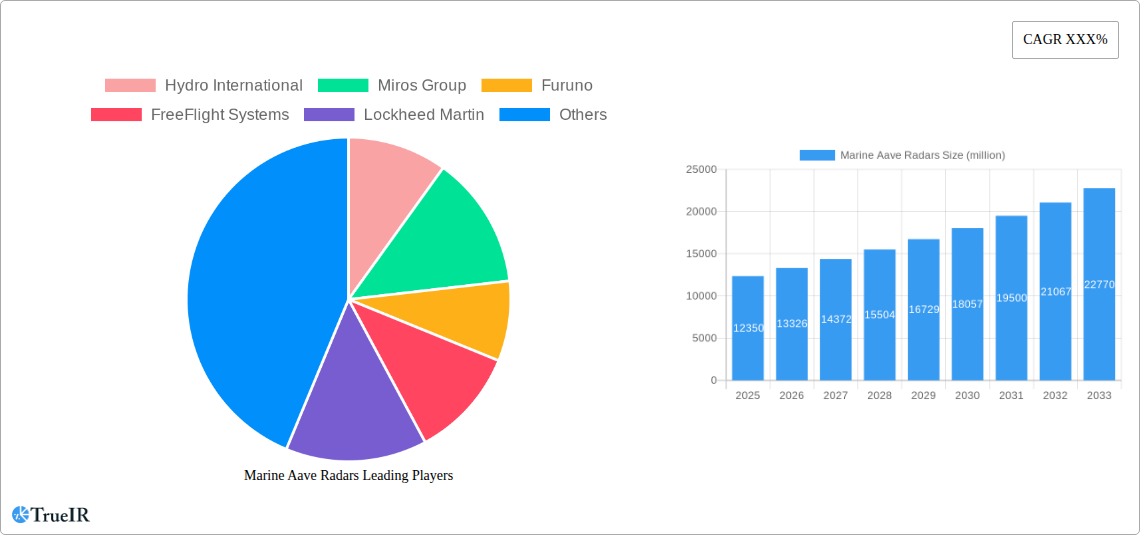

Key Insights

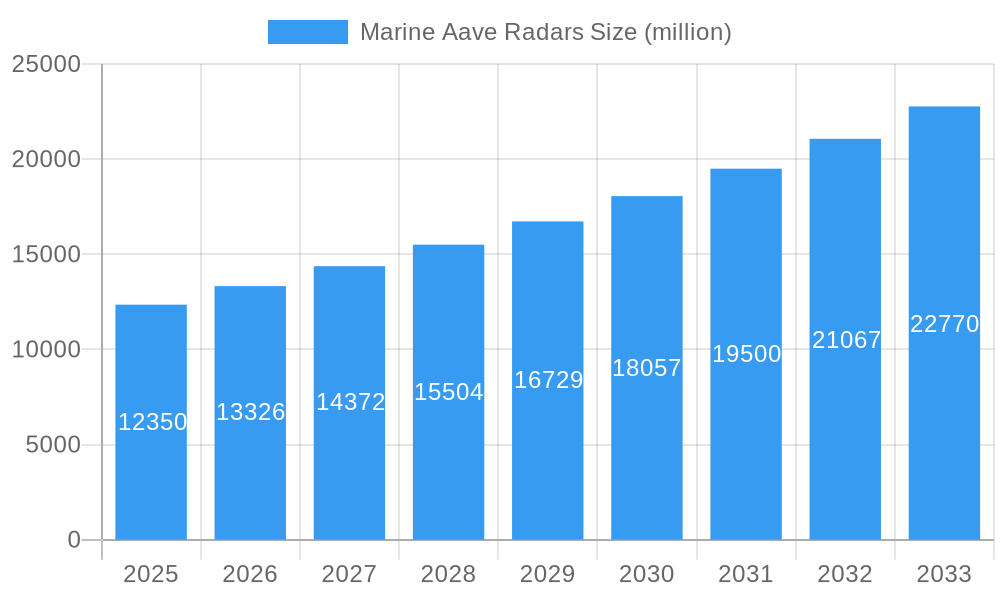

The global Marine Aave Radars market is poised for significant expansion, projected to reach an estimated $12.35 billion in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 9.7%, indicating a dynamic and thriving industry. This upward trajectory is primarily fueled by increasing global maritime trade and a burgeoning offshore energy sector, both heavily reliant on advanced navigation and surveillance technologies. The demand for enhanced safety, efficient vessel traffic management, and improved operational capabilities on ships and offshore platforms are key drivers pushing market penetration. Furthermore, advancements in radar technology, leading to more accurate, reliable, and integrated systems, are accelerating adoption rates. The market is segmented by application, with "Ship" and "Offshore Platform" being the primary beneficiaries, and by type, encompassing both "Direct Sensor" and "Indirect Sensors" solutions, each catering to specific operational needs and technological preferences within the maritime ecosystem.

Marine Aave Radars Market Size (In Billion)

The competitive landscape is characterized by the presence of established global players and emerging innovators, all vying to capture market share through technological superiority, strategic partnerships, and product diversification. Companies are focusing on developing next-generation radar systems that offer superior object detection, weather forecasting capabilities, and seamless integration with other bridge systems. The continuous evolution of regulatory frameworks emphasizing maritime safety and security also plays a crucial role in driving the adoption of advanced radar solutions. While the market exhibits strong growth, potential restraints such as high initial investment costs for advanced systems and the need for skilled personnel for installation and maintenance might pose challenges. However, the overwhelming benefits in terms of safety, efficiency, and regulatory compliance are expected to outweigh these concerns, ensuring sustained market expansion throughout the forecast period.

Marine Aave Radars Company Market Share

Marine Aave Radars Market Structure & Competitive Landscape

The global Marine Aave Radars market exhibits a moderately concentrated structure, with a blend of large, established players and emerging innovators. Key factors driving market concentration include the significant capital expenditure required for research and development, manufacturing, and regulatory compliance. Innovation is a paramount driver, fueled by the relentless pursuit of enhanced maritime safety, operational efficiency, and navigation precision. This includes advancements in sensor technology, data processing, and artificial intelligence for threat detection and environmental monitoring. Regulatory impacts, such as evolving international maritime safety standards and mandates for advanced navigation systems, play a crucial role in shaping market entry and product development. The availability of advanced sensor technology has significantly reduced the threat of direct product substitutes, though indirect sensing methods are gaining traction. End-user segmentation reveals a strong demand from both commercial shipping and offshore platforms, driven by their critical operational needs. Mergers and acquisitions (M&A) trends indicate a strategic consolidation, with larger entities acquiring specialized technology providers to expand their product portfolios and market reach. In the historical period of 2019-2024, approximately $1.2 billion in M&A activities have been recorded, reflecting a desire for synergistic growth and competitive advantage within this billion-dollar industry. Concentration ratios, particularly for direct sensor technology, are estimated to be around 65%, with the top five players holding a significant share.

Marine Aave Radars Market Trends & Opportunities

The Marine Aave Radars market is poised for substantial growth, projecting a Compound Annual Growth Rate (CAGR) of approximately 7.8% from 2025 to 2033. This trajectory is underpinned by a projected market size exceeding $12.5 billion by 2033, an increase from an estimated $7.2 billion in the base year of 2025. Technological shifts are a dominant force, with a clear trend towards increasingly sophisticated radar systems featuring higher resolution, extended range, and advanced signal processing capabilities. The integration of AI and machine learning algorithms is revolutionizing object detection, classification, and tracking, enabling proactive threat identification and improved situational awareness for mariners. Consumer preferences are evolving, with a growing demand for integrated navigation solutions that offer seamless connectivity, enhanced data visualization, and user-friendly interfaces. Maritime operators are prioritizing systems that not only enhance safety but also contribute to operational efficiency, fuel savings, and environmental compliance. Competitive dynamics are intensifying, driven by ongoing innovation and the strategic expansion efforts of key industry players. Companies are investing heavily in research and development to stay ahead of the curve, focusing on miniaturization, power efficiency, and the development of multi-functional radar systems. Market penetration rates for advanced radar systems are expected to rise significantly, particularly within the commercial shipping and offshore energy sectors, as regulatory frameworks become more stringent and the economic benefits of advanced technology become more evident. The adoption of autonomous shipping technologies will further accelerate the demand for highly reliable and intelligent radar solutions, creating new avenues for market expansion and technological advancement.

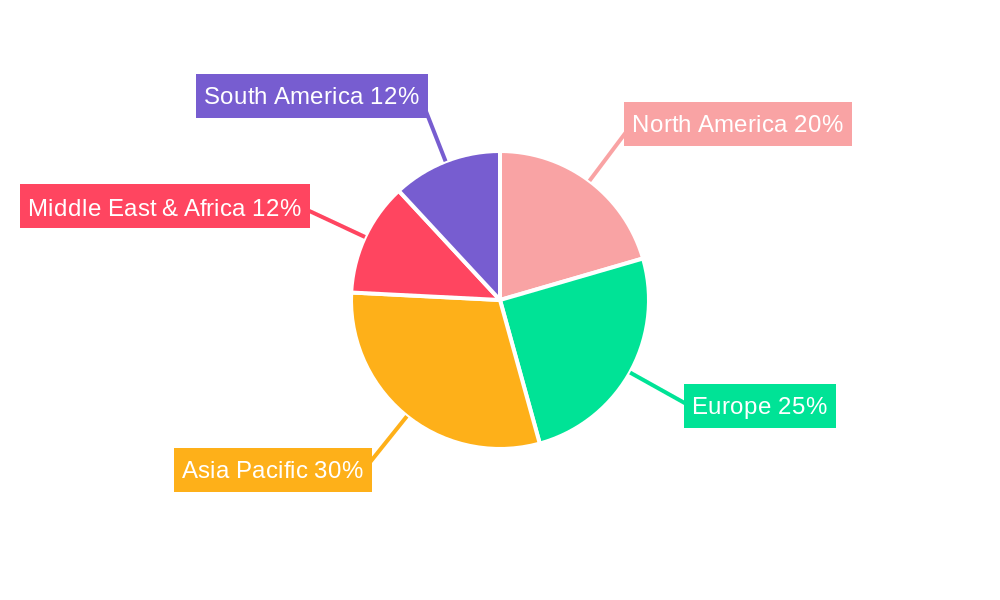

Dominant Markets & Segments in Marine Aave Radars

The dominant market segment for Marine Aave Radars is undeniably the Ship application, driven by the sheer volume of global maritime traffic and the critical need for enhanced navigation, collision avoidance, and security across a vast array of vessel types, from massive container ships to smaller fishing vessels. Within this broad category, the Direct Sensor type is experiencing robust growth due to its inherent precision, real-time data acquisition capabilities, and ability to provide direct environmental readings crucial for immediate decision-making. The Asia-Pacific region is emerging as the leading market, largely attributed to the rapidly expanding shipbuilding industry, increasing trade volumes, and substantial government investments in port infrastructure and maritime safety initiatives. Countries such as China, South Korea, and Japan are at the forefront of adopting advanced radar technologies.

Application: Ship:

- Key Growth Drivers: Escalating global trade necessitating larger and more efficient fleets, stringent international maritime safety regulations (e.g., SOLAS), the rise of autonomous and remotely operated vessels, and the increasing need for ice navigation and search and rescue capabilities. The continuous growth of the global shipping fleet, projected to exceed $5.0 billion in value by 2030, directly fuels demand.

- Detailed Analysis: The commercial shipping sector, encompassing container vessels, tankers, bulk carriers, and Ro-Pax ferries, represents the largest consumer base. The inherent risks associated with long-haul voyages, complex port approaches, and challenging weather conditions mandate sophisticated radar solutions for accurate target detection, navigation in fog, and adherence to traffic separation schemes. The increasing complexity of maritime operations and the growing emphasis on risk mitigation are powerful catalysts for the adoption of advanced radar systems.

Type: Direct Sensor:

- Key Growth Drivers: Superior accuracy and real-time data, ability to detect small targets, lower latency in data processing for immediate threat response, and integration capabilities with other onboard systems for comprehensive situational awareness. The projected market for direct sensors is expected to reach $8.5 billion by 2033.

- Detailed Analysis: Direct sensors, such as traditional radar transceivers and advanced Doppler radars, offer unparalleled capabilities in detecting the precise location, velocity, and bearing of other vessels, buoys, and navigational hazards. Their direct interaction with the marine environment provides the most immediate and accurate data, essential for safe navigation and collision avoidance. The ongoing miniaturization and cost reduction of these components are making them accessible to a wider range of vessels.

While Offshore Platforms (including oil rigs, wind farms, and research vessels) represent a significant and growing market segment, their overall volume is currently lower than that of commercial shipping. However, their demand for robust, long-range, and highly reliable radar systems for operational safety, security, and environmental monitoring is substantial, with an estimated market value of $3.0 billion in 2033. The Indirect Sensors segment, while currently smaller, is projected for significant growth as technologies like AIS (Automatic Identification System) and ECDIS (Electronic Chart Display and Information System) integration mature, offering complementary data for enhanced maritime situational awareness, contributing an estimated $1.0 billion to the market by 2033.

Marine Aave Radars Product Analysis

Marine Aave Radar products are characterized by continuous innovation aimed at enhancing maritime safety and operational efficiency. Key advancements include the integration of AI for improved target detection and classification, higher resolution imaging for clearer identification of smallcraft and debris, and extended range capabilities for early threat assessment. These products offer significant competitive advantages through their reliability, accuracy, and ease of integration into existing vessel systems. Applications span navigation, collision avoidance, search and rescue, and security monitoring, all critical for the safe and efficient operation of ships and offshore platforms.

Key Drivers, Barriers & Challenges in Marine Aave Radars

The Marine Aave Radars market is propelled by several key drivers. Technologically, advancements in solid-state radar, AI-powered signal processing, and multi-functionality are enhancing performance and reducing costs. Economically, the global increase in maritime trade and the growing value of offshore energy assets necessitate improved safety and operational efficiency. Policy-driven factors, such as stricter maritime safety regulations and the push towards autonomous shipping, are creating significant demand for advanced radar systems. For example, the International Maritime Organization's (IMO) mandates for mandatory radar carriage on all vessels over a certain tonnage directly influence market growth.

Challenges impacting Marine Aave Radars growth include regulatory complexities, with differing standards and implementation timelines across regions. Supply chain issues, particularly for specialized electronic components, can lead to production delays and increased costs, with potential impacts of 5-10% on production timelines. Competitive pressures from a fragmented market and the need for continuous R&D investment to maintain a technological edge also present significant hurdles. The high initial investment cost for some advanced radar systems can also be a barrier for smaller operators, limiting widespread adoption in certain segments.

Growth Drivers in the Marine Aave Radars Market

The growth of the Marine Aave Radars market is primarily fueled by technological advancements such as the integration of artificial intelligence (AI) and machine learning for enhanced object detection and classification, along with the development of more compact and power-efficient solid-state radar systems. Economically, the surge in global maritime trade and the expansion of offshore energy exploration and production activities are creating a substantial demand for advanced navigation and safety equipment. Regulatory mandates from international bodies like the IMO, emphasizing enhanced maritime safety and the adoption of advanced technologies, are also significant growth catalysts. Furthermore, the increasing adoption of autonomous shipping technologies is creating a pressing need for highly reliable and intelligent radar solutions.

Challenges Impacting Marine Aave Radars Growth

Several challenges are impacting the growth of the Marine Aave Radars market. Regulatory complexities, including variations in compliance standards and certification processes across different maritime authorities, can create hurdles for global product deployment. Supply chain disruptions, particularly for critical electronic components and rare earth materials, can lead to production delays and increased manufacturing costs, potentially impacting delivery timelines by 5-10%. Competitive pressures from both established players and emerging technology providers necessitate continuous innovation and significant R&D investment to maintain market share. The substantial upfront investment required for some sophisticated radar systems also presents an economic barrier for smaller operators and developing regions.

Key Players Shaping the Marine Aave Radars Market

- Hydro International

- Miros Group

- Furuno

- FreeFlight Systems

- Lockheed Martin

- Northrop Grumman

- JRC (Alphatron Marine)

- Garmin

- Saab

- Enraf

- Radac

- RS Aqua

- Rutter

- CODAR Ocean Sensors

- Helzel Messtechnik GmbH

- FLIR Systems

- Applied Physical Sciences Corp (APS)

Significant Marine Aave Radars Industry Milestones

- 2019: Introduction of AI-powered object recognition algorithms in marine radar systems, enhancing target classification accuracy.

- 2020: Significant advancements in solid-state radar technology, leading to smaller, more power-efficient, and more reliable radar units.

- 2021: Increased regulatory focus on enhanced maritime situational awareness and collision avoidance systems by the IMO.

- 2022: Major players like Lockheed Martin and Northrop Grumman began investing heavily in the development of integrated maritime surveillance solutions.

- 2023: Emergence of advanced Doppler radar capabilities for improved detection of small craft and debris in challenging sea states.

- 2024: Growing interest and investment in radar technologies for the burgeoning autonomous shipping sector.

Future Outlook for Marine Aave Radars Market

The future outlook for the Marine Aave Radars market is exceptionally promising, driven by a confluence of technological innovation and increasing global demand for maritime safety and efficiency. Strategic opportunities lie in the continued integration of AI and machine learning, leading to truly intelligent radar systems capable of predictive analysis and automated decision support. The expansion of autonomous shipping will create a substantial market for highly sophisticated, networked radar solutions that can operate seamlessly in complex environments. Furthermore, the growing emphasis on environmental monitoring and sustainable shipping practices will foster the development of radar systems capable of providing valuable data for these applications. The market potential is significant, with continuous advancements expected to drive increased adoption across all maritime sectors, reinforcing its position as a critical technology for the future of global navigation and safety, projected to reach over $12.5 billion by 2033.

Marine Aave Radars Segmentation

-

1. Application

- 1.1. Ship

- 1.2. Offshore Platform

-

2. Type

- 2.1. Direct Sensor

- 2.2. Indirect Sensors

Marine Aave Radars Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Marine Aave Radars Regional Market Share

Geographic Coverage of Marine Aave Radars

Marine Aave Radars REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Ship

- 5.1.2. Offshore Platform

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Direct Sensor

- 5.2.2. Indirect Sensors

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Ship

- 6.1.2. Offshore Platform

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Direct Sensor

- 6.2.2. Indirect Sensors

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Ship

- 7.1.2. Offshore Platform

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Direct Sensor

- 7.2.2. Indirect Sensors

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Ship

- 8.1.2. Offshore Platform

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Direct Sensor

- 8.2.2. Indirect Sensors

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Ship

- 9.1.2. Offshore Platform

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Direct Sensor

- 9.2.2. Indirect Sensors

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Marine Aave Radars Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Ship

- 10.1.2. Offshore Platform

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Direct Sensor

- 10.2.2. Indirect Sensors

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Hydro International

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Miros Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Furuno

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 FreeFlight Systems

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lockheed Martin

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Northrop Grumman

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 JRC (Alphatron Marine)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Garmin

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Saab

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Enraf

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Radac

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 RS Aqua

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Rutter

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CODAR Ocean Sensors

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Helzel Messtechnik GmbH

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 FLIR Systems

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Applied Physical Sciences Corp (APS)

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Hydro International

List of Figures

- Figure 1: Global Marine Aave Radars Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Marine Aave Radars Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Marine Aave Radars Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Marine Aave Radars Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Marine Aave Radars Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Marine Aave Radars Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Marine Aave Radars Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Marine Aave Radars Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Marine Aave Radars Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Marine Aave Radars Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Marine Aave Radars Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Marine Aave Radars Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Marine Aave Radars Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Marine Aave Radars Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Marine Aave Radars Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Marine Aave Radars Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Marine Aave Radars Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Marine Aave Radars Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Marine Aave Radars Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Marine Aave Radars Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Marine Aave Radars Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Marine Aave Radars Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Marine Aave Radars Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Marine Aave Radars Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Marine Aave Radars Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Marine Aave Radars Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Marine Aave Radars Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Marine Aave Radars Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Marine Aave Radars Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Marine Aave Radars Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Marine Aave Radars Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Marine Aave Radars Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Marine Aave Radars Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Marine Aave Radars Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Marine Aave Radars Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Marine Aave Radars Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Marine Aave Radars Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Marine Aave Radars Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Marine Aave Radars Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Marine Aave Radars Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Aave Radars?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Marine Aave Radars?

Key companies in the market include Hydro International, Miros Group, Furuno, FreeFlight Systems, Lockheed Martin, Northrop Grumman, JRC (Alphatron Marine), Garmin, Saab, Enraf, Radac, RS Aqua, Rutter, CODAR Ocean Sensors, Helzel Messtechnik GmbH, FLIR Systems, Applied Physical Sciences Corp (APS).

3. What are the main segments of the Marine Aave Radars?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Marine Aave Radars," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Marine Aave Radars report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Marine Aave Radars?

To stay informed about further developments, trends, and reports in the Marine Aave Radars, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence