Key Insights

The Polish Third-Party Logistics (3PL) market, projected to reach $35.71 billion by 2025, is poised for significant expansion. The industry is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.63% from 2025 to 2033. This robust growth is propelled by several key drivers. The rapidly expanding e-commerce sector in Poland significantly boosts demand for efficient warehousing and distribution solutions, particularly within wholesale, retail, and online trade. Concurrently, advancements in manufacturing and the automotive industry necessitate advanced domestic and international logistics management. Favorable government initiatives supporting infrastructure development and Poland's strategic EU location further enhance the logistics ecosystem. Despite potential challenges such as fuel price volatility and driver shortages, the market outlook remains strong.

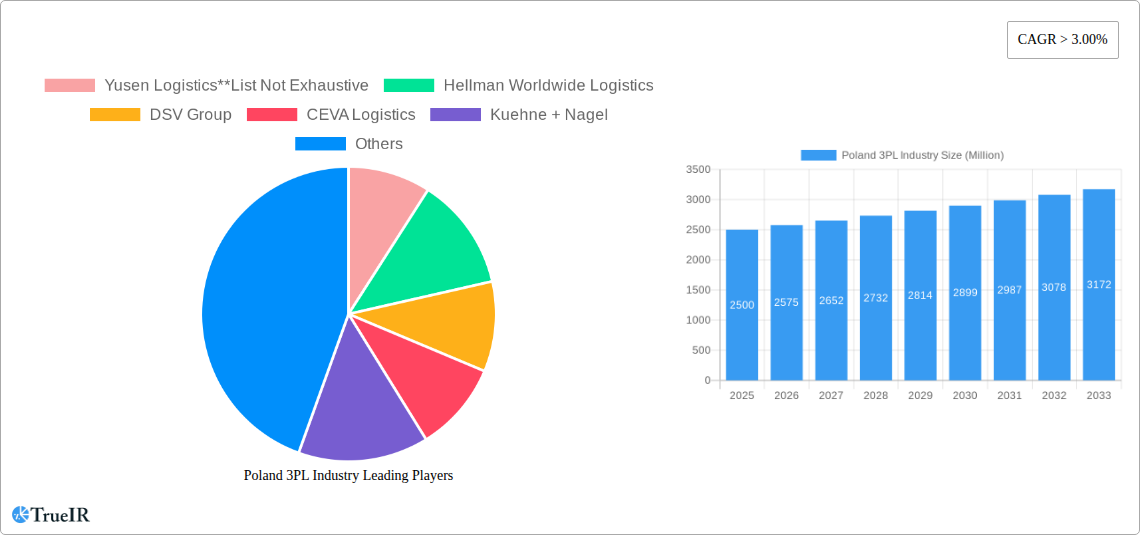

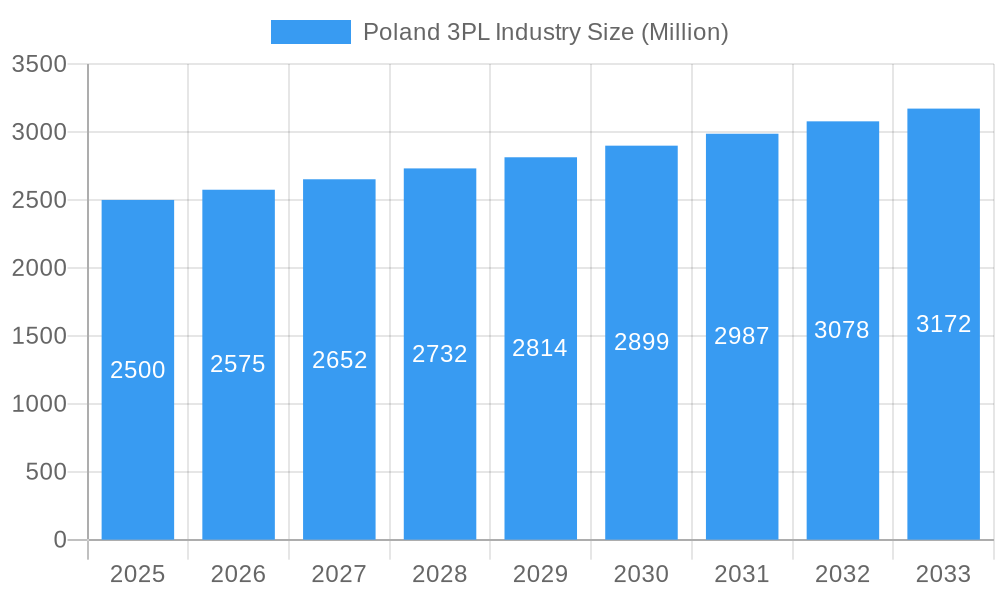

Poland 3PL Industry Market Size (In Billion)

The Polish 3PL market is characterized by a dynamic competitive landscape, featuring global leaders like Yusen Logistics, DHL Supply Chain, and Kuehne + Nagel. These companies offer a comprehensive suite of services including domestic and international transportation, alongside value-added warehousing. A key trend is the increasing adoption of advanced technologies like Warehouse Management Systems (WMS) and Transportation Management Systems (TMS). Investment in these technologies is crucial for enhancing operational efficiency, optimizing supply chains, and elevating customer service standards. Furthermore, there is a growing demand for specialized logistics solutions tailored to specific industries, such as pharmaceuticals and healthcare. This trend fosters the growth of niche segments within the Polish 3PL market, requiring bespoke logistics strategies and expertise.

Poland 3PL Industry Company Market Share

Poland 3PL Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Poland 3PL (Third-Party Logistics) industry, offering valuable insights for investors, industry professionals, and strategic planners. Covering the period from 2019 to 2033, with a focus on 2025, this report delivers a detailed examination of market size, key players, emerging trends, and future growth potential. The study incorporates extensive quantitative and qualitative data to provide a complete picture of this dynamic market.

Poland 3PL Industry Market Structure & Competitive Landscape

The Polish 3PL market exhibits a moderately concentrated structure, with several multinational giants and strong domestic players vying for market share. The market concentration ratio (CR4) is estimated at xx% in 2025, indicating a competitive landscape with opportunities for both established and emerging players. Innovation drivers include the adoption of advanced technologies like AI and automation in warehouse management and transportation optimization. Regulatory impacts, such as EU directives on transport and data privacy, significantly influence operational costs and compliance strategies. Product substitutes are limited, with the primary competition originating from in-house logistics operations of larger companies. Mergers and acquisitions (M&A) activity has been steadily increasing, with an estimated xx Million USD in M&A volume in 2024, driving consolidation and market expansion. End-user segmentation shows a strong reliance on the Manufacturing & Automotive sector, contributing to xx% of the market in 2025.

- Market Concentration: CR4 estimated at xx% in 2025.

- M&A Activity: Estimated xx Million USD in M&A volume in 2024.

- Key End-Users: Manufacturing & Automotive (xx% in 2025).

- Regulatory Influences: EU directives on transport and data privacy.

Poland 3PL Industry Market Trends & Opportunities

The Polish 3PL market is experiencing robust growth, driven by the expansion of e-commerce, increasing outsourcing trends, and the ongoing development of Poland's manufacturing and logistics infrastructure. The market size is projected to reach xx Million USD by 2025 and is expected to register a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological advancements, particularly in automation, data analytics, and the Internet of Things (IoT), are significantly shaping the industry landscape. Consumer preferences for faster and more reliable delivery services are creating new opportunities for 3PL providers specializing in last-mile delivery and e-fulfillment. Intense competition is driving innovation and efficiency improvements among 3PL companies. Market penetration rates are increasing across all segments, but especially in the growing e-commerce sector.

Dominant Markets & Segments in Poland 3PL Industry

The Distributive Trade (Wholesale and Retail trade including e-commerce) segment continues to be the powerhouse of the Polish 3PL market, projected to account for a substantial XX% of the total market revenue by 2025. This dominance is closely followed by the robust Manufacturing & Automotive sector. The sustained growth in these key segments is primarily propelled by:

- Distributive Trade: Fueled by the explosive growth of e-commerce and an escalating demand for agile and cost-effective last-mile delivery solutions to meet evolving consumer expectations.

- Manufacturing & Automotive: Driven by the ongoing expansion of manufacturing facilities across various industries and the critical need for optimized, end-to-end supply chain management to ensure operational efficiency and timely product delivery.

- Pharma & Healthcare: Characterized by the stringent regulatory compliance requirements and a specialized demand for temperature-controlled, secure, and traceable logistics solutions to maintain product integrity and patient safety.

- Consumer Goods: Experiencing steady growth due to rising consumer spending and the increasing complexity of multi-channel distribution strategies.

In terms of services, Value-added Warehousing and Distribution remains the leading segment. This is largely attributed to the growing requirement for sophisticated warehousing capabilities, including advanced inventory management, efficient order fulfillment, kitting, and product customization. Furthermore, International Transportation Management is witnessing significant acceleration, underscoring Poland's strategic geographical position as a pivotal hub within Europe and its increasingly vital role in facilitating global trade flows.

Poland 3PL Industry Product Analysis

The Polish 3PL industry is currently at the forefront of significant product innovation, with technological advancements acting as a primary catalyst. The seamless integration of Artificial Intelligence (AI) and Machine Learning (ML) into Warehouse Management Systems (WMS) is revolutionizing operational efficiency, accuracy, and predictive capabilities. The widespread adoption of real-time tracking and advanced monitoring technologies is dramatically enhancing supply chain visibility, enabling proactive problem-solving and significantly improving delivery timeframes and reliability. These sophisticated technological integrations are not merely incremental improvements; they are providing substantial competitive advantages to 3PL providers that strategically invest in and implement these cutting-edge solutions. This investment is directly translating into increased market share, enhanced customer satisfaction, and improved profitability.

Key Drivers, Barriers & Challenges in Poland 3PL Industry

Key Drivers: Poland's strategic location within the European Union, its growing manufacturing sector, and the expansion of e-commerce are driving strong demand for 3PL services. Government initiatives promoting logistics infrastructure development and attracting foreign investment also contribute to market growth. Technological advancements, particularly automation and digitalization, are increasing efficiency and reducing costs.

Challenges: The Polish 3PL industry faces challenges such as driver shortages, rising fuel costs, and increasing regulatory complexity. Competition from established and emerging players puts pressure on profit margins. Supply chain disruptions caused by geopolitical events and global economic uncertainty pose significant risks to operational continuity. These factors can impact efficiency, increase costs and potentially hinder overall market growth.

Growth Drivers in the Poland 3PL Industry Market

The sustained growth trajectory of the Poland 3PL industry is underpinned by a confluence of potent factors. The unrelenting expansion of the e-commerce sector, coupled with the continued growth and diversification of manufacturing operations, forms a strong foundation. Crucially, supportive government initiatives focused on enhancing logistics infrastructure, including modernizing road networks and expanding intermodal transport capabilities, are significantly boosting the sector's potential. Furthermore, rapid technological advancements in areas such as warehouse automation, robotics, and sophisticated transportation management systems are not only improving efficiency but also expanding the service offerings of 3PL providers. Poland's prime geographical location within the European Union acts as a significant enabler, facilitating seamless cross-border trade and thereby escalating the demand for comprehensive 3PL services across international supply chains.

Challenges Impacting Poland 3PL Industry Growth

Despite the positive outlook, the Poland 3PL industry faces several persistent challenges that require strategic navigation. A significant concern remains the ongoing shortage of skilled drivers, which can lead to service delays and increased operational costs. The volatility of fuel prices continues to exert pressure on transportation budgets, necessitating greater efficiency and alternative fuel exploration. Escalating regulatory complexities, particularly concerning cross-border logistics and labor laws, add layers of operational intricacy. Furthermore, ongoing global supply chain disruptions, amplified by geopolitical uncertainties, introduce inherent instability and operational risks that demand robust contingency planning. The intensely competitive landscape mandates continuous investment in both advanced technology and operational streamlining to not only maintain but also improve profitability margins and service levels.

Key Players Shaping the Poland 3PL Industry Market

- Yusen Logistics

- Hellman Worldwide Logistics

- DSV Group

- CEVA Logistics

- Kuehne + Nagel

- Kerry Logistics

- Ekol - Logistics 4.0

- Erontrans Logistics Services

- Raben

- Geis Global Logistics

- Geodis

- Dartom

- DHL Supply Chain

- Feige Logistics

- ID Logistics

Significant Poland 3PL Industry Milestones

- 2020: Increased investment in automated warehousing solutions by several key players.

- 2021: Implementation of new regulations regarding data privacy and security in the logistics sector.

- 2022: Significant M&A activity amongst smaller 3PL providers.

- 2023: Growth in the adoption of sustainable logistics practices among leading 3PL providers.

Future Outlook for Poland 3PL Industry Market

The Poland 3PL market is robustly positioned for continued and accelerated growth. The relentless expansion of e-commerce, coupled with sustained investment in state-of-the-art logistics infrastructure and the proactive adoption of transformative technological advancements, are key pillars supporting this positive trajectory. Significant strategic opportunities abound for 3PL providers who strategically focus on niche areas such as advanced e-fulfillment solutions, optimized last-mile delivery networks, and the provision of highly specialized value-added services tailored to evolving client needs. The market's inherent potential remains substantial, with projections indicating further expansion across virtually all segments, most notably within the dynamic e-commerce and burgeoning manufacturing sectors. The ongoing development of Poland’s comprehensive logistics infrastructure, alongside its commitment to embracing cutting-edge technologies, will be absolutely pivotal in dictating the pace and direction of future growth and solidifying its position as a leading logistics hub in Europe.

Poland 3PL Industry Segmentation

-

1. Services

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End-User

- 2.1. Manufacturing & Automotive

- 2.2. Oil & Gas and Chemicals

- 2.3. Distribu

- 2.4. Pharma & Healthcare

- 2.5. Construction

- 2.6. Other End Users

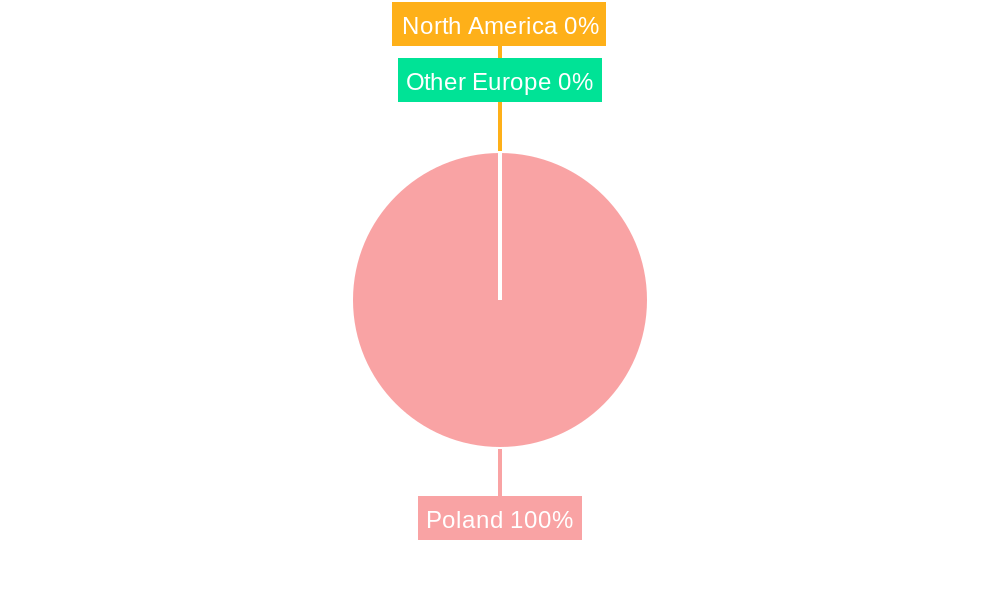

Poland 3PL Industry Segmentation By Geography

- 1. Poland

Poland 3PL Industry Regional Market Share

Geographic Coverage of Poland 3PL Industry

Poland 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Manufacturing & Automotive

- 5.2.2. Oil & Gas and Chemicals

- 5.2.3. Distribu

- 5.2.4. Pharma & Healthcare

- 5.2.5. Construction

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Poland 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Manufacturing & Automotive

- 6.2.2. Oil & Gas and Chemicals

- 6.2.3. Distribu

- 6.2.4. Pharma & Healthcare

- 6.2.5. Construction

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Yusen Logistics**List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hellman Worldwide Logistics

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DSV Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CEVA Logistics

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kuehne + Nagel

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Kerry Logistics

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ekol - Logistics 4 0

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Erontrans Logistics Services

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Raben

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Geis Global Logistics

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Geodis

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Dartom

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 DHL Supply Chain

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Feige Logistics

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 ID Logistics

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Yusen Logistics**List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland 3PL Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: Poland 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 2: Poland 3PL Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: Poland 3PL Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 5: Poland 3PL Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 6: Poland 3PL Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland 3PL Industry?

The projected CAGR is approximately 5.63%.

2. Which companies are prominent players in the Poland 3PL Industry?

Key companies in the market include Yusen Logistics**List Not Exhaustive, Hellman Worldwide Logistics, DSV Group, CEVA Logistics, Kuehne + Nagel, Kerry Logistics, Ekol - Logistics 4 0, Erontrans Logistics Services, Raben, Geis Global Logistics, Geodis, Dartom, DHL Supply Chain, Feige Logistics, ID Logistics.

3. What are the main segments of the Poland 3PL Industry?

The market segments include Services, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.71 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Number of Partnerships among Automobile Manufacturers and Logistics Partners; Growth in international trade.

6. What are the notable trends driving market growth?

Boom in the Warehousing Sector.

7. Are there any restraints impacting market growth?

Nature of Supply Chain Business.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland 3PL Industry?

To stay informed about further developments, trends, and reports in the Poland 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence