Key Insights

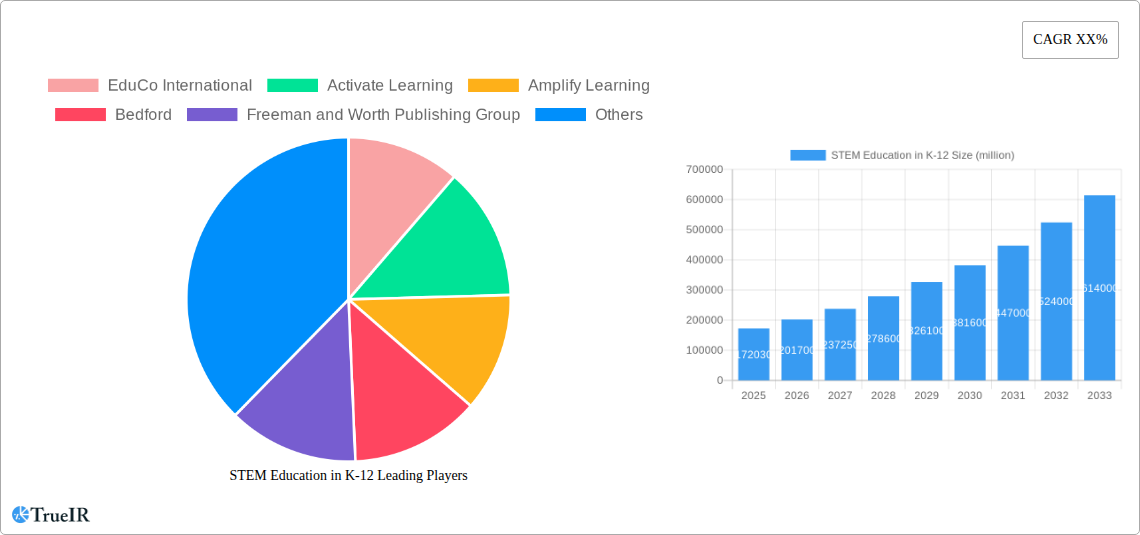

The global STEM Education market for K-12 students is poised for substantial growth, projected to reach $172.03 billion in 2025. This impressive expansion is driven by a compelling CAGR of 17.47% over the forecast period. The increasing recognition of the critical importance of STEM skills for future career success and national economic competitiveness is a primary catalyst. Educational institutions worldwide are prioritizing the integration of science, technology, engineering, and mathematics into their curricula, aiming to equip young learners with the foundational knowledge and critical thinking abilities necessary to thrive in an increasingly complex and technology-driven world. Furthermore, government initiatives and private sector investments are bolstering the development of innovative teaching methodologies, interactive learning platforms, and hands-on educational resources, all contributing to a more engaging and effective STEM learning experience for students across all age groups within the K-12 spectrum.

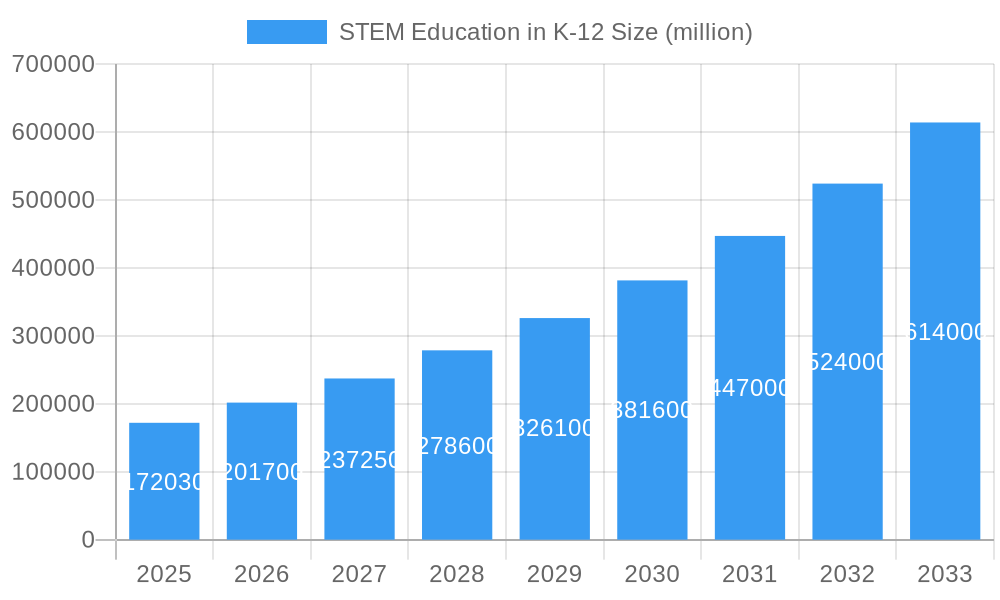

STEM Education in K-12 Market Size (In Billion)

The market is characterized by a dynamic interplay of robust demand for customized learning experiences and the widespread adoption of standardized recorded courses, catering to diverse educational needs and learning styles. The "5-6 years old" segment, focused on early exposure and foundational concepts, is witnessing significant uptake, laying the groundwork for future academic pursuits. Similarly, the "13-18 years old" segment is experiencing a surge in demand for advanced STEM content and specialized training to prepare students for higher education and emerging career fields. Key market drivers include the escalating need for a skilled STEM workforce to fuel technological advancements and address global challenges, alongside the continuous evolution of educational technologies that enhance accessibility and engagement. While the market shows immense promise, potential restraints could arise from disparities in educational resource allocation across regions and the ongoing need for teacher training to effectively implement new STEM curricula. Nonetheless, the overarching trend points towards a dynamic and expanding market for K-12 STEM education.

STEM Education in K-12 Company Market Share

Report Title: Navigating the Future: A Comprehensive Analysis of the K-12 STEM Education Market (2019-2033)

Report Description: Unlock critical insights into the burgeoning K-12 STEM Education market. This definitive report, covering the study period from 2019 to 2033 with a base and estimated year of 2025, provides an in-depth analysis of market structure, trends, and opportunities. We meticulously dissect market concentration, innovation drivers, and regulatory impacts, alongside exploring product substitutes and end-user segmentation. With a projected market size of billions, this report identifies dominant regions and segments, including detailed breakdowns for 5-6 year olds, 7-12 year olds, and 13-18 year olds, and analyzes the competitive landscape of Customized Live Courses, Standard Recorded Courses, and Other types of STEM education. Discover the pivotal role of key players like EduCo International, Activate Learning, Amplify Learning, Bedford, Freeman and Worth Publishing Group, Carolina Biological Supply, Cengage Learning, Discovery Education, Houghton Mifflin Harcourt, Kendall Hunt Publishing Company, Lab-Aids, McGraw Hill, OpenSciEd, PASCO Scientific, Savvas Learning, and School Specialty. Examine significant industry milestones and understand the key drivers, barriers, and future outlook shaping this dynamic sector. This report is essential for educators, policymakers, investors, and technology providers seeking to capitalize on the billions in growth opportunities within the K-12 STEM education sector.

STEM Education in K-12 Market Structure & Competitive Landscape

The K-12 STEM Education market exhibits a moderately concentrated structure, with a significant portion of market share held by a few dominant players, estimated at billions in value. Innovation drivers are heavily influenced by the integration of advanced technologies such as AI-powered personalized learning platforms, virtual reality (VR) and augmented reality (AR) for immersive experiences, and sophisticated data analytics to track student progress. Regulatory impacts are increasingly positive, with governments worldwide implementing policies to boost STEM education funding and curriculum development, aiming to produce a future-ready workforce. Product substitutes are emerging, including free online educational resources and open-source learning materials, though dedicated K-12 STEM solutions offer a more structured and comprehensive approach. End-user segmentation clearly divides the market by age group: 5-6 years old, 7-12 years old, and 13-18 years old, each with distinct pedagogical needs and product demands. Mergers and acquisition (M&A) trends indicate consolidation among providers, driven by the desire to expand product portfolios, gain market access, and achieve economies of scale, with an estimated billions in M&A activity projected over the forecast period. Key M&A drivers include the acquisition of innovative technologies and the expansion into new geographic markets.

STEM Education in K-12 Market Trends & Opportunities

The K-12 STEM Education market is experiencing robust growth, projected to reach a valuation of billions by the end of the forecast period in 2033, with an estimated Compound Annual Growth Rate (CAGR) of xx% from the base year of 2025. This expansion is fueled by a confluence of transformative technological shifts, evolving consumer preferences, and dynamic competitive forces. The increasing demand for digital learning solutions, accelerated by recent global events, has pushed the adoption of online platforms, interactive simulations, and AI-driven personalized learning experiences. Educational technology (EdTech) companies are investing heavily in research and development, leading to the introduction of cutting-edge tools that enhance engagement and improve learning outcomes in science, technology, engineering, and mathematics.

Consumer preferences are shifting towards more hands-on, project-based learning approaches that foster critical thinking, problem-solving, and creativity. Parents and educators are recognizing the long-term career benefits of a strong STEM foundation, leading to higher demand for specialized STEM curricula and extracurricular activities. This sentiment is particularly pronounced in the 13-18 years old segment, where students are preparing for higher education and future careers.

The competitive landscape is characterized by both established educational publishers and agile EdTech startups. Companies are differentiating themselves through unique content delivery methods, adaptive learning technologies, and comprehensive support services. Partnerships between technology providers and educational institutions are becoming increasingly common, facilitating the integration of new tools and curricula into classrooms. The market penetration rate for digital STEM learning solutions is steadily increasing, especially in developed regions, but significant opportunities remain in emerging economies where infrastructure development and government initiatives are prioritizing STEM education.

Furthermore, the focus on inclusivity and equity in education presents a substantial opportunity. Providers are developing accessible STEM resources and platforms that cater to diverse learning needs and socio-economic backgrounds, widening the market's reach. The growing awareness of the skills gap in STEM fields globally is a primary catalyst, driving investment and innovation across all segments of the K-12 education ecosystem. The market is ripe for solutions that can effectively demonstrate measurable improvements in student engagement and academic achievement, thereby securing greater market share and influencing educational policy.

Dominant Markets & Segments in STEM Education in K-12

The K-12 STEM Education market is characterized by the dominance of specific regions and segments, driven by robust infrastructure, supportive governmental policies, and a high propensity for technological adoption.

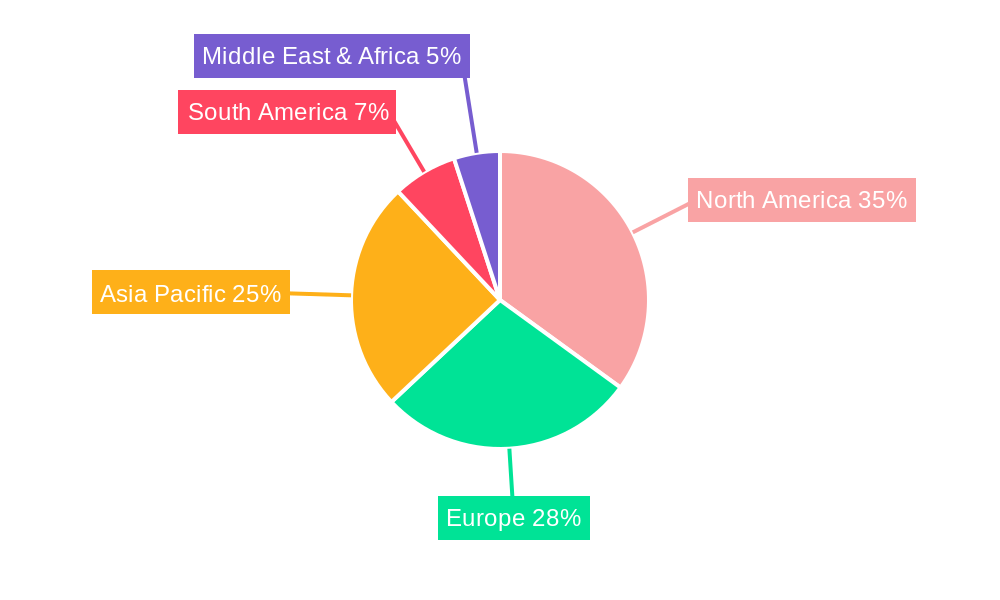

Leading Region: North America and Asia-Pacific are emerging as dominant markets, collectively representing a significant portion of the global K-12 STEM education market value, estimated at billions.

North America:

- Key Growth Drivers: Strong emphasis on innovation in curriculum development, substantial private and public investment in EdTech, and a well-established network of K-12 institutions actively seeking to integrate advanced STEM learning tools. Government initiatives to promote STEM careers and a high adoption rate of digital learning technologies further bolster its position.

- Detailed Analysis: The region benefits from a mature educational ecosystem that readily embraces new pedagogical approaches. Federal and state-level funding initiatives aimed at improving STEM education, coupled with the presence of leading technology companies, create a fertile ground for market growth. The demand for personalized learning experiences and adaptive assessment tools is particularly high.

Asia-Pacific:

- Key Growth Drivers: Rapidly growing student populations, increasing government focus on STEM education to drive economic growth, and a burgeoning middle class with a strong emphasis on quality education for their children. The widespread adoption of mobile devices and increasing internet penetration are also key enablers.

- Detailed Analysis: Countries like China and India are witnessing exponential growth in their K-12 STEM education markets. Governments are actively investing in STEM infrastructure, teacher training, and curriculum reforms. The demand for affordable yet effective online learning solutions is immense, creating significant opportunities for providers who can cater to large student cohorts.

Dominant Application Segments:

13-18 years old: This segment is the largest contributor to the K-12 STEM education market, valued at billions, due to the critical stage of career exploration and preparation for higher education.

- Key Growth Drivers: Increased focus on advanced STEM subjects, preparation for standardized college entrance exams, and the growing recognition of the need for specialized skills in fields like computer science, robotics, and bio-engineering. The demand for in-depth online courses, virtual labs, and coding bootcamps is particularly high.

- Detailed Analysis: As students in this age group approach critical junctures in their academic and professional journeys, there is a heightened demand for rigorous STEM programs that provide a competitive edge. This segment benefits from the availability of more sophisticated learning tools and curricula that align with university-level expectations.

7-12 years old: This segment is also a substantial contributor, valued at billions, focusing on foundational STEM concepts and fostering early interest.

- Key Growth Drivers: Growing awareness among parents and educators about the importance of early STEM exposure, the development of engaging and interactive learning materials, and the integration of STEM into mainstream curricula. The shift towards inquiry-based learning methods is a significant factor.

- Detailed Analysis: Early exposure to STEM principles is crucial for building a strong foundation. This segment thrives on gamified learning experiences, project-based activities, and hands-on kits that make learning fun and accessible, encouraging curiosity and a positive attitude towards STEM subjects.

Dominant Types of Offerings:

Standard Recorded Courses: This segment, valued at billions, offers scalability and affordability, making it accessible to a wider audience.

- Key Growth Drivers: Cost-effectiveness, flexibility for students to learn at their own pace, and the ability of educational institutions to integrate pre-recorded content into blended learning models.

- Detailed Analysis: Standard recorded courses provide a consistent and reliable learning experience. Their widespread availability through various platforms makes them a popular choice for both individual learners and institutions looking to supplement their teaching resources without incurring high costs associated with live instruction.

Customized Live Courses: While a smaller segment valued at billions, this offers high engagement and personalized attention.

- Key Growth Drivers: The demand for immediate feedback, direct interaction with instructors and peers, and tailored learning experiences that can address specific student needs or curriculum gaps.

- Detailed Analysis: Customized live courses, often delivered through virtual classrooms, provide a highly interactive and engaging learning environment. They are particularly valuable for advanced topics, specialized skill development, and for students who thrive in a more guided and responsive setting.

STEM Education in K-12 Product Analysis

The K-12 STEM Education market is witnessing an influx of innovative products designed to enhance learning and engagement. These innovations center around interactive digital platforms, virtual and augmented reality (VR/AR) simulations for immersive scientific exploration, and AI-powered adaptive learning systems that personalize instruction based on individual student progress. Competitive advantages are being gained by products that offer seamless integration with existing school IT infrastructure, provide robust analytics for educators to track student performance, and deliver hands-on learning experiences through robotics kits, coding platforms, and digital science labs. The market fit for these products is strong, driven by a growing demand for future-ready skills and a desire to make complex STEM concepts more accessible and engaging for students across all age groups.

Key Drivers, Barriers & Challenges in STEM Education in K-12

Key Drivers: The K-12 STEM Education market is propelled by several critical drivers, estimated to contribute billions to its growth. These include:

- Technological Advancements: The integration of AI, VR, AR, and gamification is revolutionizing how STEM is taught and learned, creating more engaging and effective learning experiences.

- Government Initiatives & Funding: Global governments are increasingly prioritizing STEM education through policy reforms, curriculum development support, and direct financial investment to address skills gaps and foster innovation, injecting billions into the sector.

- Growing Demand for STEM Careers: The escalating need for skilled professionals in science, technology, engineering, and mathematics fields globally is creating a strong pull for early STEM education.

- Parental and Educator Awareness: An increasing understanding of the long-term benefits of STEM proficiency is leading to higher demand for quality STEM resources.

Barriers & Challenges: Despite the growth potential, the market faces several significant barriers and challenges, impacting an estimated billions in potential expansion.

- Digital Divide and Equity: Unequal access to technology and reliable internet connectivity in some regions and socio-economic groups hinders widespread adoption and creates educational disparities.

- Teacher Training and Professional Development: A shortage of adequately trained STEM educators and a need for continuous professional development to keep pace with evolving technologies and pedagogy present a significant hurdle.

- Curriculum Integration and Standardization: Challenges in effectively integrating new STEM curricula into existing educational frameworks and achieving standardization across diverse school systems can slow down adoption.

- Cost of Technology and Resources: The initial investment in advanced STEM hardware, software, and specialized curriculum materials can be prohibitive for some schools and districts, limiting access.

Growth Drivers in the STEM Education in K-12 Market

The growth of the K-12 STEM Education market, projected to contribute billions in value, is significantly influenced by several key factors. Technological innovation remains a primary catalyst, with advancements in AI, machine learning, and immersive technologies like VR and AR making STEM learning more interactive, personalized, and engaging for students. Government policies and funding are instrumental, with an increasing number of nations prioritizing STEM education to cultivate a future-ready workforce and boost economic competitiveness. For instance, the billions allocated in national budgets for STEM initiatives directly translate into increased demand for educational resources and platforms. Economic factors, such as rising disposable incomes and a growing middle class in emerging economies, are also driving demand for higher-quality education, including specialized STEM programs.

Challenges Impacting STEM Education in K-12 Growth

Several challenges are impacting the growth trajectory of the STEM Education in K-12 market, potentially limiting its expansion by billions. Regulatory complexities, including varying curriculum standards and approval processes across different regions, can slow down the widespread adoption of new educational products. Supply chain issues, particularly for hardware-intensive STEM kits and equipment, can lead to delays and increased costs, impacting accessibility. Competitive pressures are also intensifying, with a crowded market demanding constant innovation and differentiation. Furthermore, the digital divide remains a significant barrier, as unequal access to technology and reliable internet connectivity in certain communities prevents an equitable distribution of STEM learning opportunities.

Key Players Shaping the STEM Education in K-12 Market

- EduCo International

- Activate Learning

- Amplify Learning

- Bedford, Freeman and Worth Publishing Group

- Carolina Biological Supply

- Cengage Learning

- Discovery Education

- Houghton Mifflin Harcourt

- Kendall Hunt Publishing Company

- Lab-Aids

- McGraw Hill

- OpenSciEd

- PASCO Scientific

- Savvas Learning

- School Specialty

Significant STEM Education in K-12 Industry Milestones

- 2019: Increased adoption of coding and robotics programs in elementary schools, signifying a shift towards early exposure to computational thinking.

- 2020: Widespread implementation of remote learning solutions due to global health events, accelerating the demand for digital STEM content and platforms.

- 2021: Launch of advanced VR/AR educational tools for science labs, enabling more immersive and interactive learning experiences for millions of students.

- 2022: Significant government investments in STEM teacher training programs across multiple countries to address the skills gap and improve educational quality.

- 2023: Emergence of AI-powered personalized learning platforms that adapt to individual student needs, offering tailored STEM pathways.

- 2024: Growth in project-based learning initiatives and the integration of real-world problem-solving into K-12 STEM curricula.

Future Outlook for STEM Education in K-12 Market

The future outlook for the K-12 STEM Education market is exceptionally bright, with projected growth contributing billions to the global educational landscape. Continued technological advancements, including sophisticated AI-driven learning, widespread adoption of VR/AR, and the development of accessible digital platforms, will be key growth catalysts. Strategic opportunities lie in addressing the global demand for personalized learning, bridging the digital divide through innovative solutions, and fostering stronger partnerships between educational institutions, technology providers, and policymakers. The increasing emphasis on developing critical thinking, problem-solving, and computational skills positions the K-12 STEM education market for sustained expansion and profound impact on future generations.

STEM Education in K-12 Segmentation

-

1. Application

- 1.1. 5~6 years old

- 1.2. 7~12 years old

- 1.3. 13~18 years old

-

2. Types

- 2.1. Customized Live Courses

- 2.2. Standard Recorded Courses

- 2.3. Others

STEM Education in K-12 Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

STEM Education in K-12 Regional Market Share

Geographic Coverage of STEM Education in K-12

STEM Education in K-12 REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. 5~6 years old

- 5.1.2. 7~12 years old

- 5.1.3. 13~18 years old

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Customized Live Courses

- 5.2.2. Standard Recorded Courses

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. 5~6 years old

- 6.1.2. 7~12 years old

- 6.1.3. 13~18 years old

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Customized Live Courses

- 6.2.2. Standard Recorded Courses

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. 5~6 years old

- 7.1.2. 7~12 years old

- 7.1.3. 13~18 years old

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Customized Live Courses

- 7.2.2. Standard Recorded Courses

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. 5~6 years old

- 8.1.2. 7~12 years old

- 8.1.3. 13~18 years old

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Customized Live Courses

- 8.2.2. Standard Recorded Courses

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. 5~6 years old

- 9.1.2. 7~12 years old

- 9.1.3. 13~18 years old

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Customized Live Courses

- 9.2.2. Standard Recorded Courses

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific STEM Education in K-12 Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. 5~6 years old

- 10.1.2. 7~12 years old

- 10.1.3. 13~18 years old

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Customized Live Courses

- 10.2.2. Standard Recorded Courses

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 EduCo International

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Activate Learning

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Amplify Learning

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bedford

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Freeman and Worth Publishing Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Carolina Biological Supply

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cengage Learning

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Discovery Education

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Houghton Mifflin Harcourt

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Kendall Hunt Publishing Company

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Lab-Aids

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 McGraw Hill

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 OpenSciEd

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 PASCO Scientifc

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Savvas Learning

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 School Specialty

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 EduCo International

List of Figures

- Figure 1: Global STEM Education in K-12 Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America STEM Education in K-12 Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America STEM Education in K-12 Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America STEM Education in K-12 Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America STEM Education in K-12 Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America STEM Education in K-12 Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America STEM Education in K-12 Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America STEM Education in K-12 Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America STEM Education in K-12 Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America STEM Education in K-12 Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America STEM Education in K-12 Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America STEM Education in K-12 Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America STEM Education in K-12 Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe STEM Education in K-12 Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe STEM Education in K-12 Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe STEM Education in K-12 Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe STEM Education in K-12 Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe STEM Education in K-12 Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe STEM Education in K-12 Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa STEM Education in K-12 Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa STEM Education in K-12 Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa STEM Education in K-12 Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa STEM Education in K-12 Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa STEM Education in K-12 Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa STEM Education in K-12 Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific STEM Education in K-12 Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific STEM Education in K-12 Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific STEM Education in K-12 Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific STEM Education in K-12 Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific STEM Education in K-12 Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific STEM Education in K-12 Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global STEM Education in K-12 Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global STEM Education in K-12 Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global STEM Education in K-12 Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global STEM Education in K-12 Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global STEM Education in K-12 Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global STEM Education in K-12 Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global STEM Education in K-12 Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global STEM Education in K-12 Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific STEM Education in K-12 Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the STEM Education in K-12?

The projected CAGR is approximately 17.47%.

2. Which companies are prominent players in the STEM Education in K-12?

Key companies in the market include EduCo International, Activate Learning, Amplify Learning, Bedford, Freeman and Worth Publishing Group, Carolina Biological Supply, Cengage Learning, Discovery Education, Houghton Mifflin Harcourt, Kendall Hunt Publishing Company, Lab-Aids, McGraw Hill, OpenSciEd, PASCO Scientifc, Savvas Learning, School Specialty.

3. What are the main segments of the STEM Education in K-12?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "STEM Education in K-12," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the STEM Education in K-12 report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the STEM Education in K-12?

To stay informed about further developments, trends, and reports in the STEM Education in K-12, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence