Key Insights

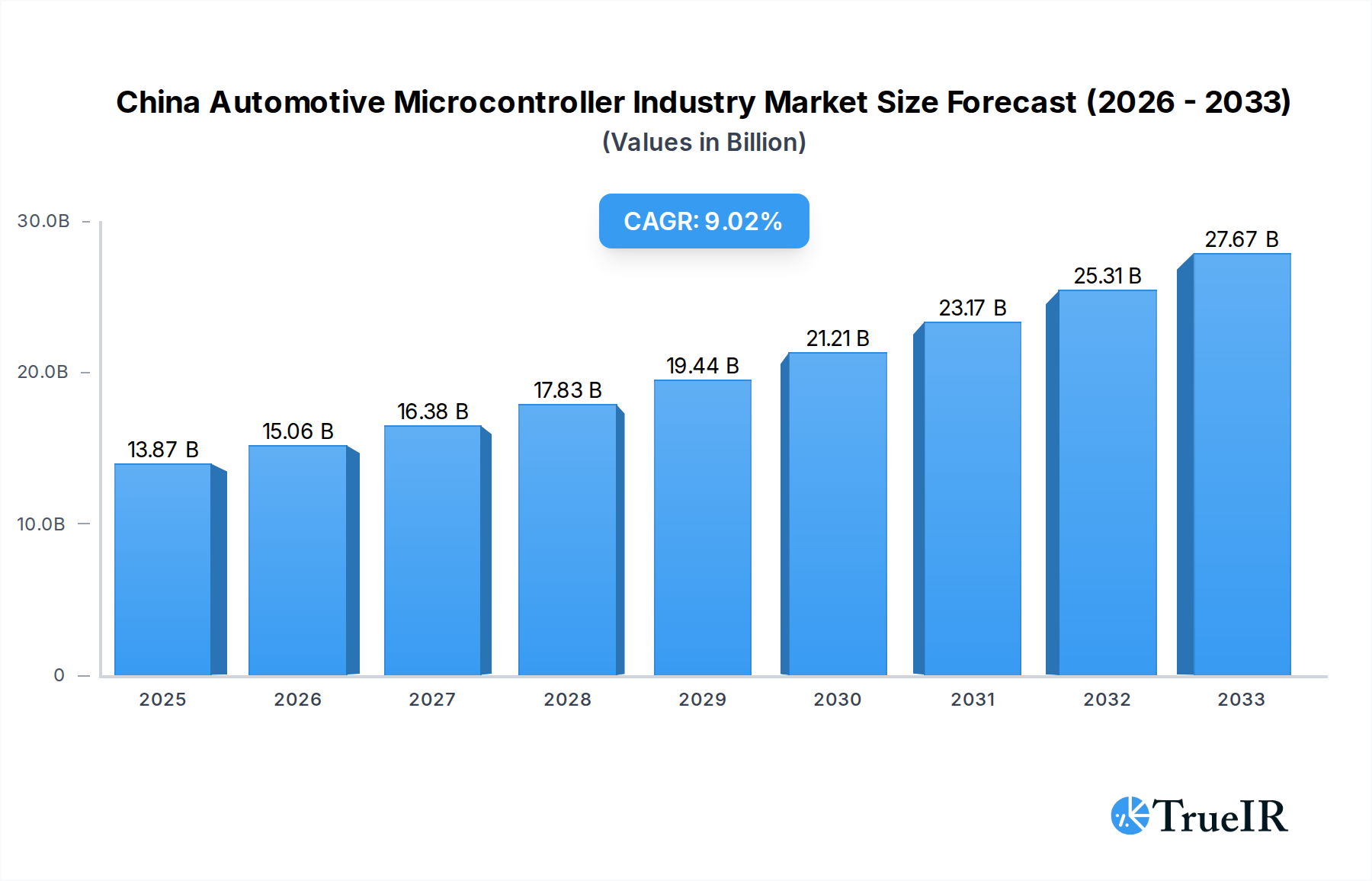

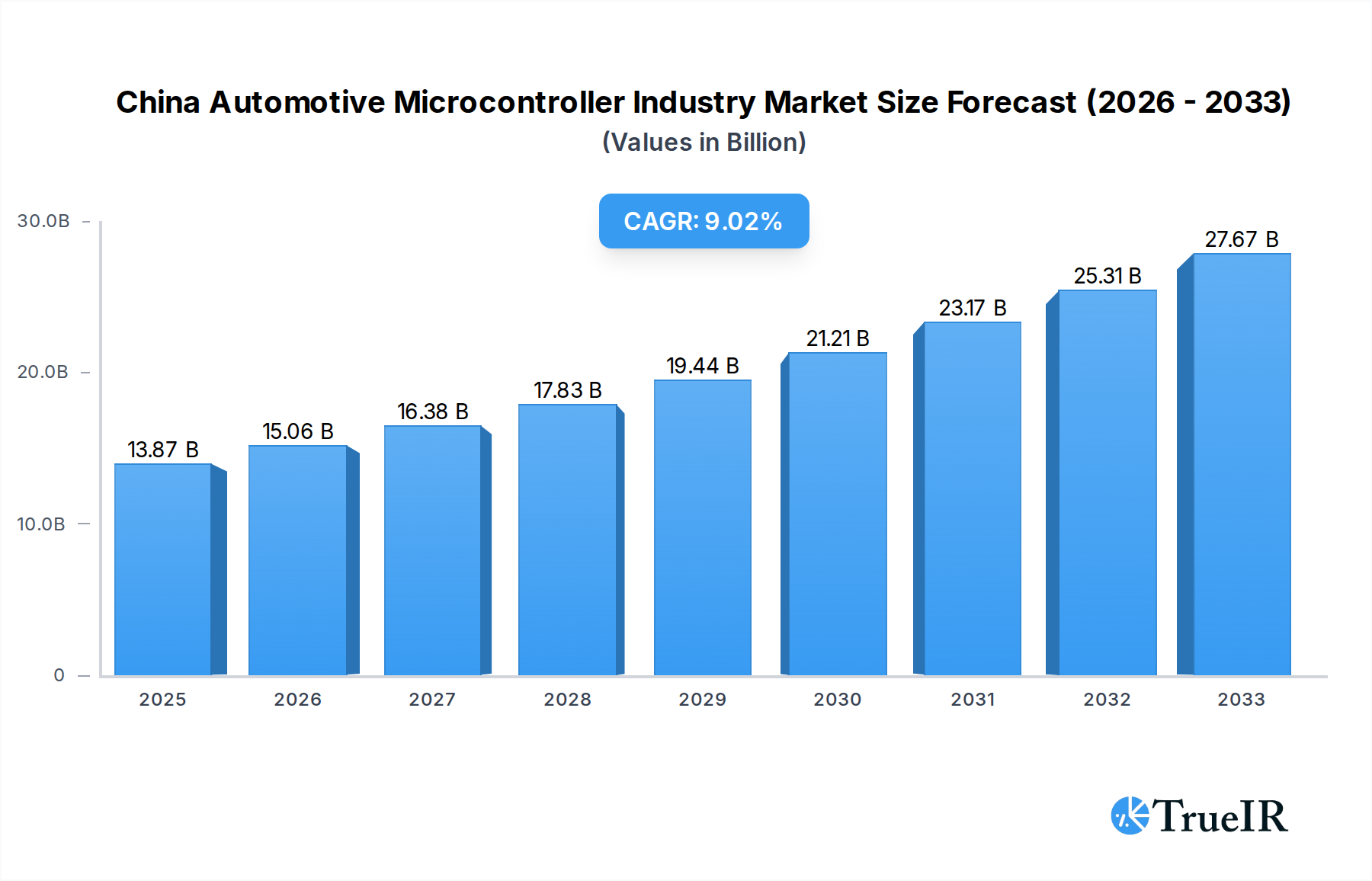

The China automotive microcontroller market is poised for substantial expansion, driven by the nation's robust automotive industry and its rapid adoption of advanced technologies. Valued at an estimated $13.87 billion in 2025, the market is projected to witness a Compound Annual Growth Rate (CAGR) of 8.74% throughout the forecast period of 2025-2033. This remarkable growth is propelled by several key factors. The increasing demand for sophisticated safety and security features, including Advanced Driver-Assistance Systems (ADAS), is a significant catalyst. Furthermore, the burgeoning adoption of in-car telematics and infotainment systems, alongside the electrification and digitalization of powertrains and chassis, are creating a strong demand for high-performance microcontrollers. The market is also significantly influenced by the growing emphasis on body electronics for enhanced vehicle functionality and user experience.

China Automotive Microcontroller Industry Market Size (In Billion)

The competitive landscape features a mix of established global players and emerging Chinese manufacturers, indicating a dynamic market environment. Key companies like Microchip Technology Inc., NXP Semiconductors NV, Renesas Electronics Corporation, and STMicroelectronics are actively participating, alongside prominent Chinese firms such as Puolop China and Shanghai Neusoft Carrier Microelectronics Co. The market is segmented by microcontroller type, with both 8/16-bit and 64-bit microcontrollers playing crucial roles, catering to diverse application needs from basic control to complex processing. Despite the strong growth trajectory, potential restraints could include supply chain disruptions for semiconductor components and evolving regulatory landscapes. However, the overarching trend points towards a significant and sustained expansion of the China automotive microcontroller market, fueled by innovation and consumer demand for smarter, safer, and more connected vehicles.

China Automotive Microcontroller Industry Company Market Share

Here is the SEO-optimized report description for the China Automotive Microcontroller Industry, crafted to maximize search visibility and industry engagement.

China Automotive Microcontroller Industry Market Structure & Competitive Landscape

The China automotive microcontroller market exhibits a dynamic competitive landscape characterized by moderate to high concentration, driven by significant innovation in advanced driver-assistance systems (ADAS), electrification, and connected vehicle technologies. Leading players like NXP Semiconductors NV, STMicroelectronics, and Renesas Electronics Corporation command substantial market share, leveraging their extensive product portfolios and strong R&D capabilities. Emerging Chinese domestic manufacturers, including Puolop China and Shanghai Neusoft Carrier Microelectronics Co, are rapidly gaining traction, fueled by government support and a focus on localized solutions.

Key innovation drivers include the relentless pursuit of enhanced safety features, improved fuel efficiency, and seamless in-car experiences. Regulatory impacts, such as stricter emissions standards and increasing ADAS mandates, are pushing demand for sophisticated microcontroller units (MCUs). Product substitutes are limited due to the specialized nature of automotive-grade MCUs, though advancements in SoC integration present potential long-term competition. End-user segmentation highlights the automotive industry's diverse needs, spanning safety and security (ADAS, etc.), body electronics, telematics and infotainment, and powertrain and chassis. Mergers and acquisitions (M&A) are a significant trend, with companies seeking to consolidate market positions, acquire new technologies, and expand their geographic reach. For instance, M&A activity in the global automotive semiconductor space has reached hundreds of billions in value in recent years, signaling a strategic consolidation essential for navigating the evolving market. Concentration ratios, particularly among the top five players, are estimated to exceed 65%, underscoring the influence of established leaders.

China Automotive Microcontroller Industry Market Trends & Opportunities

The China automotive microcontroller market is poised for robust expansion, with an estimated market size projected to reach over 50 billion by 2033, expanding from approximately 15 billion in 2024. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of roughly 11.5% during the forecast period (2025–2033). The market is experiencing a profound technological shift, primarily driven by the rapid electrification of vehicles and the widespread adoption of Advanced Driver-Assistance Systems (ADAS). Consumer preferences are increasingly leaning towards vehicles equipped with sophisticated infotainment systems, enhanced safety features, and seamless connectivity, directly fueling demand for high-performance automotive MCUs.

The competitive dynamics are intensifying, with both established global semiconductor giants and ambitious domestic Chinese players vying for market dominance. The ongoing semiconductor shortage, though showing signs of easing, has highlighted the strategic importance of resilient supply chains and has prompted increased investment in domestic production and R&D. Opportunities abound in specialized segments like high-performance MCUs for AI-driven ADAS applications, ultra-low-power MCUs for IoT integration in vehicles, and secure MCUs for cybersecurity in connected cars. The burgeoning Chinese electric vehicle (EV) market represents a significant growth catalyst, demanding a new generation of power-efficient and feature-rich MCUs for battery management systems, motor control, and advanced thermal management. Furthermore, the push for autonomous driving technologies is creating a substantial demand for MCUs with advanced processing capabilities, including AI acceleration and high-speed sensor fusion. Market penetration rates for safety-critical MCUs are steadily increasing as regulatory bodies worldwide implement stricter safety standards, compelling automakers to integrate more sophisticated electronic control units into their vehicle architectures. The increasing complexity of vehicle electronics, from advanced infotainment to sophisticated powertrain management, necessitates a continuous upgrade cycle of microcontroller technologies, ensuring a sustained demand for innovative solutions. The integration of cloud connectivity and over-the-air (OTA) updates also creates opportunities for MCUs that can support these advanced functionalities efficiently and securely.

Dominant Markets & Segments in China Automotive Microcontroller Industry

The China automotive microcontroller industry is experiencing dominant growth and significant potential within specific segments, driven by key technological advancements and supportive policy frameworks.

Dominant Segments by Application:

- Safety and Security (ADAS, etc.): This segment is the primary growth engine, projected to witness the highest CAGR. The Chinese government's strong emphasis on improving road safety, coupled with the rapid adoption of ADAS features like adaptive cruise control, lane-keeping assist, and automatic emergency braking, is propelling demand for high-performance and highly integrated MCUs. Billions are being invested by automakers in ADAS development, requiring MCUs with advanced processing power for sensor fusion and real-time decision-making.

- Telematics and Infotainment: The increasing demand for connected car services, enhanced in-car entertainment, and sophisticated navigation systems is driving significant growth in this segment. Advanced infotainment systems require MCUs capable of handling complex graphics, audio processing, and seamless connectivity, contributing billions to the overall market.

- Powertrain and Chassis: With the ongoing shift towards vehicle electrification and stricter emissions regulations for internal combustion engine vehicles, this segment remains critical. MCUs for battery management systems, motor control in EVs, and advanced transmission control are essential, representing a substantial portion of the market.

- Body Electronics: This segment encompasses a wide range of functionalities, including lighting control, climate control, and power windows. While perhaps not as high-growth as ADAS, the sheer volume of vehicles produced ensures a steady demand for cost-effective and reliable MCUs in this area, contributing billions to the market.

Dominant Segments by Type:

- 64-bit Microcontrollers: The increasing complexity of automotive software, particularly for ADAS, autonomous driving, and advanced infotainment, is driving a strong shift towards 64-bit MCUs. These offer greater processing power, larger memory addressability, and improved efficiency for demanding applications. The market for 64-bit MCUs is expected to see the most rapid expansion, driven by innovation and higher value applications.

- 8 and 16-bit Microcontrollers: These segments continue to hold a significant market share due to their cost-effectiveness and suitability for less computationally intensive applications within body electronics and basic powertrain control. Billions in volume continue to be generated from these established architectures. However, their growth rate is expected to be slower compared to 64-bit MCUs.

The dominant regions within China are the major automotive manufacturing hubs, including the Yangtze River Delta, Pearl River Delta, and the Beijing-Tianjin-Hebei region, where substantial investments in automotive R&D and production infrastructure are concentrated. Government policies supporting new energy vehicles (NEVs) and smart mobility are crucial growth catalysts, incentivizing the adoption of advanced microcontroller technologies across all automotive segments.

China Automotive Microcontroller Industry Product Analysis

The China automotive microcontroller industry is characterized by a rapid evolution of product offerings, driven by demands for increased processing power, enhanced safety, and improved connectivity. Innovations focus on higher bit architectures (e.g., 64-bit MCUs) for demanding ADAS and infotainment applications, alongside specialized MCUs for electric vehicle powertrains and battery management systems. Competitive advantages are being built on integrated safety features (ISO 26262 compliance), reduced power consumption, robust cybersecurity capabilities, and advanced sensor fusion processing. Market fit is achieved through tailored solutions addressing the specific needs of vehicle segments, from entry-level body electronics to high-end autonomous driving systems, ensuring billions in revenue through diverse product portfolios.

Key Drivers, Barriers & Challenges in China Automotive Microcontroller Industry

Key Drivers:

- Government Support & Policy: The Chinese government's strong backing for NEVs, smart mobility, and domestic semiconductor self-sufficiency is a primary driver, creating favorable market conditions and incentives.

- Technological Advancements: Rapid progress in AI, IoT, and advanced computing fuels demand for sophisticated automotive MCUs for ADAS, autonomous driving, and connected car features.

- Electrification Trend: The accelerating adoption of electric vehicles necessitates specialized MCUs for battery management, motor control, and charging infrastructure, contributing billions in demand.

- Increasing Vehicle Sophistication: Consumers' demand for advanced infotainment, enhanced safety, and connected services pushes automakers to integrate more complex electronic systems.

Key Barriers & Challenges:

- Global Supply Chain Volatility: Persistent semiconductor shortages and geopolitical tensions continue to pose significant challenges to consistent supply and production, impacting billions in potential sales.

- Intense Competition: The market faces intense competition from both established global players and rapidly emerging domestic manufacturers, leading to price pressures.

- Talent Shortage: A shortage of skilled engineers and researchers in the automotive semiconductor domain can hinder innovation and development.

- Regulatory Compliance: Navigating diverse and evolving automotive safety and environmental regulations requires significant investment and R&D effort.

Growth Drivers in the China Automotive Microcontroller Industry Market

The growth trajectory of the China automotive microcontroller market is primarily propelled by the nation's aggressive push towards electrification and intelligent vehicle technologies. Government mandates and incentives for New Energy Vehicles (NEVs) are directly translating into a massive demand for MCUs powering battery management systems, electric drivetrains, and advanced thermal management. Furthermore, the widespread adoption of Advanced Driver-Assistance Systems (ADAS), driven by both consumer preference and regulatory pressure for enhanced road safety, is creating substantial opportunities for high-performance MCUs capable of complex sensor fusion and real-time decision-making, representing billions in new market value. The increasing integration of connectivity and in-car infotainment features also fuels demand for powerful and efficient microcontrollers.

Challenges Impacting China Automotive Microcontroller Industry Growth

Despite robust growth prospects, the China automotive microcontroller industry faces significant hurdles. The lingering effects of global semiconductor supply chain disruptions continue to impact production volumes and can lead to increased costs, potentially affecting billions in revenue. Intense competition, both from established international players and rapidly evolving domestic manufacturers, exerts downward pressure on pricing and necessitates continuous innovation to maintain market share. Moreover, the stringent and evolving regulatory landscape surrounding automotive safety and emissions standards requires substantial and ongoing investment in R&D to ensure product compliance, adding complexity and cost to development cycles. The need for specialized talent in advanced semiconductor design and automotive electronics also presents a challenge.

Key Players Shaping the China Automotive Microcontroller Industry Market

- Puolop China

- Shanghai Neusoft Carrier Microelectronics Co

- Microchip Technology Inc

- NXP Semiconductors NV

- Toshiba Corporation

- Sunplus Innovation Technology Inc

- STMicroelectronics

- Bojuxing Industrial

- Renesas Electronics Corporation

- Holtek Semiconductor Inc

Significant China Automotive Microcontroller Industry Industry Milestones

- 2020: Launch of key domestic automotive MCU platforms by Chinese companies, supported by government initiatives.

- 2021: Increased investment in R&D for AI-powered MCUs for ADAS and autonomous driving solutions.

- 2022: Intensified focus on securing semiconductor supply chains amidst global shortages, leading to strategic partnerships and capacity expansions.

- 2023: Significant advancements in 32-bit and 64-bit automotive MCU offerings catering to the growing EV and ADAS markets.

- 2024: Growing emphasis on cybersecurity features within automotive MCUs in response to increasing connected vehicle threats, with billions invested in secure solutions.

Future Outlook for China Automotive Microcontroller Industry Market

The future outlook for the China automotive microcontroller industry remains exceptionally strong, projected to witness sustained double-digit growth throughout the forecast period. Key growth catalysts include the accelerating penetration of electric vehicles, the expanding capabilities and adoption of ADAS, and the pervasive trend towards vehicle connectivity and digitalization. Strategic opportunities lie in developing next-generation MCUs for Level 4/5 autonomous driving, high-performance computing platforms for advanced in-car AI, and secure, ultra-low-power solutions for the evolving automotive IoT ecosystem. The market's potential is further enhanced by ongoing government support for domestic innovation and manufacturing, ensuring billions in continued investment and market expansion.

China Automotive Microcontroller Industry Segmentation

-

1. Type

- 1.1. 8 and 16-bit microcontrollers

- 1.2. 64-bit microcontrollers

-

2. Application

- 2.1. Safety and Security (ADAS, etc.)

- 2.2. Body Electronics

- 2.3. Telematics and Infotainment

- 2.4. Powertrain and Chassis

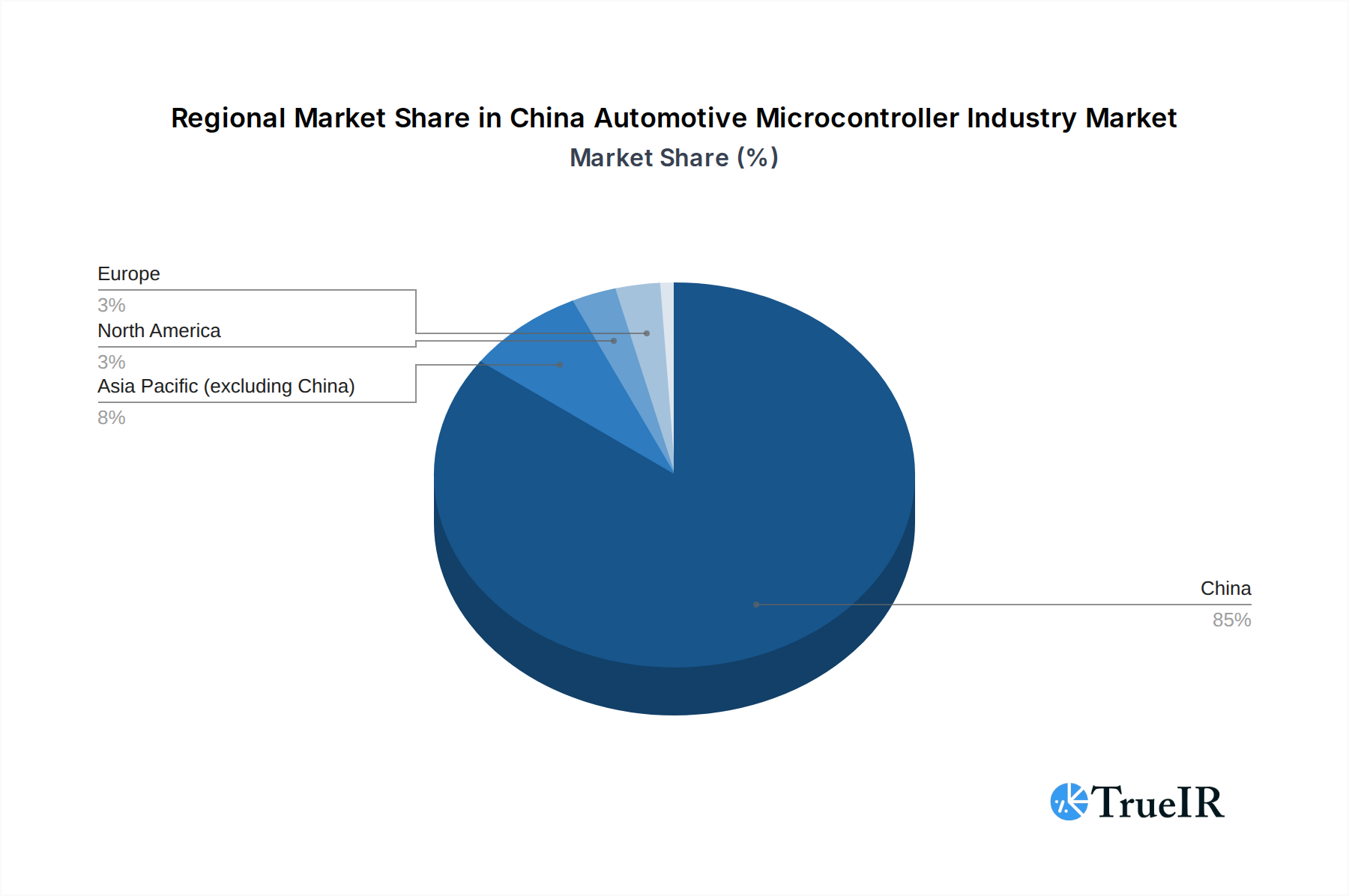

China Automotive Microcontroller Industry Segmentation By Geography

- 1. China

China Automotive Microcontroller Industry Regional Market Share

Geographic Coverage of China Automotive Microcontroller Industry

China Automotive Microcontroller Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.74% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. 8 and 16-bit microcontrollers

- 5.1.2. 64-bit microcontrollers

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Safety and Security (ADAS, etc.)

- 5.2.2. Body Electronics

- 5.2.3. Telematics and Infotainment

- 5.2.4. Powertrain and Chassis

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Automotive Microcontroller Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. 8 and 16-bit microcontrollers

- 6.1.2. 64-bit microcontrollers

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Safety and Security (ADAS, etc.)

- 6.2.2. Body Electronics

- 6.2.3. Telematics and Infotainment

- 6.2.4. Powertrain and Chassis

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Puolop China

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Shanghai Neusoft Carrier Microelectronics Co *List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Microchip Technology Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 NXP Semiconductors NV

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Toshiba Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sunplus Innovation Technology Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 STMicroelectronics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Bojuxing Industrial

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Renesas Electronics Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Holtek Semiconductor Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Puolop China

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Automotive Microcontroller Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Automotive Microcontroller Industry Share (%) by Company 2025

List of Tables

- Table 1: China Automotive Microcontroller Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: China Automotive Microcontroller Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: China Automotive Microcontroller Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Automotive Microcontroller Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: China Automotive Microcontroller Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: China Automotive Microcontroller Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Automotive Microcontroller Industry?

The projected CAGR is approximately 8.74%.

2. Which companies are prominent players in the China Automotive Microcontroller Industry?

Key companies in the market include Puolop China, Shanghai Neusoft Carrier Microelectronics Co *List Not Exhaustive, Microchip Technology Inc, NXP Semiconductors NV, Toshiba Corporation, Sunplus Innovation Technology Inc, STMicroelectronics, Bojuxing Industrial, Renesas Electronics Corporation, Holtek Semiconductor Inc.

3. What are the main segments of the China Automotive Microcontroller Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.87 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand for Electric Vehicles in Major Regions; Rising Demand for Safety and Infotainment-based Features; Anticipated Rise in Advanced Features from the Mid and High-end Segments.

6. What are the notable trends driving market growth?

ADAS to Witness a Significant Growth in the Safety and Security Segment.

7. Are there any restraints impacting market growth?

; Ongoing Trade Stand-off and Recent Decline in the Automotive Sector Expected to Have an Adverse Impact; Low-end MCU Manufacturers Posing a Strong Challenge for Established Vendors; Operational and Adaptability Related Concerns.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Automotive Microcontroller Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Automotive Microcontroller Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Automotive Microcontroller Industry?

To stay informed about further developments, trends, and reports in the China Automotive Microcontroller Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence