Key Insights

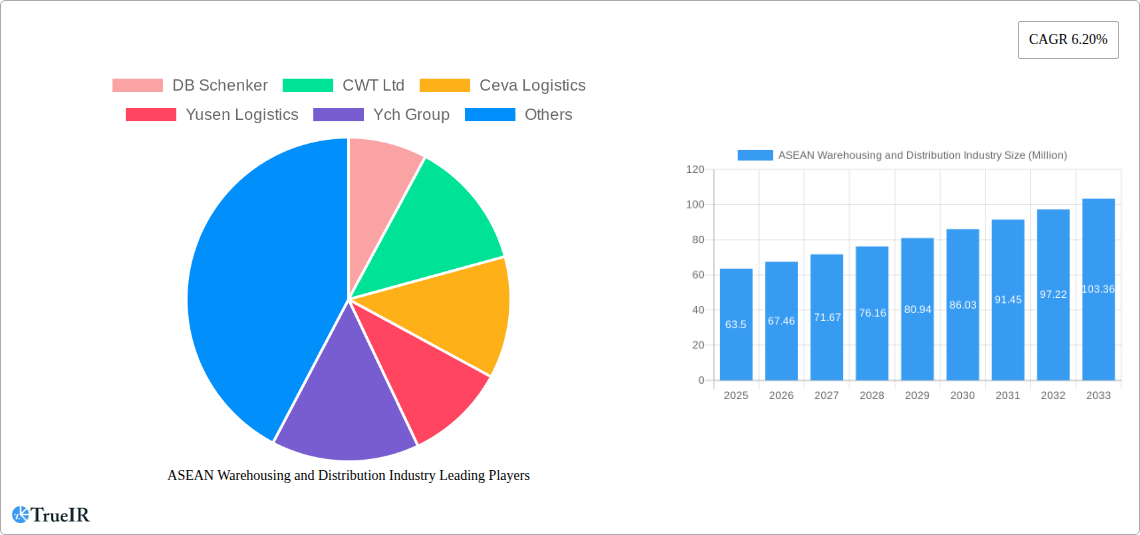

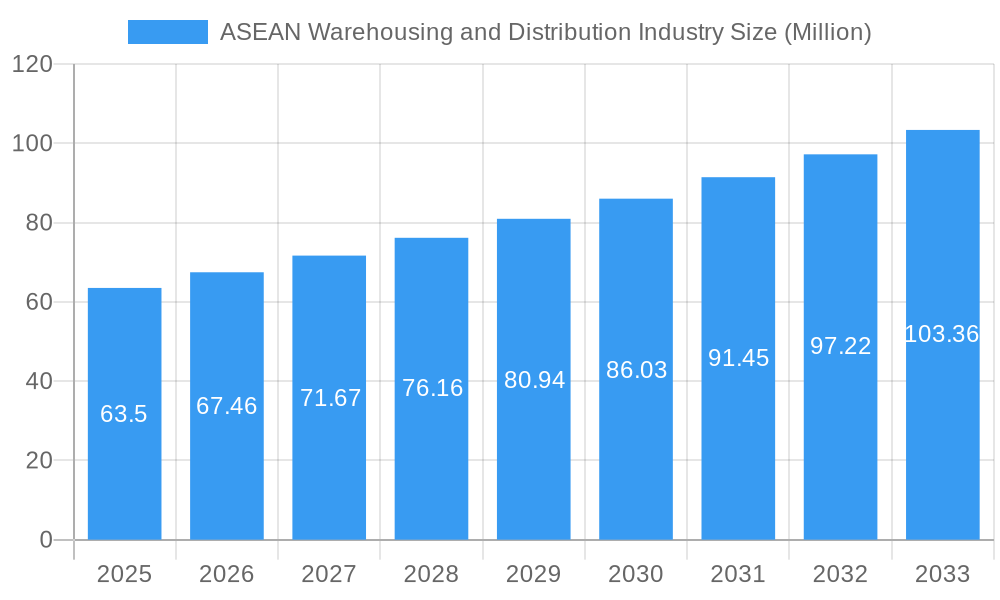

The ASEAN warehousing and distribution industry is experiencing robust growth, driven by the region's expanding e-commerce sector, burgeoning manufacturing activities, and increasing focus on supply chain optimization. The market, currently estimated at $63.50 million in 2025, is projected to maintain a Compound Annual Growth Rate (CAGR) of 6.20% from 2025 to 2033. This growth is fueled by several key factors. The rise of e-commerce necessitates efficient warehousing and distribution networks to handle the surge in online orders, leading to increased demand for warehousing services, particularly value-added services like packaging and labeling. Simultaneously, the automotive, pharmaceutical & healthcare, FMCG, and manufacturing sectors are driving demand for specialized warehousing solutions tailored to their specific needs, including temperature-controlled storage and secure handling of sensitive goods. Furthermore, increasing foreign direct investment (FDI) in the region is further bolstering the industry's expansion. Despite these positive trends, challenges remain. These include infrastructure limitations in certain areas, increasing labor costs, and the need for continuous technological upgrades to enhance efficiency and transparency across the supply chain. The industry is segmented by service type (warehousing, distribution, value-added) and end-user industry (retail & e-commerce, automotive, pharmaceutical & healthcare, FMCG, manufacturing, electronics). Key players include DB Schenker, CWT Ltd, Ceva Logistics, and others, competing on service quality, technology adoption, and geographical reach. The competitive landscape is dynamic, with both established players and emerging local companies vying for market share. The long-term outlook remains positive, with substantial opportunities for growth, particularly within the value-added services segment and expansion into underserved markets.

ASEAN Warehousing and Distribution Industry Market Size (In Million)

The continued growth in ASEAN's warehousing and distribution market relies on addressing existing infrastructure gaps and fostering technological advancements. This includes investing in modern warehousing facilities equipped with automation technologies to improve efficiency and reduce operational costs. Strategic partnerships and collaborations between logistics providers and technology companies can accelerate the digital transformation of the industry. Adopting sustainable practices, such as optimizing transportation routes and utilizing eco-friendly vehicles, will also become increasingly crucial for attracting environmentally conscious businesses. The regulatory environment will play a significant role; supportive policies that encourage investment and streamline logistical processes will be vital in sustaining the industry's growth trajectory. Focusing on skilled workforce development and talent acquisition will also be essential to meet the industry's evolving needs for skilled professionals in areas such as logistics management, technology, and data analytics.

ASEAN Warehousing and Distribution Industry Company Market Share

This dynamic report provides a comprehensive analysis of the ASEAN warehousing and distribution industry, offering invaluable insights for businesses, investors, and policymakers. With a detailed examination of market trends, competitive landscapes, and future projections, this report is an essential resource for navigating this rapidly evolving sector. The study period covers 2019-2033, with a base and estimated year of 2025.

ASEAN Warehousing and Distribution Industry Market Structure & Competitive Landscape

The ASEAN warehousing and distribution industry is characterized by a dynamic and increasingly consolidated market structure. A significant number of prominent multinational logistics providers and established regional players are actively shaping this landscape. Key industry participants include global giants such as DB Schenker, Ceva Logistics, Kuehne + Nagel, and DHL Supply Chain, alongside strong regional contenders like CWT Ltd, Yusen Logistics, YCH Group, Gemadept, WHA Corporation, Singapore Post, Agility, Kerry Logistics, CJ Century Logistics, Tiong Nam Logistics, and Keppel Logistics. The market is witnessing a notable trend towards consolidation, underscored by strategic mergers and acquisitions (M&A). While specific concentration ratios (e.g., CR4) fluctuate and depend on granular market segmentation, the overall landscape indicates a moderately to highly competitive environment, especially in key economic hubs.

Innovation is a critical differentiator, with significant investments being channeled into advanced technologies. Automation, Artificial Intelligence (AI), and the Internet of Things (IoT) are revolutionizing operational efficiency, enhancing accuracy, and driving down costs across warehousing and distribution operations. Regulatory frameworks, encompassing customs procedures, trade policies, and cross-border logistics agreements, play a crucial role in influencing operational expenditures and market accessibility. The emergence of alternative logistics models, such as decentralized warehousing and sophisticated direct-to-consumer (DTC) fulfillment strategies, presents both challenges and opportunities for traditional players, pushing them to adapt and innovate.

The industry exhibits substantial segmentation by both service type – including core warehousing, intricate distribution networks, and a growing array of value-added services (VAS) – and by end-user industry. The Retail & E-commerce sector continues to be a dominant force, followed closely by crucial sectors like Automotive, Pharmaceutical & Healthcare, Fast-Moving Consumer Goods (FMCG), Manufacturing, and Electronics. Recent M&A activities, such as Maersk's acquisition of LF Logistics and Geodis' acquisition of Keppel Logistics, highlight a strategic move towards the creation of larger, more integrated logistics powerhouses. These strategic consolidations are significantly expanding the warehouse footprint of major players across the region. The total value of M&A transactions in the ASEAN warehousing and distribution sector from 2019 to 2024 is estimated at approximately [Insert Estimated Value Here, e.g., 'a substantial amount, estimated to be in the hundreds of millions of USD'] Million, reflecting the ongoing industry transformation.

ASEAN Warehousing and Distribution Industry Market Trends & Opportunities

The ASEAN warehousing and distribution market is poised for significant and sustained growth, propelled by a confluence of robust economic factors. The region's burgeoning e-commerce sector, a continuously expanding manufacturing base, and ongoing improvements in logistical infrastructure are all key contributors to this expansion. The market size was estimated at approximately [Insert 2024 Market Size Here, e.g., 'USD XX Billion'] Million in 2024 and is forecasted to achieve a Compound Annual Growth Rate (CAGR) of [Insert CAGR Here, e.g., 'around X.X%'] from 2025 to 2033, projecting a market value of [Insert 2033 Market Size Here, e.g., 'USD YY Billion'] Million by the end of the forecast period. This impressive growth trajectory is further fueled by rapid technological advancements. Innovations in automation, the strategic application of big data analytics for demand forecasting and route optimization, and the adoption of cloud computing are collectively enhancing operational efficiency and providing unprecedented levels of visibility across complex supply chains.

Evolving consumer behavior, particularly the escalating demand for faster, more reliable, and convenient delivery services, is profoundly influencing industry dynamics. The widespread adoption of omnichannel retail strategies is creating fertile ground for the expansion of value-added services. This includes specialized last-mile delivery solutions, sophisticated inventory management, and highly customized fulfillment operations tailored to meet diverse customer needs. The competitive landscape is characterized by intense rivalry among established global and regional players, as well as the strategic entry of new, innovative companies. This dynamic environment is a powerful catalyst for ongoing innovation and the implementation of highly optimized pricing strategies.

Market penetration rates for various services and segments exhibit considerable variation, largely dictated by the maturity of infrastructure development and regional consumer spending power. For instance, the adoption of automated warehousing solutions, currently standing at approximately [Insert Current Automation Penetration Here, e.g., 'XX%'], is projected to reach [Insert Future Automation Penetration Here, e.g., 'YY%'] by 2033, signaling a significant shift towards more technologically advanced operations. The continuous development and integration of smart logistics networks across the ASEAN region present a substantial and ongoing opportunity for innovation, efficiency gains, and overall market expansion.

Dominant Markets & Segments in ASEAN Warehousing and Distribution Industry

-

Leading Regions/Countries: Singapore, Thailand, and Malaysia currently stand out as the dominant markets within the ASEAN warehousing and distribution sector. This leadership is attributed to their well-developed infrastructure, strong economic foundations, and highly strategic geographic positions that facilitate regional trade and connectivity. Emerging markets like Indonesia and Vietnam are demonstrating significant growth potential, largely driven by their expanding manufacturing capabilities and rapidly growing e-commerce penetration.

-

Dominant Segments:

-

By Service Type: Warehousing services represent the largest segment of the market, providing essential storage and inventory management solutions. This is closely followed by distribution services, which encompass the transportation and movement of goods. Value-added services (VAS) are experiencing particularly robust growth, propelled by increasing demand for customized logistics solutions that go beyond basic storage and transportation, such as kitting, assembly, and reverse logistics.

-

By End-User Industry: The Retail & E-commerce sector is the most dynamic and fastest-growing segment, a direct consequence of the exponential rise in online shopping across the ASEAN region. Other significant contributors to the market's overall value include the Manufacturing sector, the Fast-Moving Consumer Goods (FMCG) industry, and the critical Pharmaceutical & Healthcare sector, all of which rely heavily on efficient and reliable warehousing and distribution networks.

-

Key Growth Drivers:

- Improved Infrastructure: Substantial investments in multimodal transportation networks, including world-class ports, efficient airports, and extensive highway systems, are fundamentally enhancing logistics efficiency and reducing transit times across the region.

- Government Policies: Proactive and supportive government initiatives aimed at promoting industrial development, fostering trade liberalization, and simplifying cross-border trade procedures are providing a significant impetus for market growth.

- Technological Advancements: The widespread adoption of automation, digitalization, and advanced analytics is a critical factor in improving operational efficiency, optimizing resource utilization, and driving down overall logistics costs.

ASEAN Warehousing and Distribution Industry Product Analysis

The ASEAN warehousing and distribution industry is witnessing a surge in product innovation, driven by the need for enhanced efficiency, visibility, and security. Technological advancements such as automation (robotics, automated guided vehicles), warehouse management systems (WMS), and transportation management systems (TMS) are significantly improving operational efficiency and supply chain visibility. The adoption of cloud-based solutions and data analytics is improving decision-making and resource optimization. These innovations are crucial in addressing the growing demands for faster delivery times, increased order volumes, and customized fulfillment options within the increasingly complex and competitive environment of the ASEAN region. The key competitive advantage lies in providing integrated, technology-driven solutions that offer greater speed, reliability, and visibility across the entire supply chain.

Key Drivers, Barriers & Challenges in ASEAN Warehousing and Distribution Industry

Key Drivers:

- E-commerce Boom: The unprecedented and rapid expansion of e-commerce activities across ASEAN countries is a primary driver, creating substantial demand for modern warehousing facilities and sophisticated distribution networks to meet online order fulfillment needs.

- Foreign Direct Investment (FDI): Significant inflows of FDI into the manufacturing and logistics sectors are bolstering market expansion, leading to increased demand for warehousing space, advanced logistics infrastructure, and specialized services.

- Infrastructure Development: Continuous and strategic investments in transportation and logistics infrastructure, encompassing ports, roads, and digital connectivity, are crucial for enhancing operational efficiency and facilitating seamless movement of goods.

Key Challenges:

- Infrastructure Gaps: Despite ongoing improvements, significant disparities in infrastructure development across various sub-regions and countries within ASEAN can still hinder the efficiency and cost-effectiveness of logistics operations.

- Regulatory Complexity: The existence of varied, sometimes inconsistent, and often complex regulatory frameworks across different ASEAN member states can pose significant challenges for companies operating on a regional scale, impacting customs procedures, licensing, and compliance.

- Intense Competition: The market is characterized by fierce competition among a large number of established global players, regional specialists, and emerging local logistics providers. This intense competition, particularly in major hubs like Singapore and Bangkok, can exert downward pressure on pricing and profit margins, requiring continuous innovation and strategic differentiation.

Growth Drivers in the ASEAN Warehousing and Distribution Industry Market

The ASEAN warehousing and distribution market is propelled by a combination of factors. The expansion of e-commerce significantly increases demand for efficient warehousing and last-mile delivery solutions. Rising foreign direct investment (FDI) in manufacturing and logistics supports the expansion of warehousing capacity. Furthermore, government initiatives to improve infrastructure and streamline logistics processes, like developing specialized economic zones, enhance the industry's attractiveness for businesses. The growing adoption of technology, such as automated systems and data analytics, enhances operational efficiency and optimizes supply chains, further fueling growth.

Challenges Impacting ASEAN Warehousing and Distribution Industry Growth

Several challenges hinder the growth of the ASEAN warehousing and distribution sector. Infrastructure limitations in certain areas, such as limited road networks and inadequate port facilities, lead to logistical bottlenecks and increased costs. Inconsistent regulatory frameworks across the region create complexities and uncertainty for businesses. Competition among both established and new players remains fierce, resulting in pressure on margins and pricing. Finally, the lack of skilled labor in some parts of the region is a concern for maintaining efficient operations and expanding capabilities.

Key Players Shaping the ASEAN Warehousing and Distribution Industry Market

- DB Schenker

- CWT Ltd

- Ceva Logistics

- Yusen Logistics

- YCH Group

- Gemadept

- WHA Corporation

- Kuehne + Nagel

- Singapore Post

- Agility

- Kerry Logistics

- CJ Century Logistics

- Tiong Nam Logistics

- Keppel Logistics

- DHL Supply Chain

Significant ASEAN Warehousing and Distribution Industry Industry Milestones

August 2022: A.P. Moller - Maersk (Maersk) acquired LF Logistics, adding 223 warehouses and 9.5 million square meters of warehouse space to its network, significantly expanding its presence in ASEAN omnichannel fulfillment and e-commerce. This acquisition significantly altered the competitive landscape and increased Maersk’s market share.

April 2022: Geodis acquired Keppel Logistics, bolstering its contract logistics capabilities and e-commerce fulfillment services in Singapore and Southeast Asia, adding over 200,000 square meters of warehouse space. This acquisition strengthened Geodis' position in the region and enhanced its portfolio of services.

Future Outlook for ASEAN Warehousing and Distribution Industry Market

The ASEAN warehousing and distribution market is poised for continued strong growth, driven by ongoing e-commerce expansion, increasing manufacturing activity, and supportive government policies. Strategic opportunities lie in investing in advanced technologies, such as automation and AI, to enhance efficiency and create competitive advantages. The focus on sustainable and environmentally friendly logistics solutions will also play a key role in the sector’s future. The market's potential is significant, presenting opportunities for both established players and new entrants to capitalize on the region's dynamic economic growth and evolving consumer demands.

ASEAN Warehousing and Distribution Industry Segmentation

-

1. Geography

- 1.1. Singapore

- 1.2. Thailand

- 1.3. Malaysia

- 1.4. Vietnam

- 1.5. Indonesia

- 1.6. Philippines

- 1.7. Rest of ASEAN

ASEAN Warehousing and Distribution Industry Segmentation By Geography

- 1. Singapore

- 2. Thailand

- 3. Malaysia

- 4. Vietnam

- 5. Indonesia

- 6. Philippines

- 7. Rest of ASEAN

ASEAN Warehousing and Distribution Industry Regional Market Share

Geographic Coverage of ASEAN Warehousing and Distribution Industry

ASEAN Warehousing and Distribution Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 5.1.1. Singapore

- 5.1.2. Thailand

- 5.1.3. Malaysia

- 5.1.4. Vietnam

- 5.1.5. Indonesia

- 5.1.6. Philippines

- 5.1.7. Rest of ASEAN

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Singapore

- 5.2.2. Thailand

- 5.2.3. Malaysia

- 5.2.4. Vietnam

- 5.2.5. Indonesia

- 5.2.6. Philippines

- 5.2.7. Rest of ASEAN

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 6. Global ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 6.1.1. Singapore

- 6.1.2. Thailand

- 6.1.3. Malaysia

- 6.1.4. Vietnam

- 6.1.5. Indonesia

- 6.1.6. Philippines

- 6.1.7. Rest of ASEAN

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 7. Singapore ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 7.1.1. Singapore

- 7.1.2. Thailand

- 7.1.3. Malaysia

- 7.1.4. Vietnam

- 7.1.5. Indonesia

- 7.1.6. Philippines

- 7.1.7. Rest of ASEAN

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 8. Thailand ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 8.1.1. Singapore

- 8.1.2. Thailand

- 8.1.3. Malaysia

- 8.1.4. Vietnam

- 8.1.5. Indonesia

- 8.1.6. Philippines

- 8.1.7. Rest of ASEAN

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 9. Malaysia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 9.1.1. Singapore

- 9.1.2. Thailand

- 9.1.3. Malaysia

- 9.1.4. Vietnam

- 9.1.5. Indonesia

- 9.1.6. Philippines

- 9.1.7. Rest of ASEAN

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 10. Vietnam ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 10.1.1. Singapore

- 10.1.2. Thailand

- 10.1.3. Malaysia

- 10.1.4. Vietnam

- 10.1.5. Indonesia

- 10.1.6. Philippines

- 10.1.7. Rest of ASEAN

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 11. Indonesia ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 11.1.1. Singapore

- 11.1.2. Thailand

- 11.1.3. Malaysia

- 11.1.4. Vietnam

- 11.1.5. Indonesia

- 11.1.6. Philippines

- 11.1.7. Rest of ASEAN

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 12. Philippines ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 12.1.1. Singapore

- 12.1.2. Thailand

- 12.1.3. Malaysia

- 12.1.4. Vietnam

- 12.1.5. Indonesia

- 12.1.6. Philippines

- 12.1.7. Rest of ASEAN

- 12.1. Market Analysis, Insights and Forecast - by Geography

- 13. Rest of ASEAN ASEAN Warehousing and Distribution Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 13.1.1. Singapore

- 13.1.2. Thailand

- 13.1.3. Malaysia

- 13.1.4. Vietnam

- 13.1.5. Indonesia

- 13.1.6. Philippines

- 13.1.7. Rest of ASEAN

- 13.1. Market Analysis, Insights and Forecast - by Geography

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 DB Schenker

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 CWT Ltd

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Ceva Logistics

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Yusen Logistics

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Ych Group

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Gemadept

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 WHA Corporation

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Kuehne + Nagel

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Singapore Post

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Agility

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Kerry Logistics

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 CJ Century Logistics

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Tiong Nam Logistics

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.15 DHL Supply Chain

- 14.1.15.1. Company Overview

- 14.1.15.2. Products

- 14.1.15.3. Company Financials

- 14.1.15.4. SWOT Analysis

- 14.1.1 DB Schenker

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Global ASEAN Warehousing and Distribution Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 3: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 4: Singapore ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: Singapore ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 7: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: Thailand ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Thailand ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 11: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 12: Malaysia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Malaysia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 15: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: Vietnam ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Vietnam ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 19: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 20: Indonesia ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Indonesia ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 23: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Philippines ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Philippines ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Geography 2025 & 2033

- Figure 27: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 28: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue (Million), by Country 2025 & 2033

- Figure 29: Rest of ASEAN ASEAN Warehousing and Distribution Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 2: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Global ASEAN Warehousing and Distribution Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the ASEAN Warehousing and Distribution Industry?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the ASEAN Warehousing and Distribution Industry?

Key companies in the market include DB Schenker, CWT Ltd, Ceva Logistics, Yusen Logistics, Ych Group, Gemadept, WHA Corporation, Kuehne + Nagel, Singapore Post, Agility, Kerry Logistics, CJ Century Logistics, Tiong Nam Logistics, Keppel Logistics**List Not Exhaustive 6 3 Other Companies (Key Information/Overview, DHL Supply Chain.

3. What are the main segments of the ASEAN Warehousing and Distribution Industry?

The market segments include Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.50 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in the demand for the Air Cargo Capacity; The Rise of E-commerce.

6. What are the notable trends driving market growth?

Increase in Warehousing Space in Thailand.

7. Are there any restraints impacting market growth?

Cargo Restrictions.

8. Can you provide examples of recent developments in the market?

August 2022: A.P. Moller - Maersk (Maersk) announced the successful completion of its acquisition of LF Logistics, a logistics firm with premium capabilities in omnichannel fulfillment services, e-commerce, and inland shipping in the ASEAN region. Following the acquisition, Maersk will expand its warehouse network by adding 223 warehouses to its current network and increasing the total number of facilities, spread across 9.5 million square meters, to 549.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "ASEAN Warehousing and Distribution Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the ASEAN Warehousing and Distribution Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the ASEAN Warehousing and Distribution Industry?

To stay informed about further developments, trends, and reports in the ASEAN Warehousing and Distribution Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence