Key Insights

The Spanish packaging industry is projected for substantial growth, expected to reach a market size of 620 million by 2025, with a Compound Annual Growth Rate (CAGR) of 7.01%. Key growth drivers include increasing demand from the food and beverage sector for innovative and sustainable solutions, and the healthcare and pharmaceutical industries' need for sterile and tamper-evident packaging. The beauty and personal care market also contributes significantly, driven by consumer preference for visually appealing and eco-friendly options. Industrial applications continue to support market volume through specialized protective packaging.

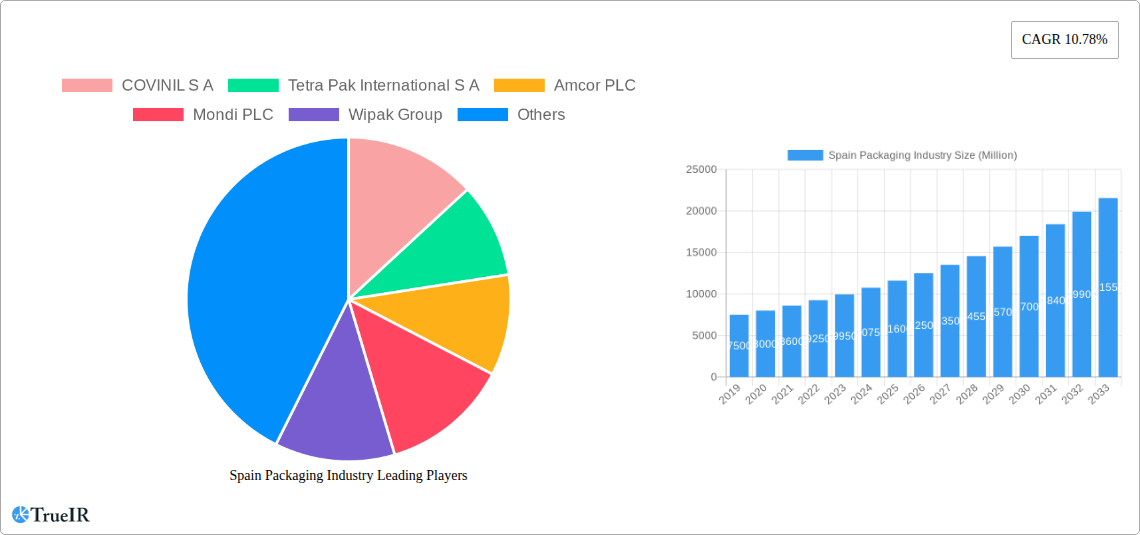

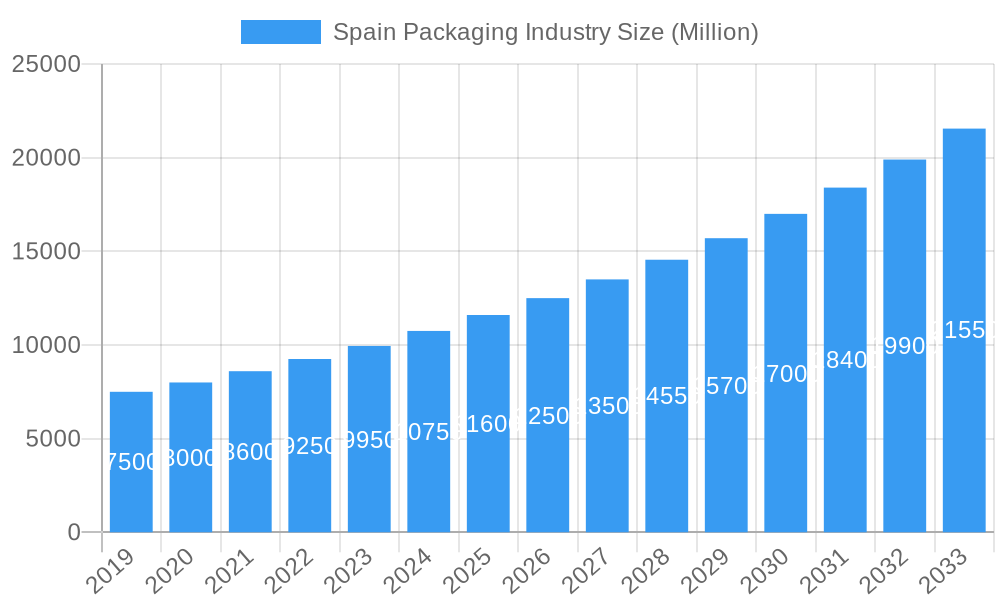

Spain Packaging Industry Market Size (In Million)

Evolving consumer preferences and regulatory frameworks are shaping industry dynamics. Sustainability and the circular economy are paramount, leading to increased adoption of recyclable and biodegradable materials like paper and advanced plastics, alongside continued use of glass and metal. Innovations in primary, secondary, and tertiary packaging focus on lightweighting, enhanced barrier properties, and smart packaging for traceability. Challenges include volatile raw material prices and stringent environmental regulations, requiring adaptation in manufacturing processes. The competitive landscape features global players and significant Spanish and European entities, fostering innovation and strategic partnerships.

Spain Packaging Industry Company Market Share

Spain Packaging Industry Market Outlook: Innovation, Sustainability, and Growth to 2033

This comprehensive report delves into the dynamic Spain packaging industry, a sector projected for significant expansion and transformation. Analyzing the market from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this study provides invaluable insights into market structures, trends, key players, and future opportunities. Leveraging high-volume keywords such as packaging solutions Spain, sustainable packaging Spain, food packaging Spain, flexible packaging Spain, and glass packaging Spain, this report is meticulously crafted for industry professionals seeking a competitive edge. The study period covers the historical performance from 2019–2024, offering a robust foundation for future projections.

Spain Packaging Industry Market Structure & Competitive Landscape

The Spanish packaging market is characterized by a moderately consolidated structure, with a few key players holding significant market share in specific segments. Innovation remains a critical driver, with companies actively investing in R&D to develop advanced packaging materials and functionalities. Regulatory impacts, particularly concerning environmental sustainability and recyclability, are increasingly shaping market dynamics. The proliferation of eco-friendly alternatives and stringent waste management policies are pushing manufacturers towards sustainable packaging solutions. Product substitutes, such as the ongoing shift from rigid to flexible packaging in certain applications, also present a dynamic competitive landscape. End-user segmentation reveals the dominance of the food and beverage packaging Spain sector, followed by growing demand from healthcare and personal care. Mergers and acquisitions (M&A) activity, while not at extreme levels, is a notable trend, indicating strategic consolidation and market expansion efforts. For instance, an estimated XX Million in M&A deals were observed in the historical period, reflecting a strategic approach to growth and diversification within the packaging industry Spain. Concentration ratios, estimated to be in the range of XX% for the top 5 players in key segments, highlight the competitive intensity.

Spain Packaging Industry Market Trends & Opportunities

The Spain packaging market size is poised for substantial growth, driven by a confluence of evolving consumer preferences, technological advancements, and macroeconomic factors. Throughout the forecast period of 2025–2033, the industry is expected to witness a Compound Annual Growth Rate (CAGR) of approximately XX%, reaching an estimated XX Million by the end of the forecast horizon. This growth is fueled by an increasing demand for convenience, enhanced product shelf-life, and aesthetically appealing packaging, particularly within the food and beverage packaging Spain segment. Technological shifts are revolutionizing the industry, with a marked increase in the adoption of smart packaging solutions, including those with integrated traceability and anti-counterfeiting features, as exemplified by Sealed Air's PRISTIQ launch. The growing consumer consciousness regarding environmental impact is a significant trend, propelling the demand for sustainable packaging Spain, including recyclable, biodegradable, and compostable materials. This presents a significant opportunity for manufacturers to innovate and capture market share by offering eco-friendly alternatives. Competitive dynamics are intensifying, with both domestic and international players vying for dominance through product differentiation, strategic partnerships, and a focus on operational efficiency. The flexible packaging Spain segment, in particular, is experiencing robust growth due to its versatility and cost-effectiveness. Opportunities also lie in the expansion of e-commerce packaging Spain, catering to the burgeoning online retail sector. Market penetration rates for advanced packaging technologies Spain are projected to rise significantly, indicating a readiness for innovation across various end-user industries.

Dominant Markets & Segments in Spain Packaging Industry

Within the Spain packaging industry, the Plastic packaging segment continues to assert its dominance, driven by its versatility, cost-effectiveness, and suitability for a wide range of applications. This dominance is further bolstered by innovations in bioplastics and recycled plastics, aligning with sustainability trends. The Food and Beverage end-user industry remains the largest consumer of packaging solutions in Spain, accounting for an estimated XX% of the total market. Key growth drivers in this segment include the demand for ready-to-eat meals, fresh produce packaging, and beverages requiring extended shelf-life. The Primary Layer of packaging, directly in contact with the product, is critical for preservation and safety, experiencing steady demand.

Packaging Material Dominance:

- Plastic: Continues to lead due to its versatility, durability, and cost-effectiveness, with growing demand for recycled and biodegradable options.

- Paper and Paperboard: Strong performance driven by sustainable attributes and increasing use in e-commerce and premium food packaging.

- Glass: Experiencing a resurgence for its premium appeal and recyclability, particularly in the beverage and food sectors, with an increasing focus on lightweighting.

- Metal: Remains a staple for certain food products and beverages, with ongoing innovation in barrier properties and ease of opening.

End-User Industry Leadership:

- Food and Beverage: The undisputed leader, driven by population growth, changing dietary habits, and the demand for convenience.

- Healthcare and Pharmaceutical: Steady growth due to stringent regulatory requirements for product safety and integrity, and an aging population.

- Beauty and Personal Care: Driven by premiumization, product innovation, and the demand for attractive and functional packaging.

The Primary Layer of packaging holds significant market share due to its essential role in product protection and preservation across all end-user industries. Policies promoting recycling and circular economy principles are indirectly influencing material choices and driving innovation in sustainable packaging Spain.

Spain Packaging Industry Product Analysis

Product innovation in the Spanish packaging industry is heavily focused on enhancing sustainability, functionality, and consumer convenience. Innovations include the development of advanced barrier films for extended shelf-life in food packaging Spain, smart labels for product traceability, and lightweighted glass bottles to reduce transportation costs and environmental impact. The competitive advantage lies in offering tailored solutions that address specific industry needs, such as tamper-evident closures for pharmaceuticals or resealable pouches for convenience foods. Technological advancements in material science and manufacturing processes are enabling the creation of packaging that is both environmentally responsible and highly effective in protecting products.

Key Drivers, Barriers & Challenges in Spain Packaging Industry

The Spain packaging industry is propelled by several key drivers. Technological innovation, particularly in sustainable materials and smart packaging, is a significant growth catalyst. Economic factors, including a growing middle class and increasing disposable income, contribute to higher consumption and, consequently, packaging demand. Favorable government policies promoting a circular economy and waste reduction also play a crucial role. For example, the strategic cooperation between Fives and Verallia to lower carbon emissions in glass production exemplifies this trend.

Conversely, the industry faces several barriers and challenges. Stringent and evolving environmental regulations, while driving innovation, can also impose significant compliance costs and operational adjustments. Supply chain disruptions, as witnessed globally, can impact raw material availability and pricing, affecting production efficiency. Intense competitive pressures, both from established players and emerging entrants, necessitate continuous investment in R&D and cost optimization. The cost of adopting new, sustainable technologies can also be a restraint, particularly for smaller enterprises.

Growth Drivers in the Spain Packaging Industry Market

The Spain packaging industry is experiencing robust growth fueled by several factors. The increasing consumer demand for convenience and on-the-go consumption is driving the market for flexible and single-serving packaging solutions. Furthermore, the burgeoning e-commerce sector is creating a significant demand for specialized, durable, and protective e-commerce packaging. Technological advancements in material science are enabling the development of innovative sustainable packaging Spain, such as compostable films and biodegradable plastics, which are gaining traction among environmentally conscious consumers and businesses. Government initiatives aimed at promoting a circular economy and reducing plastic waste also act as strong growth catalysts, encouraging the adoption of recyclable and reusable packaging formats.

Challenges Impacting Spain Packaging Industry Growth

Despite the positive growth trajectory, the Spain packaging industry faces several challenges. The complex and ever-evolving regulatory landscape concerning packaging waste and recycling can pose significant compliance hurdles and increase operational costs for businesses. Fluctuations in raw material prices, particularly for plastics and paper, can impact profitability and necessitate proactive supply chain management strategies. Intense competition from both domestic and international players, coupled with the constant need for innovation to stay ahead of market trends, puts pressure on profit margins. Moreover, the investment required for adopting advanced sustainable packaging technologies can be substantial, posing a barrier for smaller and medium-sized enterprises.

Key Players Shaping the Spain Packaging Industry Market

- COVINIL S A

- Tetra Pak International S A

- Amcor PLC

- Mondi PLC

- Wipak Group

- Nekicesa Packaging SL

- Tecnocap S p A

- Plastipak Holdings Inc

- Sealed Air Corporation

Significant Spain Packaging Industry Industry Milestones

- July 2022: The industrial engineering firm Fives and Verallia, one of the third-largest makers of glass packaging for food and beverages worldwide, have formed strategic cooperation to lower carbon emissions and move toward greener glass production. With all-electric melting technologies supplied by Fives, Verallia is investing in the electric melting technologies of its Cognac production in France and Spain.

- April 2022: Sealed Air announced PRISTIQ, a digital packaging brand with a portfolio of solutions for design services, digital printing, and smart packaging, which eliminates waste and excess packaging while enhancing products and customer engagement.

Future Outlook for Spain Packaging Industry Market

The future outlook for the Spain packaging industry is highly promising, driven by sustained demand for innovative and sustainable solutions. The growing emphasis on a circular economy and the increasing consumer awareness regarding environmental impact will continue to fuel the demand for recyclable, reusable, and biodegradable packaging materials. The food and beverage packaging Spain sector is expected to remain a key growth engine, with further advancements in active and intelligent packaging to enhance food safety and extend shelf life. Opportunities also lie in the expansion of specialized packaging for niche markets, such as sustainable packaging for luxury goods and advanced pharmaceutical packaging. Strategic collaborations and investments in new technologies will be crucial for companies to maintain a competitive edge in this evolving market.

Spain Packaging Industry Segmentation

-

1. Packaging Material

- 1.1. Plastic

- 1.2. Paper

- 1.3. Glass

- 1.4. Metal

-

2. Layers of Packaging

- 2.1. Primary Layer

- 2.2. Secondary Layer

- 2.3. Tertiary Layer

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Beauty and Personal Care

- 3.4. Industrial

- 3.5. Other End-user Industry

Spain Packaging Industry Segmentation By Geography

- 1. Spain

Spain Packaging Industry Regional Market Share

Geographic Coverage of Spain Packaging Industry

Spain Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 5.1.1. Plastic

- 5.1.2. Paper

- 5.1.3. Glass

- 5.1.4. Metal

- 5.2. Market Analysis, Insights and Forecast - by Layers of Packaging

- 5.2.1. Primary Layer

- 5.2.2. Secondary Layer

- 5.2.3. Tertiary Layer

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Beauty and Personal Care

- 5.3.4. Industrial

- 5.3.5. Other End-user Industry

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6. Spain Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6.1.1. Plastic

- 6.1.2. Paper

- 6.1.3. Glass

- 6.1.4. Metal

- 6.2. Market Analysis, Insights and Forecast - by Layers of Packaging

- 6.2.1. Primary Layer

- 6.2.2. Secondary Layer

- 6.2.3. Tertiary Layer

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Beauty and Personal Care

- 6.3.4. Industrial

- 6.3.5. Other End-user Industry

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 COVINIL S A

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tetra Pak International S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Amcor PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mondi PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Wipak Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nekicesa Packaging SL

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Tecnocap S p A

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Plastipak Holdings Inc *List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sealed Air Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 COVINIL S A

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Packaging Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Spain Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Spain Packaging Industry Revenue million Forecast, by Packaging Material 2020 & 2033

- Table 2: Spain Packaging Industry Revenue million Forecast, by Layers of Packaging 2020 & 2033

- Table 3: Spain Packaging Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 4: Spain Packaging Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Spain Packaging Industry Revenue million Forecast, by Packaging Material 2020 & 2033

- Table 6: Spain Packaging Industry Revenue million Forecast, by Layers of Packaging 2020 & 2033

- Table 7: Spain Packaging Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 8: Spain Packaging Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Packaging Industry?

The projected CAGR is approximately 7.01%.

2. Which companies are prominent players in the Spain Packaging Industry?

Key companies in the market include COVINIL S A, Tetra Pak International S A, Amcor PLC, Mondi PLC, Wipak Group, Nekicesa Packaging SL, Tecnocap S p A, Plastipak Holdings Inc *List Not Exhaustive, Sealed Air Corporation.

3. What are the main segments of the Spain Packaging Industry?

The market segments include Packaging Material, Layers of Packaging, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 620 million as of 2022.

5. What are some drivers contributing to market growth?

Innovative and Premium Packaging to Drive the Market; Rising Demand for Small and Convenient Packaging.

6. What are the notable trends driving market growth?

Paper Based Packaging is Expected Hold a Significant Share.

7. Are there any restraints impacting market growth?

Stringent Rules and Regulations Regarding Packaging Materials.

8. Can you provide examples of recent developments in the market?

July 2022 - The industrial engineering firm Fives and Verallia, one of the third-largest makers of glass packaging for food and beverages worldwide, have formed strategic cooperation to lower carbon emissions and move toward greener glass production. With all-electric melting technologies supplied by Fives, Verallia is investing in the electric melting technologies of its Cognac production in France and Spain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Packaging Industry?

To stay informed about further developments, trends, and reports in the Spain Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence