Key Insights

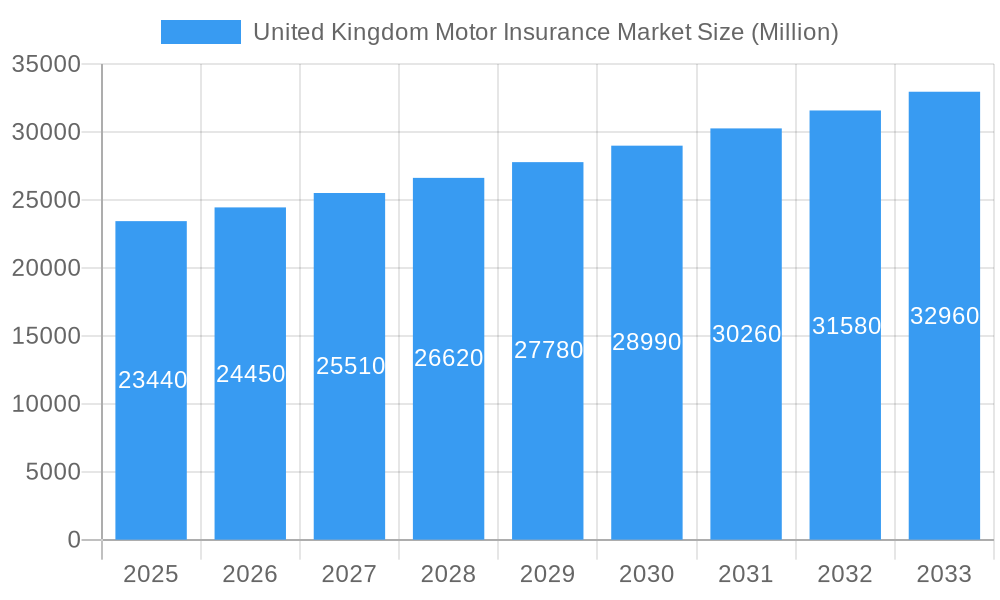

The UK motor insurance market, valued at £23.44 billion in 2025, is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 4.16% from 2025 to 2033. This growth is fueled by several key factors. Rising vehicle ownership, particularly among younger demographics, coupled with increasing urbanization and the consequential rise in traffic density, contributes significantly to the demand for motor insurance. Furthermore, stricter regulatory requirements regarding minimum insurance coverage and a growing awareness of the financial implications of uninsured driving are driving market expansion. The market is segmented by product type (Third-Party, Third-Party Fire & Theft, Comprehensive) and distribution channels (Direct, Agency, Banks, Others). While direct sales channels are gaining traction due to their cost-effectiveness and convenience, traditional agency networks continue to hold significant market share, leveraging established relationships with customers. The competitive landscape includes major players like Aviva, Allianz, and Zurich, alongside a diverse range of smaller insurers and brokers. This competition fosters innovation, driving the introduction of new products, telematics-based insurance offerings, and improved customer service. However, factors such as economic downturns, potential increases in claims frequency due to evolving driving patterns, and intense competition may act as restraints on market growth in the coming years.

United Kingdom Motor Insurance Market Market Size (In Billion)

The forecast for the UK motor insurance market points towards continued expansion, albeit at a moderate pace. The dominance of established players suggests a relatively stable market structure, although the entry of new, digitally-focused insurers and the increasing adoption of Insurtech solutions will likely reshape the competitive dynamics. The market's sensitivity to macroeconomic conditions necessitates careful consideration of potential economic fluctuations. Sustained growth in the coming years hinges on navigating these potential headwinds, while successfully capitalizing on opportunities presented by technological advancements and changing consumer behavior. Specific regional variations within the UK market, though not detailed in the provided data, may exist and should be considered for a more granular analysis. Further insights into specific driver and trend details would allow for a more comprehensive and accurate forecast.

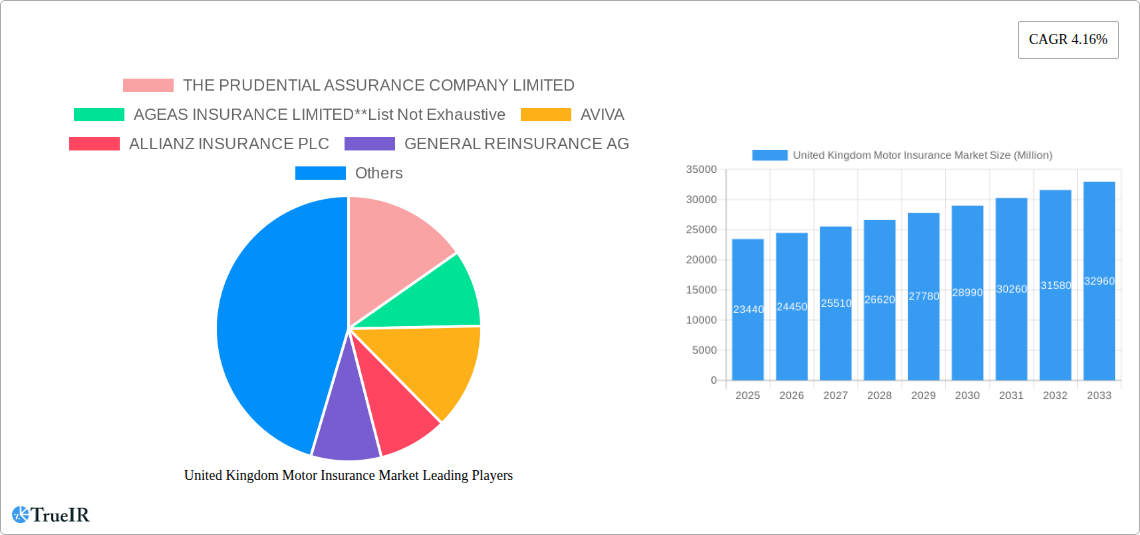

United Kingdom Motor Insurance Market Company Market Share

United Kingdom Motor Insurance Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the UK motor insurance market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report examines market size, segmentation, competitive dynamics, and future growth potential. The report leverages extensive data and qualitative analysis to present a complete picture of this dynamic market.

United Kingdom Motor Insurance Market Structure & Competitive Landscape

The UK motor insurance market is characterized by a moderately concentrated landscape, with a handful of major players dominating market share. The market's concentration ratio (CR4) is estimated at xx% in 2025, indicating a relatively consolidated structure. Key players such as Aviva, Allianz Insurance PLC, AXA Insurance UK PLC, and Zurich Assurance Ltd compete intensely, driving innovation in product offerings and distribution channels. Regulatory changes, particularly those related to pricing transparency and consumer protection, significantly impact market dynamics. Product substitution is limited, with the core offering remaining relatively standardized, although technological advancements are gradually introducing more personalized and data-driven insurance solutions. The market exhibits substantial M&A activity, exemplified by recent transactions such as AXA UK&I's acquisition of Ageas UK's commercial operations. The total value of M&A transactions in the UK motor insurance market between 2019 and 2024 was approximately £xx Million. End-user segmentation is primarily driven by vehicle type, age of driver, and risk profile.

- High Market Concentration: Dominated by a few large players.

- Innovation Drivers: Technological advancements in telematics and data analytics.

- Regulatory Impacts: Stringent regulations concerning pricing and consumer protection.

- Limited Product Substitution: Core offerings remain similar, with gradual technological advancements.

- Significant M&A Activity: Consolidation and strategic acquisitions driving market shifts.

- Diverse End-User Segmentation: Based on vehicle type, driver demographics, and risk assessments.

United Kingdom Motor Insurance Market Market Trends & Opportunities

The UK motor insurance market is projected to experience steady growth, with a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033. This growth is fueled by several factors, including increasing vehicle ownership, particularly in urban areas, rising vehicle values, and government regulations promoting safer driving practices. Technological advancements, such as the adoption of telematics and usage-based insurance (UBI), are transforming the industry, allowing for more accurate risk assessment and personalized pricing. Consumer preferences are shifting towards digital channels and more flexible, customized insurance products. The competitive landscape is characterized by intense rivalry, with companies investing heavily in digital transformation and customer experience initiatives. Market penetration rates remain relatively high, leaving limited untapped potential in the core market but presenting opportunities within niche areas such as specialist vehicle insurance or young driver segments. The total market size is estimated at £xx Million in 2025, projected to reach £xx Million by 2033.

Dominant Markets & Segments in United Kingdom Motor Insurance Market

The Comprehensive insurance segment holds the largest market share, driven by increasing awareness of the potential financial burdens of accidents. Within distribution channels, the Agency model remains prevalent, although Direct channels are gaining traction, especially amongst younger demographics. Regionally, the market is largely homogeneous in terms of penetration and growth, although variations might exist according to regional income levels and vehicle ownership rates.

Key Growth Drivers:

- Increasing Vehicle Ownership: Rising car ownership fuels demand for insurance.

- Higher Vehicle Values: More expensive vehicles necessitate higher insurance coverage.

- Technological Advancements: Telematics and UBI enabling personalized pricing and risk assessment.

- Regulatory changes: promoting safer driving and influencing insurance policies

Market Dominance Analysis:

The Comprehensive segment's dominance stems from its comprehensive coverage against various risks, appealing to risk-averse customers. Agency distribution channels remain dominant due to established relationships and trust, while direct channels are rapidly increasing market share due to convenience and lower costs. Regional variation is minimal, with growth relatively consistent throughout the UK.

United Kingdom Motor Insurance Market Product Analysis

Product innovation within the UK motor insurance market is largely driven by technological advancements. Telematics and usage-based insurance (UBI) are increasingly popular, allowing insurers to offer more accurate and customized pricing based on driver behavior. The incorporation of AI and machine learning enhances risk assessment and fraud detection. These innovative products offer competitive advantages by improving risk management and providing more tailored solutions to customer needs.

Key Drivers, Barriers & Challenges in United Kingdom Motor Insurance Market

Key Drivers:

- Technological advancements: Telematics, AI-driven risk assessment, and digital distribution channels are streamlining operations and improving customer experience.

- Economic growth: Rising disposable incomes increase the demand for motor insurance.

- Government policies: Regulations promoting road safety and consumer protection drive industry evolution.

Challenges and Restraints:

- Intense competition: Numerous insurers compete fiercely for market share, placing downward pressure on premiums.

- Regulatory complexity: Stringent regulations impact operational costs and increase compliance burdens.

- Supply chain issues: Disruptions in the supply chain can impact the availability of vehicles and spare parts, indirectly influencing claim payouts.

Growth Drivers in the United Kingdom Motor Insurance Market Market

The growth of the UK motor insurance market is fueled by several factors. Technological innovation, particularly in telematics and AI, enhances efficiency, personalization, and risk management. Economic growth increases disposable incomes and car ownership. Stringent government regulations promoting road safety inadvertently increase the demand for comprehensive insurance coverage.

Challenges Impacting United Kingdom Motor Insurance Market Growth

The UK motor insurance market faces challenges like intense competition, leading to price wars. Regulatory hurdles, especially concerning data privacy and pricing transparency, increase compliance costs. Supply chain disruptions from global events affect claims processing and operational efficiency.

Key Players Shaping the United Kingdom Motor Insurance Market Market

Significant United Kingdom Motor Insurance Market Industry Milestones

- February 2022: AXA UK&I acquired the renewal rights to Ageas UK's commercial operations for GBP 47.5 Million, strengthening AXA's position in the commercial insurance sector.

- January 2022: Comprehensive car insurance premiums in the UK increased by 5% in Q4 2021, reaching an average of GBP 539 (USD 734.06), indicating volatile market conditions.

Future Outlook for United Kingdom Motor Insurance Market Market

The UK motor insurance market is poised for continued growth, driven by technological advancements, increasing vehicle ownership, and evolving consumer preferences. Strategic opportunities exist in developing innovative products leveraging telematics and AI, targeting niche market segments, and optimizing distribution channels for greater efficiency and customer reach. The market's potential for growth is significant, with opportunities for both established and new entrants.

United Kingdom Motor Insurance Market Segmentation

-

1. Product Type

- 1.1. Third-Party

- 1.2. Third-party Fire and Theft

- 1.3. Comprehensive

-

2. Distribution channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Others

United Kingdom Motor Insurance Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Motor Insurance Market Regional Market Share

Geographic Coverage of United Kingdom Motor Insurance Market

United Kingdom Motor Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Third-Party

- 5.1.2. Third-party Fire and Theft

- 5.1.3. Comprehensive

- 5.2. Market Analysis, Insights and Forecast - by Distribution channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United Kingdom Motor Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Third-Party

- 6.1.2. Third-party Fire and Theft

- 6.1.3. Comprehensive

- 6.2. Market Analysis, Insights and Forecast - by Distribution channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 THE PRUDENTIAL ASSURANCE COMPANY LIMITED

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 AGEAS INSURANCE LIMITED**List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AVIVA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ALLIANZ INSURANCE PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 GENERAL REINSURANCE AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ZURICH ASSURANCE LTD

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 AXA INSURANCE UK PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 DL INSURANCE SERVICES LIMITED

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ROYAL & SUN ALLIANCE INSURANCE PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 THE PRUDENTIAL ASSURANCE COMPANY LIMITED

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Motor Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United Kingdom Motor Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Motor Insurance Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: United Kingdom Motor Insurance Market Revenue Million Forecast, by Distribution channel 2020 & 2033

- Table 3: United Kingdom Motor Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: United Kingdom Motor Insurance Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: United Kingdom Motor Insurance Market Revenue Million Forecast, by Distribution channel 2020 & 2033

- Table 6: United Kingdom Motor Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Motor Insurance Market?

The projected CAGR is approximately 4.16%.

2. Which companies are prominent players in the United Kingdom Motor Insurance Market?

Key companies in the market include THE PRUDENTIAL ASSURANCE COMPANY LIMITED, AGEAS INSURANCE LIMITED**List Not Exhaustive, AVIVA, ALLIANZ INSURANCE PLC, GENERAL REINSURANCE AG, ZURICH ASSURANCE LTD, AXA INSURANCE UK PLC, DL INSURANCE SERVICES LIMITED, ROYAL & SUN ALLIANCE INSURANCE PLC.

3. What are the main segments of the United Kingdom Motor Insurance Market?

The market segments include Product Type, Distribution channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.44 Million as of 2022.

5. What are some drivers contributing to market growth?

Data Privacy Regulations; Business Interruption.

6. What are the notable trends driving market growth?

High Volatility in Car Insurance Premiums During the Past Few Years.

7. Are there any restraints impacting market growth?

Complexity and Lack of Understanding; Cost of Coverage.

8. Can you provide examples of recent developments in the market?

Feb 2022: For an initial payment of GBP 47.5 million, AXA UK&I purchased the renewal rights to Ageas UK's commercial operations. This acquisition reinforces AXA's growth strategy and dedication to its commercial business clients and broker alliances, particularly in the SME and Schemes market sectors. About 100 Ageas UK personnel will transfer to AXA Commercial as part of the arrangement to provide continued support and service delivery.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Motor Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Motor Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Motor Insurance Market?

To stay informed about further developments, trends, and reports in the United Kingdom Motor Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence