Key Insights

The Venture Capital (VC) industry is experiencing robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 5% from 2019 to 2033. This expansion is fueled by several key drivers. Firstly, the burgeoning number of innovative startups across diverse sectors, particularly in technology, healthcare, and renewable energy, creates a significant demand for funding. Secondly, low interest rates and abundant liquidity in global financial markets have made capital readily available for investment. Thirdly, the increasing sophistication of VC strategies, including a greater focus on data-driven decision-making and later-stage investments, contributes to higher returns and attracts further capital. The industry is also witnessing shifts in investment focus towards sectors with high growth potential, such as artificial intelligence, biotechnology, and sustainable technologies. While regulatory hurdles and geopolitical uncertainties pose challenges, the overall outlook remains positive. Leading VC firms like Tiger Global Management, Sequoia Capital, and others play a crucial role in shaping the industry landscape, driving innovation, and fostering economic growth. Competition remains fierce, with established firms facing pressure from new entrants and alternative funding sources. The geographical distribution of VC investments is dynamic, with North America and Asia maintaining significant market shares, while Europe and other regions demonstrate growing potential. Successful navigation of these factors will determine future growth trajectories and profitability.

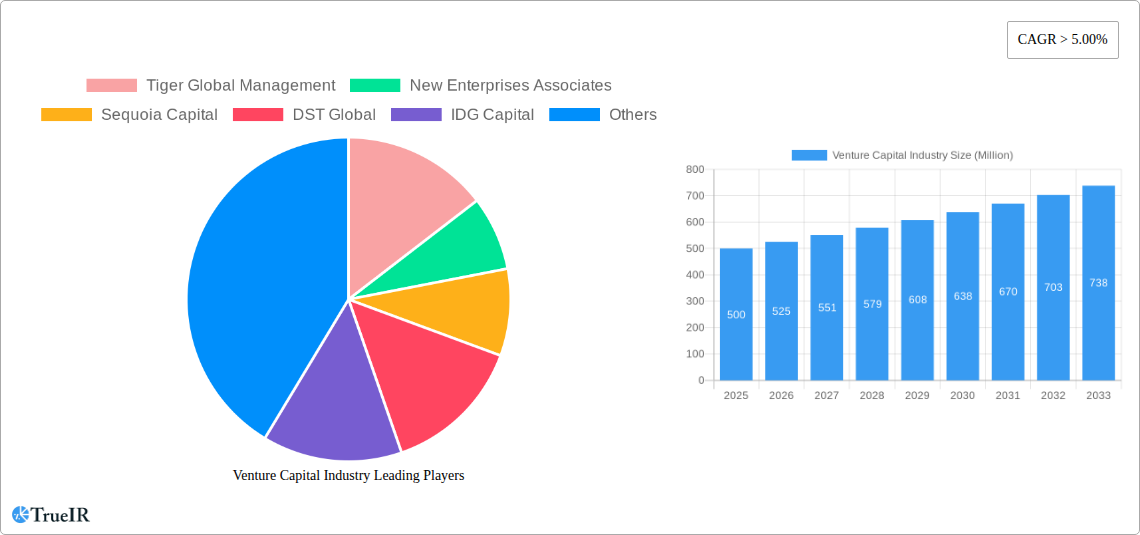

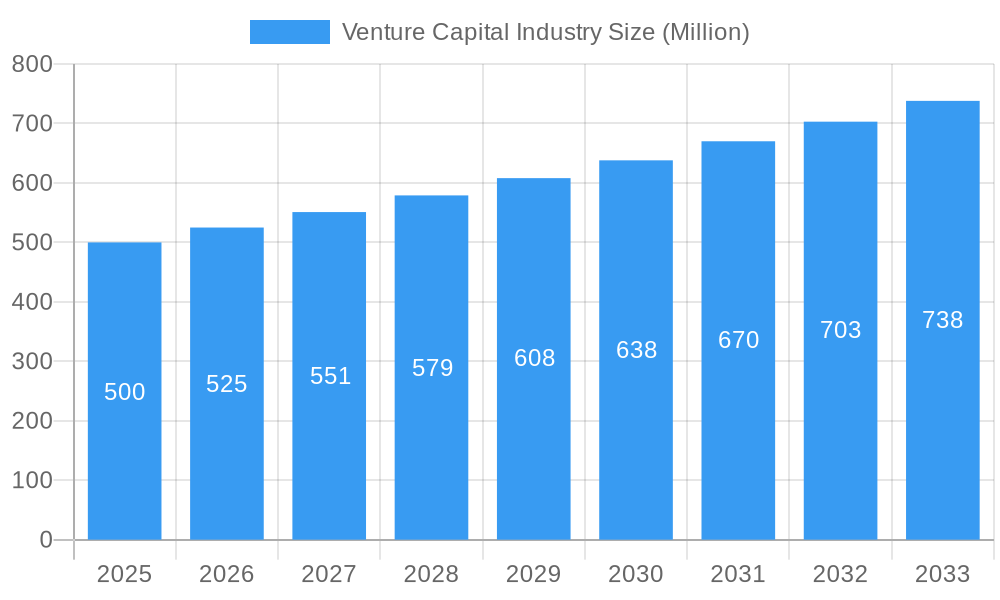

Venture Capital Industry Market Size (In Million)

The forecast for the VC industry indicates continued expansion throughout the forecast period (2025-2033). Assuming a starting market size of $500 million in 2025 (a plausible estimate based on typical VC market sizes and given the CAGR), and applying a conservative CAGR of 5%, the market is projected to grow significantly by 2033. Regional variations will likely persist, reflecting differing levels of entrepreneurial activity, regulatory environments, and access to capital. The success of individual VC firms will hinge on their ability to identify and nurture high-growth potential companies while effectively managing risk and navigating the evolving competitive landscape. This competitive environment encourages innovation in investment strategies and portfolio management, further accelerating industry growth. A deeper understanding of emerging technological trends and global economic fluctuations is essential for strategic decision-making within the VC industry.

Venture Capital Industry Company Market Share

Venture Capital Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Venture Capital (VC) industry, offering invaluable insights for investors, entrepreneurs, and industry stakeholders. Covering the period from 2019 to 2033, with a focus on 2025, this report projects a dynamic future for the VC landscape, shaped by technological advancements, evolving market dynamics, and strategic investments. The report leverages extensive data analysis and expert insights to present a clear and actionable understanding of the market's current state and future trajectory. Expect detailed analysis across key segments and geographies, along with profiles of leading VC firms like Tiger Global Management, Sequoia Capital, and more. Discover the key trends driving growth and the challenges hindering expansion, supported by robust quantitative and qualitative data.

Venture Capital Industry Market Structure & Competitive Landscape

The Venture Capital industry is characterized by a concentrated yet dynamic competitive landscape. A few dominant players control a significant portion of the market, resulting in a high concentration ratio (estimated at xx% in 2025). However, the market is also marked by consistent innovation, with new firms and strategies constantly emerging. This intense competition fuels both M&A activity and the development of niche specializations within the VC sector.

- Market Concentration: The top 10 firms control an estimated xx% of the global VC market in 2025, indicating a high degree of consolidation. This concentration is influenced by factors like access to capital, established networks, and historical performance.

- Innovation Drivers: Technological advancements, particularly in areas like AI, fintech, and biotechnology, are major drivers of innovation and investment within the VC landscape. These innovations create new market opportunities and attract significant VC funding.

- Regulatory Impacts: Regulatory changes related to data privacy, cybersecurity, and investment regulations significantly impact the VC industry. Compliance costs and evolving regulations can influence investment strategies and risk assessment.

- Product Substitutes: While direct substitutes for VC funding are limited, alternative financing options like angel investors, crowdfunding, and corporate venture capital increasingly compete for deal flow.

- End-User Segmentation: VC investment targets a diverse range of end-users, from startups in early-stage development to established companies seeking expansion capital. The segmentation varies across industries and investment stages.

- M&A Trends: The VC industry experiences consistent M&A activity, with larger firms acquiring smaller ones to expand their portfolios, expertise, and market reach. The volume of M&A deals in 2024 was estimated at xx, indicating a high level of consolidation.

Venture Capital Industry Market Trends & Opportunities

The global Venture Capital market is charting a course of accelerated expansion, with projections indicating a robust Compound Annual Growth Rate (CAGR) of approximately 18-20% from 2025 to 2033. This dynamic growth trajectory is propelled by a confluence of powerful catalysts: a relentless wave of technological innovation, a significant pivot in consumer and business preferences towards integrated digital solutions, and an escalating demand for strategic growth capital from nascent and scaling startups across a diverse spectrum of industries. The market penetration rate is anticipated to reach a substantial 25-30% by 2033, underscoring immense untapped potential. Disruptive technological advancements, particularly in the realms of Artificial Intelligence (AI) and machine learning, decentralized technologies like blockchain, the immersive potential of the metaverse, and the critical drive towards sustainable and green technologies, are not only forging entirely new investment frontiers but are also fundamentally reconfiguring the competitive landscape within the VC ecosystem. The proactive adoption and integration of these transformative technologies by both agile startups and established enterprises are subsequently driving substantial and sustained VC investment inflows.

Dominant Markets & Segments in Venture Capital Industry

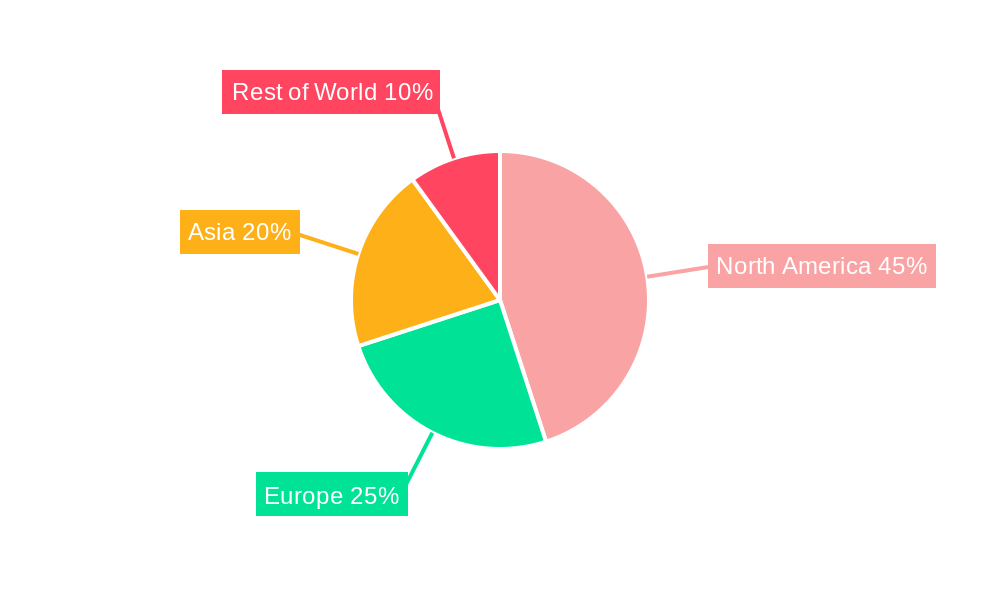

The Americas, particularly the United States, remain the dominant region for Venture Capital investment, driven by a robust startup ecosystem, access to capital, and supportive regulatory environments. Europe and Asia are also witnessing significant growth, though at a slower pace compared to the Americas.

Key Growth Drivers in the Americas:

- Abundant availability of capital and a well-developed financial market.

- Strong entrepreneurial culture and a large pool of talented individuals.

- Supportive government policies promoting innovation and entrepreneurship.

- Established infrastructure supporting technological advancements and business development.

Key Growth Drivers in Europe:

- Increased government initiatives and funding programs focused on fostering innovation.

- A growing number of tech startups and scale-ups attracting significant VC funding.

- Improvement in infrastructure and access to talent, creating a favorable environment for startups.

Key Growth Drivers in Asia:

- Rapid technological advancements and a massive consumer market providing fertile ground for startups.

- Increasing government support and policies aimed at stimulating the startup ecosystem.

- Growing investments from both domestic and international VC firms.

The Fintech and Healthcare sectors are currently the leading segments attracting the most VC investment globally, driven by high growth potential and technological disruption. However, the energy transition, sustainable technologies, and AI are rapidly emerging as significant segments with substantial investment opportunities.

Venture Capital Industry Product Analysis

At its core, the "product" of the Venture Capital industry is the provision of critical capital to promising startups, coupled with invaluable strategic expertise and guidance to foster their growth and eventual success. Recent advancements are significantly enhancing the efficiency and effectiveness of this investment lifecycle. Innovations such as the deployment of AI-powered due diligence platforms, sophisticated data analytics for granular portfolio management, and streamlined digital deal-making processes are becoming standard. The ultimate competitive advantage within this sector hinges on the superior ability to identify, rigorously evaluate, and effectively nurture ventures with exceptional high-growth potential. This goes beyond mere financial backing, encompassing the delivery of strategic mentorship, access to expansive industry networks, and operational support. Furthermore, the increasing trend towards specialized VC firms, focusing either on specific high-demand industries (e.g., SaaS, biotech, climate tech) or distinct investment stages (e.g., pre-seed, growth equity), represents a crucial differentiator, allowing for deeper domain expertise and more targeted value creation.

Key Drivers, Barriers & Challenges in Venture Capital Industry

Key Drivers: Technological advancements (AI, Biotech, Fintech), favorable economic conditions (low interest rates), and supportive government policies (tax incentives for investment) are major drivers. The increasing prevalence of disruptive technologies and the growth of the digital economy are accelerating VC investments.

Challenges: Regulatory uncertainty, intense competition among VC firms, and macroeconomic instability (e.g., inflation, recession) pose significant challenges. Supply chain disruptions can negatively impact portfolio companies, affecting returns on investment. The impact of these challenges can be quantified by looking at decreased investment rounds or decreased valuations in certain sectors.

Growth Drivers in the Venture Capital Industry Market

The relentless pace of technological innovation across a multitude of sectors continues to serve as an undeniable primary engine for market growth. The transformative potential of artificial intelligence and its applications, the rapidly evolving landscape of the metaverse and its associated technologies, and the urgent, growing global demand for sustainable and climate-friendly solutions are collectively creating novel and highly attractive investment avenues. Complementing these technological shifts, a backdrop of generally favorable economic conditions, coupled with proactive government policies and incentives designed to stimulate venture capital investment, further fortifies market expansion. The strategic global expansion into burgeoning emerging markets, characterized by their high growth potential and unmet market needs, also plays a significant role in contributing to the overall robust growth of the venture capital industry.

Challenges Impacting Venture Capital Industry Growth

Geopolitical instability, economic downturns, and regulatory hurdles significantly impact investment decisions and the overall growth trajectory of the VC industry. Increased competition among VC firms for promising startups intensifies the pressure to secure successful investments. Furthermore, supply chain disruptions can impede the progress of portfolio companies, potentially leading to decreased returns on investment.

Key Players Shaping the Venture Capital Industry Market

- Tiger Global Management

- New Enterprise Associates (NEA)

- Sequoia Capital

- DST Global

- IDG Capital

- Index Ventures

- Healthcare Royalty Partners

- GGV Capital

- Nanjing Zijin Investment

- Greylock Partners

- Note: This list is not exhaustive and represents a selection of prominent firms.

Significant Venture Capital Industry Milestones

- Q4 2020: VC investment in Europe reached a record USD 14.3 Billion across 1,192 deals, surpassing the previous quarter. The Americas accounted for USD 41 billion in VC investment during the same period.

- 2022: IDG Capital Vietnam's investment in METAIN signaled a significant move into the NFT-powered real estate market, highlighting the transformative potential of blockchain technology in the real estate sector. This investment demonstrates a broader trend of Venture Capital firms exploring innovative applications of new technologies.

Future Outlook for Venture Capital Industry Market

The Venture Capital industry is poised for continued growth, driven by ongoing technological innovation and increasing demand for funding from startups across various sectors. Strategic partnerships between VC firms and corporate investors are anticipated to increase, further fueling market expansion. The emergence of new technologies and evolving investment strategies present significant opportunities for growth and innovation within the industry, promising a dynamic and transformative future.

Venture Capital Industry Segmentation

-

1. Type

- 1.1. Local Investors

- 1.2. International Investors

-

2. Industry

- 2.1. Real Estate

- 2.2. Financial Services

- 2.3. Food & Beverages

- 2.4. Healthcare

- 2.5. Transport & Logistics

- 2.6. IT & ITeS

- 2.7. Education

- 2.8. Other Industries

Venture Capital Industry Segmentation By Geography

- 1. North America

- 2. Latin America

- 3. Europe

- 4. Asia Pacific

- 5. Middle East and Africa

Venture Capital Industry Regional Market Share

Geographic Coverage of Venture Capital Industry

Venture Capital Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Local Investors

- 5.1.2. International Investors

- 5.2. Market Analysis, Insights and Forecast - by Industry

- 5.2.1. Real Estate

- 5.2.2. Financial Services

- 5.2.3. Food & Beverages

- 5.2.4. Healthcare

- 5.2.5. Transport & Logistics

- 5.2.6. IT & ITeS

- 5.2.7. Education

- 5.2.8. Other Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Latin America

- 5.3.3. Europe

- 5.3.4. Asia Pacific

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Venture Capital Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Local Investors

- 6.1.2. International Investors

- 6.2. Market Analysis, Insights and Forecast - by Industry

- 6.2.1. Real Estate

- 6.2.2. Financial Services

- 6.2.3. Food & Beverages

- 6.2.4. Healthcare

- 6.2.5. Transport & Logistics

- 6.2.6. IT & ITeS

- 6.2.7. Education

- 6.2.8. Other Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Local Investors

- 7.1.2. International Investors

- 7.2. Market Analysis, Insights and Forecast - by Industry

- 7.2.1. Real Estate

- 7.2.2. Financial Services

- 7.2.3. Food & Beverages

- 7.2.4. Healthcare

- 7.2.5. Transport & Logistics

- 7.2.6. IT & ITeS

- 7.2.7. Education

- 7.2.8. Other Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Latin America Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Local Investors

- 8.1.2. International Investors

- 8.2. Market Analysis, Insights and Forecast - by Industry

- 8.2.1. Real Estate

- 8.2.2. Financial Services

- 8.2.3. Food & Beverages

- 8.2.4. Healthcare

- 8.2.5. Transport & Logistics

- 8.2.6. IT & ITeS

- 8.2.7. Education

- 8.2.8. Other Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Local Investors

- 9.1.2. International Investors

- 9.2. Market Analysis, Insights and Forecast - by Industry

- 9.2.1. Real Estate

- 9.2.2. Financial Services

- 9.2.3. Food & Beverages

- 9.2.4. Healthcare

- 9.2.5. Transport & Logistics

- 9.2.6. IT & ITeS

- 9.2.7. Education

- 9.2.8. Other Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Local Investors

- 10.1.2. International Investors

- 10.2. Market Analysis, Insights and Forecast - by Industry

- 10.2.1. Real Estate

- 10.2.2. Financial Services

- 10.2.3. Food & Beverages

- 10.2.4. Healthcare

- 10.2.5. Transport & Logistics

- 10.2.6. IT & ITeS

- 10.2.7. Education

- 10.2.8. Other Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Local Investors

- 11.1.2. International Investors

- 11.2. Market Analysis, Insights and Forecast - by Industry

- 11.2.1. Real Estate

- 11.2.2. Financial Services

- 11.2.3. Food & Beverages

- 11.2.4. Healthcare

- 11.2.5. Transport & Logistics

- 11.2.6. IT & ITeS

- 11.2.7. Education

- 11.2.8. Other Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Tiger Global Management

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 New Enterprises Associates

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sequoia Capital

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DST Global

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IDG Capital

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Index Ventures

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Healthcare Royalty Partners

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GGV Capital

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nanjing Zijin Investment

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Greylock Partners**List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Tiger Global Management

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Venture Capital Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 5: North America Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 6: North America Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Latin America Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Latin America Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Latin America Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 11: Latin America Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 12: Latin America Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Latin America Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 17: Europe Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 18: Europe Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Asia Pacific Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Asia Pacific Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Asia Pacific Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 23: Asia Pacific Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 24: Asia Pacific Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 29: Middle East and Africa Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 30: Middle East and Africa Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 3: Global Venture Capital Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 6: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 9: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 12: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 15: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 18: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Venture Capital Industry?

The projected CAGR is approximately 16.68%.

2. Which companies are prominent players in the Venture Capital Industry?

Key companies in the market include Tiger Global Management, New Enterprises Associates, Sequoia Capital, DST Global, IDG Capital, Index Ventures, Healthcare Royalty Partners, GGV Capital, Nanjing Zijin Investment, Greylock Partners**List Not Exhaustive.

3. What are the main segments of the Venture Capital Industry?

The market segments include Type, Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 396.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Distribution of Start-Ups Witnessing Venture Capital Industry Globally.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In 2022, IDG Capital Vietnam Confirms Investment in METAIN to Lead NFT-Empowered Real Estate Trend in Vietnam. IDG Capital also shows its ambition to lead the NFT Real estate trend and reveals its plan to proactively engage with global investors to attract investment into the Vietnam real estate market. With the high security, instantaneous settlement, transparent, seamless transaction process, blockchain, smart contract, and NFT (Non-fungible token) technology is transforming the real estate industry and will become the key trend in the next decades.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Venture Capital Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Venture Capital Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Venture Capital Industry?

To stay informed about further developments, trends, and reports in the Venture Capital Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence