Key Insights

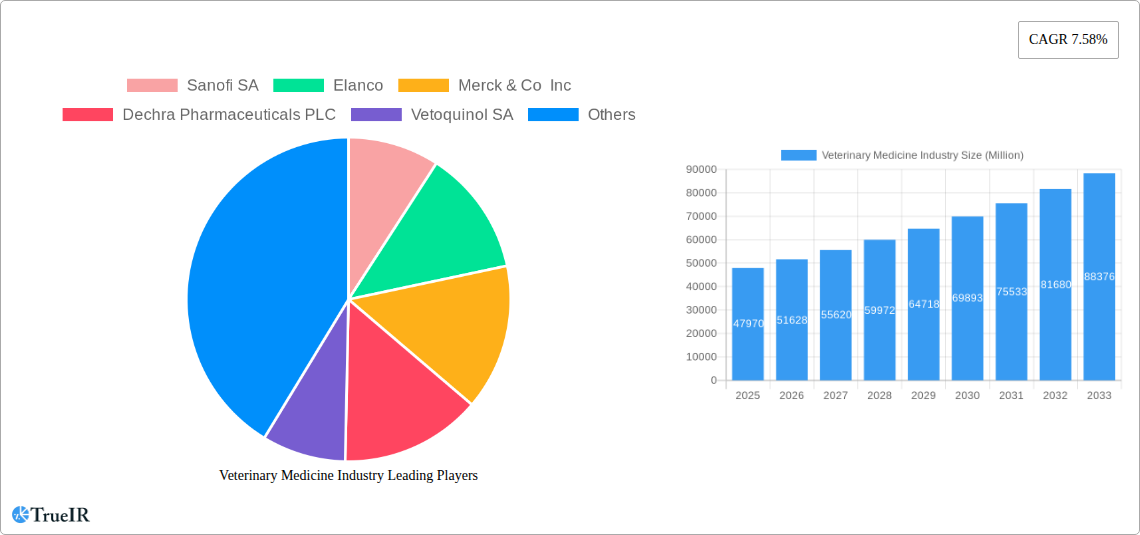

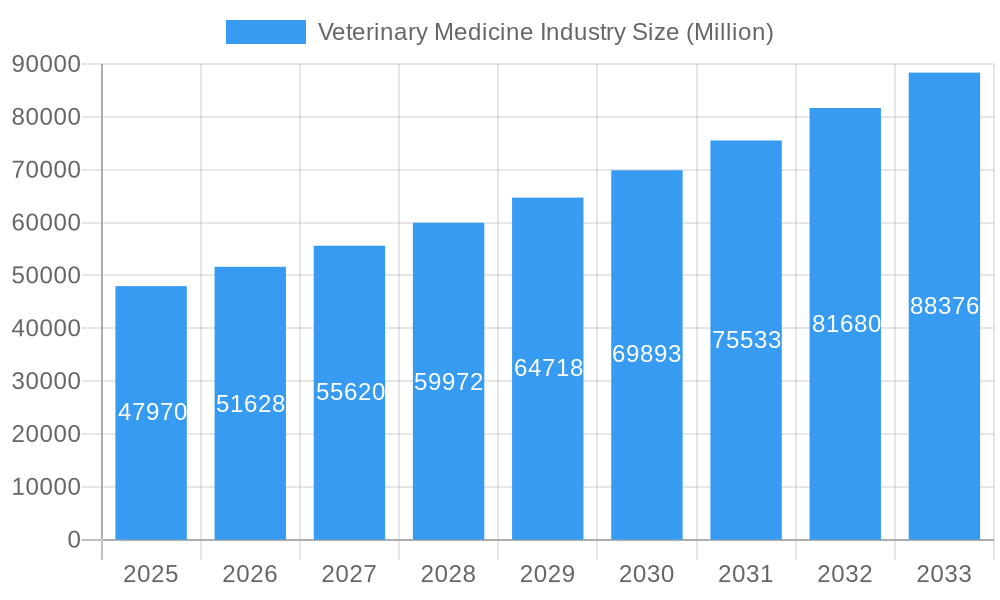

The global veterinary medicine market, valued at $47.97 billion in 2025, is projected to experience robust growth, driven by several key factors. Increasing pet ownership worldwide, coupled with rising humanization of pets and a greater willingness to invest in their healthcare, significantly fuels market expansion. Advances in veterinary diagnostics and therapeutics, including the development of innovative drugs and vaccines for both companion and livestock animals, contribute to market growth. Furthermore, the growing prevalence of zoonotic diseases (diseases transmissible between animals and humans) necessitates enhanced animal health surveillance and proactive veterinary interventions, stimulating market demand. The increasing adoption of preventative healthcare measures, such as vaccinations and regular check-ups, further bolsters market expansion. The market is segmented by animal type (companion animals and livestock) and product type (drugs, vaccines, and medicated feed additives), with companion animal medicine holding a significant share. Major players, including Sanofi SA, Elanco, Merck & Co Inc, and Zoetis, dominate the market, competing through product innovation and strategic partnerships. Geographic distribution shows a strong presence in North America and Europe, although the Asia-Pacific region is anticipated to witness considerable growth in the coming years due to expanding economies and increasing pet ownership.

Veterinary Medicine Industry Market Size (In Billion)

The market's 7.58% CAGR suggests continued expansion through 2033. However, challenges remain, including stringent regulatory approvals for new drugs and vaccines, fluctuating raw material prices, and potential economic downturns impacting consumer spending on veterinary care. Furthermore, the uneven distribution of veterinary resources across regions, particularly in developing countries, poses a barrier to market penetration. Nevertheless, the long-term outlook for the veterinary medicine market remains positive, driven by consistent technological advancements, heightened awareness of animal welfare, and a growing demand for high-quality veterinary services across the globe. Strategic collaborations between pharmaceutical companies and veterinary practices will play a crucial role in delivering innovative and accessible solutions to address the evolving needs of the animal health sector.

Veterinary Medicine Industry Company Market Share

Veterinary Medicine Industry Market Report: A Comprehensive Forecast (2019-2033)

This in-depth report provides a comprehensive analysis of the Veterinary Medicine industry, projecting a market valued at $XX Million by 2033. The study period covers 2019-2033, with 2025 serving as the base and estimated year. The forecast period spans 2025-2033, while the historical period encompasses 2019-2024. This report is essential for investors, industry professionals, and anyone seeking a clear understanding of this rapidly evolving market.

Veterinary Medicine Industry Market Structure & Competitive Landscape

The global veterinary medicine market exhibits a moderately concentrated structure, with several multinational corporations holding significant market share. Key players, including Sanofi SA, Elanco, Merck & Co Inc, Dechra Pharmaceuticals PLC, Vetoquinol SA, China Animal Husbandry Co Ltd, Zoetis, Boehringer Ingelheim, Phibro Animal Health Corporation, Virbac, Ceva Animal Health LLC, and Neogen Corporation, compete fiercely, driving innovation and shaping market dynamics. The Herfindahl-Hirschman Index (HHI) for the market is estimated at XX, indicating a moderately concentrated landscape.

- Innovation Drivers: The market is driven by continuous innovation in drug delivery systems, diagnostic tools, and therapeutic approaches. The development of novel vaccines and targeted therapies is a key growth driver.

- Regulatory Impacts: Stringent regulatory approvals and evolving safety standards influence product development and market entry. Changes in regulatory landscapes across different regions significantly impact market access.

- Product Substitutes: The availability of generic drugs and alternative treatment options creates competitive pressure, impacting pricing strategies and market share.

- End-User Segmentation: The market is segmented by animal type (companion animals, livestock animals) and product type (drugs, vaccines, medicated feed additives). Companion animals represent a larger market segment.

- M&A Trends: Consolidation through mergers and acquisitions (M&A) is a prominent feature, with an estimated XX Million in M&A volume during the historical period (2019-2024). This trend reflects the industry's pursuit of economies of scale and broader market reach.

Veterinary Medicine Industry Market Trends & Opportunities

The global veterinary medicine market is experiencing robust growth, projected to achieve a CAGR of XX% during the forecast period (2025-2033). This growth is propelled by several factors, including increasing pet ownership worldwide, rising awareness of animal health, the growing demand for advanced diagnostics and treatments, and the expansion of the livestock sector. Technological advancements, such as the integration of AI and big data analytics in diagnostics and treatment, are reshaping the market landscape. The increasing prevalence of zoonotic diseases, emphasizing the interconnectedness of animal and human health, creates significant opportunities for preventative measures and treatments. Consumer preference shifts toward premium pet care products and services contribute to the higher-value segment's growth. Furthermore, the competitive landscape is characterized by intense R&D efforts to develop innovative products and personalized animal healthcare solutions, leading to market differentiation. Market penetration rates for specific products, particularly in emerging economies, remain substantial, indicating significant growth potential.

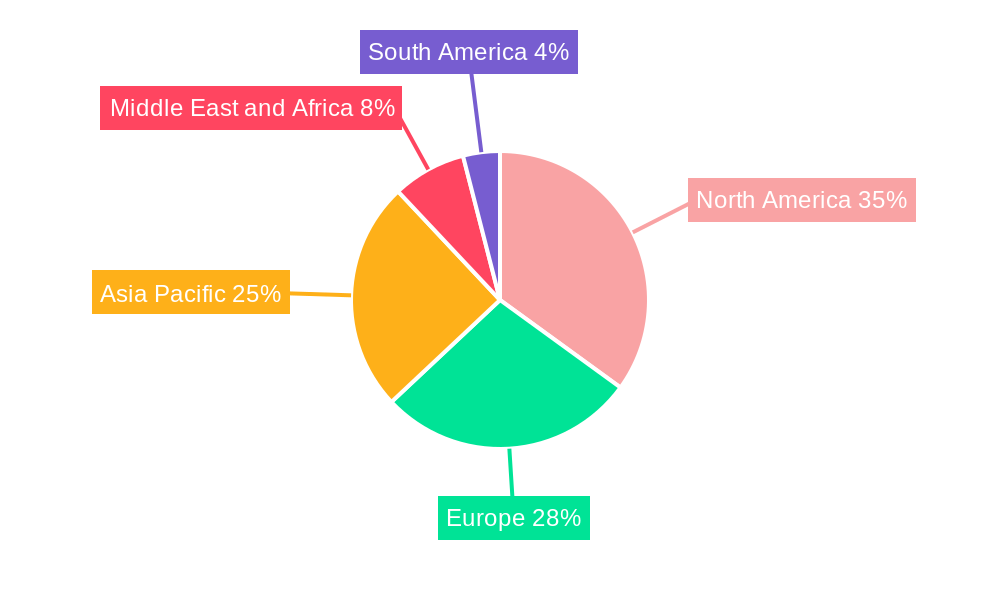

Dominant Markets & Segments in Veterinary Medicine Industry

The North American market currently holds the dominant position in the global veterinary medicine market, driven by high pet ownership rates, advanced veterinary infrastructure, and favorable regulatory environments. The companion animal segment outperforms the livestock segment due to higher disposable income and increased human-animal bond. Within the product type segments, drugs account for the largest market share followed by Vaccines, primarily because of the rising incidence of various infectious diseases among animals.

Key Growth Drivers:

- High Pet Ownership Rates: Increasing pet ownership globally, especially in developed nations, fuels demand.

- Rising Veterinary Infrastructure: Expanding veterinary clinics and hospitals enhance accessibility to healthcare services.

- Favorable Regulatory Environment: Supportive government policies and streamlined approval processes accelerate market growth.

- Increased Spending on Pet Healthcare: Pet owners are increasingly willing to invest in advanced veterinary treatments.

Market Dominance Analysis:

The significant market share of North America and the companion animal segment reflects higher per capita income and pet ownership. The drug segment's leading position stems from the wide range of animal health issues requiring medicinal intervention.

Veterinary Medicine Industry Product Analysis

Technological advancements are driving significant innovation in veterinary medicine products. Advanced diagnostic tools like advanced imaging systems and molecular diagnostics improve disease detection. Targeted drug therapies and customized vaccines are tailored to specific animal breeds and disease profiles. Novel drug delivery systems ensure effective and convenient administration, resulting in better therapeutic outcomes. The market is evolving to incorporate data-driven insights, personalized medicine approaches, and sophisticated disease management strategies.

Key Drivers, Barriers & Challenges in Veterinary Medicine Industry

Key Drivers:

- Technological Advancements: Innovations in diagnostics, therapeutics, and drug delivery systems drive efficiency and efficacy.

- Rising Pet Ownership: Growing pet ownership globally increases demand for veterinary products and services.

- Government Initiatives: supportive regulations and funding enhance R&D and market expansion.

Challenges & Restraints:

- Stringent Regulatory Approvals: Lengthy and complex regulatory processes increase product development costs and timelines. This is estimated to delay market entry by an average of XX months.

- Supply Chain Disruptions: Global events can disrupt the supply of raw materials and finished products, impacting market stability.

- High Research & Development Costs: The development of novel veterinary products requires substantial investment, potentially limiting smaller players' participation.

Growth Drivers in the Veterinary Medicine Industry Market

The veterinary medicine market's growth is fueled by increasing pet humanization, technological advancements leading to better diagnostics and treatment options, rising disposable incomes globally, supportive government regulations, and a growing awareness of animal welfare and preventive healthcare. These factors collectively contribute to the expanding market size and value.

Challenges Impacting Veterinary Medicine Industry Growth

The industry faces challenges including stringent regulatory approvals, fluctuating raw material prices impacting product costs, and intense competition among established players and emerging businesses. Supply chain vulnerabilities and increasing R&D investment needs further pose hurdles to market expansion.

Key Players Shaping the Veterinary Medicine Industry Market

- Sanofi SA

- Elanco

- Merck & Co Inc

- Dechra Pharmaceuticals PLC

- Vetoquinol SA

- China Animal Husbandry Co Ltd

- Zoetis

- Boehringer Ingelheim

- Phibro Animal Health Corporation

- Virbac

- Ceva Animal Health LLC

- Neogen Corporation

Significant Veterinary Medicine Industry Milestones

- June 2022: Launch of Anocovax, India's first homegrown COVID-19 animal vaccine.

- June 2022: US FDA approval of Vetmedin-CA1 for delaying congestive heart failure in dogs.

- September 2022: US FDA approval of Simplera Otic Solution for canine otitis externa.

- September 2022: US FDA approval of SpectoGard, a generic spectinomycin sulfate solution for bovine respiratory diseases.

Future Outlook for Veterinary Medicine Industry Market

The veterinary medicine market is poised for continued expansion, driven by increasing pet ownership, rising demand for advanced diagnostics, and the development of innovative therapies. Strategic partnerships, investments in R&D, and expansion into emerging markets will further fuel market growth, presenting significant opportunities for established and emerging players. The market is expected to see continued consolidation and a greater focus on personalized medicine approaches.

Veterinary Medicine Industry Segmentation

-

1. Product Type

-

1.1. Drugs

- 1.1.1. Anti-infectives

- 1.1.2. Anti-inflammatory

- 1.1.3. Parasiticides

- 1.1.4. Other Drugs

-

1.2. Vaccines

- 1.2.1. Inactive Vaccines

- 1.2.2. Attenuated Vaccines

- 1.2.3. Recombinant Vaccines

- 1.2.4. Other Vaccines

-

1.3. Medicated Feed Additives

- 1.3.1. Aminoacids

- 1.3.2. Antibiotics

- 1.3.3. Other Medicated Feed Additives

-

1.1. Drugs

-

2. Animal Type

-

2.1. Companion Animals

- 2.1.1. Dogs

- 2.1.2. Cats

- 2.1.3. Other Companion Animals

-

2.2. Livestock Animals

- 2.2.1. Cattle

- 2.2.2. Poultry

- 2.2.3. Swine

- 2.2.4. Sheep

- 2.2.5. Other Livestock Animals

-

2.1. Companion Animals

Veterinary Medicine Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Medicine Industry Regional Market Share

Geographic Coverage of Veterinary Medicine Industry

Veterinary Medicine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Drugs

- 5.1.1.1. Anti-infectives

- 5.1.1.2. Anti-inflammatory

- 5.1.1.3. Parasiticides

- 5.1.1.4. Other Drugs

- 5.1.2. Vaccines

- 5.1.2.1. Inactive Vaccines

- 5.1.2.2. Attenuated Vaccines

- 5.1.2.3. Recombinant Vaccines

- 5.1.2.4. Other Vaccines

- 5.1.3. Medicated Feed Additives

- 5.1.3.1. Aminoacids

- 5.1.3.2. Antibiotics

- 5.1.3.3. Other Medicated Feed Additives

- 5.1.1. Drugs

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Companion Animals

- 5.2.1.1. Dogs

- 5.2.1.2. Cats

- 5.2.1.3. Other Companion Animals

- 5.2.2. Livestock Animals

- 5.2.2.1. Cattle

- 5.2.2.2. Poultry

- 5.2.2.3. Swine

- 5.2.2.4. Sheep

- 5.2.2.5. Other Livestock Animals

- 5.2.1. Companion Animals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Veterinary Medicine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Drugs

- 6.1.1.1. Anti-infectives

- 6.1.1.2. Anti-inflammatory

- 6.1.1.3. Parasiticides

- 6.1.1.4. Other Drugs

- 6.1.2. Vaccines

- 6.1.2.1. Inactive Vaccines

- 6.1.2.2. Attenuated Vaccines

- 6.1.2.3. Recombinant Vaccines

- 6.1.2.4. Other Vaccines

- 6.1.3. Medicated Feed Additives

- 6.1.3.1. Aminoacids

- 6.1.3.2. Antibiotics

- 6.1.3.3. Other Medicated Feed Additives

- 6.1.1. Drugs

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Companion Animals

- 6.2.1.1. Dogs

- 6.2.1.2. Cats

- 6.2.1.3. Other Companion Animals

- 6.2.2. Livestock Animals

- 6.2.2.1. Cattle

- 6.2.2.2. Poultry

- 6.2.2.3. Swine

- 6.2.2.4. Sheep

- 6.2.2.5. Other Livestock Animals

- 6.2.1. Companion Animals

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Veterinary Medicine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Drugs

- 7.1.1.1. Anti-infectives

- 7.1.1.2. Anti-inflammatory

- 7.1.1.3. Parasiticides

- 7.1.1.4. Other Drugs

- 7.1.2. Vaccines

- 7.1.2.1. Inactive Vaccines

- 7.1.2.2. Attenuated Vaccines

- 7.1.2.3. Recombinant Vaccines

- 7.1.2.4. Other Vaccines

- 7.1.3. Medicated Feed Additives

- 7.1.3.1. Aminoacids

- 7.1.3.2. Antibiotics

- 7.1.3.3. Other Medicated Feed Additives

- 7.1.1. Drugs

- 7.2. Market Analysis, Insights and Forecast - by Animal Type

- 7.2.1. Companion Animals

- 7.2.1.1. Dogs

- 7.2.1.2. Cats

- 7.2.1.3. Other Companion Animals

- 7.2.2. Livestock Animals

- 7.2.2.1. Cattle

- 7.2.2.2. Poultry

- 7.2.2.3. Swine

- 7.2.2.4. Sheep

- 7.2.2.5. Other Livestock Animals

- 7.2.1. Companion Animals

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Veterinary Medicine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Drugs

- 8.1.1.1. Anti-infectives

- 8.1.1.2. Anti-inflammatory

- 8.1.1.3. Parasiticides

- 8.1.1.4. Other Drugs

- 8.1.2. Vaccines

- 8.1.2.1. Inactive Vaccines

- 8.1.2.2. Attenuated Vaccines

- 8.1.2.3. Recombinant Vaccines

- 8.1.2.4. Other Vaccines

- 8.1.3. Medicated Feed Additives

- 8.1.3.1. Aminoacids

- 8.1.3.2. Antibiotics

- 8.1.3.3. Other Medicated Feed Additives

- 8.1.1. Drugs

- 8.2. Market Analysis, Insights and Forecast - by Animal Type

- 8.2.1. Companion Animals

- 8.2.1.1. Dogs

- 8.2.1.2. Cats

- 8.2.1.3. Other Companion Animals

- 8.2.2. Livestock Animals

- 8.2.2.1. Cattle

- 8.2.2.2. Poultry

- 8.2.2.3. Swine

- 8.2.2.4. Sheep

- 8.2.2.5. Other Livestock Animals

- 8.2.1. Companion Animals

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Veterinary Medicine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Drugs

- 9.1.1.1. Anti-infectives

- 9.1.1.2. Anti-inflammatory

- 9.1.1.3. Parasiticides

- 9.1.1.4. Other Drugs

- 9.1.2. Vaccines

- 9.1.2.1. Inactive Vaccines

- 9.1.2.2. Attenuated Vaccines

- 9.1.2.3. Recombinant Vaccines

- 9.1.2.4. Other Vaccines

- 9.1.3. Medicated Feed Additives

- 9.1.3.1. Aminoacids

- 9.1.3.2. Antibiotics

- 9.1.3.3. Other Medicated Feed Additives

- 9.1.1. Drugs

- 9.2. Market Analysis, Insights and Forecast - by Animal Type

- 9.2.1. Companion Animals

- 9.2.1.1. Dogs

- 9.2.1.2. Cats

- 9.2.1.3. Other Companion Animals

- 9.2.2. Livestock Animals

- 9.2.2.1. Cattle

- 9.2.2.2. Poultry

- 9.2.2.3. Swine

- 9.2.2.4. Sheep

- 9.2.2.5. Other Livestock Animals

- 9.2.1. Companion Animals

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Veterinary Medicine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Drugs

- 10.1.1.1. Anti-infectives

- 10.1.1.2. Anti-inflammatory

- 10.1.1.3. Parasiticides

- 10.1.1.4. Other Drugs

- 10.1.2. Vaccines

- 10.1.2.1. Inactive Vaccines

- 10.1.2.2. Attenuated Vaccines

- 10.1.2.3. Recombinant Vaccines

- 10.1.2.4. Other Vaccines

- 10.1.3. Medicated Feed Additives

- 10.1.3.1. Aminoacids

- 10.1.3.2. Antibiotics

- 10.1.3.3. Other Medicated Feed Additives

- 10.1.1. Drugs

- 10.2. Market Analysis, Insights and Forecast - by Animal Type

- 10.2.1. Companion Animals

- 10.2.1.1. Dogs

- 10.2.1.2. Cats

- 10.2.1.3. Other Companion Animals

- 10.2.2. Livestock Animals

- 10.2.2.1. Cattle

- 10.2.2.2. Poultry

- 10.2.2.3. Swine

- 10.2.2.4. Sheep

- 10.2.2.5. Other Livestock Animals

- 10.2.1. Companion Animals

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Veterinary Medicine Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Drugs

- 11.1.1.1. Anti-infectives

- 11.1.1.2. Anti-inflammatory

- 11.1.1.3. Parasiticides

- 11.1.1.4. Other Drugs

- 11.1.2. Vaccines

- 11.1.2.1. Inactive Vaccines

- 11.1.2.2. Attenuated Vaccines

- 11.1.2.3. Recombinant Vaccines

- 11.1.2.4. Other Vaccines

- 11.1.3. Medicated Feed Additives

- 11.1.3.1. Aminoacids

- 11.1.3.2. Antibiotics

- 11.1.3.3. Other Medicated Feed Additives

- 11.1.1. Drugs

- 11.2. Market Analysis, Insights and Forecast - by Animal Type

- 11.2.1. Companion Animals

- 11.2.1.1. Dogs

- 11.2.1.2. Cats

- 11.2.1.3. Other Companion Animals

- 11.2.2. Livestock Animals

- 11.2.2.1. Cattle

- 11.2.2.2. Poultry

- 11.2.2.3. Swine

- 11.2.2.4. Sheep

- 11.2.2.5. Other Livestock Animals

- 11.2.1. Companion Animals

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sanofi SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Elanco

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Merck & Co Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Dechra Pharmaceuticals PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vetoquinol SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 China Animal Husbandry Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Zoetis*List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Boehringer Ingelheim

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Phibro Animal Health Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Virbac

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ceva Animal Health LLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Neogen Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Sanofi SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Veterinary Medicine Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Veterinary Medicine Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 3: North America Veterinary Medicine Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Veterinary Medicine Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 5: North America Veterinary Medicine Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 6: North America Veterinary Medicine Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Veterinary Medicine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Veterinary Medicine Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 9: Europe Veterinary Medicine Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: Europe Veterinary Medicine Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 11: Europe Veterinary Medicine Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 12: Europe Veterinary Medicine Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Veterinary Medicine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Veterinary Medicine Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 15: Asia Pacific Veterinary Medicine Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Asia Pacific Veterinary Medicine Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 17: Asia Pacific Veterinary Medicine Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 18: Asia Pacific Veterinary Medicine Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Veterinary Medicine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Veterinary Medicine Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 21: Middle East and Africa Veterinary Medicine Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Middle East and Africa Veterinary Medicine Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 23: Middle East and Africa Veterinary Medicine Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Middle East and Africa Veterinary Medicine Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Veterinary Medicine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Veterinary Medicine Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: South America Veterinary Medicine Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: South America Veterinary Medicine Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 29: South America Veterinary Medicine Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 30: South America Veterinary Medicine Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Veterinary Medicine Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 3: Global Veterinary Medicine Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 6: Global Veterinary Medicine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 11: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 12: Global Veterinary Medicine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 20: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 21: Global Veterinary Medicine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 29: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 30: Global Veterinary Medicine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Veterinary Medicine Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 35: Global Veterinary Medicine Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 36: Global Veterinary Medicine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Veterinary Medicine Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Medicine Industry?

The projected CAGR is approximately 7.58%.

2. Which companies are prominent players in the Veterinary Medicine Industry?

Key companies in the market include Sanofi SA, Elanco, Merck & Co Inc, Dechra Pharmaceuticals PLC, Vetoquinol SA, China Animal Husbandry Co Ltd, Zoetis*List Not Exhaustive, Boehringer Ingelheim, Phibro Animal Health Corporation, Virbac, Ceva Animal Health LLC, Neogen Corporation.

3. What are the main segments of the Veterinary Medicine Industry?

The market segments include Product Type, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 47.97 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Burden of Chronic Disease Conditions in Animals. Coupled with the Increasing Adoption of Animals; Increase in Drug Preferences by Pet and Poultry Farm Owners; Increased Demand for Meat and Animal-based Products in Agriculture and Human Healthcare.

6. What are the notable trends driving market growth?

Dogs Segment is Expected to Hold A Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Costs Associated with Animal Healthcare; Lack of Awareness about Animal Health in the Emerging Nations.

8. Can you provide examples of recent developments in the market?

September 2022: The US FDA approved SpectoGard, the first generic spectinomycin sulfate injectable solution for the treatment of bovine respiratory diseases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Medicine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Medicine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Medicine Industry?

To stay informed about further developments, trends, and reports in the Veterinary Medicine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence