Key Insights

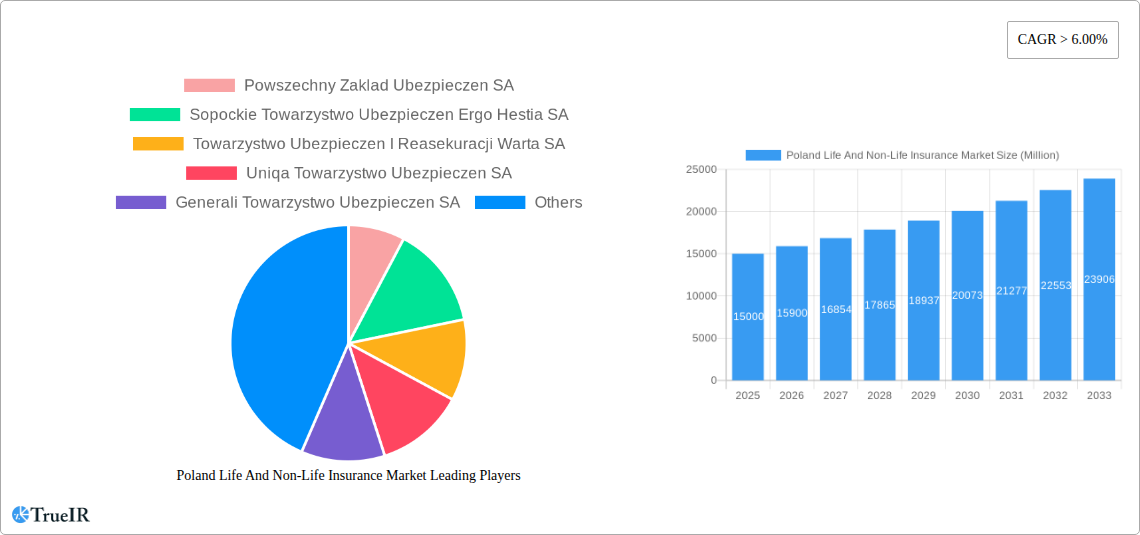

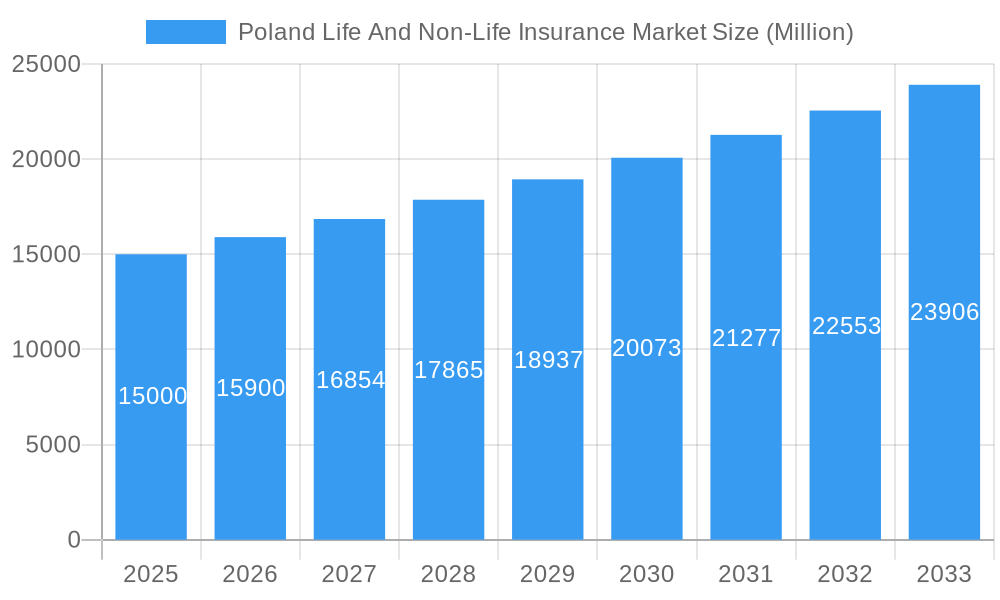

The Poland Life and Non-Life Insurance market is poised for substantial expansion, projected to achieve a Compound Annual Growth Rate (CAGR) of 7.19%. The market size is estimated at 23.51 billion in the base year of 2025, with continued growth anticipated through 2033. This growth trajectory is propelled by increasing disposable incomes, heightened risk awareness, and government-backed financial inclusion initiatives. A burgeoning middle class and the increasing adoption of digital distribution channels, coupled with innovative, customer-centric insurance solutions, are further stimulating market penetration and product diversification.

Poland Life And Non-Life Insurance Market Market Size (In Billion)

The market is comprehensively segmented by product type (Life and Non-Life), distribution channels (Online and Offline), and key geographical regions within Poland. Leading industry players, including Powszechny Zakład Ubezpieczen SA, Ergo Hestia SA, Warta SA, Uniqa, Generali, Compensa, Interrisk, Aviva, and Wiener, are actively shaping the competitive landscape and driving innovation.

Poland Life And Non-Life Insurance Market Company Market Share

While robust growth is evident, potential challenges such as economic volatility and evolving regulatory frameworks necessitate strategic adaptability. The dynamic competitive environment, marked by established incumbents and emerging players, underscores the importance of continuous innovation and strategic foresight for sustained market success. The long-term outlook remains highly positive, underpinned by favorable demographic trends and sustained economic expansion in Poland. The strategic integration of advanced technologies and the development of highly customized product offerings will be critical drivers of the market's future development.

Poland Life and Non-Life Insurance Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Poland life and non-life insurance market, offering invaluable insights for investors, insurers, and industry professionals. The report covers market structure, competitive dynamics, key trends, and future growth projections, incorporating data from 2019 to 2024 (historical period), with estimations for 2025 (base and estimated year), and forecasts extending to 2033 (forecast period). The study period covers 2019-2033.

Poland Life And Non-Life Insurance Market Market Structure & Competitive Landscape

The Polish insurance market exhibits a moderately concentrated structure, with a few dominant players holding significant market share. Key players include Powszechny Zaklad Ubezpieczen SA, Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA, Towarzystwo Ubezpieczen I Reasekuracji Warta SA, Uniqa Towarzystwo Ubezpieczen SA, Generali Towarzystwo Ubezpieczen SA, Compensa Towarzystwo Ubezpieczen SA, Interrisk Towarzystwo Ubezpieczen SA, Aviva Towarzystwo Ubezpieczen Na Zycie SA, Wiener Towarzystwo Ubezpieczen SA, and Ergo Hestia SA. However, the market also features a number of smaller, specialized insurers.

- Market Concentration: The top five players hold an estimated xx% market share in 2025, indicating a moderately consolidated market. The Herfindahl-Hirschman Index (HHI) is estimated at xx, suggesting a competitive but not excessively concentrated environment.

- Innovation Drivers: Technological advancements, particularly in digitalization and data analytics, are driving innovation. The increasing adoption of Insurtech solutions is also impacting market dynamics.

- Regulatory Impacts: The Polish Financial Supervision Authority (KNF) plays a significant role in shaping market regulations, impacting product offerings and operational procedures. Recent regulatory changes focused on consumer protection and financial stability have influenced the market.

- Product Substitutes: The market faces competition from alternative financial products and services, such as investment vehicles and peer-to-peer lending platforms.

- End-User Segmentation: The market is segmented by various factors including age, income level, and risk profile. Growth in specific segments, like the increasing middle class, presents significant opportunities.

- M&A Trends: The past five years have witnessed xx M&A deals in the Polish insurance sector, with a total value of approximately xx Million. Consolidation is expected to continue as larger players seek to expand their market share.

Poland Life And Non-Life Insurance Market Market Trends & Opportunities

The Poland life and non-life insurance market is experiencing steady growth, driven by factors such as rising disposable incomes, increasing awareness of insurance products, and government initiatives promoting financial inclusion. The market size is projected to reach xx Million by 2025, with a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration rates are increasing, particularly in the non-life segment, driven by factors such as mandatory motor insurance and the growing adoption of homeowner's insurance. Technological advancements are driving the growth of digital insurance platforms and online distribution channels, allowing for increased efficiency and customer convenience. Consumer preferences are shifting towards more customized and digitally-driven insurance products. The intensified competition among existing players and the emergence of new entrants drive innovation and pricing pressures, shaping the competitive landscape.

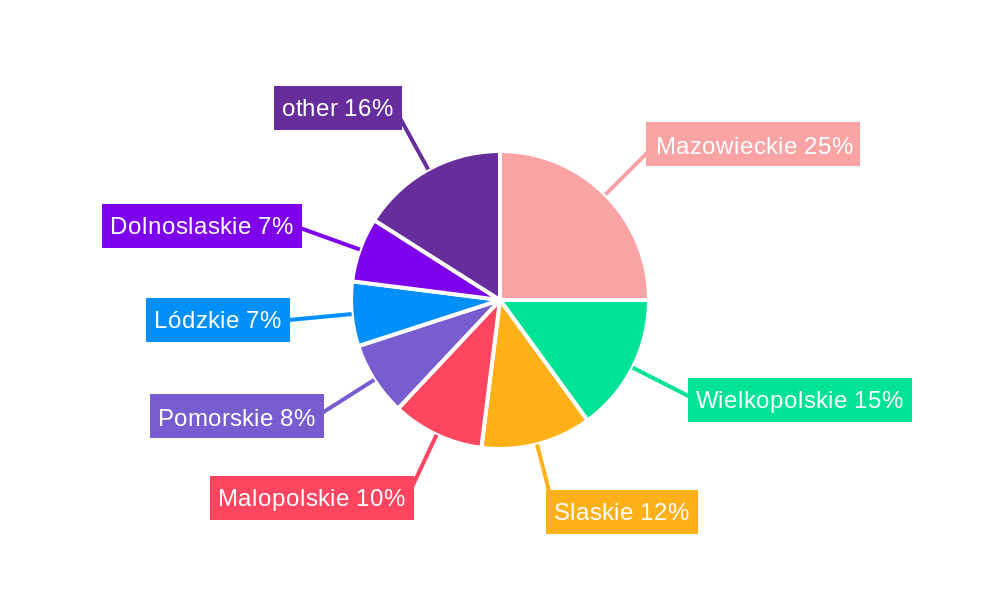

Dominant Markets & Segments in Poland Life And Non-Life Insurance Market

The Warsaw metropolitan area and other major urban centers represent the dominant regions within the Poland life and non-life insurance market. These areas benefit from higher population density, greater economic activity, and increased disposable incomes leading to higher insurance penetration rates.

- Key Growth Drivers:

- Economic Growth: Steady economic growth in major urban centers fuels higher insurance demand.

- Rising Disposable Incomes: Increasing disposable incomes in urban areas create higher purchasing power for insurance products.

- Government Initiatives: Government policies encouraging financial inclusion also contribute to growth.

- Infrastructure Development: Continued infrastructure investments in urban areas support economic activity and insurance uptake.

The non-life segment, particularly motor insurance, holds a dominant position due to legal mandates and the increasing number of vehicles. The life insurance segment is expected to show significant growth, driven by rising awareness of long-term financial security needs and the growing middle class.

Poland Life And Non-Life Insurance Market Product Analysis

The Polish insurance market offers a wide range of products including motor, health, life, property, and liability insurance. Recent innovations include the introduction of digital platforms for policy sales and management, and the development of customized products tailored to specific customer needs. These advancements enhance convenience and efficiency for both insurers and policyholders, contributing to greater market reach and customer satisfaction. The market is witnessing a shift towards parametric insurance and other innovative solutions tailored to emerging risks and technological advancements, focusing on ease of access and streamlined processes.

Key Drivers, Barriers & Challenges in Poland Life And Non-Life Insurance Market

Key Drivers:

- Technological advancements driving digitalization and personalized offerings.

- Rising disposable incomes among a growing middle class, increasing insurance purchasing power.

- Government initiatives aimed at promoting financial inclusion and insurance penetration.

Key Challenges:

- Regulatory complexities and changing compliance requirements create operational hurdles and uncertainty.

- Intense competition from existing players and new market entrants leads to pricing pressures.

- Supply chain disruptions caused by economic fluctuations can impact insurer operations and profitability.

Growth Drivers in the Poland Life And Non-Life Insurance Market Market

The market's growth is propelled by economic expansion, which leads to higher disposable incomes and increased demand for risk mitigation solutions. Technological advancements, particularly in digital distribution channels, are significantly streamlining processes, enhancing customer experience and reducing operational costs. Supportive government policies promoting financial inclusion further augment market expansion.

Challenges Impacting Poland Life And Non-Life Insurance Market Growth

Significant challenges include adapting to evolving regulatory frameworks, navigating intense competition, and addressing potential supply chain disruptions. These factors can hinder market growth by increasing operational costs, affecting profitability and limiting market expansion.

Key Players Shaping the Poland Life And Non-Life Insurance Market Market

- Powszechny Zaklad Ubezpieczen SA

- Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- Towarzystwo Ubezpieczen I Reasekuracji Warta SA

- Uniqa Towarzystwo Ubezpieczen SA

- Generali Towarzystwo Ubezpieczen SA

- Compensa Towarzystwo Ubezpieczen SA

- Interrisk Towarzystwo Ubezpieczen SA

- Aviva Towarzystwo Ubezpieczen Na Zycie SA

- Wiener Towarzystwo Ubezpieczen SA

- Ergo Hestia SA

Significant Poland Life And Non-Life Insurance Market Industry Milestones

- March 2023: Allianz Polska launched a fully digital process for individual life insurance sales, eliminating paperwork.

- May 2023: Generali agreed to sell Generali Deutschland Pensionskasse to Frankfurter Leben, reflecting consolidation trends.

Future Outlook for Poland Life And Non-Life Insurance Market Market

The Polish life and non-life insurance market is poised for continued growth, driven by sustained economic expansion, technological advancements, and supportive regulatory measures. Strategic opportunities lie in leveraging digital technologies, expanding product offerings to cater to evolving customer needs, and effectively managing the competitive landscape. The market's potential is significant, with ample room for expansion and innovation in the coming years.

Poland Life And Non-Life Insurance Market Segmentation

-

1. Insurance Type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non Life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Others

-

1.1. Life Insurance

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Others

Poland Life And Non-Life Insurance Market Segmentation By Geography

- 1. Poland

Poland Life And Non-Life Insurance Market Regional Market Share

Geographic Coverage of Poland Life And Non-Life Insurance Market

Poland Life And Non-Life Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non Life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Others

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Poland Life And Non-Life Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6.1.1. Life Insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non Life Insurance

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Others

- 6.1.1. Life Insurance

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Powszechny Zaklad Ubezpieczen SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Towarzystwo Ubezpieczen I Reasekuracji Warta SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Uniqa Towarzystwo Ubezpieczen SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Generali Towarzystwo Ubezpieczen SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Compensa Towarzystwo Ubezpieczen SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Interrisk Towarzystwo Ubezpieczen SA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Aviva Towarzystwo Ubezpieczen Na Zycie SA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wiener Towarzystwo Ubezpieczen SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Ergo Hestia SA**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Powszechny Zaklad Ubezpieczen SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland Life And Non-Life Insurance Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Life And Non-Life Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Insurance Type 2020 & 2033

- Table 2: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Insurance Type 2020 & 2033

- Table 5: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Life And Non-Life Insurance Market?

The projected CAGR is approximately 7.19%.

2. Which companies are prominent players in the Poland Life And Non-Life Insurance Market?

Key companies in the market include Powszechny Zaklad Ubezpieczen SA, Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA, Towarzystwo Ubezpieczen I Reasekuracji Warta SA, Uniqa Towarzystwo Ubezpieczen SA, Generali Towarzystwo Ubezpieczen SA, Compensa Towarzystwo Ubezpieczen SA, Interrisk Towarzystwo Ubezpieczen SA, Aviva Towarzystwo Ubezpieczen Na Zycie SA, Wiener Towarzystwo Ubezpieczen SA, Ergo Hestia SA**List Not Exhaustive.

3. What are the main segments of the Poland Life And Non-Life Insurance Market?

The market segments include Insurance Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Tax Benefits and Incentives; Changing Risk Perception; Increasing Motorization.

6. What are the notable trends driving market growth?

Non Life Insurance Policies Generate Higher Premium Revenue in Poland.

7. Are there any restraints impacting market growth?

Tax Benefits and Incentives; Changing Risk Perception; Increasing Motorization.

8. Can you provide examples of recent developments in the market?

May 2023: Generali reaches agreement to dispose of Generali Deutschland Pensionskasse to Frankfurter Leben

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Life And Non-Life Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Life And Non-Life Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Life And Non-Life Insurance Market?

To stay informed about further developments, trends, and reports in the Poland Life And Non-Life Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence