Key Insights

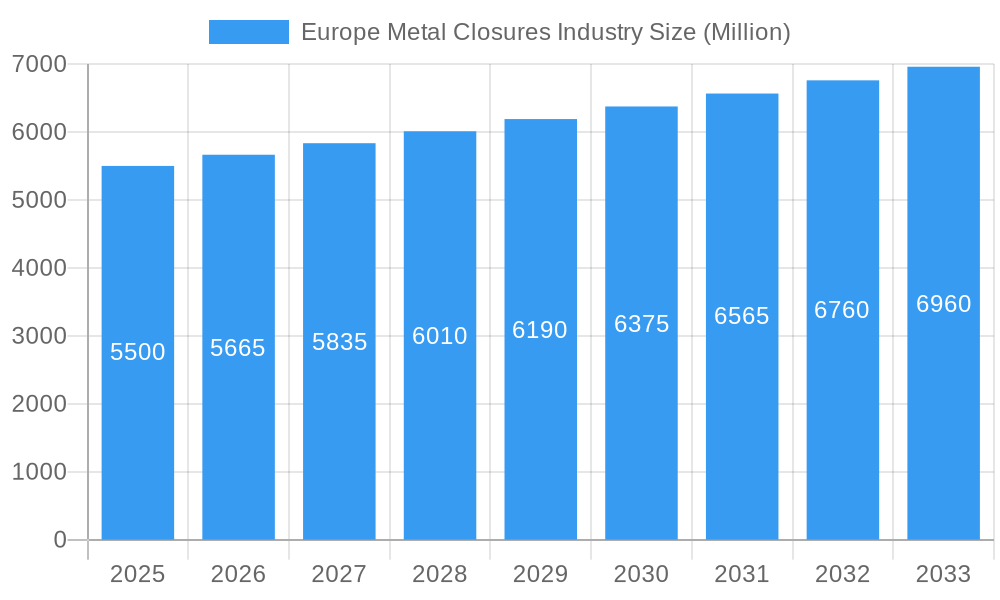

The European metal closures market is projected for robust expansion, anticipated to reach $9.79 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.28% through 2033. This growth is propelled by sustained demand from the food and beverage sectors, the primary end-user segments. Increasing consumer preference for product safety, extended shelf-life, and convenient packaging solutions drives the demand for premium metal closures. The pharmaceutical industry's ongoing need for secure, tamper-evident, and sterile packaging also significantly influences market dynamics. Emerging economies within Europe, alongside established markets like Germany, the UK, and France, are expected to experience considerable growth, fueled by rising disposable incomes and evolving consumption patterns.

Europe Metal Closures Industry Market Size (In Billion)

While the market outlook is generally positive, challenges such as fluctuating raw material costs for aluminum and steel can impact manufacturing expenses. The competitive landscape includes the increasing adoption of alternative packaging materials for specific applications. Nevertheless, the inherent durability, superior barrier properties, and recyclability of metal closures ensure their continued relevance, particularly for premium products and applications requiring stringent safety and preservation standards. Leading industry players are investing in sustainable manufacturing practices and advanced closure technologies to maintain a competitive edge and adapt to evolving regulatory requirements and consumer expectations. The forecast period indicates sustained, moderate growth, highlighting the enduring importance of metal closures in the European packaging sector.

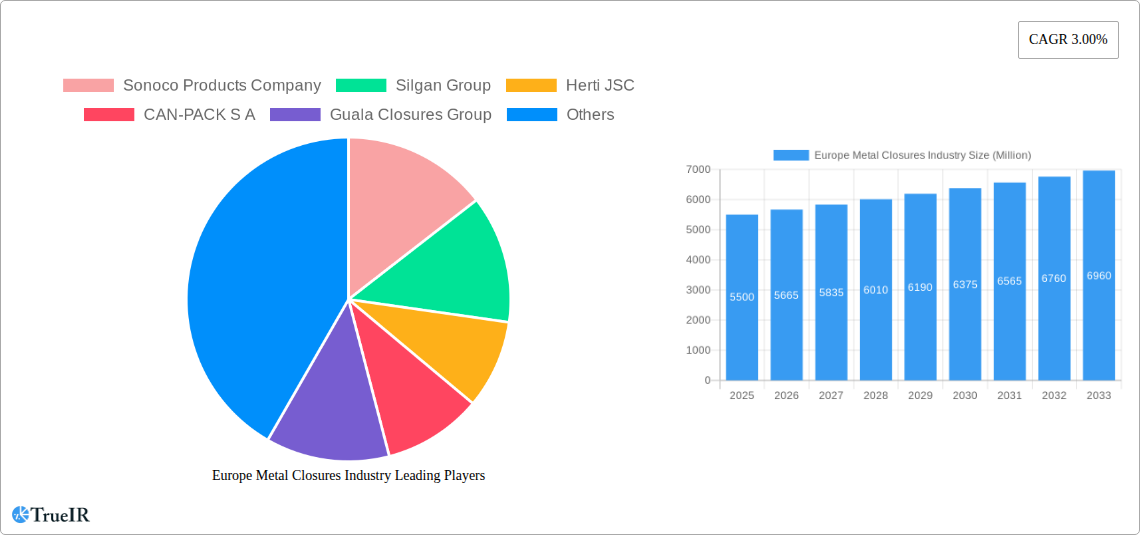

Europe Metal Closures Industry Company Market Share

This comprehensive report offers an in-depth analysis of the dynamic Europe metal closures market, examining its structure, competitive landscape, key trends, opportunities, and future outlook for the period 2019-2033. The analysis focuses on the base year 2025 and the forecast period 2025-2033. Key market participants include Sonoco Products Company, Silgan Group, Herti JSC, CAN-PACK S A, Guala Closures Group, Technocap Group, Crown Holdings Incorporated, and Pelliconi & C SpA. Market segmentation includes Food metal closures, Beverage metal closures, Pharmaceuticals metal closures, and Other End-User Industries metal closures.

Europe Metal Closures Industry Market Structure & Competitive Landscape

The Europe metal closures market exhibits a moderate to high concentration, with leading players accounting for a significant portion of the market share. Innovation drivers are primarily focused on enhanced functionality, sustainability, and improved user experience, including features like child-resistance, tamper-evidence, and ease of opening. Regulatory impacts, particularly concerning food safety and environmental standards, play a crucial role in shaping product development and manufacturing processes across the metal can lids market. Product substitutes, such as plastic closures and alternative packaging formats, present a constant competitive pressure, necessitating continuous innovation and cost optimization within the metal caps and closures industry. End-user segmentation reveals the dominance of the Food and Beverage sectors, driven by high consumption volumes. However, the Pharmaceuticals segment demonstrates strong growth potential due to stringent packaging requirements and increasing demand for sterile and secure closures. Mergers and acquisitions (M&A) are a key feature of the competitive landscape, with companies strategically consolidating to expand their market reach, acquire new technologies, and achieve economies of scale. For instance, the period saw an estimated X million in M&A deal values, impacting market concentration ratios and driving industry consolidation. The competitive landscape is characterized by intense price competition, alongside a growing emphasis on product differentiation and value-added services.

Europe Metal Closures Industry Market Trends & Opportunities

The Europe metal closures industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period. This expansion is fueled by several converging trends. A primary trend is the escalating consumer demand for convenience and portability, which directly translates to a higher need for secure and easily accessible metal closures for a wide array of products. The beverage can lids market and food tin lids market are particularly benefiting from this trend. Technological advancements are revolutionizing the manufacturing processes, leading to lighter, more durable, and cost-effective metal closures. Innovations in coatings and sealing technologies are enhancing product shelf-life and safety, particularly crucial for the pharmaceutical closures market. Consumer preference for sustainable packaging solutions is also a significant market driver. While traditionally perceived as less sustainable than some alternatives, ongoing advancements in metal recycling infrastructure and the development of metal closures with reduced material usage are improving their environmental footprint. This shift towards sustainability presents a substantial opportunity for manufacturers to innovate and differentiate their offerings in the metal caps for bottles market. Furthermore, the growing e-commerce sector is creating new avenues for growth, demanding robust and protective packaging solutions for shipping, where metal closures play a vital role in product integrity. The metal closures for jars market is also seeing steady demand due to the enduring popularity of preserved goods and specialty food items. Emerging markets within Europe, coupled with evolving dietary habits and an increasing middle class, are contributing to sustained demand across all end-user segments. The market penetration rate for metal closures remains high, yet opportunities exist in niche applications and premium product segments where enhanced aesthetics and functionality command a premium. The increasing focus on food security and waste reduction further bolsters the demand for reliable and effective metal closures.

Dominant Markets & Segments in Europe Metal Closures Industry

The Food segment stands as the dominant market within the Europe Metal Closures Industry, accounting for an estimated XX% of the total market share. This dominance is driven by the sheer volume of packaged food products consumed across the continent, ranging from canned fruits and vegetables to processed meats and dairy products. Key growth drivers within this segment include the persistent demand for shelf-stable food options, the growing popularity of ready-to-eat meals, and the expansion of private label brands. The widespread availability of advanced canning and sealing technologies ensures the integrity and extended shelf-life of food products, making metal closures the preferred choice for many manufacturers. The Beverage segment follows closely, with an estimated XX% market share, propelled by the ubiquitous presence of canned soft drinks, beers, and other beverages. Growth in this segment is supported by evolving consumer preferences for on-the-go consumption, the increasing demand for healthier beverage options packaged in cans, and the continuous innovation in beverage formulations. The infrastructure for beverage canning is well-established across Europe, further solidifying the position of metal closures. The Pharmaceuticals segment, while representing a smaller market share, demonstrates impressive growth potential. Its importance cannot be overstated, driven by stringent regulatory requirements for drug packaging, the need for absolute sterility, and the imperative for tamper-evident and child-resistant closures. The rise in chronic diseases and an aging population are key factors contributing to increased pharmaceutical production and, consequently, the demand for specialized metal closures. Within the geographical landscape, Germany and France consistently emerge as leading markets due to their large industrial bases and significant consumer spending power. Robust manufacturing capabilities, coupled with favorable government policies supporting industrial growth and food safety, contribute to their market dominance. The ongoing investments in modern packaging technologies and the presence of major food and beverage manufacturers within these countries further bolster their leading positions in the metal closures market.

Europe Metal Closures Industry Product Analysis

Innovations in the Europe metal closures industry are primarily focused on enhancing functionality, sustainability, and aesthetics. Advancements include the development of lighter-weight metal caps and closures that reduce material consumption without compromising structural integrity. Improved sealing technologies ensure superior barrier properties, extending product shelf-life and preventing spoilage, particularly crucial for food and pharmaceutical applications. The industry is also witnessing a surge in the development of child-resistant and tamper-evident closures, catering to increasing safety regulations and consumer expectations. For example, innovative designs in metal twist-off caps and screw caps offer enhanced ease of use and improved resealability. These product innovations provide manufacturers with competitive advantages by meeting evolving market demands for safer, more convenient, and environmentally responsible packaging solutions.

Key Drivers, Barriers & Challenges in Europe Metal Closures Industry

Key Drivers:

- Growing Consumer Demand for Packaged Goods: Increased consumption of processed foods, beverages, and pharmaceuticals directly fuels the need for metal closures.

- Technological Advancements: Innovations in manufacturing processes lead to more efficient, cost-effective, and functional metal closures.

- Sustainability Initiatives: Growing emphasis on recyclable and reusable packaging solutions, with metal being a highly recyclable material, presents a significant driver.

- Stringent Regulatory Standards: Demand for safe, secure, and tamper-evident packaging in the pharmaceutical and food sectors drives innovation in closure technologies.

- Expanding E-commerce Sector: The need for robust packaging to ensure product integrity during shipping supports the demand for durable metal closures.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the prices of metals like aluminum and steel can impact manufacturing costs and profitability.

- Competition from Alternative Materials: Plastic closures and other innovative packaging materials pose a competitive threat, necessitating continuous product improvement and cost competitiveness for metal closures.

- Supply Chain Disruptions: Global supply chain issues can affect the availability and cost of raw materials and finished products.

- Environmental Concerns (Perception vs. Reality): While metal is highly recyclable, negative perceptions regarding its environmental impact compared to some alternatives can be a challenge to overcome.

- Economic Downturns: Reduced consumer spending during economic recessions can lead to decreased demand for packaged goods and, consequently, metal closures.

Growth Drivers in the Europe Metal Closures Industry Market

The Europe metal closures industry is propelled by several key growth drivers. Technological innovation remains paramount, with advancements in lightweighting and advanced coating technologies leading to more efficient and cost-effective solutions. The increasing consumer preference for convenient, single-serve packaging across both food and beverage sectors directly translates into a higher demand for metal closures. Furthermore, stringent regulations surrounding food safety and pharmaceutical packaging continue to necessitate the use of secure, tamper-evident, and sterile metal closure systems. The growing emphasis on sustainability is also a significant driver, as metal closures are highly recyclable, aligning with circular economy principles. The expansion of the e-commerce market further bolsters demand, as metal closures provide the necessary protection for products during transit.

Challenges Impacting Europe Metal Closures Industry Growth

Despite robust growth prospects, the Europe metal closures industry faces several challenges. Fluctuations in the prices of key raw materials, such as aluminum and steel, can significantly impact manufacturing costs and profit margins. Intense competition from alternative packaging materials, particularly plastics, continues to exert pressure on market share. Global supply chain disruptions, as experienced in recent years, can lead to material shortages and increased lead times, affecting production schedules. Moreover, while metal is inherently recyclable, overcoming negative consumer perceptions regarding its environmental footprint compared to some emerging alternatives remains a continuous effort. Economic uncertainties and potential recessions can also dampen consumer spending on packaged goods, indirectly affecting the demand for metal closures.

Key Players Shaping the Europe Metal Closures Industry Market

- Sonoco Products Company

- Silgan Group

- Herti JSC

- CAN-PACK S A

- Guala Closures Group

- Technocap Group

- Crown Holdings Incorporated

- Pelliconi & C SpA

Significant Europe Metal Closures Industry Industry Milestones

- 2019: Introduction of advanced tamper-evident sealing technologies by Guala Closures Group, enhancing product security.

- 2020: Sonoco Products Company acquires various packaging assets, expanding its market footprint in metal closures.

- 2021: Herti JSC invests significantly in new production lines to increase capacity for beverage can lids.

- 2022: CAN-PACK S A focuses on lightweighting initiatives for aluminum closures, contributing to sustainability goals.

- 2023: Silgan Group announces strategic partnerships to develop innovative closure solutions for the pharmaceutical sector.

- 2024: Crown Holdings Incorporated launches new recyclable metal closures with improved grip and opening features.

Future Outlook for Europe Metal Closures Industry Market

The future outlook for the Europe metal closures industry is exceptionally positive, driven by continued innovation, evolving consumer preferences, and a strong emphasis on sustainability. The increasing demand for convenience and product safety across the Food, Beverage, and Pharmaceutical sectors will remain a primary growth catalyst. Advancements in material science and manufacturing technologies are expected to yield even lighter, more functional, and environmentally friendly metal closures. Strategic opportunities lie in further developing specialized closures for niche markets, expanding recycling infrastructure, and leveraging digital technologies for enhanced supply chain management and customer engagement. The industry is poised for sustained growth, offering attractive prospects for stakeholders invested in this essential segment of the packaging market.

Europe Metal Closures Industry Segmentation

-

1. End-user

- 1.1. Food

- 1.2. Beverage

- 1.3. Pharmaceuticals

- 1.4. Other End-User Industries

Europe Metal Closures Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

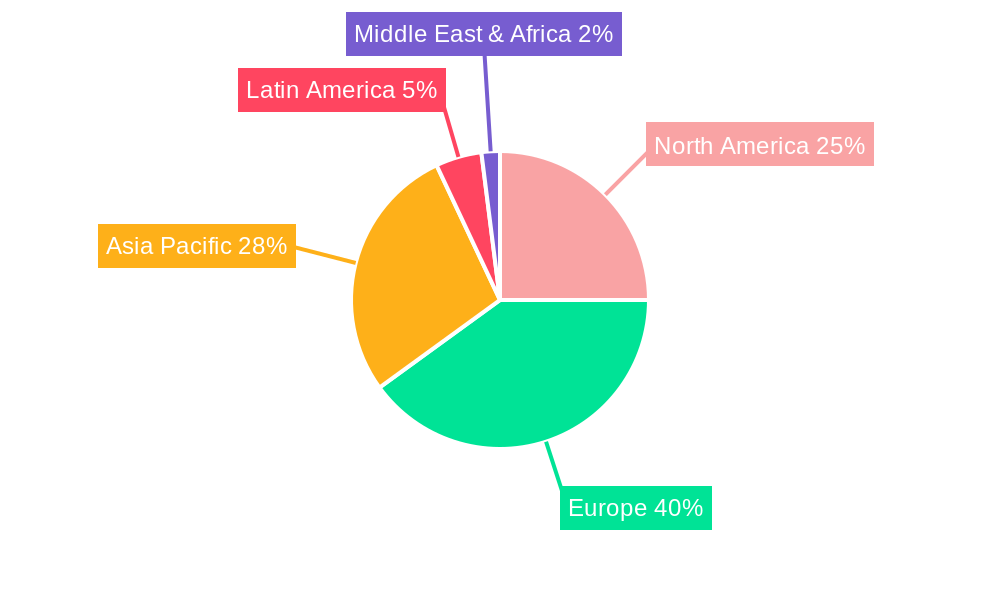

Europe Metal Closures Industry Regional Market Share

Geographic Coverage of Europe Metal Closures Industry

Europe Metal Closures Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user

- 5.1.1. Food

- 5.1.2. Beverage

- 5.1.3. Pharmaceuticals

- 5.1.4. Other End-User Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End-user

- 6. Europe Metal Closures Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user

- 6.1.1. Food

- 6.1.2. Beverage

- 6.1.3. Pharmaceuticals

- 6.1.4. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by End-user

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sonoco Products Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Silgan Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Herti JSC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CAN-PACK S A

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Guala Closures Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Technocap Group*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Crown Holdings Incorporated

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pelliconi & C SpA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Sonoco Products Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Metal Closures Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Metal Closures Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Metal Closures Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 2: Europe Metal Closures Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Metal Closures Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 4: Europe Metal Closures Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Metal Closures Industry?

The projected CAGR is approximately 4.28%.

2. Which companies are prominent players in the Europe Metal Closures Industry?

Key companies in the market include Sonoco Products Company, Silgan Group, Herti JSC, CAN-PACK S A, Guala Closures Group, Technocap Group*List Not Exhaustive, Crown Holdings Incorporated, Pelliconi & C SpA.

3. What are the main segments of the Europe Metal Closures Industry?

The market segments include End-user .

4. Can you provide details about the market size?

The market size is estimated to be USD 9.79 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumption of Convenience Food; Innovation and Added Value Offering to Change the Image of Food Cans.

6. What are the notable trends driving market growth?

Beverage Industry Expected to Exhibit Maximum Adoption.

7. Are there any restraints impacting market growth?

; Stringent Regulations on the Usage of Plastic Bottles.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Metal Closures Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Metal Closures Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Metal Closures Industry?

To stay informed about further developments, trends, and reports in the Europe Metal Closures Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence