Key Insights

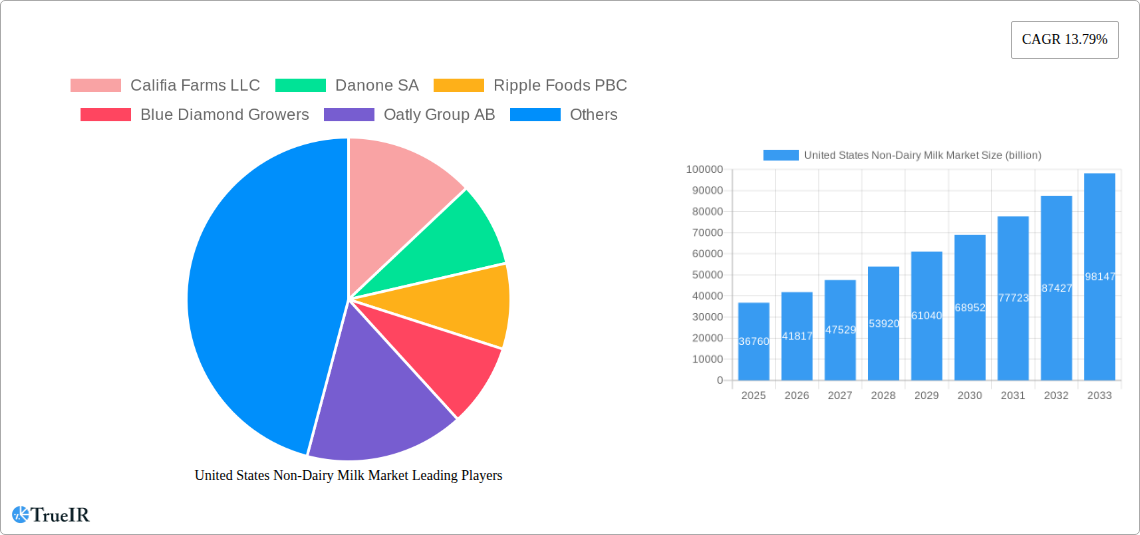

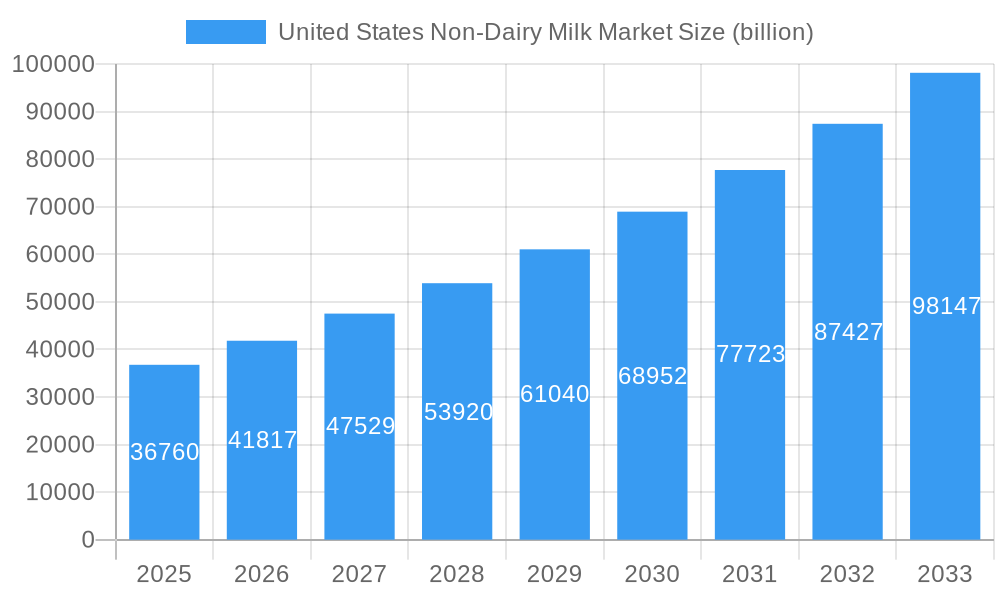

The United States Non-Dairy Milk Market is poised for significant expansion, projected to reach an estimated $36.76 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 13.79% during the forecast period of 2025-2033. A primary driver for this surge is the escalating consumer demand for healthier and more sustainable dietary alternatives, fueled by increasing awareness of lactose intolerance, dairy allergies, and the environmental impact of traditional dairy farming. The "plant-based revolution" is not merely a fleeting trend but a fundamental shift in consumer preferences, pushing innovation and product diversification across various non-dairy milk types.

United States Non-Dairy Milk Market Market Size (In Billion)

The market's dynamism is further evident in its segmentation. Oat milk and almond milk continue to dominate consumer choice, driven by their versatility and established presence. However, emerging segments like cashew milk and hemp milk are gaining traction due to their unique nutritional profiles and perceived health benefits. Distribution channels are also evolving, with off-trade channels, particularly online retail and supermarkets, experiencing substantial growth. This reflects the convenience-oriented purchasing habits of modern consumers. While the market is characterized by strong growth, potential restraints could include fluctuating raw material costs and intense competition among established players and new entrants. Nevertheless, the overall outlook remains exceptionally positive, indicating a highly attractive investment and growth landscape for the United States non-dairy milk industry.

United States Non-Dairy Milk Market Company Market Share

Explore the dynamic growth and evolving landscape of the United States non-dairy milk market, projected to reach a staggering value of over USD 15 billion by 2033. This comprehensive report delves deep into market trends, dominant segments, product innovations, key drivers, and the competitive strategies of leading players. Covering a study period from 2019 to 2033, with a base year of 2025, this analysis provides actionable insights for stakeholders navigating this rapidly expanding sector.

United States Non-Dairy Milk Market Market Structure & Competitive Landscape

The United States non-dairy milk market is characterized by a moderately concentrated structure, with a few key players holding significant market share. Innovation remains a primary driver, fueled by increasing consumer demand for healthier, sustainable, and ethically sourced alternatives to traditional dairy. Regulatory impacts, while not overtly restrictive, focus on clear labeling and nutritional transparency. Product substitutes, including other plant-based beverages and even dairy milk itself, continue to present competitive pressures. End-user segmentation reveals a broad appeal, from health-conscious individuals and lactose-intolerant consumers to environmentally aware shoppers. Mergers and acquisitions (M&A) trends are a notable aspect, indicating a drive for consolidation and expansion of product portfolios. For instance, SunOpta Inc.'s strategic acquisition of Dream® and WestSoy® plant-based beverage brands in April 2022 underscores this consolidation. The market’s concentration ratio is estimated to be between 45-55% for the top five players, with approximately 3-5 significant M&A deals annually over the historical period.

United States Non-Dairy Milk Market Market Trends & Opportunities

The United States non-dairy milk market is experiencing robust growth, driven by a confluence of factors including rising health consciousness, increased prevalence of lactose intolerance, growing environmental concerns, and a wider array of product offerings. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of over 8.5% during the forecast period of 2025–2033. Technological advancements in processing and formulation are leading to improved taste, texture, and nutritional profiles, making non-dairy milk more appealing to a broader consumer base. Consumer preferences are shifting towards plant-based diets, with a particular surge in demand for oat milk and almond milk due to their perceived health benefits and versatility.

The competitive landscape is intensifying, with established dairy giants venturing into the non-dairy segment and agile startups continuously innovating. This dynamic environment presents significant opportunities for new product development, particularly in niche categories and fortified beverages. The increasing availability across various distribution channels, from online retail to traditional supermarkets, is further boosting market penetration rates, which are expected to exceed 60% for key non-dairy milk types by 2033. The demand for unsweetened and low-sugar options is also a growing trend, aligning with the broader wellness movement. Furthermore, innovations in packaging and sustainability are becoming crucial differentiators, appealing to an increasingly eco-conscious consumer. The expansion of on-trade applications, such as in coffee shops and restaurants, also presents a significant growth avenue.

Dominant Markets & Segments in United States Non-Dairy Milk Market

The dominance within the United States non-dairy milk market is significantly influenced by specific product types and distribution channels, with Off-Trade channels leading the charge.

Dominant Product Types:

- Almond Milk: Continues to hold a substantial market share due to its established presence, mild flavor, and perceived health benefits. Its versatility in various culinary applications contributes to its sustained popularity.

- Oat Milk: Exhibits the most rapid growth trajectory, driven by its creamy texture, neutral taste, and suitability for frothing in coffee beverages. This has made it a favorite in the foodservice industry and among consumers seeking dairy-free alternatives for their daily routines.

- Soy Milk: While facing increased competition, soy milk remains a significant player due to its high protein content and long history of availability. It appeals to consumers seeking a nutritionally comparable alternative to dairy milk.

- Coconut Milk: Offers a distinct flavor profile and creamy texture, finding favor in both culinary uses and as a beverage, particularly in smoothies and exotic dishes.

- Cashew Milk and Hemp Milk: These segments, while smaller, are experiencing consistent growth as consumers seek variety and explore the unique nutritional benefits and taste profiles of these less conventional options.

Dominant Distribution Channels:

- Off-Trade: This segment is the primary driver of market growth, accounting for approximately 85% of overall sales.

- Supermarkets and Hypermarkets: Remain the largest sub-segment within Off-Trade, offering wide product selection and convenient shopping experiences for a broad consumer base.

- Online Retail: Demonstrates the fastest growth within Off-Trade. The ease of ordering, home delivery, and access to a wider range of specialty brands make online platforms increasingly crucial for market reach.

- Convenience Stores and Specialist Retailers: Cater to immediate consumption needs and niche consumer segments, respectively, contributing to overall market accessibility.

- On-Trade: While a smaller segment, the on-trade channel, which includes coffee shops, restaurants, and cafes, is a critical touchpoint for trial and brand building, particularly for oat milk due to its popularity in coffee-based beverages.

- Off-Trade: This segment is the primary driver of market growth, accounting for approximately 85% of overall sales.

The dominance of Supermarkets and Hypermarkets is driven by their extensive reach and ability to cater to household stocking needs. The accelerating growth of Online Retail is fueled by convenience and the expansion of e-commerce infrastructure across the nation. Policies promoting healthy eating and environmental sustainability indirectly bolster the demand for plant-based alternatives, further solidifying the dominance of these product types and distribution channels.

United States Non-Dairy Milk Market Product Analysis

Product innovation in the United States non-dairy milk market is primarily focused on enhancing nutritional profiles, improving taste and texture, and expanding flavor varieties. Companies are investing in research to create beverages that closely mimic the sensory experience of dairy milk, while also fortifying them with essential vitamins and minerals like Vitamin D and Calcium. The competitive advantage lies in offering unique formulations, such as unsweetened options, barista-blend varieties for superior frothing, and innovative ingredient combinations. Applications are diverse, ranging from direct consumption and use in cooking and baking to being a staple in smoothies and coffee beverages, highlighting the market's adaptability and broad consumer appeal.

Key Drivers, Barriers & Challenges in United States Non-Dairy Milk Market

Key Drivers:

- Growing Health Consciousness: A significant portion of the population is actively seeking healthier dietary options, driving demand for plant-based alternatives perceived as lower in saturated fat and cholesterol.

- Increasing Prevalence of Lactose Intolerance: A substantial percentage of the U.S. population experiences lactose intolerance, creating a direct need for dairy-free milk substitutes.

- Environmental Sustainability Concerns: Consumers are increasingly aware of the environmental impact of dairy farming, making plant-based milks a more appealing, sustainable choice.

- Product Innovation and Variety: Manufacturers are continuously introducing new flavors, textures, and fortified options, catering to diverse consumer preferences.

- Wider Availability and Accessibility: Non-dairy milk is now readily available across a broad spectrum of retail channels, from supermarkets to online platforms.

Barriers & Challenges:

- Price Sensitivity: Non-dairy milk is often priced higher than conventional dairy milk, which can be a barrier for price-conscious consumers.

- Taste and Texture Preferences: While improving, some consumers still find the taste and texture of certain non-dairy milks less appealing than dairy milk.

- Allergen Concerns: Soy and nuts, common bases for non-dairy milk, are allergens for a segment of the population, limiting their consumption options.

- Supply Chain Volatility: Dependence on agricultural commodities can lead to price fluctuations and supply chain disruptions, impacting production costs. For example, almond production is susceptible to drought conditions.

- Regulatory Scrutiny and Labeling: Evolving regulations around plant-based product labeling and ingredient claims can pose compliance challenges for manufacturers.

Growth Drivers in the United States Non-Dairy Milk Market Market

The United States non-dairy milk market is propelled by significant growth drivers, with technological advancements in product formulation playing a pivotal role. Innovations are leading to non-dairy milks with superior taste, texture, and nutritional profiles, closely mimicking dairy milk. Economic factors, such as rising disposable incomes and a growing middle class with a propensity for premium and health-conscious products, also contribute significantly. Furthermore, supportive government policies and public health initiatives that promote healthier diets and sustainable food choices indirectly foster market expansion. The increasing focus on plant-based diets, driven by wellness trends and ethical considerations, continues to be a powerful catalyst.

Challenges Impacting United States Non-Dairy Milk Market Growth

Several challenges impact the growth trajectory of the United States non-dairy milk market. Regulatory complexities surrounding plant-based product labeling and claims can create an uneven playing field and require significant compliance efforts. Supply chain issues, including the availability and price volatility of key agricultural ingredients like almonds and oats, can disrupt production and affect profitability. Competitive pressures from both established dairy brands expanding into the non-dairy space and numerous emerging plant-based alternatives are intense. Additionally, the inherent taste and texture preferences of some consumers, who remain loyal to dairy milk, present a persistent barrier to widespread adoption.

Key Players Shaping the United States Non-Dairy Milk Market Market

- Califia Farms LLC

- Danone SA

- Ripple Foods PBC

- Blue Diamond Growers

- Oatly Group AB

- Otsuka Holdings Co Ltd

- Campbell Soup Company

- SunOpta Inc

- Walmart Inc

Significant United States Non-Dairy Milk Market Industry Milestones

- October 2022: SunOpta completed the first phase of its USD 100-million sterile alternative milk plant in Midlothian, Texas, enhancing its sustainable milk and food product manufacturing capabilities.

- April 2022: Califia Farms launched an unsweetened Oat Milk specifically designed for at-home consumption and made available through natural, specialty, and grocery retailers nationwide.

- April 2022: SunOpta Inc. strategically acquired the Dream® and WestSoy® plant-based beverage brands from The Hain Celestial Group Inc., further expanding its portfolio of plant-based products. The company currently manufactures the entire WestSoy product portfolio.

Future Outlook for United States Non-Dairy Milk Market Market

The future outlook for the United States non-dairy milk market is exceptionally promising, fueled by ongoing consumer shifts towards healthier and more sustainable lifestyles. Strategic opportunities lie in further product diversification, including the development of specialized functional beverages and allergen-free options. Market penetration is expected to deepen as manufacturers continue to innovate on taste, texture, and affordability, making plant-based milks a household staple. Investments in sustainable sourcing and production will also be crucial for long-term growth and brand loyalty. The expanding online retail sector and the growing acceptance in the foodservice industry will further solidify its market position, projecting continued robust growth well into the future.

United States Non-Dairy Milk Market Segmentation

-

1. Product Type

- 1.1. Almond Milk

- 1.2. Cashew Milk

- 1.3. Coconut Milk

- 1.4. Hemp Milk

- 1.5. Oat Milk

- 1.6. Soy Milk

-

2. Distribution Channel

-

2.1. Off-Trade

- 2.1.1. Convenience Stores

- 2.1.2. Online Retail

- 2.1.3. Specialist Retailers

- 2.1.4. Supermarkets and Hypermarkets

- 2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 2.2. On-Trade

-

2.1. Off-Trade

United States Non-Dairy Milk Market Segmentation By Geography

- 1. United States

United States Non-Dairy Milk Market Regional Market Share

Geographic Coverage of United States Non-Dairy Milk Market

United States Non-Dairy Milk Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Almond Milk

- 5.1.2. Cashew Milk

- 5.1.3. Coconut Milk

- 5.1.4. Hemp Milk

- 5.1.5. Oat Milk

- 5.1.6. Soy Milk

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Off-Trade

- 5.2.1.1. Convenience Stores

- 5.2.1.2. Online Retail

- 5.2.1.3. Specialist Retailers

- 5.2.1.4. Supermarkets and Hypermarkets

- 5.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 5.2.2. On-Trade

- 5.2.1. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States Non-Dairy Milk Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Almond Milk

- 6.1.2. Cashew Milk

- 6.1.3. Coconut Milk

- 6.1.4. Hemp Milk

- 6.1.5. Oat Milk

- 6.1.6. Soy Milk

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Off-Trade

- 6.2.1.1. Convenience Stores

- 6.2.1.2. Online Retail

- 6.2.1.3. Specialist Retailers

- 6.2.1.4. Supermarkets and Hypermarkets

- 6.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 6.2.2. On-Trade

- 6.2.1. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Califia Farms LLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Danone SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Ripple Foods PBC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Blue Diamond Growers

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Oatly Group AB

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Otsuka Holdings Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Campbell Soup Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 SunOpta Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Walmart Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Califia Farms LLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Non-Dairy Milk Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Non-Dairy Milk Market Share (%) by Company 2025

List of Tables

- Table 1: United States Non-Dairy Milk Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: United States Non-Dairy Milk Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: United States Non-Dairy Milk Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: United States Non-Dairy Milk Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: United States Non-Dairy Milk Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: United States Non-Dairy Milk Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Non-Dairy Milk Market?

The projected CAGR is approximately 13.79%.

2. Which companies are prominent players in the United States Non-Dairy Milk Market?

Key companies in the market include Califia Farms LLC, Danone SA, Ripple Foods PBC, Blue Diamond Growers, Oatly Group AB, Otsuka Holdings Co Ltd, Campbell Soup Company, SunOpta Inc, Walmart Inc.

3. What are the main segments of the United States Non-Dairy Milk Market?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 36.76 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Competition from Substitute Products.

8. Can you provide examples of recent developments in the market?

October 2022: SunOpta completed the first phase of the USD 100-million sterile alternative milk plant in Midlothian to manufacture sustainable milk and food products.April 2022: Califia Farms launched an unsweetened Oat Milk designed for at-home consumption and purchase in natural, specialty, and grocery retailers.April 2022: SunOpta Inc. acquired Dream® and WestSoy® plant-based beverage brands from The Hain Celestial Group Inc. The company currently produces the entire WestSoy product portfolio.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Non-Dairy Milk Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Non-Dairy Milk Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Non-Dairy Milk Market?

To stay informed about further developments, trends, and reports in the United States Non-Dairy Milk Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence