Key Insights

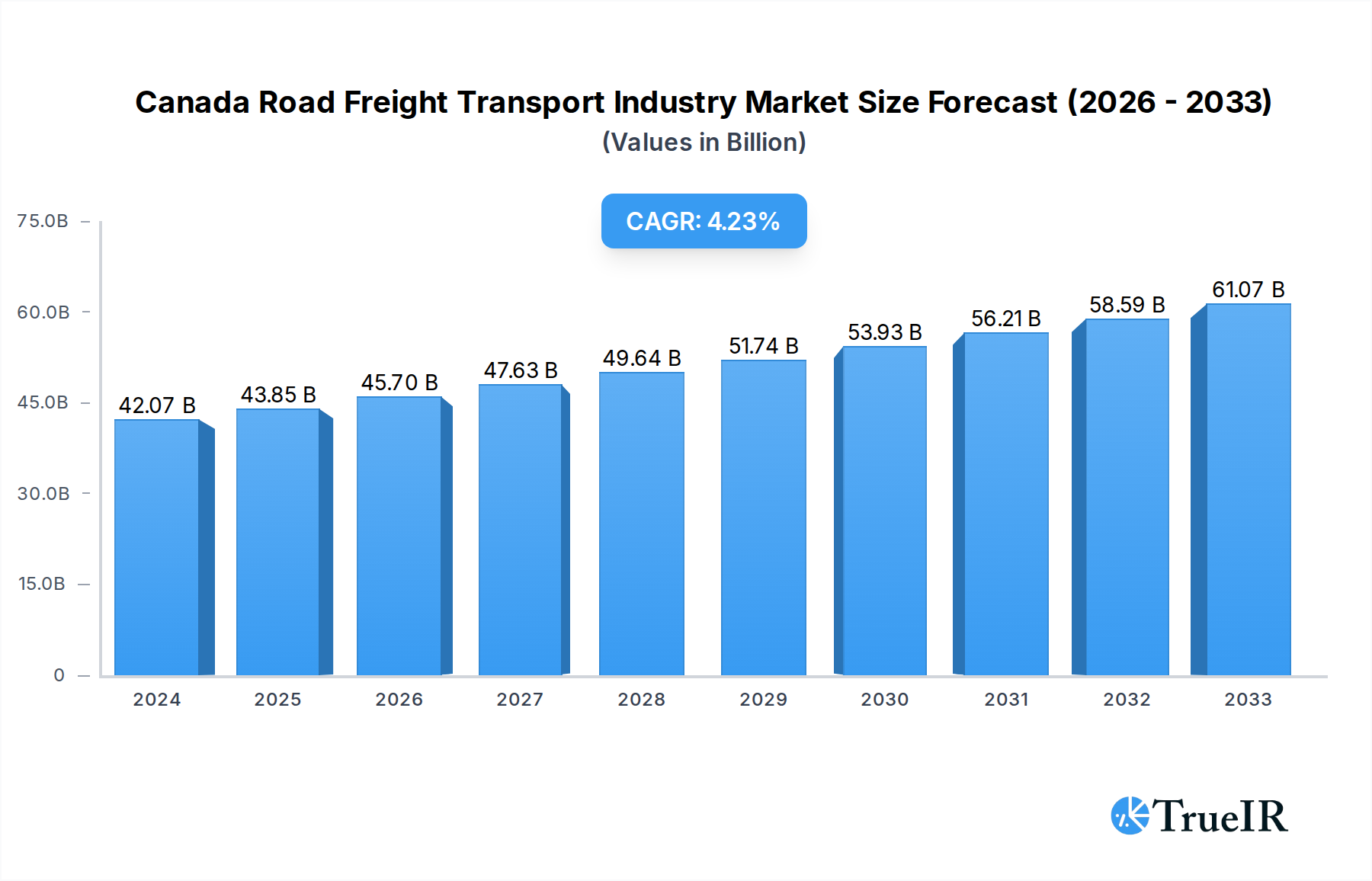

The Canadian Road Freight Transport Industry is poised for steady expansion, projecting a market size of $42.07 billion in 2024. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 4.32%, indicating a robust and consistent upward trajectory. The industry's dynamism is fueled by several key drivers, including the increasing demand for goods across diverse sectors such as e-commerce, manufacturing, and construction, all of which heavily rely on efficient road transportation. The evolving consumer behavior, characterized by a preference for faster deliveries and the burgeoning online retail landscape, directly translates into higher volumes of freight moving across Canada. Furthermore, government initiatives aimed at infrastructure development and trade facilitation are expected to create a more conducive environment for freight movement, thereby supporting the industry's expansion. The demand for both Full-Truck-Load (FTL) and Less-than-Truck-Load (LTL) services is expected to remain strong, catering to the varying needs of businesses. The increasing adoption of technology in logistics, such as advanced tracking systems and route optimization software, is also playing a crucial role in enhancing operational efficiency and reducing costs.

Canada Road Freight Transport Industry Market Size (In Billion)

While the outlook is largely positive, certain factors could present challenges. Rising fuel costs, a perennial concern for the transportation sector, could impact profitability and freight rates. Additionally, driver shortages and stringent regulatory frameworks related to emissions and working hours may pose operational hurdles. Despite these restraints, the industry's ability to adapt and innovate, coupled with the continuous demand for goods movement, is expected to ensure sustained growth. The market is segmented across various end-user industries, including Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, and Wholesale and Retail Trade, all contributing to the overall freight volume. The dominance of domestic movements is anticipated, though international freight also plays a significant role. The increasing preference for containerized shipping for efficient handling and the ongoing demand for both long and short haul services highlight the industry's versatility.

Canada Road Freight Transport Industry Company Market Share

Canada Road Freight Transport Industry Market Report: Dominant Trends, Opportunities, and Competitive Landscape (2019-2033)

This comprehensive report delves into the dynamic Canada Road Freight Transport Industry, providing an in-depth analysis of its market structure, competitive landscape, growth trends, and future outlook. Covering the historical period of 2019-2024 and a forecast period extending to 2033, with a base and estimated year of 2025, this study is an indispensable resource for stakeholders seeking to navigate this vital sector. Discover key industry developments, dominant market segments, and strategic opportunities within the Canadian trucking market, encompassing Full-Truck-Load (FTL) and Less than-Truck-Load (LTL) services, containerized and non-containerized freight, and the critical roles of agriculture, manufacturing, and wholesale & retail trade end-user industries.

Canada Road Freight Transport Industry Market Structure & Competitive Landscape

The Canada Road Freight Transport Industry exhibits a moderately concentrated market structure, with a significant presence of large, established players alongside a robust network of smaller, specialized carriers. Innovation is a key differentiator, driven by the constant pursuit of operational efficiency and cost reduction. Technology adoption, particularly in logistics management software and fleet optimization, plays a pivotal role in shaping competitive advantages. Regulatory impacts, such as evolving emissions standards and driver Hour-of-Service regulations, are significant considerations for all market participants. Product substitutes, while less prevalent in direct freight movement, can emerge in the form of intermodal transport solutions and specialized logistics services. End-user segmentation reveals distinct demands across sectors like Manufacturing, Wholesale and Retail Trade, and the burgeoning Oil and Gas industry, each requiring tailored freight solutions. Mergers and acquisitions (M&A) trends are actively reshaping the competitive landscape, with companies like Mullen Group and Ryder System Inc. demonstrating strategic expansion through acquisitions. Quantitative analysis of market concentration ratios reveals a steady consolidation in specific niches, while qualitative insights highlight the importance of network reach and service diversification.

Canada Road Freight Transport Industry Market Trends & Opportunities

The Canada Road Freight Transport Industry is projected for substantial growth, driven by robust economic activity and evolving consumer demand, with an estimated CAGR of XX% for the forecast period. The market size is expected to reach over $XXX billion by 2033. Technological shifts are profoundly impacting operations, with the integration of Artificial Intelligence (AI) in route optimization, predictive maintenance for fleets, and enhanced supply chain visibility becoming increasingly crucial. Companies like C.H. Robinson are at the forefront of this technological wave, developing innovative solutions that streamline freight scheduling and appointment management. Consumer preferences are leaning towards faster delivery times and greater transparency in shipment tracking, placing pressure on carriers to enhance their service offerings. Competitive dynamics are intensifying, characterized by a focus on sustainability initiatives, including the adoption of electric and alternative fuel vehicles, to meet growing environmental concerns and regulatory demands. The demand for specialized freight services, such as temperature-controlled transport for the food and pharmaceutical sectors, continues to expand. Opportunities abound for businesses that can leverage digital platforms to connect shippers with carriers, optimize loads, and provide end-to-end logistics solutions, thereby capturing a larger share of the Canadian logistics market. The cross-border freight sector also presents significant growth potential, facilitated by trade agreements and increasing economic integration. Furthermore, the rise of e-commerce continues to fuel demand for efficient and reliable less-than-truckload (LTL) services.

Dominant Markets & Segments in Canada Road Freight Transport Industry

The Canada Road Freight Transport Industry is characterized by several dominant markets and segments, each contributing significantly to overall market dynamics.

End User Industry:

- Wholesale and Retail Trade currently represents the largest segment, driven by the insatiable demand from e-commerce and traditional retail channels. The sheer volume of goods requiring movement across the country makes this sector a consistent driver of Canadian freight volumes.

- Manufacturing remains a cornerstone, with the production and distribution of finished goods and raw materials underpinning a substantial portion of road freight. Industries such as automotive, machinery, and consumer goods are particularly reliant on efficient trucking services.

- Construction significantly impacts the industry, especially during peak building seasons, requiring the transport of heavy equipment, materials like lumber and cement, and prefabricated components.

- Oil and Gas and Mining and Quarrying sectors, while cyclical, generate immense demand for specialized heavy-haul transportation of equipment and extracted resources, particularly in Western Canada.

- Agriculture, Fishing, and Forestry also contribute, requiring the movement of raw produce, harvested timber, and processed goods, often with specific temperature-controlled requirements.

Destination:

- Domestic freight movement constitutes the largest share, reflecting the vast geographical expanse of Canada and the need to connect production centers with consumer markets nationwide.

- International freight, particularly cross-border trade with the United States, represents a substantial and growing segment, facilitated by robust trade relationships.

Truckload Specification:

- Full-Truck-Load (FTL) services are paramount for large, single-shipper loads, offering efficiency and dedicated capacity. This segment is vital for manufacturers and large distributors.

- Less than-Truck-Load (LTL) services are experiencing significant growth due to the rise of e-commerce and the increasing number of smaller shipments from various businesses. This segment offers flexibility and cost-effectiveness for smaller volumes.

Containerization:

- Containerized freight is increasingly important, especially for international shipments and intermodal connections, providing standardized handling and security.

- Non-Containerized freight remains crucial for oversized or specialized cargo not suited for standard containers.

Distance:

- Long Haul routes are critical for connecting distant production hubs with major consumption centers across Canada, forming the backbone of national logistics networks.

- Short Haul services are essential for regional distribution, last-mile delivery, and connecting with larger freight hubs.

Goods Configuration:

- Solid Goods constitute the majority of road freight, encompassing a wide array of manufactured products, consumer goods, and raw materials.

- Fluid Goods, transported via tankers, represent a significant but more specialized segment, primarily serving the energy and chemical industries.

Temperature Control:

- Non-Temperature Controlled freight remains the dominant category, covering general merchandise and non-perishable goods.

- Temperature Controlled transport is a high-growth segment, crucial for perishable goods, pharmaceuticals, and sensitive chemicals, demanding specialized equipment and stringent handling protocols.

Canada Road Freight Transport Industry Product Analysis

The Canada Road Freight Transport Industry is increasingly defined by service innovations focused on efficiency, visibility, and sustainability. Companies are investing in advanced logistics management systems powered by AI for route optimization, load consolidation, and predictive analytics, thereby enhancing freight efficiency and reducing transit times. The deployment of telematics and IoT devices offers real-time shipment tracking and condition monitoring, particularly vital for temperature-controlled goods and high-value cargo. Competitive advantages are being built on offering specialized services, such as expedited FTL and LTL solutions, and expanding intermodal capabilities. The industry is also witnessing a push towards greener logistics, with the introduction of electric and alternative fuel vehicles aimed at reducing the carbon footprint of Canadian trucking. These product innovations are directly aligned with market demands for more reliable, cost-effective, and environmentally responsible freight solutions.

Key Drivers, Barriers & Challenges in Canada Road Freight Transport Industry

Key Drivers: The Canada Road Freight Transport Industry is propelled by several key drivers. Economic growth, particularly in sectors like manufacturing and retail, directly translates to increased freight demand. Technological advancements, including AI-driven route optimization and advanced fleet management systems, enhance efficiency and reduce operating costs. Government policies supporting infrastructure development and trade liberalization also provide a significant impetus. The burgeoning e-commerce sector is a relentless driver, necessitating faster and more flexible delivery services.

Barriers & Challenges: Despite the growth, the industry faces considerable challenges. A persistent shortage of qualified truck drivers represents a significant operational hurdle, impacting capacity and increasing labor costs. Regulatory complexities, including varying provincial regulations and stringent emissions standards, add to operational burdens. Fluctuations in fuel prices can drastically impact profitability, as fuel costs are a major component of operational expenses. Supply chain disruptions, whether due to weather events, labor disputes, or global unforeseen circumstances, pose risks to timely deliveries and can lead to increased transportation costs. The high capital investment required for fleet modernization and technology adoption also presents a barrier for smaller operators.

Growth Drivers in the Canada Road Freight Transport Industry Market

Several key factors are driving growth in the Canada Road Freight Transport Industry Market. Technologically, the adoption of AI in logistics and advanced telematics is revolutionizing route planning, fuel efficiency, and predictive maintenance, leading to significant operational improvements. Economically, robust demand from sectors like wholesale and retail trade and the continued expansion of e-commerce are creating sustained freight volumes. Government initiatives aimed at improving infrastructure, such as road and bridge upgrades, facilitate smoother and faster transportation. Furthermore, increasing consumer expectations for rapid delivery times are compelling carriers to invest in capacity and optimize their networks. The growing emphasis on sustainable logistics and the transition towards electric and alternative fuel vehicles also presents a significant growth avenue.

Challenges Impacting Canada Road Freight Transport Industry Growth

The Canada Road Freight Transport Industry faces multifaceted challenges that can impede growth. A chronic shortage of skilled truck drivers remains a critical issue, impacting service availability and driving up labor costs. Regulatory complexities and varying provincial compliance requirements add layers of operational difficulty. Volatile fuel prices continue to pose a significant threat to profitability, as they are a major expenditure for trucking companies. Supply chain disruptions, including port congestion and labor disputes, can lead to significant delays and increased costs. Furthermore, the substantial capital investment required for fleet modernization, including the adoption of greener technologies and advanced IT systems, presents a barrier, particularly for smaller and medium-sized enterprises. Intense competition within the market also exerts pressure on profit margins.

Key Players Shaping the Canada Road Freight Transport Industry Market

- XPO Inc

- Mullen Group

- DHL Group

- Day & Ross

- Yellow Corporation

- FedEx

- United Parcel Service of America Inc (UPS)

- C H Robinson

- J B Hunt Transport Inc

- Ryder System Inc

Significant Canada Road Freight Transport Industry Industry Milestones

- February 2024: C.H. Robinson has developed a new technology that creates a major efficiency in freight shipping: removing the work of scheduling an appointment at the place where a load needs to be picked up and scheduling another appointment where the load needs to be delivered. The technology also uses artificial intelligence to determine the optimal appointment, based on transit-time data from C.H. Robinson’s millions of shipments across 300,000 shipping lanes.

- January 2024: Mullen Group Ltd has entered into a letter of intent (LOI) to acquire Richmond, British Columbia-based ContainerWorld Forwarding Services Inc. and its operating subsidiaries. The transaction will close in the second quarter of 2024, subject to regulatory approval and final closing conditions. ContainerWorld will operate within Mullen Group's Logistics & Warehousing segment ("L&W segment") and it is expected to generate annualized revenue of approximately USD 150 million.

- October 2023: Ryder System has entered into a definitive agreement to acquire IFS Holdings, known as Impact Fulfillment Services. The 3PL provides a range of services, including contract packaging and manufacturing, warehousing and more. The deal aims to expand Ryder’s supply chain services by adding 15 operations across nine states, involving California, Florida, Georgia, Illinois, North Carolina, Ohio, Pennsylvania, Texas and Utah.

Future Outlook for Canada Road Freight Transport Industry Market

The future outlook for the Canada Road Freight Transport Industry is characterized by sustained growth and ongoing transformation. Key growth catalysts include the continued expansion of e-commerce, which will further drive demand for efficient LTL and last-mile delivery services. Strategic opportunities lie in the widespread adoption of AI and machine learning for advanced supply chain optimization, predictive logistics, and enhanced customer experience. The industry will witness a significant push towards sustainability, with increased investment in electric and alternative fuel fleets to meet environmental regulations and corporate social responsibility goals. Consolidation through M&A activities is expected to continue as larger players seek to expand their service offerings and geographical reach. The market potential for specialized temperature-controlled freight and intermodal solutions remains high, catering to evolving consumer and industrial needs. Innovation in freight visibility and data analytics will be paramount for carriers to maintain a competitive edge in this dynamic sector.

Canada Road Freight Transport Industry Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Destination

- 2.1. Domestic

- 2.2. International

-

3. Truckload Specification

- 3.1. Full-Truck-Load (FTL)

- 3.2. Less than-Truck-Load (LTL)

-

4. Containerization

- 4.1. Containerized

- 4.2. Non-Containerized

-

5. Distance

- 5.1. Long Haul

- 5.2. Short Haul

-

6. Goods Configuration

- 6.1. Fluid Goods

- 6.2. Solid Goods

-

7. Temperature Control

- 7.1. Non-Temperature Controlled

Canada Road Freight Transport Industry Segmentation By Geography

- 1. Canada

Canada Road Freight Transport Industry Regional Market Share

Geographic Coverage of Canada Road Freight Transport Industry

Canada Road Freight Transport Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Destination

- 5.2.1. Domestic

- 5.2.2. International

- 5.3. Market Analysis, Insights and Forecast - by Truckload Specification

- 5.3.1. Full-Truck-Load (FTL)

- 5.3.2. Less than-Truck-Load (LTL)

- 5.4. Market Analysis, Insights and Forecast - by Containerization

- 5.4.1. Containerized

- 5.4.2. Non-Containerized

- 5.5. Market Analysis, Insights and Forecast - by Distance

- 5.5.1. Long Haul

- 5.5.2. Short Haul

- 5.6. Market Analysis, Insights and Forecast - by Goods Configuration

- 5.6.1. Fluid Goods

- 5.6.2. Solid Goods

- 5.7. Market Analysis, Insights and Forecast - by Temperature Control

- 5.7.1. Non-Temperature Controlled

- 5.8. Market Analysis, Insights and Forecast - by Region

- 5.8.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Canada Road Freight Transport Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Agriculture, Fishing, and Forestry

- 6.1.2. Construction

- 6.1.3. Manufacturing

- 6.1.4. Oil and Gas, Mining and Quarrying

- 6.1.5. Wholesale and Retail Trade

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Destination

- 6.2.1. Domestic

- 6.2.2. International

- 6.3. Market Analysis, Insights and Forecast - by Truckload Specification

- 6.3.1. Full-Truck-Load (FTL)

- 6.3.2. Less than-Truck-Load (LTL)

- 6.4. Market Analysis, Insights and Forecast - by Containerization

- 6.4.1. Containerized

- 6.4.2. Non-Containerized

- 6.5. Market Analysis, Insights and Forecast - by Distance

- 6.5.1. Long Haul

- 6.5.2. Short Haul

- 6.6. Market Analysis, Insights and Forecast - by Goods Configuration

- 6.6.1. Fluid Goods

- 6.6.2. Solid Goods

- 6.7. Market Analysis, Insights and Forecast - by Temperature Control

- 6.7.1. Non-Temperature Controlled

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 XPO Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mullen Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DHL Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Day & Ross

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Yellow Corporatio

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FedEx

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Parcel Service of America Inc (UPS)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 C H Robinson

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 J B Hunt Transport Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Ryder System Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 XPO Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Road Freight Transport Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Road Freight Transport Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Road Freight Transport Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: Canada Road Freight Transport Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 3: Canada Road Freight Transport Industry Revenue billion Forecast, by Truckload Specification 2020 & 2033

- Table 4: Canada Road Freight Transport Industry Revenue billion Forecast, by Containerization 2020 & 2033

- Table 5: Canada Road Freight Transport Industry Revenue billion Forecast, by Distance 2020 & 2033

- Table 6: Canada Road Freight Transport Industry Revenue billion Forecast, by Goods Configuration 2020 & 2033

- Table 7: Canada Road Freight Transport Industry Revenue billion Forecast, by Temperature Control 2020 & 2033

- Table 8: Canada Road Freight Transport Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 9: Canada Road Freight Transport Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 10: Canada Road Freight Transport Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 11: Canada Road Freight Transport Industry Revenue billion Forecast, by Truckload Specification 2020 & 2033

- Table 12: Canada Road Freight Transport Industry Revenue billion Forecast, by Containerization 2020 & 2033

- Table 13: Canada Road Freight Transport Industry Revenue billion Forecast, by Distance 2020 & 2033

- Table 14: Canada Road Freight Transport Industry Revenue billion Forecast, by Goods Configuration 2020 & 2033

- Table 15: Canada Road Freight Transport Industry Revenue billion Forecast, by Temperature Control 2020 & 2033

- Table 16: Canada Road Freight Transport Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Road Freight Transport Industry?

The projected CAGR is approximately 4.32%.

2. Which companies are prominent players in the Canada Road Freight Transport Industry?

Key companies in the market include XPO Inc, Mullen Group, DHL Group, Day & Ross, Yellow Corporatio, FedEx, United Parcel Service of America Inc (UPS), C H Robinson, J B Hunt Transport Inc, Ryder System Inc.

3. What are the main segments of the Canada Road Freight Transport Industry?

The market segments include End User Industry, Destination, Truckload Specification, Containerization, Distance, Goods Configuration, Temperature Control.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.07 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing production of chemical and allied products driving the market4.; Rising demand for green warehouses.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; Stringent Rules and Regulations4.; Higher Costs.

8. Can you provide examples of recent developments in the market?

February 2024: C.H. Robinson has developed a new technology that creates a major efficiency in freight shipping: removing the work of scheduling an appointment at the place where a load needs to be picked up and scheduling another appointment where the load needs to be delivered. The technology also uses artificial intelligence to determine the optimal appointment, based on transit-time data from C.H. Robinson’s millions of shipments across 300,000 shipping lanes.January 2024: Mullen Group Ltd has entered into a letter of intent (LOI) to acquire Richmond, British Columbia-based ContainerWorld Forwarding Services Inc. and its operating subsidiaries. The transaction will close in the second quarter of 2024, subject to regulatory approval and final closing conditions. ContainerWorld will operate within Mullen Group's Logistics & Warehousing segment ("L&W segment") and it is expected to generate annualized revenue of approximately USD 150 million.October 2023: Ryder System has entered into a definitive agreement to acquire IFS Holdings, known as Impact Fulfillment Services. The 3PL provides a range of services, including contract packaging and manufacturing, warehousing and more. The deal aims to expand Ryder’s supply chain services by adding 15 operations across nine states, involving California, Florida, Georgia, Illinois, North Carolina, Ohio, Pennsylvania, Texas and Utah.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Road Freight Transport Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Road Freight Transport Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Road Freight Transport Industry?

To stay informed about further developments, trends, and reports in the Canada Road Freight Transport Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence