End-User Industry 2025 & 2033

- Figure 21: South America US Industrial Gas Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 22: South America US Industrial Gas Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 23: South America US Industrial Gas Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: South America US Industrial Gas Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: South America US Industrial Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America US Industrial Gas Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe US Industrial Gas Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 28: Europe US Industrial Gas Industry Volume (K Tons), by Product Type 2025 & 2033

- Figure 29: Europe US Industrial Gas Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Europe US Industrial Gas Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 31: Europe US Industrial Gas Industry Revenue (Million), by End-User Industry 2025 & 2033

- Figure 32: Europe US Industrial Gas Industry Volume (K Tons), by End-User Industry 2025 & 2033

- Figure 33: Europe US Industrial Gas Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 34: Europe US Industrial Gas Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 35: Europe US Industrial Gas Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe US Industrial Gas Industry Volume (K Tons), by Country 2025 & 2033

- Figure 37: Europe US Industrial Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe US Industrial Gas Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa US Industrial Gas Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 40: Middle East & Africa US Industrial Gas Industry Volume (K Tons), by Product Type 2025 & 2033

- Figure 41: Middle East & Africa US Industrial Gas Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 42: Middle East & Africa US Industrial Gas Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 43: Middle East & Africa US Industrial Gas Industry Revenue (Million), by End-User Industry 2025 & 2033

- Figure 44: Middle East & Africa US Industrial Gas Industry Volume (K Tons), by End-User Industry 2025 & 2033

- Figure 45: Middle East & Africa US Industrial Gas Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 46: Middle East & Africa US Industrial Gas Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 47: Middle East & Africa US Industrial Gas Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East & Africa US Industrial Gas Industry Volume (K Tons), by Country 2025 & 2033

- Figure 49: Middle East & Africa US Industrial Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa US Industrial Gas Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific US Industrial Gas Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 52: Asia Pacific US Industrial Gas Industry Volume (K Tons), by Product Type 2025 & 2033

- Figure 53: Asia Pacific US Industrial Gas Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Asia Pacific US Industrial Gas Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Asia Pacific US Industrial Gas Industry Revenue (Million), by End-User Industry 2025 & 2033

- Figure 56: Asia Pacific US Industrial Gas Industry Volume (K Tons), by End-User Industry 2025 & 2033

- Figure 57: Asia Pacific US Industrial Gas Industry Revenue Share (%), by End-User Industry 2025 & 2033

- Figure 58: Asia Pacific US Industrial Gas Industry Volume Share (%), by End-User Industry 2025 & 2033

- Figure 59: Asia Pacific US Industrial Gas Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Asia Pacific US Industrial Gas Industry Volume (K Tons), by Country 2025 & 2033

- Figure 61: Asia Pacific US Industrial Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific US Industrial Gas Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 4: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 5: Global US Industrial Gas Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global US Industrial Gas Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 9: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 10: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 11: Global US Industrial Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global US Industrial Gas Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: United States US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Canada US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Mexico US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 20: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 21: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 22: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 23: Global US Industrial Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global US Industrial Gas Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: Brazil US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Brazil US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: Argentina US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Argentina US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 32: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 33: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 34: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 35: Global US Industrial Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global US Industrial Gas Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 37: United Kingdom US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 39: Germany US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Germany US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 41: France US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: France US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: Italy US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Italy US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: Spain US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Spain US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: Russia US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Russia US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Benelux US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Benelux US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Nordics US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Nordics US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 55: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 56: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 57: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 58: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 59: Global US Industrial Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global US Industrial Gas Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 61: Turkey US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Turkey US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 63: Israel US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Israel US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 65: GCC US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: GCC US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 67: North Africa US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: North Africa US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 69: South Africa US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: South Africa US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 73: Global US Industrial Gas Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 74: Global US Industrial Gas Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 75: Global US Industrial Gas Industry Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 76: Global US Industrial Gas Industry Volume K Tons Forecast, by End-User Industry 2020 & 2033

- Table 77: Global US Industrial Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 78: Global US Industrial Gas Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 79: China US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: China US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 81: India US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 82: India US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 83: Japan US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 84: Japan US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 85: South Korea US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: South Korea US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 87: ASEAN US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 89: Oceania US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Oceania US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific US Industrial Gas Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific US Industrial Gas Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Industrial Gas Industry?

The projected CAGR is approximately 3.79%.

2. Which companies are prominent players in the US Industrial Gas Industry?

Key companies in the market include Linde PLC, Air Products and Chemicals Inc, Messer North America Inc, AIR WATER INC, nexAir LLC, Matheson Tri-Gas Inc, BASF SE, Iwatani Corporation, NIPPON SANSO HOLDINGS CORPORATION, Air Liquide, UIG*List Not Exhaustive.

3. What are the main segments of the US Industrial Gas Industry?

The market segments include Product Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 363.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand from the Healthcare Sector; Increasing Demand for Frozen and Stored Food; Growing Need for Alternate Energy Sources.

6. What are the notable trends driving market growth?

Resilient Demand from the Healthcare Industry.

7. Are there any restraints impacting market growth?

Environmental Regulations and Safety Issues; Other Restraints.

8. Can you provide examples of recent developments in the market?

January 2023: Iwatani Corporation of America, a wholly-owned subsidiary of Iwatani Corporation, announced the acquisition of Aspen Air US, LLC, a leading manufacturer and distributor of bulk liquid industrial gases. This acquisition marks Iwatani's entrance into the United States Industrial Gases sector and highlights the company's expansion focus in this business segment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Industrial Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Industrial Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Industrial Gas Industry?

To stay informed about further developments, trends, and reports in the US Industrial Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence