Key Insights

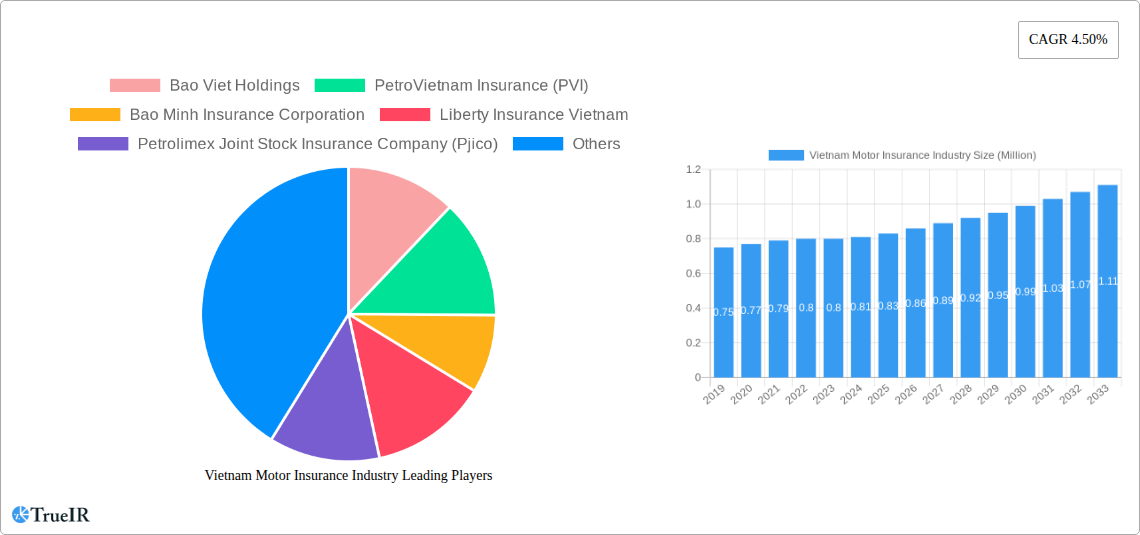

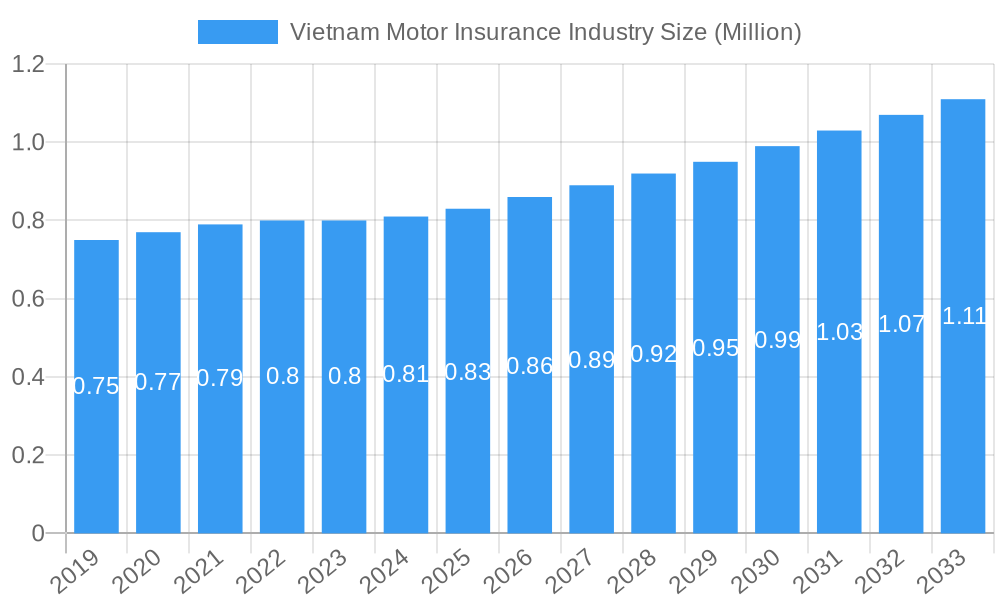

The Vietnam Motor Insurance Industry is poised for significant expansion, with a current market size of approximately USD 0.81 million and a projected Compound Annual Growth Rate (CAGR) of 4.50% from 2019 to 2033. This growth is primarily propelled by a robust increase in vehicle ownership across passenger and commercial segments, fueled by a burgeoning middle class and a developing economy. The compulsory third-party liability insurance (CTPL) segment continues to be a foundational pillar, ensuring basic coverage for vehicle owners. However, a notable trend is the increasing adoption of comprehensive insurance policies, driven by greater consumer awareness of asset protection and a desire for broader coverage against damages and theft. The expansion of the automotive sector, including the introduction of new models and the strengthening of commercial transportation networks, directly correlates with the demand for motor insurance. Furthermore, government initiatives aimed at enhancing road safety and formalizing the insurance sector contribute to a more stable and growing market environment.

Vietnam Motor Insurance Industry Market Size (In Million)

The distribution landscape is undergoing a dynamic transformation, with online channels rapidly gaining traction alongside traditional methods like agents, brokers, and banks. This shift is indicative of evolving consumer preferences for convenience and digital accessibility. Insurance companies are investing in digital platforms to streamline policy acquisition, claims processing, and customer service. Key players like Bao Viet Holdings, PetroVietnam Insurance (PVI), and Bao Minh Insurance Corporation are actively competing, alongside emerging entities and international insurers such as Liberty Insurance Vietnam and Fubon Insurance Company. The competitive environment is fostering innovation in product offerings and customer engagement strategies. While growth is robust, potential restraints could stem from economic downturns affecting disposable income, an increase in fraudulent claims requiring stringent regulatory oversight, and evolving vehicle technologies that may necessitate adjustments in underwriting and pricing strategies. Despite these challenges, the industry is expected to maintain a steady upward trajectory, driven by consistent demand and a maturing insurance market.

Vietnam Motor Insurance Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Vietnam Motor Insurance Industry. Covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this study offers unparalleled insights into market dynamics, emerging trends, and future growth opportunities. Leveraging high-volume keywords such as "Vietnam auto insurance," "car insurance Vietnam," "motor vehicle insurance market," and "insurance Vietnam," this report is optimized for search engines and designed to engage industry stakeholders, including insurers, regulators, investors, and market analysts. We delve into key segments like Compulsory Third-Party Liability Insurance (CTPL) and Comprehensive Insurance, alongside vehicle types including Passenger Vehicles and Commercial Vehicles. The report also examines various Distribution Channels, from traditional Agents and Brokers to evolving Online platforms and Banks.

Vietnam Motor Insurance Industry Market Structure & Competitive Landscape

The Vietnam Motor Insurance Industry is characterized by a moderately concentrated market structure, with leading players like Bao Viet Holdings, PetroVietnam Insurance (PVI), and Bao Minh Insurance Corporation holding significant market share. Innovation drivers are increasingly focused on digital transformation, enhanced customer experience, and the development of tailored insurance products. Regulatory impacts, particularly those related to road safety and mandatory coverage, significantly shape the competitive landscape. Product substitutes, while limited in the core motor insurance offerings, are emerging in the form of bundled services and advanced warranty programs. End-user segmentation is becoming more nuanced, with distinct needs identified for individual car owners versus fleet operators. Mergers and acquisitions (M&A) trends are notable as companies seek to expand their market reach and diversify their portfolios. In the historical period (2019-2024), we observed xx number of M&A deals, with a combined transaction value estimated at xx Million. Concentration ratios for the top 3 players stand at approximately xx%, indicating a competitive yet consolidated market.

- Market Concentration: Moderate, with key players dominating market share.

- Innovation Drivers: Digitalization, customer-centric product development, risk management technology.

- Regulatory Impacts: Evolving policies on mandatory coverage and safety standards.

- Product Substitutes: Growing interest in value-added services and extended warranties.

- End-User Segmentation: Differentiated needs for retail and commercial vehicle owners.

- M&A Trends: Strategic acquisitions aimed at market expansion and service enhancement.

Vietnam Motor Insurance Industry Market Trends & Opportunities

The Vietnam Motor Insurance Industry is poised for substantial growth, driven by a rising vehicle parc, increasing disposable incomes, and a growing awareness of insurance benefits. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching an estimated value of xx Million by the end of the forecast period. Technological shifts, including the adoption of telematics, AI-powered claims processing, and online sales platforms, are reshaping customer engagement and operational efficiency. Consumer preferences are leaning towards more personalized and flexible insurance solutions, with a demand for faster claims settlement and improved customer service. Competitive dynamics are intensifying, with both domestic and international players vying for market share. The market penetration rate for motor insurance is expected to grow from xx% in 2025 to xx% by 2033, indicating a significant untapped potential. Opportunities abound for insurers to develop innovative products that cater to the evolving needs of the Vietnamese consumer, such as usage-based insurance, electric vehicle coverage, and integrated mobility solutions. The increasing digitalization of the economy and the government's focus on digital transformation further present opportunities for online distribution channels and InsurTech partnerships. The growing middle class and urbanization are also key drivers for increased demand for both passenger and commercial vehicle insurance.

Dominant Markets & Segments in Vietnam Motor Insurance Industry

Within the Vietnam Motor Insurance Industry, Passenger Vehicles represent the dominant vehicle type segment, accounting for an estimated xx% of the total market value in 2025. This dominance is fueled by Vietnam's rapidly growing middle class and increasing urbanization, leading to a surge in private car ownership. The Comprehensive Insurance policy type is also a key growth driver, showing a higher uptake among individual vehicle owners seeking broader protection beyond mandatory requirements. The Agents distribution channel continues to hold a significant market share, valued at xx Million in 2025, due to the trust and personalized advice they offer. However, the Online distribution channel is experiencing rapid growth, projected to increase its share by xx% over the forecast period, driven by convenience and competitive pricing.

- Dominant Vehicle Type: Passenger Vehicles.

- Key Growth Drivers: Rising disposable incomes, urbanization, expanding road infrastructure, increasing new vehicle sales.

- Detailed Analysis: The burgeoning middle class and a cultural affinity for private transportation have led to a sustained increase in passenger vehicle ownership, directly translating into higher demand for motor insurance.

- Dominant Policy Type: Comprehensive Insurance.

- Key Growth Drivers: Increased consumer awareness of potential risks, desire for holistic protection against damages, theft, and third-party liabilities.

- Detailed Analysis: As vehicle values increase and drivers become more aware of the financial implications of accidents, demand for comprehensive coverage that offers peace of mind is on the rise.

- Dominant Distribution Channel: Agents.

- Key Growth Drivers: Established trust, personalized customer service, ability to explain complex policy terms, strong network penetration in urban and rural areas.

- Detailed Analysis: Despite the rise of digital channels, the human touch and expert advice provided by agents remain crucial for many consumers, especially for understanding the nuances of motor insurance policies.

- Emerging Distribution Channel: Online.

- Key Growth Drivers: Convenience, ease of comparison, competitive pricing, tech-savvy younger demographic, government push for digital services.

- Detailed Analysis: The increasing adoption of e-commerce and digital payment systems is making online platforms an attractive and efficient way for consumers to purchase motor insurance.

Vietnam Motor Insurance Industry Product Analysis

Product innovation in the Vietnam Motor Insurance Industry is increasingly centered on leveraging technology for enhanced customer experiences and risk management. This includes the development of usage-based insurance (UBI) models that reward safe driving, and integrated telematics solutions for fleet management. Insurers are also exploring niche products tailored for specific vehicle types, such as electric vehicles, and offering personalized coverage options based on individual driving habits and needs. Competitive advantages are being built through faster claims processing enabled by AI and digital platforms, as well as the integration of value-added services like roadside assistance and accident repair network partnerships. The focus is on providing not just financial protection, but also convenience and proactive risk mitigation.

Key Drivers, Barriers & Challenges in Vietnam Motor Insurance Industry

The Vietnam Motor Insurance Industry is propelled by several key drivers, including a growing vehicle parc, increasing economic prosperity, and a rising awareness of the importance of insurance. Technological advancements, such as telematics and digital platforms, are enabling more personalized products and efficient operations. Government initiatives promoting road safety and insurance penetration also play a crucial role. However, the industry faces significant barriers and challenges. These include a price-sensitive market, the persistent issue of underinsurance for certain segments, and regulatory hurdles that can impact product development and pricing.

- Key Drivers:

- Economic Growth: Rising disposable incomes and a growing middle class.

- Vehicle Parc Expansion: Increasing number of passenger and commercial vehicles on the road.

- Technological Adoption: Telematics, digital platforms, and InsurTech innovations.

- Regulatory Support: Government focus on insurance penetration and road safety.

- Barriers & Challenges:

- Price Sensitivity: Consumers often prioritize cost over comprehensive coverage.

- Underinsurance: A significant portion of the market remains underinsured or uninsured.

- Regulatory Complexity: Evolving regulations can impact operational efficiency.

- Fraudulent Claims: Persistent challenge requiring robust detection mechanisms.

- Competition: Intense competition among established and new market entrants.

Growth Drivers in the Vietnam Motor Insurance Industry Market

Growth in the Vietnam Motor Insurance Industry is primarily driven by the consistent increase in the number of vehicles on the road, coupled with a growing middle class with enhanced purchasing power. Technological advancements, particularly in telematics and digital distribution, are opening new avenues for customer engagement and product customization. Furthermore, the Vietnamese government's commitment to improving road safety and financial inclusion through insurance initiatives acts as a significant catalyst. The increasing adoption of comprehensive insurance policies, as opposed to solely mandatory third-party liability, also contributes to market expansion.

Challenges Impacting Vietnam Motor Insurance Industry Growth

Despite robust growth prospects, the Vietnam Motor Insurance Industry faces several impediments. The inherent price sensitivity of the Vietnamese consumer often leads to a preference for cheaper, less comprehensive coverage, limiting the potential for higher premium collections. Regulatory complexities and the need for constant adaptation to evolving legal frameworks can create operational challenges. Moreover, the persistent issue of fraudulent claims necessitates significant investment in fraud detection and prevention mechanisms, impacting profitability. Intense competition within the market also puts pressure on pricing and profit margins.

Key Players Shaping the Vietnam Motor Insurance Industry Market

- Bao Viet Holdings

- PetroVietnam Insurance (PVI)

- Bao Minh Insurance Corporation

- Liberty Insurance Vietnam

- Petrolimex Joint Stock Insurance Company (Pjico)

- AAA Assurance Corporation

- BIDV Insurance Corporation

- Fubon Insurance Company

- Phu Hung Assurance Corporation

- Samsung Vina Insurance Company

Significant Vietnam Motor Insurance Industry Industry Milestones

- December 2023: Cathay Insurance Vietnam partnered with SAWAD to launch an "Dual Finance" initiative, providing customers with financial assistance alongside mandatory insurance coverage. Cathay also announced plans to introduce a personal injury insurance scheme.

- November 2023: Vietnam officially joined the Association of Southeast Asian Nations (ASEAN) Compulsory Motor Insurance Scheme (ACMI), mandating third-party motor liability insurance for all vehicles in transit within ASEAN member states.

Future Outlook for Vietnam Motor Insurance Industry Market

The future outlook for the Vietnam Motor Insurance Industry is highly promising, characterized by sustained growth and increasing sophistication. The burgeoning vehicle parc, coupled with a rising middle class, will continue to be a fundamental growth driver. Insurers that successfully embrace digital transformation, offer personalized and value-added products, and leverage data analytics will be best positioned to capture market share. The evolving regulatory landscape, particularly with Vietnam's integration into regional insurance frameworks like ACMI, presents both opportunities for expansion and challenges for adaptation. Strategic partnerships and a focus on customer-centricity will be paramount for long-term success in this dynamic and expanding market. The industry is expected to witness significant growth in comprehensive insurance offerings and the adoption of digital sales and service channels, further solidifying its trajectory of positive development.

Vietnam Motor Insurance Industry Segmentation

-

1. Policy Type

- 1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 1.2. Comprehensive Insurance

-

2. Vehicle Type

- 2.1. Passenger Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Agents

- 3.2. Brokers

- 3.3. Banks

- 3.4. Online

- 3.5. Other Distribution Channels

Vietnam Motor Insurance Industry Segmentation By Geography

- 1. Vietnam

Vietnam Motor Insurance Industry Regional Market Share

Geographic Coverage of Vietnam Motor Insurance Industry

Vietnam Motor Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 5.1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 5.1.2. Comprehensive Insurance

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Agents

- 5.3.2. Brokers

- 5.3.3. Banks

- 5.3.4. Online

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 6. Vietnam Motor Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Policy Type

- 6.1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 6.1.2. Comprehensive Insurance

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Agents

- 6.3.2. Brokers

- 6.3.3. Banks

- 6.3.4. Online

- 6.3.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Policy Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bao Viet Holdings

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 PetroVietnam Insurance (PVI)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bao Minh Insurance Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Liberty Insurance Vietnam

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Petrolimex Joint Stock Insurance Company (Pjico)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 AAA Assurance Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BIDV Insurance Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Fubon Insurance Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Phu Hung Assurance Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Samsung Vina Insurance Company**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Bao Viet Holdings

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Vietnam Motor Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Vietnam Motor Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2020 & 2033

- Table 2: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2020 & 2033

- Table 3: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 4: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 7: Vietnam Motor Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Vietnam Motor Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2020 & 2033

- Table 10: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2020 & 2033

- Table 11: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 12: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2020 & 2033

- Table 13: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Vietnam Motor Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Vietnam Motor Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Motor Insurance Industry?

The projected CAGR is approximately 4.50%.

2. Which companies are prominent players in the Vietnam Motor Insurance Industry?

Key companies in the market include Bao Viet Holdings, PetroVietnam Insurance (PVI), Bao Minh Insurance Corporation, Liberty Insurance Vietnam, Petrolimex Joint Stock Insurance Company (Pjico), AAA Assurance Corporation, BIDV Insurance Corporation, Fubon Insurance Company, Phu Hung Assurance Corporation, Samsung Vina Insurance Company**List Not Exhaustive.

3. What are the main segments of the Vietnam Motor Insurance Industry?

The market segments include Policy Type, Vehicle Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

6. What are the notable trends driving market growth?

Surge in Vehicle Ownership Generating Major Demand in the Market.

7. Are there any restraints impacting market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

8. Can you provide examples of recent developments in the market?

December 2023: Cathay Insurance Vietnam joined hands with SAWAD to unveil an all-inclusive "Dual Finance" initiative. This program empowers customers to seek financial assistance while securing mandatory insurance coverage seamlessly. To cater to its clientele's diverse needs, Cathay has set to roll out a personal injury insurance scheme in December, complementing its existing financial support and automobile insurance offerings.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Motor Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Motor Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Motor Insurance Industry?

To stay informed about further developments, trends, and reports in the Vietnam Motor Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence