Key Insights

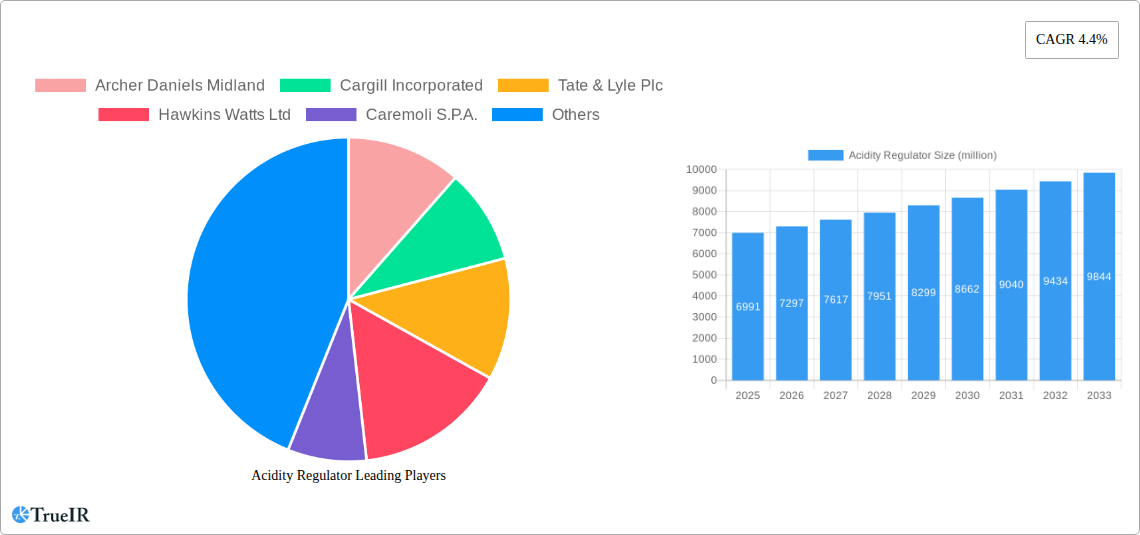

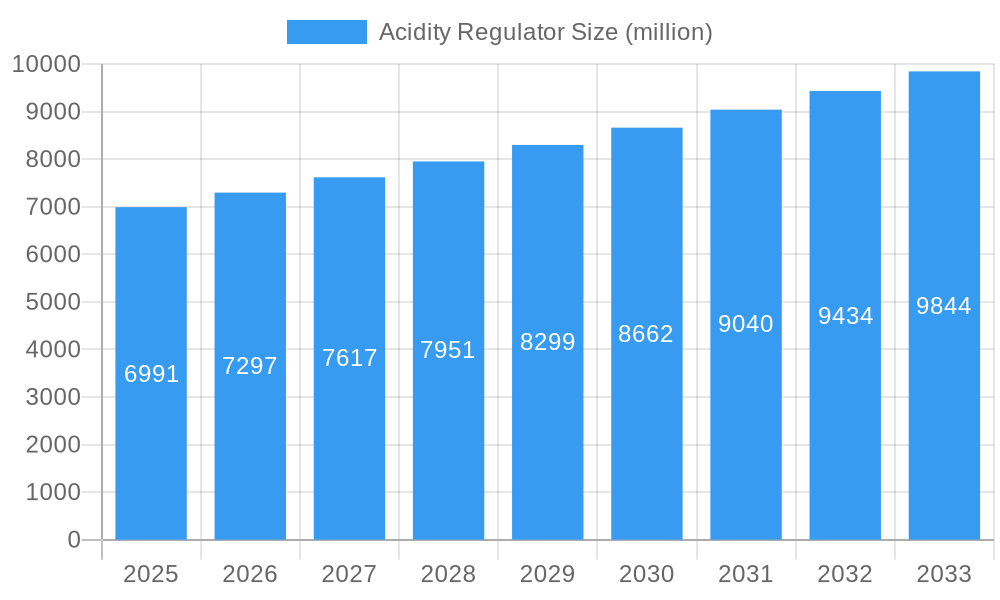

The global Acidity Regulator market is poised for robust growth, projected to reach a substantial USD 6991 million by 2025. This expansion is driven by a confluence of factors, including the increasing consumer demand for processed foods and beverages, a growing awareness of food preservation techniques, and the critical role of acidity regulators in enhancing flavor profiles and product shelf life. The market's CAGR of 4.4% over the forecast period (2025-2033) underscores its sustained upward trajectory. Key applications such as beverages, sauces, dressings, and condiments, along with processed foods, are expected to be significant contributors to this growth. The rising popularity of convenience foods and the expansion of the food service industry globally are further bolstering the demand for these essential food additives. Innovations in production processes and the development of novel acidity regulators are also anticipated to play a crucial role in market expansion.

Acidity Regulator Market Size (In Billion)

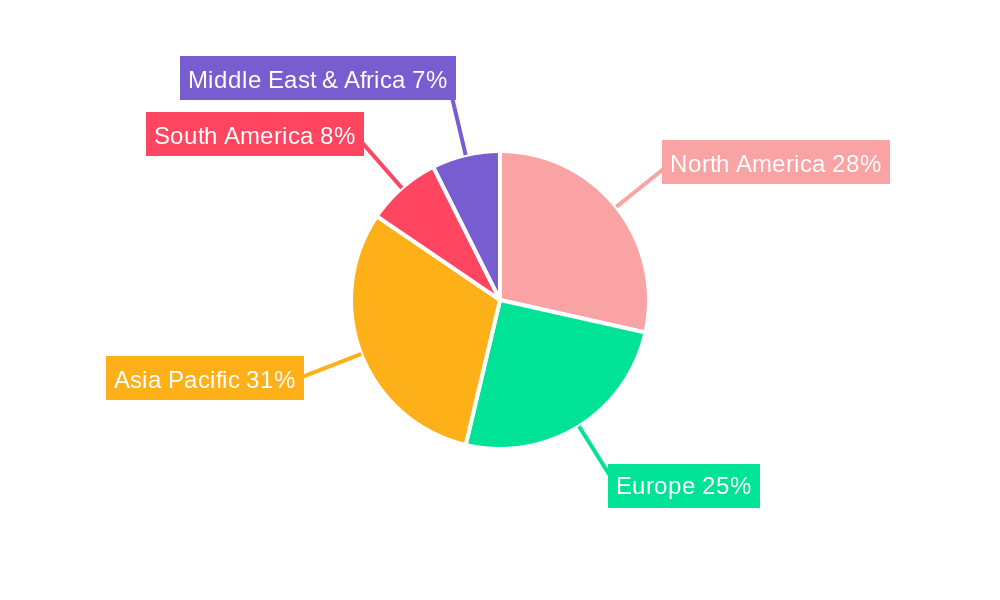

The market is segmented by type, with Acetic Acid, Citric Acid, and Lactic Acid emerging as dominant categories due to their widespread use and versatility in food and beverage formulations. While the overall outlook is positive, the market may face certain restraints, including fluctuating raw material prices and stringent regulatory compliances in specific regions. However, the sheer breadth of applications across various food categories and the continuous innovation by leading companies such as Archer Daniels Midland, Cargill Incorporated, and Tate & Lyle Plc are expected to overcome these challenges. Geographically, Asia Pacific is anticipated to witness the fastest growth, fueled by rapid industrialization, increasing disposable incomes, and a burgeoning food processing sector in countries like China and India. North America and Europe will continue to be significant markets, driven by established food industries and a focus on product quality and innovation.

Acidity Regulator Company Market Share

Acidity Regulator Market: Comprehensive Analysis and Future Projections (2019-2033)

This in-depth report offers a dynamic and SEO-optimized analysis of the global Acidity Regulator market. Leveraging high-volume keywords and detailed insights, this report is designed for industry professionals seeking a comprehensive understanding of market structure, trends, opportunities, and future outlook. Our analysis spans the historical period of 2019–2024, with a base year of 2025 and a forecast period extending to 2033.

Acidity Regulator Market Structure & Competitive Landscape

The global Acidity Regulator market exhibits a moderately concentrated structure, with key players investing heavily in research and development to drive innovation. Food ingredients, food additives, and food processing are central to market dynamics. Regulatory frameworks, particularly concerning food safety regulations and labeling requirements, significantly influence market entry and product development. The presence of numerous acetic acid manufacturers, citric acid suppliers, and lactic acid producers creates a competitive environment. Product substitutes, while present in some niche applications, are generally less effective in replicating the functional and cost-efficiency benefits of established acidity regulators. End-user segmentation reveals strong demand from the beverage industry, bakery and confectionery sector, and sauces, dressings, and condiments manufacturers. Merger and acquisition (M&A) activity is a significant trend, with an estimated volume of over 500 million USD in transactions over the past five years, aimed at expanding market share and diversifying product portfolios. Key M&A drivers include acquiring innovative technologies and gaining access to new geographical markets. Concentration ratios for the top five players are estimated to be around 35%, indicating a balance between established giants and emerging specialized companies.

- Innovation Drivers: Focus on natural and clean-label acidity regulators, enhanced shelf-life solutions, and cost-effective production methods.

- Regulatory Impacts: Stringent quality control measures and evolving food additive approval processes.

- Product Substitutes: Limited in many core applications due to cost, efficacy, and consumer acceptance of established options.

- End-User Segmentation: Dominance of beverages and processed foods, with growing interest in dairy and meat applications.

- M&A Trends: Strategic acquisitions to consolidate market position and broaden technological capabilities.

Acidity Regulator Market Trends & Opportunities

The global Acidity Regulator market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This expansion is fueled by an escalating global demand for processed foods and beverages, driven by changing consumer lifestyles, urbanization, and a rising middle-class population in emerging economies. The food and beverage industry, being the primary consumer of acidity regulators, is continuously innovating, leading to new product formulations that require specific pH control. Technological shifts are increasingly leaning towards natural and organically sourced acidity regulators, such as citric acid derived from fermentation and lactic acid from sustainable sources. This trend caters to the growing consumer preference for “clean-label” products and natural ingredients. The bakery and confectionery sector is a significant contributor, utilizing acidity regulators for leavening, flavor enhancement, and texture improvement. Similarly, the sauces, dressings, and condiments market relies on these compounds for pH stability, preservation, and taste profile development. Opportunities lie in developing novel acidity regulators with improved functional properties, such as enhanced buffering capacity or synergistic effects with other food ingredients. The rise of functional foods and beverages also presents a lucrative avenue, where acidity regulators can play a role in stabilizing active ingredients or improving palatability. Furthermore, the increasing focus on food preservation techniques to reduce food waste globally will continue to drive demand for effective acidity regulators. Market penetration rates for advanced acidity regulator solutions are still relatively low in some developing regions, presenting significant expansion opportunities for manufacturers willing to invest in localized production and distribution networks. The acetic acid market and phosphoric acid market remain substantial, but innovation in these areas is shifting towards higher purity and specialized industrial applications. The malic acid market, while smaller, is seeing growth due to its widespread use in confectionery and beverages. The overall market size is expected to grow from an estimated 12 million tons in the base year to over 20 million tons by the end of the forecast period.

Dominant Markets & Segments in Acidity Regulator

The Beverages application segment stands out as the dominant force in the global Acidity Regulator market, accounting for an estimated 45% of the total market share. This dominance is attributed to the extensive use of acidity regulators in a wide array of beverages, including carbonated drinks, fruit juices, and dairy-based beverages, where they are crucial for taste, preservation, and flavor enhancement. Within the beverage segment, citric acid is a leading type of acidity regulator, widely favored for its mild taste and excellent chelating properties. The Asia-Pacific region, particularly countries like China and India, is emerging as the fastest-growing geographical market. This growth is propelled by rapid industrialization, a burgeoning food processing industry, and increasing consumer disposable income, leading to higher consumption of processed foods and beverages. Government initiatives promoting food safety standards and encouraging investment in the food sector further bolster market expansion in this region.

Dominant Application Segment: Beverages

- Key Growth Drivers: Growing demand for carbonated soft drinks and functional beverages, improved shelf life of beverage products, and the use of acidity regulators in flavor enhancement.

- Market Dominance Analysis: The beverage industry's sheer volume and the constant innovation in product formulations necessitate reliable and cost-effective pH control, making acidity regulators indispensable.

Dominant Type Segment: Citric Acid

- Key Growth Drivers: Natural origin, versatility across various food and beverage applications, cost-effectiveness in large-scale production, and widespread consumer acceptance as a safe ingredient.

- Market Dominance Analysis: Citric acid's ability to act as an acidulant, flavor enhancer, and preservative makes it a preferred choice for manufacturers in beverages, confectionery, and processed foods.

Dominant Geographical Region: Asia-Pacific

- Key Growth Drivers: Rapid economic development, increasing urbanization leading to higher consumption of convenience foods, a growing middle class with increased purchasing power, and government support for the food processing industry.

- Market Dominance Analysis: The region's vast population and the expanding food manufacturing base create a significant and growing demand for acidity regulators across all application segments.

The Processed Foods segment is the second-largest application, followed by Bakery and Confectionery, and then Sauces, Dressings, and Condiments. In terms of types, after Citric Acid, Phosphoric Acid holds a significant share, particularly in the beverage industry for its tartness and preservative qualities. Lactic Acid is gaining traction due to its role in fermented foods and its natural origin. The Other category for types, which includes organic acids like tartaric and malic acid, also contributes substantially, especially in niche applications like wine production and sugar confectionery. The United States and European Union countries continue to be mature markets with steady demand, driven by a well-established food processing industry and stringent quality standards.

Acidity Regulator Product Analysis

Acidity regulators are essential food additives that control the pH of food products, influencing taste, preservation, and texture. Recent product innovations focus on enhancing their natural origins and improving functional properties. Citric acid, derived primarily through microbial fermentation of carbohydrates, remains a cornerstone due to its versatile applications in beverages, confectionery, and processed foods. Lactic acid, produced via bacterial fermentation, is gaining prominence for its role in improving the flavor and shelf-life of dairy products and baked goods, aligning with the clean-label trend. Phosphoric acid, while a synthetic option, continues to be widely used in carbonated beverages for its sharp taste and preservative effects. Malic acid and tartaric acid find specific applications in confectionery and wine production, respectively. Competitive advantages are increasingly tied to cost-effectiveness, purity, and sustainability of sourcing and production processes.

Key Drivers, Barriers & Challenges in Acidity Regulator

The Acidity Regulator market is propelled by several key drivers. The burgeoning global food and beverage industry, driven by population growth and urbanization, is a primary catalyst. Increasing consumer demand for processed and convenience foods necessitates effective preservation and flavor enhancement, directly boosting the need for acidity regulators. Furthermore, the growing trend towards clean-label and natural ingredients is spurring innovation in naturally derived acidity regulators like citric acid and lactic acid. Technological advancements in fermentation processes are also making these natural options more cost-competitive and scalable.

Conversely, the market faces significant barriers and challenges. Stringent and evolving regulatory landscapes across different countries can pose hurdles to market entry and product approval, impacting the pace of innovation and adoption. Fluctuations in raw material prices, particularly for agricultural inputs used in fermentation, can affect production costs and profit margins. Intense competition among numerous global and regional players also exerts pressure on pricing. Supply chain disruptions, as evidenced in recent global events, can impact the availability and cost of key ingredients and finished products.

Growth Drivers in the Acidity Regulator Market

The growth of the Acidity Regulator market is significantly influenced by several interconnected factors. The escalating global demand for convenience foods and beverages, a direct consequence of changing consumer lifestyles and urbanization, provides a consistent base for market expansion. Technological advancements in food processing and preservation techniques are continuously creating new avenues for acidity regulators to enhance product quality and extend shelf life. Government policies promoting food safety and quality standards, alongside incentives for the food processing sector in emerging economies, further stimulate growth. The increasing consumer consciousness regarding health and wellness is also driving demand for natural and clean-label food ingredients, creating opportunities for bio-based acidity regulators.

Challenges Impacting Acidity Regulator Growth

Several challenges can impede the growth trajectory of the Acidity Regulator market. The complex and often varied regulatory environments across different geographical regions necessitate substantial investment in compliance and product registration, which can be a barrier for smaller players. Fluctuations in the prices of key raw materials, such as corn and sugar, used in the production of fermentation-based acidity regulators, can lead to cost volatility and impact profitability. The highly competitive nature of the market, with a large number of established and emerging manufacturers, can lead to price wars and reduced profit margins. Moreover, potential supply chain disruptions, from raw material sourcing to finished product distribution, can create bottlenecks and affect market availability.

Key Players Shaping the Acidity Regulator Market

- Archer Daniels Midland

- Cargill Incorporated

- Tate & Lyle Plc

- Hawkins Watts Ltd

- Caremoli S.P.A.

- American Tartaric Products

- Bartek Ingredients

- Jungbunzlauer Ag

- Foodchem International Corporation

- Gremount International Co. Ltd

- Jones Hamilton Co.

- Merko Group Llc

- Prinova Group L.L.C

- Purac Biochem B.V.

- Parry Enterprises India Ltd

- Univar Canada Ltd

- Weifang Ensign Industry Co. Ltd

Significant Acidity Regulator Industry Milestones

- 2019: Increased focus on sustainable sourcing and production methods for citric acid.

- 2020: Emergence of novel lactic acid applications in plant-based food products.

- 2021: Heightened demand for natural acidity regulators due to consumer preference shifts.

- 2022: Significant M&A activities aimed at market consolidation and technological integration.

- 2023: Advancements in enzyme technology for more efficient malic acid production.

- 2024: Growing investment in research for acidity regulators with enhanced antimicrobial properties.

Future Outlook for Acidity Regulator Market

The future outlook for the Acidity Regulator market remains highly optimistic, driven by sustained global demand for processed foods and beverages. Innovations leaning towards natural and sustainable sourcing will continue to shape product development, catering to evolving consumer preferences. The market is poised for further expansion in emerging economies, supported by growing disposable incomes and a strengthening food processing infrastructure. Strategic opportunities lie in the development of customized acidity regulator solutions for niche applications and the integration of advanced fermentation technologies for cost-effective and eco-friendly production. The increasing awareness of food waste reduction is also expected to drive demand for acidity regulators that enhance product shelf-life and stability.

Acidity Regulator Segmentation

-

1. Application

- 1.1. Beverages

- 1.2. Sauces, Dressings, and Condiments

- 1.3. Processed Foods

- 1.4. Bakery and Confectionary

- 1.5. Others

-

2. Type

- 2.1. Acetic Acid

- 2.2. Citric Acid

- 2.3. Lactic Acid

- 2.4. Malic Acid

- 2.5. Phosphoric Acid

- 2.6. Others

Acidity Regulator Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Acidity Regulator Regional Market Share

Geographic Coverage of Acidity Regulator

Acidity Regulator REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Beverages

- 5.1.2. Sauces, Dressings, and Condiments

- 5.1.3. Processed Foods

- 5.1.4. Bakery and Confectionary

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Acetic Acid

- 5.2.2. Citric Acid

- 5.2.3. Lactic Acid

- 5.2.4. Malic Acid

- 5.2.5. Phosphoric Acid

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Beverages

- 6.1.2. Sauces, Dressings, and Condiments

- 6.1.3. Processed Foods

- 6.1.4. Bakery and Confectionary

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Acetic Acid

- 6.2.2. Citric Acid

- 6.2.3. Lactic Acid

- 6.2.4. Malic Acid

- 6.2.5. Phosphoric Acid

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Beverages

- 7.1.2. Sauces, Dressings, and Condiments

- 7.1.3. Processed Foods

- 7.1.4. Bakery and Confectionary

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Acetic Acid

- 7.2.2. Citric Acid

- 7.2.3. Lactic Acid

- 7.2.4. Malic Acid

- 7.2.5. Phosphoric Acid

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Beverages

- 8.1.2. Sauces, Dressings, and Condiments

- 8.1.3. Processed Foods

- 8.1.4. Bakery and Confectionary

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Acetic Acid

- 8.2.2. Citric Acid

- 8.2.3. Lactic Acid

- 8.2.4. Malic Acid

- 8.2.5. Phosphoric Acid

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Beverages

- 9.1.2. Sauces, Dressings, and Condiments

- 9.1.3. Processed Foods

- 9.1.4. Bakery and Confectionary

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Acetic Acid

- 9.2.2. Citric Acid

- 9.2.3. Lactic Acid

- 9.2.4. Malic Acid

- 9.2.5. Phosphoric Acid

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Acidity Regulator Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Beverages

- 10.1.2. Sauces, Dressings, and Condiments

- 10.1.3. Processed Foods

- 10.1.4. Bakery and Confectionary

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Acetic Acid

- 10.2.2. Citric Acid

- 10.2.3. Lactic Acid

- 10.2.4. Malic Acid

- 10.2.5. Phosphoric Acid

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Archer Daniels Midland

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cargill Incorporated

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Tate & Lyle Plc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Hawkins Watts Ltd

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Caremoli S.P.A.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 American Tartaric Products

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bartek Ingredients

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Jungbunzlauer Ag

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Foodchem International Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Gremount International Co. Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jones Hamilton Co.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Merko Group Llc

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Prinova Group L.L.C

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Purac Biochem B.V.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Parry Enterprises India Ltd

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Univar Canada Ltd

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Weifang Ensign Industry Co. Ltd

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Archer Daniels Midland

List of Figures

- Figure 1: Global Acidity Regulator Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Acidity Regulator Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Acidity Regulator Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Acidity Regulator Volume (K), by Application 2025 & 2033

- Figure 5: North America Acidity Regulator Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Acidity Regulator Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Acidity Regulator Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Acidity Regulator Volume (K), by Type 2025 & 2033

- Figure 9: North America Acidity Regulator Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Acidity Regulator Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Acidity Regulator Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Acidity Regulator Volume (K), by Country 2025 & 2033

- Figure 13: North America Acidity Regulator Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Acidity Regulator Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Acidity Regulator Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Acidity Regulator Volume (K), by Application 2025 & 2033

- Figure 17: South America Acidity Regulator Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Acidity Regulator Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Acidity Regulator Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Acidity Regulator Volume (K), by Type 2025 & 2033

- Figure 21: South America Acidity Regulator Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Acidity Regulator Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Acidity Regulator Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Acidity Regulator Volume (K), by Country 2025 & 2033

- Figure 25: South America Acidity Regulator Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Acidity Regulator Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Acidity Regulator Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Acidity Regulator Volume (K), by Application 2025 & 2033

- Figure 29: Europe Acidity Regulator Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Acidity Regulator Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Acidity Regulator Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Acidity Regulator Volume (K), by Type 2025 & 2033

- Figure 33: Europe Acidity Regulator Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Acidity Regulator Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Acidity Regulator Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Acidity Regulator Volume (K), by Country 2025 & 2033

- Figure 37: Europe Acidity Regulator Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Acidity Regulator Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Acidity Regulator Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Acidity Regulator Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Acidity Regulator Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Acidity Regulator Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Acidity Regulator Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Acidity Regulator Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Acidity Regulator Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Acidity Regulator Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Acidity Regulator Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Acidity Regulator Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Acidity Regulator Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Acidity Regulator Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Acidity Regulator Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Acidity Regulator Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Acidity Regulator Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Acidity Regulator Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Acidity Regulator Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Acidity Regulator Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Acidity Regulator Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Acidity Regulator Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Acidity Regulator Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Acidity Regulator Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Acidity Regulator Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Acidity Regulator Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Acidity Regulator Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Acidity Regulator Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Acidity Regulator Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Acidity Regulator Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Acidity Regulator Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Acidity Regulator Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Acidity Regulator Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Acidity Regulator Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Acidity Regulator Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Acidity Regulator Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Acidity Regulator Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Acidity Regulator Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Acidity Regulator Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Acidity Regulator Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Acidity Regulator Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Acidity Regulator Volume K Forecast, by Country 2020 & 2033

- Table 79: China Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Acidity Regulator Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Acidity Regulator Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Acidity Regulator?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Acidity Regulator?

Key companies in the market include Archer Daniels Midland, Cargill Incorporated, Tate & Lyle Plc, Hawkins Watts Ltd, Caremoli S.P.A., American Tartaric Products, Bartek Ingredients, Jungbunzlauer Ag, Foodchem International Corporation, Gremount International Co. Ltd, Jones Hamilton Co., Merko Group Llc, Prinova Group L.L.C, Purac Biochem B.V., Parry Enterprises India Ltd, Univar Canada Ltd, Weifang Ensign Industry Co. Ltd.

3. What are the main segments of the Acidity Regulator?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Acidity Regulator," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Acidity Regulator report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Acidity Regulator?

To stay informed about further developments, trends, and reports in the Acidity Regulator, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence