Key Insights

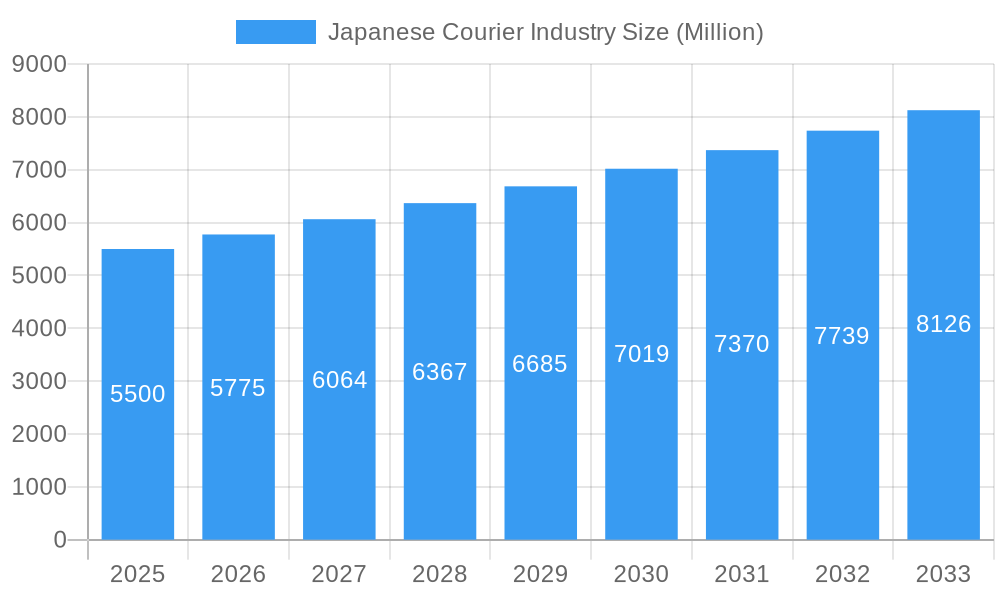

The Japanese Courier Industry is set for significant expansion, projected to reach a market size of 30.8 billion by 2025. Driven by a Compound Annual Growth Rate (CAGR) of 12.21%, the market is expected to surpass 7.3 billion by 2033. This growth is largely propelled by the e-commerce surge and the increasing demand for efficient logistics solutions across various sectors.

Japanese Courier Industry Market Size (In Billion)

Key growth drivers include the booming e-commerce sector, the rise of B2C and C2C models for smaller shipments, and the escalating needs of the healthcare and manufacturing industries for reliable delivery services.

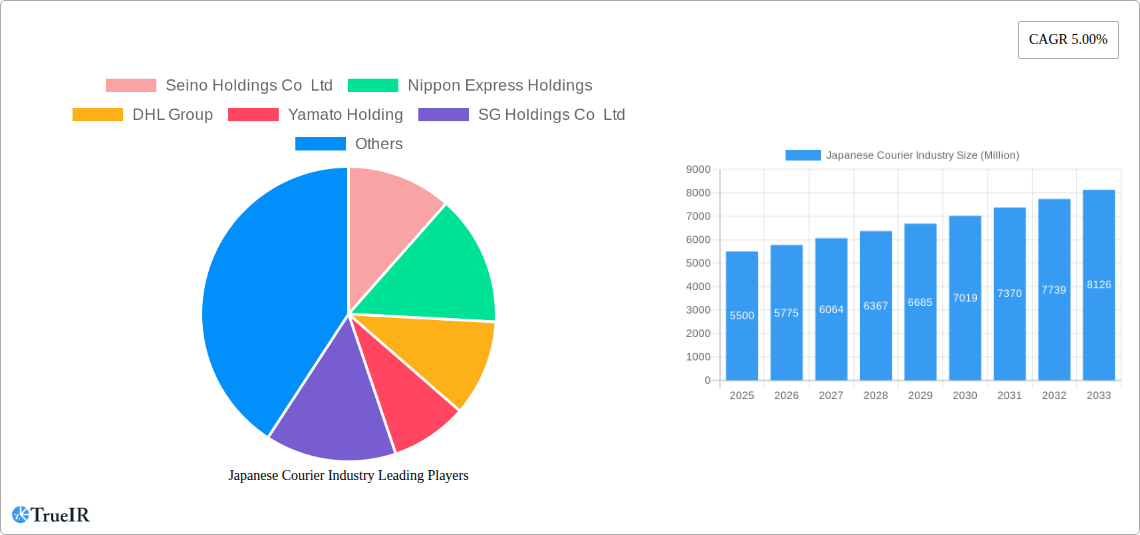

Japanese Courier Industry Company Market Share

Challenges such as rising operational costs, stringent environmental regulations, and the logistical complexities of delivering to remote areas may temper growth. However, ongoing advancements in tracking technologies, route optimization, and strategic partnerships are expected to mitigate these restraints.

This comprehensive market research report offers an in-depth analysis of the Japanese Courier Industry, including market size, growth projections, key trends, and competitive landscape.

Japanese Courier Industry Market Structure & Competitive Landscape

The Japanese courier industry is characterized by a moderately concentrated market, with a few dominant players like Seino Holdings Co Ltd, Nippon Express Holdings, DHL Group, Yamato Holding, SG Holdings Co Ltd, FedEx, UPS, and Japan Post Holdings Co Ltd commanding a significant share. Innovation is a key driver, fueled by the adoption of advanced logistics technologies, automation, and sustainable practices to meet evolving customer demands. Regulatory frameworks, particularly those concerning labor, environmental standards, and cross-border trade, play a crucial role in shaping operational strategies and market entry. The threat of product substitutes, such as on-demand delivery platforms and in-house logistics solutions, is present but is countered by the comprehensive service offerings of established courier companies. End-user segmentation is diverse, with E-commerce, Manufacturing, and Wholesale & Retail Trade (Offline) representing major segments. Mergers and acquisitions (M&A) are a notable trend, with an estimated X Million in M&A deal volume observed during the historical period, aimed at expanding service portfolios, geographical reach, and operational efficiencies. Concentration ratios are estimated to be above 60% for the top 5 players, indicating a consolidated landscape.

Japanese Courier Industry Market Trends & Opportunities

The Japanese courier industry is poised for substantial growth, driven by a projected Compound Annual Growth Rate (CAGR) of approximately 5-7% throughout the forecast period of 2025-2033. The market size is estimated to reach over XX Trillion Japanese Yen by 2033, a significant increase from its current valuation of approximately XX Trillion Japanese Yen in 2025. This expansion is underpinned by robust technological shifts, with increasing adoption of Artificial Intelligence (AI) for route optimization, robotics for warehouse automation, and advanced tracking systems for enhanced visibility and efficiency. Consumer preferences are rapidly evolving, with a growing demand for faster delivery speeds, more flexible delivery options, and sustainable logistics solutions. The rise of e-commerce continues to be a primary growth catalyst, driving higher shipment volumes and necessitating more sophisticated last-mile delivery networks. Competitive dynamics are intensifying, with established players investing heavily in digitalization and service innovation to maintain their market share, while new entrants and specialized service providers are carving out niches. Market penetration rates for express delivery services are expected to surpass 70% by 2030, highlighting a significant shift towards premium offerings. The increasing focus on supply chain resilience and the need for efficient inventory management further present significant opportunities for courier companies to offer value-added services.

Dominant Markets & Segments in Japanese Courier Industry

The Domestic segment is expected to continue its dominance within the Japanese courier industry, driven by the country's dense population and robust internal trade. This dominance is further amplified by the widespread adoption of Business-to-Consumer (B2C) models, largely fueled by the burgeoning e-commerce market. The Road mode of transport remains the backbone of domestic logistics, owing to Japan's extensive and well-maintained road network. Light Weight Shipments constitute a significant portion of the market volume, reflecting the prevalence of smaller parcel deliveries, particularly from online retail.

- Destination: Domestic logistics is the leading segment, projected to account for over 75% of the total market value by 2033. This is attributed to strong intra-Japan trade and the convenience of local delivery.

- Model: Business-to-Consumer (B2C) is the fastest-growing model, with an estimated market share of over 60% in 2025, projected to reach over 70% by 2033. The sustained growth of e-commerce is the primary driver.

- Shipment Weight: Light Weight Shipments are expected to maintain their lead, driven by the increasing volume of online purchases for smaller goods and consumer electronics.

- Mode Of Transport: Road transport remains dominant for domestic deliveries, estimated to handle over 80% of all shipments due to its accessibility and cost-effectiveness.

- End User Industry: E-Commerce is the most significant end-user industry, expected to contribute over 40% to the total market revenue by 2033. This is followed by Wholesale and Retail Trade (Offline), which is adapting to omni-channel strategies.

- Speed Of Delivery: While Express delivery is gaining traction due to e-commerce demands, Non-Express services still hold a substantial market share due to cost-effectiveness for less time-sensitive shipments.

- International courier services are experiencing steady growth, particularly with the expansion of Japanese businesses into global markets and increased inbound tourism, though it represents a smaller segment compared to domestic.

Japanese Courier Industry Product Analysis

The Japanese courier industry is witnessing continuous product innovation focused on enhancing efficiency, speed, and customer experience. Key advancements include the integration of AI and machine learning for sophisticated route optimization, reducing delivery times and fuel consumption. The deployment of advanced tracking technologies, such as IoT sensors and RFID chips, provides real-time visibility of shipments, improving security and customer satisfaction. Furthermore, there is a growing emphasis on eco-friendly delivery solutions, including the adoption of electric vehicles and optimized packaging to minimize environmental impact. These innovations offer competitive advantages by enabling faster, more reliable, and sustainable logistics services, meeting the evolving demands of both businesses and consumers.

Key Drivers, Barriers & Challenges in Japanese Courier Industry

Key Drivers: The Japanese courier industry is propelled by several significant drivers. The relentless growth of the e-commerce sector is a primary catalyst, increasing shipment volumes exponentially. Technological advancements, including AI for route optimization, robotics for warehouse automation, and real-time tracking, are enhancing operational efficiency. Government initiatives promoting digitalization and sustainable logistics also provide a supportive environment. Economic growth and increasing consumer disposable income further fuel demand for courier services.

Barriers & Challenges: Despite robust growth, the industry faces considerable challenges. An aging workforce and labor shortages pose a significant constraint on operational capacity, impacting delivery speeds and costs. Intense competition among established players and the emergence of new, agile competitors exert downward pressure on pricing. Regulatory complexities, particularly concerning labor laws and environmental compliance, can increase operational costs. Furthermore, disruptions in global supply chains, such as port congestion and geopolitical events, can impact international express services. The cost of implementing new technologies and maintaining sophisticated infrastructure also presents a barrier for smaller players.

Growth Drivers in the Japanese Courier Industry Market

The Japanese courier industry's growth is primarily driven by the insatiable demand from the e-commerce sector, which continues to expand at an accelerated pace, leading to higher parcel volumes and a need for faster, more reliable delivery. Technological advancements are also pivotal; the adoption of AI and machine learning for intelligent route planning and demand forecasting, alongside automation in warehousing and sorting facilities, significantly boosts operational efficiency and reduces costs. Furthermore, increasing consumer expectations for same-day or next-day delivery services are pushing courier companies to innovate and offer premium express options. Government support for digital transformation and the development of advanced logistics infrastructure, including smart ports and efficient road networks, further catalyze industry expansion and enhance the overall competitiveness of the Japanese logistics ecosystem.

Challenges Impacting Japanese Courier Industry Growth

The Japanese courier industry grapples with significant challenges that impede its growth trajectory. Labor shortages, exacerbated by an aging population and demanding working conditions, directly impact the capacity to handle increasing shipment volumes, leading to potential delivery delays and increased operational costs. Intense competition from both domestic and international players, including new entrants with innovative business models, puts constant pressure on profit margins and necessitates continuous investment in service improvement and technological upgrades. Navigating complex regulatory environments, particularly those related to labor, environmental protection, and cross-border trade, adds to operational complexities and costs. Furthermore, the susceptibility of global supply chains to disruptions, such as natural disasters and geopolitical tensions, can significantly affect international express services, posing risks to timely deliveries and overall market stability.

Key Players Shaping the Japanese Courier Industry Market

- Seino Holdings Co Ltd

- Nippon Express Holdings

- DHL Group

- Yamato Holding

- SG Holdings Co Ltd

- FedEx

- United Parcel Service of America Inc (UPS)

- Japan Post Holdings Co Ltd

- Ecohai

Significant Japanese Courier Industry Industry Milestones

- June 2023: Nippon Express Co. Ltd, a group company of NIPPON EXPRESS HOLDINGS INC., was commissioned by Shandong Port Shipping Group Co. Ltd (SPGS) to serve as its sole agent in Japan and operate container terminals in Tokyo, Yokohama, Osaka, and Kobe, enhancing its port logistics capabilities.

- March 2023: UPS entered a strategic partnership with Google Cloud to leverage advanced tracking technologies, including radio-frequency identification (RFID) chips on packages, for enhanced operational visibility and efficiency.

- March 2023: Colowide MD Co. Ltd and Yamato Transport Co. Ltd formed an agreement to visualize and optimize the entire supply chain of the Colowide Group, aiming for improved operational efficiency across its multiple restaurant brands.

Future Outlook for Japanese Courier Industry Market

The future outlook for the Japanese courier industry is exceptionally promising, driven by continued technological integration and evolving consumer demands. The persistent growth of e-commerce will remain a foundational pillar, necessitating further advancements in last-mile delivery solutions, including drone delivery and autonomous vehicles, to enhance speed and efficiency. The industry is expected to see a greater emphasis on sustainability, with companies investing in electric fleets, optimized packaging, and carbon-neutral logistics strategies to meet environmental regulations and consumer expectations. Furthermore, the integration of advanced data analytics and AI will enable hyper-personalized delivery services, predictive logistics, and more resilient supply chains. Strategic collaborations and potential mergers will continue to shape the competitive landscape, as companies seek to expand their service offerings and geographical reach. The market is poised for continued innovation, promising a more efficient, sustainable, and customer-centric logistics ecosystem.

Japanese Courier Industry Segmentation

-

1. Destination

- 1.1. Domestic

- 1.2. International

-

2. Speed Of Delivery

- 2.1. Express

- 2.2. Non-Express

-

3. Model

- 3.1. Business-to-Business (B2B)

- 3.2. Business-to-Consumer (B2C)

- 3.3. Consumer-to-Consumer (C2C)

-

4. Shipment Weight

- 4.1. Heavy Weight Shipments

- 4.2. Light Weight Shipments

- 4.3. Medium Weight Shipments

-

5. Mode Of Transport

- 5.1. Air

- 5.2. Road

- 5.3. Others

-

6. End User Industry

- 6.1. E-Commerce

- 6.2. Financial Services (BFSI)

- 6.3. Healthcare

- 6.4. Manufacturing

- 6.5. Primary Industry

- 6.6. Wholesale and Retail Trade (Offline)

- 6.7. Others

Japanese Courier Industry Segmentation By Geography

- 1. Japan

Japanese Courier Industry Regional Market Share

Geographic Coverage of Japanese Courier Industry

Japanese Courier Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 5.1.1. Domestic

- 5.1.2. International

- 5.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 5.2.1. Express

- 5.2.2. Non-Express

- 5.3. Market Analysis, Insights and Forecast - by Model

- 5.3.1. Business-to-Business (B2B)

- 5.3.2. Business-to-Consumer (B2C)

- 5.3.3. Consumer-to-Consumer (C2C)

- 5.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 5.4.1. Heavy Weight Shipments

- 5.4.2. Light Weight Shipments

- 5.4.3. Medium Weight Shipments

- 5.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 5.5.1. Air

- 5.5.2. Road

- 5.5.3. Others

- 5.6. Market Analysis, Insights and Forecast - by End User Industry

- 5.6.1. E-Commerce

- 5.6.2. Financial Services (BFSI)

- 5.6.3. Healthcare

- 5.6.4. Manufacturing

- 5.6.5. Primary Industry

- 5.6.6. Wholesale and Retail Trade (Offline)

- 5.6.7. Others

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 6. Japanese Courier Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 6.1.1. Domestic

- 6.1.2. International

- 6.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 6.2.1. Express

- 6.2.2. Non-Express

- 6.3. Market Analysis, Insights and Forecast - by Model

- 6.3.1. Business-to-Business (B2B)

- 6.3.2. Business-to-Consumer (B2C)

- 6.3.3. Consumer-to-Consumer (C2C)

- 6.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 6.4.1. Heavy Weight Shipments

- 6.4.2. Light Weight Shipments

- 6.4.3. Medium Weight Shipments

- 6.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 6.5.1. Air

- 6.5.2. Road

- 6.5.3. Others

- 6.6. Market Analysis, Insights and Forecast - by End User Industry

- 6.6.1. E-Commerce

- 6.6.2. Financial Services (BFSI)

- 6.6.3. Healthcare

- 6.6.4. Manufacturing

- 6.6.5. Primary Industry

- 6.6.6. Wholesale and Retail Trade (Offline)

- 6.6.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Seino Holdings Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Nippon Express Holdings

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DHL Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yamato Holding

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 SG Holdings Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FedEx

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Parcel Service of America Inc (UPS)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Japan Post Holdings Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ecohai

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Seino Holdings Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japanese Courier Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Japanese Courier Industry Share (%) by Company 2025

List of Tables

- Table 1: Japanese Courier Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 2: Japanese Courier Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 3: Japanese Courier Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 4: Japanese Courier Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 5: Japanese Courier Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 6: Japanese Courier Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 7: Japanese Courier Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Japanese Courier Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 9: Japanese Courier Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 10: Japanese Courier Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 11: Japanese Courier Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 12: Japanese Courier Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 13: Japanese Courier Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 14: Japanese Courier Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japanese Courier Industry?

The projected CAGR is approximately 12.21%.

2. Which companies are prominent players in the Japanese Courier Industry?

Key companies in the market include Seino Holdings Co Ltd, Nippon Express Holdings, DHL Group, Yamato Holding, SG Holdings Co Ltd, FedEx, United Parcel Service of America Inc (UPS), Japan Post Holdings Co Ltd, Ecohai.

3. What are the main segments of the Japanese Courier Industry?

The market segments include Destination, Speed Of Delivery, Model, Shipment Weight, Mode Of Transport, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Exhibitions and Conferences are driving the market; Sports Events are driving the market growth.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Lack of Skilled Labor.

8. Can you provide examples of recent developments in the market?

June 2023: Nippon Express Co. Ltd, a group company of NIPPON EXPRESS HOLDINGS INC., was commissioned by Shandong Port Shipping Group Co. Ltd (hereinafter, SPGS), a shipping company based in Shandong Province, China, to serve as its sole agent in Japan and to operate container terminals in Tokyo, Yokohama, Osaka, and Kobe. These operations began with shipments arriving in Yokohama on December 20, 2022.March 2023: UPS entered a partnership with Google Cloud, where Google will help UPS by putting radio-frequency identification chips on packages to track them efficiently.March 2023: Colowide MD Co. Ltd, which oversees merchandising for the Colowide Group, and Yamato Transport Co. Ltd entered an agreement. The two companies will promote the visualization and optimization of the entire supply chain of Colowide Group, which operates multiple brands such as Gyu-Kaku, Kappa Sushi, and OOTOYA.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japanese Courier Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japanese Courier Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japanese Courier Industry?

To stay informed about further developments, trends, and reports in the Japanese Courier Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence