Key Insights

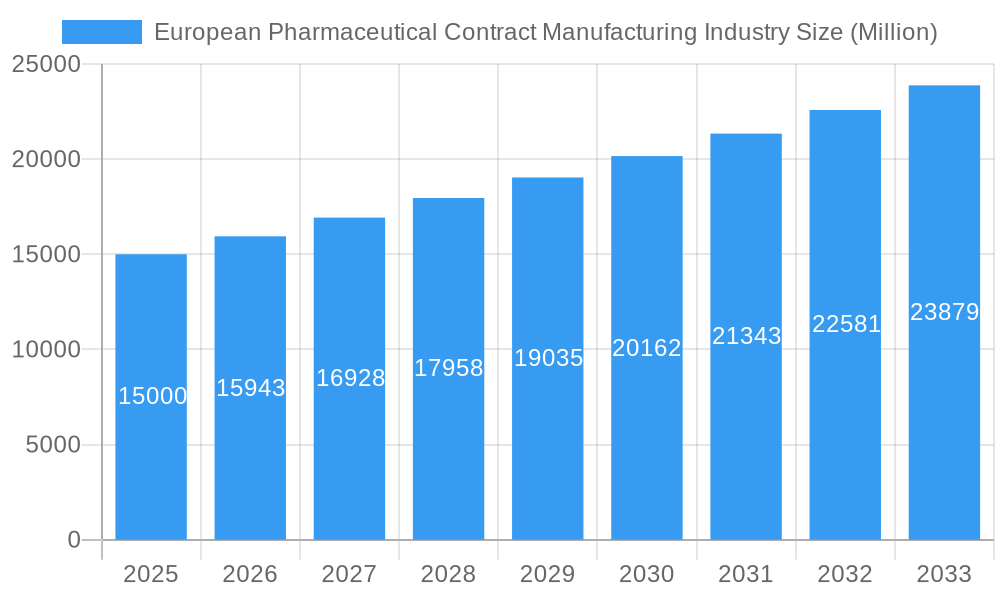

The European pharmaceutical contract manufacturing market, valued at approximately €[Estimate based on XX million and market trends - e.g., €15 billion] in 2025, is projected to experience robust growth, driven by a 5.71% CAGR from 2025 to 2033. This expansion is fueled by several key factors. Firstly, the increasing complexity of drug development and manufacturing necessitates outsourcing for pharmaceutical companies seeking to optimize costs and timelines. Secondly, the growing demand for specialized services, particularly in areas like aseptic filling and advanced drug delivery systems, is boosting the demand for contract manufacturers with specialized expertise. Finally, the rising prevalence of chronic diseases and the consequent increase in demand for pharmaceutical products across Europe further contributes to market expansion. This growth is particularly evident in segments such as Active Pharmaceutical Ingredient (API) manufacturing and finished dosage formulation (FDF) development and manufacturing, where contract manufacturing plays a crucial role in efficient and cost-effective drug production.

European Pharmaceutical Contract Manufacturing Industry Market Size (In Billion)

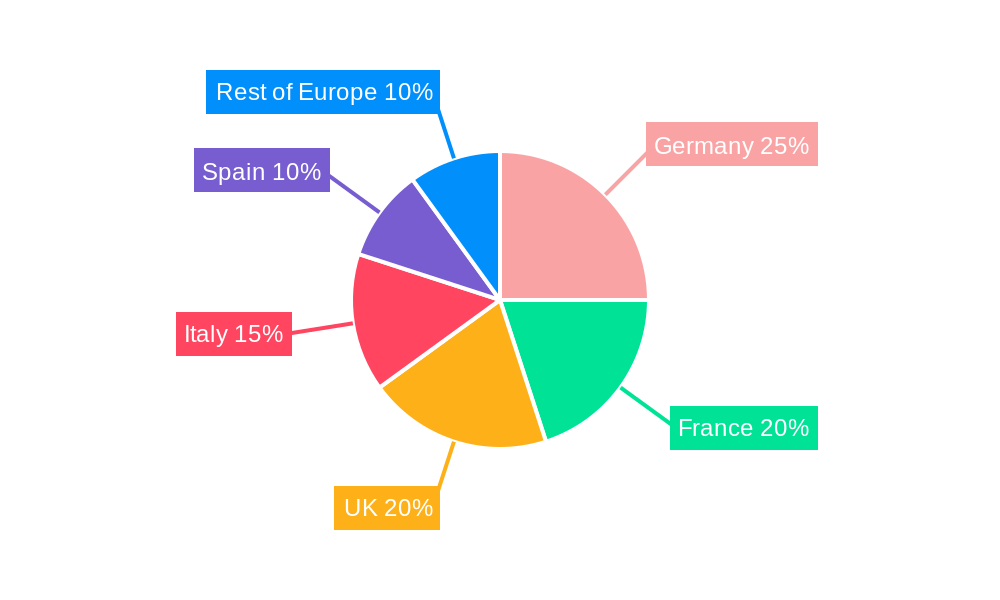

However, the market faces certain challenges. Regulatory hurdles and stringent quality control requirements can increase costs and complexity for contract manufacturers. Furthermore, competition from established players and emerging market entrants requires manufacturers to continually innovate and offer competitive pricing and specialized services. While the UK, Germany, France, and Italy represent major market segments, growth opportunities also exist in other European countries, driving the expansion of the "Rest of Europe" segment. Companies like Fareva Holdings SA, Famar SA, and Lonza Group are key players shaping the market landscape through strategic partnerships, acquisitions, and capacity expansions to meet the rising demand. The market's future trajectory depends on the continued innovation in drug delivery, the evolution of regulatory landscapes, and the capacity of contract manufacturers to maintain high quality standards while efficiently scaling operations.

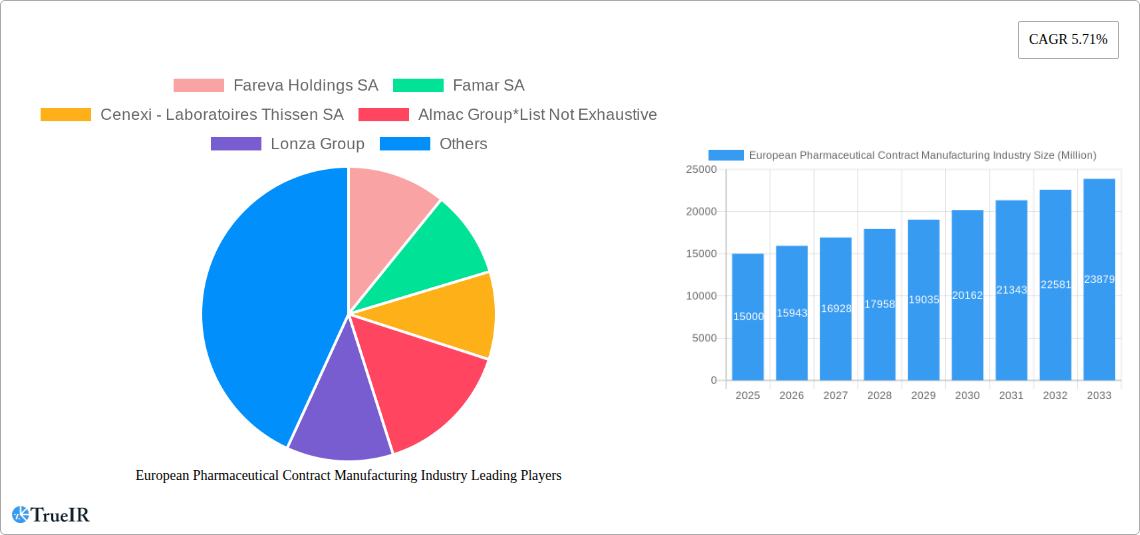

European Pharmaceutical Contract Manufacturing Industry Company Market Share

This comprehensive report provides a detailed analysis of the European Pharmaceutical Contract Manufacturing (PCM) industry, covering market size, growth drivers, competitive landscape, and future outlook from 2019 to 2033. The study period spans 2019–2024 (Historical Period), with 2025 as the base and estimated year. The forecast period extends to 2033. This in-depth analysis will equip stakeholders with critical insights to navigate this dynamic market.

European Pharmaceutical Contract Manufacturing Industry Market Structure & Competitive Landscape

The European PCM market exhibits a moderately concentrated structure, with several large players commanding significant market share. Concentration ratios (e.g., CR4, CR8) are expected to be around xx%, reflecting the presence of both multinational corporations and specialized regional players. Innovation is a key driver, fueled by the demand for advanced drug delivery systems and personalized medicines. Regulatory changes, particularly those related to GMP (Good Manufacturing Practices) and data privacy, significantly impact market dynamics. Product substitution pressures are moderate, primarily driven by the emergence of biosimilars and generic drugs. The market is segmented by end-users (pharmaceutical companies, biotech firms, etc.). Mergers and acquisitions (M&A) activity has been robust in recent years, with an estimated xx Million USD in deal volume between 2019 and 2024. Key M&A trends include vertical integration strategies by major CDMOs and consolidation among smaller players.

- Key Market Players: Fareva Holdings SA, Famar SA, Cenexi - Laboratoires Thissen SA, Almac Group, Lonza Group, Aenova Group, Boehringer Ingelheim Group, Recipharm AB (This list is not exhaustive).

- Concentration Ratios: CR4: xx%; CR8: xx% (estimated)

- M&A Activity (2019-2024): Approximately xx Million USD

European Pharmaceutical Contract Manufacturing Industry Market Trends & Opportunities

The European PCM market is experiencing significant growth, driven by several factors. The market size is projected to reach xx Million USD by 2025, growing at a CAGR of xx% from 2025 to 2033. This growth is fueled by an increase in pharmaceutical R&D expenditure, growing demand for outsourcing services from pharmaceutical companies seeking to reduce operational costs and enhance efficiency, and the expanding biopharmaceutical market. Technological advancements, such as automation and digitalization in manufacturing, are transforming the industry. Consumer preferences for innovative drug delivery systems and personalized therapies are driving demand for specialized contract manufacturing services. The competitive landscape is characterized by intense rivalry among established players and the emergence of new entrants, particularly in niche segments like cell and gene therapy manufacturing. Market penetration of advanced technologies, such as continuous manufacturing, is gradually increasing, with xx% penetration by 2025.

Dominant Markets & Segments in European Pharmaceutical Contract Manufacturing Industry

Germany, the United Kingdom, and France are currently the leading national markets, together accounting for approximately xx% of the overall European PCM market. However, growth opportunities exist across all major markets within the region. The Active Pharmaceutical Ingredient (API) manufacturing segment holds the largest market share driven by increasing demand for generics and biosimilars. Finished Dosage Formulation (FDF) development and manufacturing are also experiencing strong growth. Within these segments, there is substantial opportunity for contract manufacturing of innovative dosage forms, including injectables, and biologics.

By Country:

- United Kingdom: Strong regulatory environment and established pharmaceutical industry.

- Germany: Significant presence of major pharmaceutical companies and CDMOs.

- France: Growing biotech sector and investment in pharmaceutical manufacturing.

- Italy: Expanding market driven by generic drug production.

- Spain: Increasing R&D investment and government support for the pharmaceutical sector.

- Rest of Europe: Consolidated growth across emerging markets in Eastern Europe.

By Service Type:

- API Manufacturing: Driven by increasing demand for generics and biosimilars.

- FDF Development and Manufacturing: High demand for complex and innovative dosage forms.

- Injectable Dose Formulation: Secondary Packaging: Growth propelled by the rise of biologics.

Key Growth Drivers:

- Robust regulatory frameworks supporting pharmaceutical innovation.

- Government incentives and investment in pharmaceutical manufacturing infrastructure.

- Growing demand for outsourced pharmaceutical manufacturing services.

- Technological advancements leading to increased efficiency and productivity.

European Pharmaceutical Contract Manufacturing Industry Product Analysis

The European PCM industry offers a diverse range of products and services, catering to the evolving needs of pharmaceutical companies. Recent product innovations include advanced drug delivery systems, such as liposomes and nanoparticles, and personalized medicine manufacturing capabilities. These innovations provide competitive advantages by offering enhanced efficacy, improved patient compliance, and tailored treatment options. Technological advancements, including automation, continuous manufacturing, and process analytical technology (PAT), contribute significantly to product quality, efficiency, and cost-effectiveness. The market fit for these innovative products is strong, driven by increasing demand for sophisticated therapies and the pressure on pharmaceutical companies to improve efficiency and reduce costs.

Key Drivers, Barriers & Challenges in European Pharmaceutical Contract Manufacturing Industry

Key Drivers:

The European PCM market is driven by increased outsourcing by pharmaceutical companies, technological advancements (automation, continuous manufacturing), and rising R&D spending in the pharmaceutical sector. Government regulations supporting pharmaceutical innovation also play a significant role.

Key Challenges & Restraints:

The industry faces challenges including regulatory complexities (GMP compliance), supply chain disruptions (raw material shortages), and intense competition from established players and new entrants. These factors can lead to delays in product launches, increased costs, and reduced profitability. The COVID-19 pandemic highlighted the vulnerability of global supply chains, resulting in increased focus on regionalization and diversification of sourcing. Estimated impact of supply chain disruptions on industry revenue in 2022: xx Million USD.

Growth Drivers in the European Pharmaceutical Contract Manufacturing Industry Market

The European PCM market is propelled by technological advancements (automation, digitalization), increasing demand for specialized services (e.g., cell and gene therapy manufacturing), and supportive regulatory environments across several European countries that encourage investment in the pharmaceutical sector. The rising prevalence of chronic diseases and increasing healthcare expenditure across Europe further contribute to market expansion.

Challenges Impacting European Pharmaceutical Contract Manufacturing Industry Growth

Significant challenges include stringent regulatory requirements, increasing price pressures from generic competition, and the complexity of managing global supply chains. Furthermore, skilled labor shortages and securing sufficient funding for capital investments pose considerable obstacles to market growth.

Key Players Shaping the European Pharmaceutical Contract Manufacturing Industry Market

- Fareva Holdings SA

- Famar SA

- Cenexi - Laboratoires Thissen SA

- Almac Group

- Lonza Group

- Aenova Group

- Boehringer Ingelheim Group

- Recipharm AB

Significant European Pharmaceutical Contract Manufacturing Industry Industry Milestones

- February 2022: Merck (Germany) restructured its business to strengthen its CDMO business, creating Life Science Services (LSS). This consolidation aimed to improve efficiency and competitiveness in the CDMO market.

- March 2022: MorphoSys (Germany) incurred USD 254 Million in charges after terminating its US R&D operations, consolidating its work in Germany. This strategic shift reflects a focus on domestic operations and cost optimization.

Future Outlook for European Pharmaceutical Contract Manufacturing Industry Market

The European PCM market is poised for continued growth, driven by technological innovation, increased outsourcing by pharmaceutical companies, and expanding demand for specialized services. Strategic partnerships and investments in advanced manufacturing technologies will play a key role in shaping future market dynamics. The market's future success hinges on effectively addressing challenges related to regulatory compliance, supply chain resilience, and competition. The expected market size by 2033 is estimated at xx Million USD, representing significant growth opportunities for industry players.

European Pharmaceutical Contract Manufacturing Industry Segmentation

-

1. Service Type

- 1.1. Active P

-

1.2. Finished

- 1.2.1. Solid Dose Formulation

- 1.2.2. Liquid Dose Formulation

- 1.2.3. Injectable Dose Formulation

- 1.3. Secondary Packaging

European Pharmaceutical Contract Manufacturing Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Pharmaceutical Contract Manufacturing Industry Regional Market Share

Geographic Coverage of European Pharmaceutical Contract Manufacturing Industry

European Pharmaceutical Contract Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Active P

- 5.1.2. Finished

- 5.1.2.1. Solid Dose Formulation

- 5.1.2.2. Liquid Dose Formulation

- 5.1.2.3. Injectable Dose Formulation

- 5.1.3. Secondary Packaging

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. European Pharmaceutical Contract Manufacturing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Active P

- 6.1.2. Finished

- 6.1.2.1. Solid Dose Formulation

- 6.1.2.2. Liquid Dose Formulation

- 6.1.2.3. Injectable Dose Formulation

- 6.1.3. Secondary Packaging

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Fareva Holdings SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Famar SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cenexi - Laboratoires Thissen SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Almac Group*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lonza Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Aenova Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Boehringer Ingelheim Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Recipharm AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Fareva Holdings SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: European Pharmaceutical Contract Manufacturing Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Pharmaceutical Contract Manufacturing Industry Share (%) by Company 2025

List of Tables

- Table 1: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 4: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Pharmaceutical Contract Manufacturing Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the European Pharmaceutical Contract Manufacturing Industry?

Key companies in the market include Fareva Holdings SA, Famar SA, Cenexi - Laboratoires Thissen SA, Almac Group*List Not Exhaustive, Lonza Group, Aenova Group, Boehringer Ingelheim Group, Recipharm AB.

3. What are the main segments of the European Pharmaceutical Contract Manufacturing Industry?

The market segments include Service Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 209.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Outsourcing Volume by Pharmaceutical Companies; Increasing Investment in R&D.

6. What are the notable trends driving market growth?

Rising Investment in R&D will Drive The Market Growth.

7. Are there any restraints impacting market growth?

Increasing Lead Time and Logistics Costs; Stringent Regulatory Requirements; Capacity Utilization Issues Affecting the Profitability of CMOs.

8. Can you provide examples of recent developments in the market?

March 2022: MorphoSys sacked US R&D to consolidate work in Germany, taking USD 254 million in charges. MorphoSys axed its early pipeline and U.S. R&D work that came with the USD 1.7 billion purchase of Constellation Pharmaceuticals, meaning a more than USD 250 million impairment charge as the German pharma shifted the focus home.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Pharmaceutical Contract Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Pharmaceutical Contract Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Pharmaceutical Contract Manufacturing Industry?

To stay informed about further developments, trends, and reports in the European Pharmaceutical Contract Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence