Key Insights

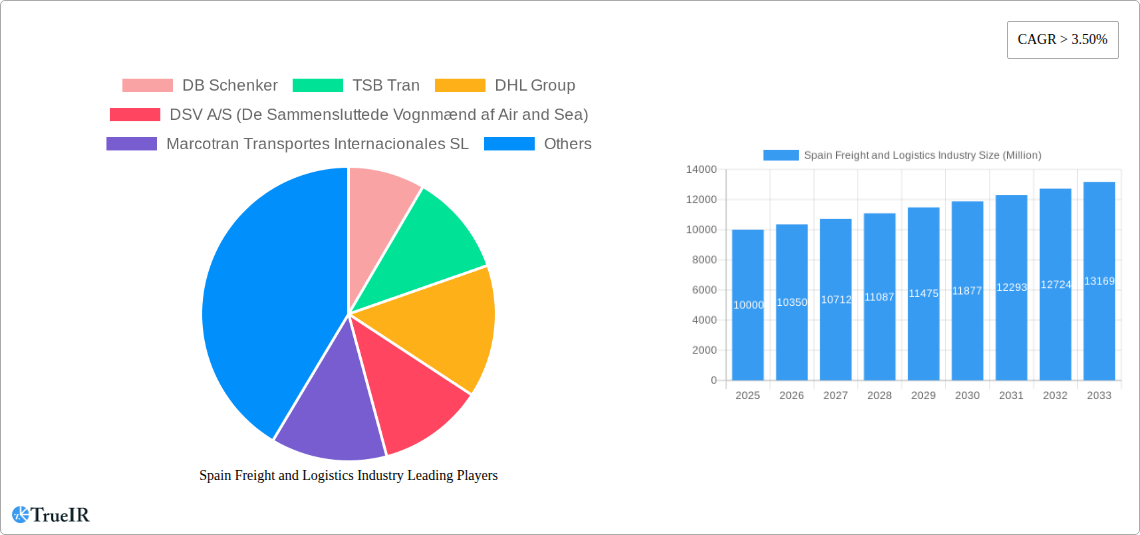

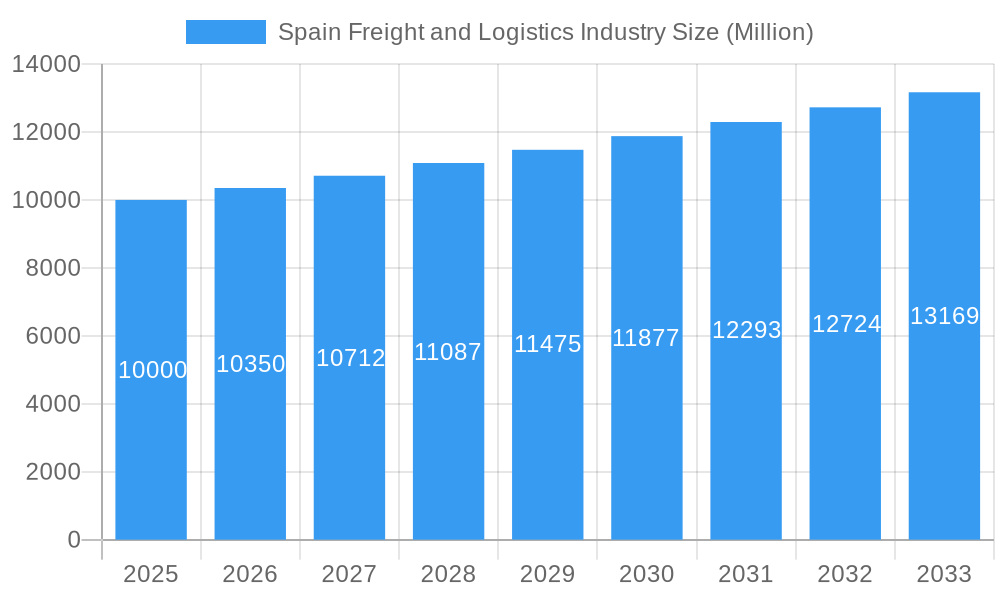

The Spanish freight and logistics market is poised for significant expansion, projected to achieve a Compound Annual Growth Rate (CAGR) of 6.3%. With a market size estimated at 17.96 billion in the base year of 2025, this sector's growth is driven by robust e-commerce adoption, Spain's strategic geographical position, and expanding end-user industries. Key growth accelerators include the burgeoning e-commerce sector, necessitating advanced Courier, Express, and Parcel (CEP) services. Spain's role as a vital trade link between Europe and North Africa, alongside increasing cross-border commerce, further fuels sector dynamism. Contributions from the construction, manufacturing, and agricultural sectors also bolster market expansion. Despite challenges like fuel price volatility and driver shortages, industry resilience, technological advancements, and the adoption of sophisticated logistics management systems and autonomous vehicles are mitigating these obstacles. The temperature-controlled logistics segment is anticipated to experience exceptional growth due to rising demand for the secure transport of perishable goods. The market is characterized by the strong presence of industry leaders such as DB Schenker, DHL, and Kuehne + Nagel, fostering an environment of continuous innovation, strategic alliances, competitive pricing, and service enhancement.

Spain Freight and Logistics Industry Market Size (In Billion)

Market segmentation highlights significant opportunities within the Spanish freight and logistics sector. The expanding e-commerce landscape directly influences the CEP segment, while heightened emphasis on food safety and quality in agriculture and food processing drives substantial growth in temperature-controlled logistics. The manufacturing and construction industries offer extensive potential for specialized logistics services and customized solutions. Spain's advantageous location and increasing international trade present considerable opportunities for growth through infrastructure investment and the adoption of innovative technologies. Companies are increasingly prioritizing sustainable practices, integrating eco-friendly solutions to address environmental concerns. Market consolidation, including mergers and acquisitions, is also expected to redefine the competitive landscape in the coming years.

Spain Freight and Logistics Industry Company Market Share

Spain Freight & Logistics Industry: A Comprehensive Market Report (2019-2033)

This dynamic report provides an in-depth analysis of the Spain freight and logistics industry, offering invaluable insights for investors, businesses, and industry professionals. Leveraging extensive data from 2019-2024 (historical period), with a base year of 2025 and forecast extending to 2033, this report unveils the market's structure, competitive landscape, key trends, and future potential. The report covers a market valued at €xx Million in 2024 and projects a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching €xx Million by 2033.

Spain Freight and Logistics Industry Market Structure & Competitive Landscape

The Spanish freight and logistics market exhibits a moderately concentrated structure, with a Herfindahl-Hirschman Index (HHI) estimated at xx in 2024. Key players like DHL Group, FedEx, and Kuehne + Nagel hold significant market share, yet numerous smaller, specialized firms cater to niche segments. Innovation is driven by technological advancements in areas such as automation, data analytics, and sustainable solutions. Stringent EU regulations regarding environmental sustainability and digitalization are shaping industry practices. Product substitutes, primarily within specific logistics functions, pose a moderate competitive threat. Consolidation through mergers and acquisitions (M&A) is a recurring trend, with a total M&A volume estimated at €xx Million in the historical period.

- Market Concentration: Moderately concentrated, with a few major players and many smaller, specialized firms.

- Innovation Drivers: Technological advancements in automation, data analytics, and sustainable logistics.

- Regulatory Impacts: Stringent EU regulations on sustainability and digitalization influencing operational strategies.

- Product Substitutes: Limited substitution, mainly within specific logistics functions (e.g., specialized courier services).

- End-User Segmentation: Significant market penetration across agriculture, construction, manufacturing, and retail sectors.

- M&A Trends: Consistent M&A activity, suggesting ongoing market consolidation.

Spain Freight and Logistics Industry Market Trends & Opportunities

The Spanish freight and logistics market is experiencing robust growth, driven by expanding e-commerce, increasing cross-border trade, and advancements in supply chain management technologies. The market size grew from €xx Million in 2019 to €xx Million in 2024, reflecting a CAGR of xx%. This positive trajectory is projected to continue, with opportunities arising from the increasing demand for efficient, sustainable, and technologically advanced logistics solutions. Technological shifts, such as the adoption of AI, blockchain, and IoT, are improving operational efficiency, transparency, and security. Consumer preferences are shifting toward faster delivery times and increased transparency in supply chains. Competitive dynamics are marked by increased consolidation, strategic alliances, and the emergence of innovative business models. Market penetration rates for key segments, such as temperature-controlled logistics and express delivery, are steadily increasing, creating new business opportunities.

Dominant Markets & Segments in Spain Freight and Logistics Industry

The Manufacturing sector is the dominant end-user industry in the Spanish freight and logistics market, followed closely by Wholesale and Retail Trade. The high volume of goods movement in these sectors drives demand for various logistics services. Within logistics functions, Courier, Express, and Parcel (CEP) services lead, benefiting from e-commerce expansion. Temperature-controlled logistics is also a rapidly growing segment, fueled by the need to transport perishable goods effectively.

- Key Growth Drivers for Manufacturing: Strong domestic manufacturing base, export-oriented businesses, and increased automation in supply chains.

- Key Growth Drivers for Wholesale & Retail Trade: E-commerce boom, expansion of omnichannel retail, and demand for efficient last-mile delivery solutions.

- Key Growth Drivers for CEP: E-commerce expansion, growing consumer preference for quick delivery, and technological advancements in delivery management.

- Key Growth Drivers for Temperature Controlled: Increased demand for the transport of perishable goods, particularly in the food and pharmaceutical industries, strict regulatory requirements.

Spain Freight and Logistics Industry Product Analysis

The Spanish freight and logistics market is characterized by a diverse range of services, from basic transportation to specialized solutions. Recent innovations include the application of AI and machine learning for route optimization and predictive maintenance, improved track-and-trace technologies for enhanced visibility and security, and sustainable transport solutions like electric vehicles and optimized routing to minimize environmental impact. These innovations reflect market trends toward greater efficiency, transparency, and environmental sustainability.

Key Drivers, Barriers & Challenges in Spain Freight and Logistics Industry

Key Drivers: E-commerce growth, increased international trade, technological advancements (AI, automation), government investments in infrastructure.

Challenges: Infrastructure limitations (especially in some regions), rising fuel costs, driver shortages, stringent environmental regulations (requiring significant capital expenditure for many companies), intense competition, and fluctuations in global economic conditions. These challenges represent a significant cost increase across the board, impacting profitability.

Growth Drivers in the Spain Freight and Logistics Industry Market

The Spanish freight and logistics industry is propelled by strong growth in e-commerce, requiring efficient last-mile delivery solutions. Technological innovations like AI and blockchain are increasing efficiency and transparency. Government initiatives focusing on infrastructure improvements and sustainable transportation further stimulate growth.

Challenges Impacting Spain Freight and Logistics Industry Growth

Major hurdles include aging infrastructure in certain regions, impacting delivery times and costs. Driver shortages cause capacity constraints and increased wages, affecting profitability. Stricter environmental regulations necessitate expensive upgrades to fleets, posing a financial strain. Intense competition requires continuous innovation to maintain a competitive edge.

Key Players Shaping the Spain Freight and Logistics Industry Market

- DB Schenker

- TSB Tran

- DHL Group

- DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- Marcotran Transportes Internacionales SL

- FedEx

- Kuehne + Nagel

- Alfil Logistics

- Across Logistics

- Grupo Carreras

- Rhenus Logistics

- Grupo Sese

- Salvesen Logistica S A

Significant Spain Freight and Logistics Industry Industry Milestones

- September 2023: Kuehne+Nagel and Capgemini partnered to create a supply chain orchestration service, leveraging AI and data analytics. This enhances end-to-end supply chain visibility and efficiency for large corporations.

- October 2023: Kuehne+Nagel launched three new charter connections between the Americas, Europe, and Asia, expanding its global reach and capacity in key sectors.

- January 2024: Kuehne + Nagel introduced its Book & Claim insetting solution for electric vehicles, furthering its commitment to sustainable logistics practices.

Future Outlook for Spain Freight and Logistics Industry Market

The Spanish freight and logistics market is poised for continued expansion. Growth catalysts include sustained e-commerce growth, increasing automation, and the ongoing adoption of sustainable practices. Strategic opportunities exist in niche areas such as temperature-controlled logistics and specialized transportation solutions. The market's future potential is substantial, driven by technological innovation and evolving consumer preferences. Further consolidation amongst industry players is highly likely.

Spain Freight and Logistics Industry Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Logistics Function

-

2.1. Courier, Express, and Parcel (CEP)

-

2.1.1. By Destination Type

- 2.1.1.1. Domestic

- 2.1.1.2. International

-

2.1.1. By Destination Type

-

2.2. Freight Forwarding

-

2.2.1. By Mode Of Transport

- 2.2.1.1. Air

- 2.2.1.2. Sea and Inland Waterways

- 2.2.1.3. Others

-

2.2.1. By Mode Of Transport

-

2.3. Freight Transport

- 2.3.1. Pipelines

- 2.3.2. Rail

- 2.3.3. Road

-

2.4. Warehousing and Storage

-

2.4.1. By Temperature Control

- 2.4.1.1. Non-Temperature Controlled

-

2.4.1. By Temperature Control

- 2.5. Other Services

-

2.1. Courier, Express, and Parcel (CEP)

Spain Freight and Logistics Industry Segmentation By Geography

- 1. Spain

Spain Freight and Logistics Industry Regional Market Share

Geographic Coverage of Spain Freight and Logistics Industry

Spain Freight and Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Logistics Function

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.2.1.1. By Destination Type

- 5.2.1.1.1. Domestic

- 5.2.1.1.2. International

- 5.2.1.1. By Destination Type

- 5.2.2. Freight Forwarding

- 5.2.2.1. By Mode Of Transport

- 5.2.2.1.1. Air

- 5.2.2.1.2. Sea and Inland Waterways

- 5.2.2.1.3. Others

- 5.2.2.1. By Mode Of Transport

- 5.2.3. Freight Transport

- 5.2.3.1. Pipelines

- 5.2.3.2. Rail

- 5.2.3.3. Road

- 5.2.4. Warehousing and Storage

- 5.2.4.1. By Temperature Control

- 5.2.4.1.1. Non-Temperature Controlled

- 5.2.4.1. By Temperature Control

- 5.2.5. Other Services

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Spain Freight and Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Agriculture, Fishing, and Forestry

- 6.1.2. Construction

- 6.1.3. Manufacturing

- 6.1.4. Oil and Gas, Mining and Quarrying

- 6.1.5. Wholesale and Retail Trade

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Logistics Function

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.2.1.1. By Destination Type

- 6.2.1.1.1. Domestic

- 6.2.1.1.2. International

- 6.2.1.1. By Destination Type

- 6.2.2. Freight Forwarding

- 6.2.2.1. By Mode Of Transport

- 6.2.2.1.1. Air

- 6.2.2.1.2. Sea and Inland Waterways

- 6.2.2.1.3. Others

- 6.2.2.1. By Mode Of Transport

- 6.2.3. Freight Transport

- 6.2.3.1. Pipelines

- 6.2.3.2. Rail

- 6.2.3.3. Road

- 6.2.4. Warehousing and Storage

- 6.2.4.1. By Temperature Control

- 6.2.4.1.1. Non-Temperature Controlled

- 6.2.4.1. By Temperature Control

- 6.2.5. Other Services

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 TSB Tran

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DHL Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Marcotran Transportes Internacionales SL

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 FedEx

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kuehne + Nagel

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Alfil Logistics

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Across Logistics

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Grupo Carreras

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Rhenus Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Grupo Sese

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Salvesen Logistica S A

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Freight and Logistics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Spain Freight and Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: Spain Freight and Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 2: Spain Freight and Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 3: Spain Freight and Logistics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Spain Freight and Logistics Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 5: Spain Freight and Logistics Industry Revenue billion Forecast, by Logistics Function 2020 & 2033

- Table 6: Spain Freight and Logistics Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Freight and Logistics Industry?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the Spain Freight and Logistics Industry?

Key companies in the market include DB Schenker, TSB Tran, DHL Group, DSV A/S (De Sammensluttede Vognmænd af Air and Sea), Marcotran Transportes Internacionales SL, FedEx, Kuehne + Nagel, Alfil Logistics, Across Logistics, Grupo Carreras, Rhenus Logistics, Grupo Sese, Salvesen Logistica S A.

3. What are the main segments of the Spain Freight and Logistics Industry?

The market segments include End User Industry, Logistics Function.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.96 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing volume of international trade4.; The rise of trade agreements between nations.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; Surge in fuel costs affecting the market4.; Increasing trade tension.

8. Can you provide examples of recent developments in the market?

January 2024: Kuehne + Nagel has announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles.October 2023: Kuehne+Nagel has introduced three new charter connections between the Americas, Europe, and Asia. It has begun its operations with its own freighter, the B747-8 “Inspire”, from October 23, 2023. It has conducted two additional weekly routings from Atlanta and Chicago to Amsterdam and from there to Taipei. This flight will serve key industries such as healthcare, perishables and semiconductors.September 2023: Kuehne+Nagel and Capgemini have entered into a strategic agreement to create a supply chain orchestration service offering to provide end-to-end services across the supply chain network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Freight and Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Freight and Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Freight and Logistics Industry?

To stay informed about further developments, trends, and reports in the Spain Freight and Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence