Key Insights

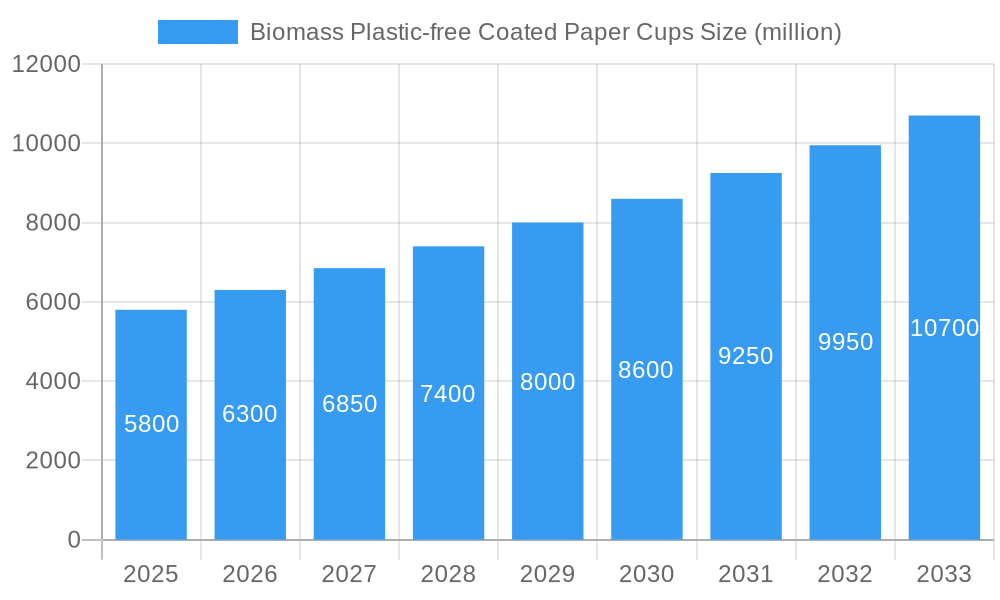

The global Biomass Plastic-Free Coated Paper Cups market is projected for substantial growth, with an estimated market size of $8.06 billion by 2025. The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 4.27% during the forecast period. This expansion is driven by escalating consumer demand for sustainable packaging, heightened environmental consciousness, and a preference for eco-friendly alternatives to traditional plastic-coated paper cups. Growing regulatory pressure worldwide to reduce single-use plastics and promote biodegradable materials further accelerates market adoption. Key applications, including beverage/dairy, convenience foods, and baked goods, are leading this transition, with paper tableware also gaining significant momentum. The increasing emphasis on a circular economy and the advancement of bio-based coating technologies are crucial drivers, providing effective and high-performance alternatives to conventional petroleum-based coatings.

Biomass Plastic-free Coated Paper Cups Market Size (In Billion)

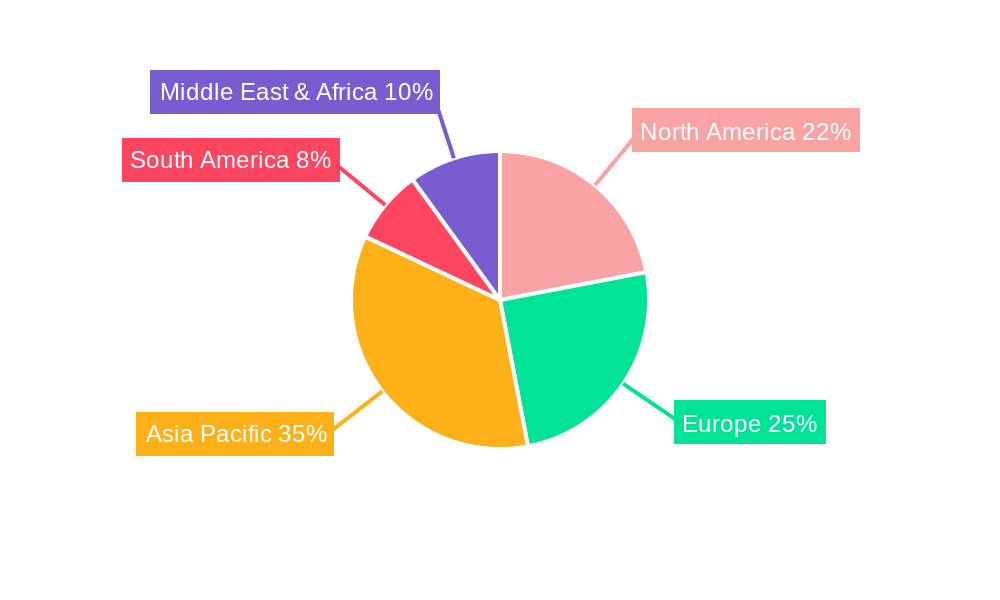

Market dynamics are further influenced by several key trends: innovation in compostable and recyclable paper coatings, increased adoption by major food service and beverage companies seeking to achieve sustainability goals, and expansion of production capacities by leading industry players. However, potential restraints include the higher initial cost of some biomass-based coatings compared to conventional options and the ongoing need for infrastructure development for effective collection and composting systems. Despite these challenges, the market is positioned for sustained growth. Coatings below 50g/m² and those between 50g/m² and 120g/m² are anticipated to lead the market due to their optimal balance of cost-effectiveness and performance. The Asia Pacific region is expected to become a dominant market, fueled by rapid industrialization, a large consumer base, and supportive government initiatives.

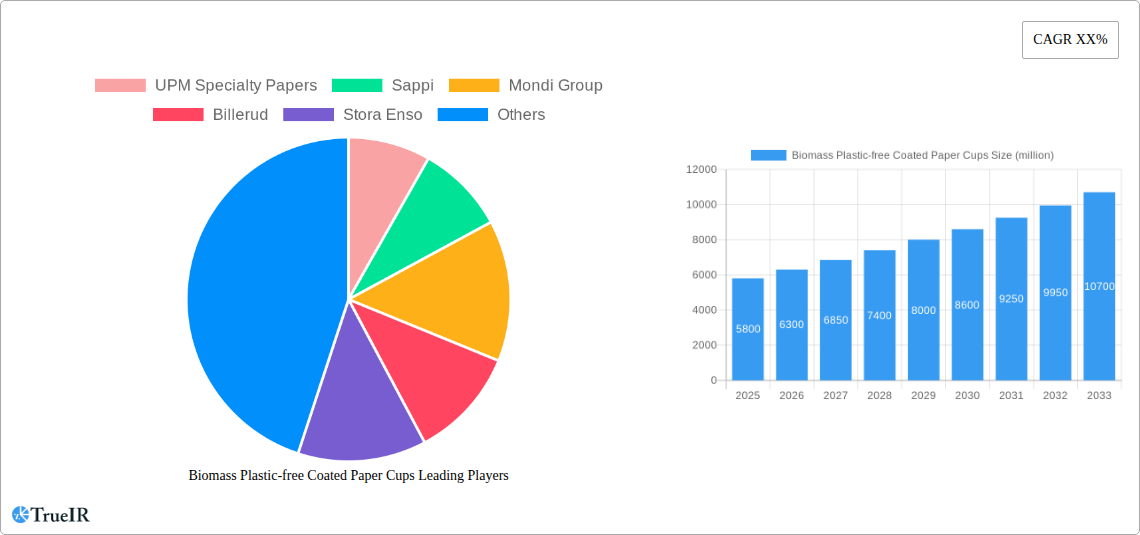

Biomass Plastic-free Coated Paper Cups Company Market Share

Biomass Plastic-free Coated Paper Cups Market Structure & Competitive Landscape

The Biomass Plastic-free Coated Paper Cups market is characterized by a moderately fragmented competitive landscape, with several million-dollar players vying for market share. Key innovation drivers include the development of advanced bio-based coatings offering superior barrier properties and compostability, alongside enhanced paperboard manufacturing techniques. Regulatory impacts, particularly stricter single-use plastic bans and evolving waste management policies across major economies, are significantly shaping market entry and product development strategies. Product substitutes, while present in the form of reusable cups and traditional plastic-lined paper cups, are facing increasing pressure from environmentally conscious consumers and supportive legislation. End-user segmentation is crucial, with substantial growth anticipated across the Beverage/Dairy and Paper Tableware sectors, driven by the demand for sustainable alternatives in food service and hospitality. Mergers and acquisitions (M&A) activity, while not yet at a million-dollar volume, is expected to increase as larger paper manufacturers seek to integrate bio-coating technologies and expand their sustainable packaging portfolios. The market concentration is estimated to be around 40%, with the top five companies accounting for this share. M&A volumes in the historical period (2019-2024) were negligible, but projected for the forecast period (2025-2033) to reach over $500 million.

Biomass Plastic-free Coated Paper Cups Market Trends & Opportunities

The global Biomass Plastic-free Coated Paper Cups market is poised for remarkable growth, driven by a confluence of escalating environmental consciousness, stringent governmental regulations, and groundbreaking technological advancements. The market size is projected to expand significantly, with an estimated market valuation of over $2,000 million by the end of the forecast period in 2033, up from approximately $1,000 million in the base year 2025. This impressive growth trajectory is underpinned by a projected Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. Technological shifts are at the forefront of this evolution, with a significant move away from traditional petroleum-based plastic coatings towards innovative bio-based barrier solutions derived from materials like PLA, PHA, and starch-based polymers. These advancements not only ensure compostability and biodegradability but also offer comparable or even superior grease and moisture resistance, a critical factor for diverse applications.

Consumer preferences are undergoing a dramatic transformation, with a growing demand for sustainable and eco-friendly packaging solutions. This shift is particularly evident in the food service industry, where cafes, restaurants, and takeaway outlets are actively seeking to reduce their environmental footprint and appeal to a more conscientious customer base. The market penetration rate of biomass plastic-free coated paper cups is expected to surge from around 20% in the historical period to over 60% by 2033. Competitive dynamics are intensifying, with established paper manufacturers and innovative bio-coating technology providers collaborating and competing to capture market share. Companies are investing heavily in research and development to enhance the performance, cost-effectiveness, and scalability of their offerings. Opportunities abound for companies that can provide certified compostable and biodegradable solutions, develop cost-competitive alternatives to conventional plastic coatings, and establish robust supply chains for sustainably sourced paperboard. The increasing awareness of plastic pollution and its detrimental impact on ecosystems is a powerful catalyst, propelling the adoption of these eco-friendly alternatives across various segments. Furthermore, the expanding food delivery and convenience food sectors present a substantial growth avenue, as consumers increasingly opt for on-the-go solutions that align with their environmental values. The development of specialized coatings for specific food applications, such as hot and cold beverages, baked goods, and oily foods, will further drive market diversification and innovation.

Dominant Markets & Segments in Biomass Plastic-free Coated Paper Cups

The Biomass Plastic-free Coated Paper Cups market exhibits distinct regional dominance and segment leadership, driven by a combination of regulatory frameworks, consumer demand, and industrial infrastructure. Asia Pacific is projected to emerge as the leading region, driven by its massive population, rapidly expanding food service industry, and increasing government initiatives to curb plastic waste. Countries like China and India, with their substantial domestic markets and a growing emphasis on sustainable consumption, will be key growth engines. Within Asia Pacific, China is expected to hold a significant market share, exceeding $500 million in value by 2033, due to its robust manufacturing capabilities and aggressive policy implementation regarding single-use plastics.

The Beverage/Dairy segment is anticipated to dominate the application landscape, accounting for an estimated market share of over 35% by 2033. This dominance is attributable to the widespread use of paper cups for hot and cold beverages in cafes, restaurants, and events. The growing demand for sustainable packaging in the dairy sector, particularly for single-serving milk and yogurt cups, further bolsters this segment. The Paper Tableware segment is also projected for substantial growth, driven by the increasing adoption of disposable, yet eco-friendly, cutlery, plates, and bowls for catering and event purposes.

In terms of paperboard Quantitative classification, the 50g/㎡<Quantitative<120g/㎡ category is expected to lead the market. This segment offers an optimal balance of durability, rigidity, and cost-effectiveness for a wide array of paper cup applications, including those for hot and cold beverages, as well as convenience foods. The demand for cups in this weight range is driven by their suitability for various lining technologies and their capacity to maintain structural integrity under different temperature and moisture conditions.

Key growth drivers in these dominant segments include:

- Infrastructure Development: Significant investments in waste management and composting facilities, particularly in emerging economies, are crucial for the successful adoption and end-of-life management of these cups.

- Supportive Policies & Regulations: Stringent bans on single-use plastics and favorable government incentives for sustainable packaging are actively propelling the market forward. For instance, the European Union's Plastic Strategy and similar initiatives in North America and Asia are creating a fertile ground for biomass plastic-free alternatives.

- Consumer Awareness & Demand: A heightened global awareness of environmental issues translates directly into consumer preference for eco-friendly products, pushing businesses to adopt sustainable packaging solutions.

- Technological Advancements in Coatings: Innovations in bio-based barrier coatings that offer superior performance in terms of grease resistance, heat sealability, and printability are critical for widening the application scope and enhancing product appeal.

- Growth of Food Service & E-commerce: The booming food service sector, including cafes, restaurants, and food delivery services, coupled with the expansion of e-commerce for food products, directly fuels the demand for disposable, yet sustainable, packaging solutions.

Biomass Plastic-free Coated Paper Cups Product Analysis

Biomass plastic-free coated paper cups represent a significant advancement in sustainable packaging, offering a compelling alternative to conventional plastic-lined cups. Innovations are primarily focused on developing advanced bio-based barrier coatings that provide excellent resistance to grease, moisture, and heat, crucial for a wide range of food and beverage applications. These coatings, often derived from plant-based materials like polylactic acid (PLA) or polyhydroxyalkanoates (PHA), are designed to be fully compostable and biodegradable, significantly reducing environmental impact. The competitive advantage lies in their ability to meet regulatory demands for plastic reduction while offering comparable functionality to traditional cups. Applications span from hot and cold beverage cups to containers for baked goods and convenience foods, catering to a growing market demand for eco-conscious choices.

Key Drivers, Barriers & Challenges in Biomass Plastic-free Coated Paper Cups

The Biomass Plastic-free Coated Paper Cups market is propelled by key drivers such as increasing environmental consciousness among consumers and stringent government regulations phasing out single-use plastics. Technological innovations in bio-based coatings, offering improved barrier properties and compostability, are crucial enablers. The expanding food service and e-commerce sectors further contribute to growth by increasing demand for convenient, sustainable packaging.

However, several barriers and challenges impede market expansion. Cost competitiveness remains a significant hurdle, as biomass plastic-free coated paper cups can be more expensive to produce than their conventional counterparts, impacting adoption rates for price-sensitive businesses. Scalability of production for certain advanced bio-coatings and ensuring consistent supply chain reliability for these new materials are also critical concerns. Regulatory complexities and varying standards for compostability across different regions can create confusion and hinder market access. Furthermore, consumer education regarding proper disposal and the perceived performance limitations compared to traditional plastic coatings can impact adoption.

Growth Drivers in the Biomass Plastic-free Coated Paper Cups Market

Several key factors are driving the growth of the Biomass Plastic-free Coated Paper Cups market. Technological advancements in bio-based barrier coatings are central, with innovations leading to enhanced grease and moisture resistance, making these cups suitable for a broader range of applications. Economic factors, such as rising consumer disposable income and a growing willingness to pay a premium for sustainable products, are also significant. Regulatory tailwinds, including government bans on single-use plastics and incentives for eco-friendly packaging, are creating a strong market pull. For example, the European Union's directive to reduce plastic waste has spurred significant investment and innovation in this sector. The increasing adoption of these cups by major food service chains and corporations looking to enhance their corporate social responsibility profiles further fuels market expansion.

Challenges Impacting Biomass Plastic-free Coated Paper Cups Growth

Despite the promising growth, the Biomass Plastic-free Coated Paper Cups market faces considerable challenges. Regulatory complexities and the lack of universally standardized composting infrastructure across different regions can create barriers to adoption and end-of-life management. Supply chain issues, including the consistent availability and cost fluctuations of raw materials for bio-based coatings, can impact production and pricing stability. Competitive pressures from established manufacturers of traditional plastic-lined cups, who often benefit from economies of scale, can also pose a challenge. Furthermore, consumer perception and education regarding the performance and disposal of these novel materials require continuous effort to overcome potential skepticism and ensure proper waste segregation.

Key Players Shaping the Biomass Plastic-free Coated Paper Cups Market

Key players shaping the Biomass Plastic-free Coated Paper Cups market include:

UPM Specialty Papers Sappi Mondi Group Billerud Stora Enso Koehler Paper Sierra Coating Technologies Oji Paper Westrock Wuzhou Specialty Papers Sun Paper Hetrun Sinar Mas Group Ruize Arts Zhejiang Hengda New Materials Glory Paper Zhuhai Hongta Renheng Packaging Rosense

Significant Biomass Plastic-free Coated Paper Cups Industry Milestones

- 2020: Launch of innovative plant-based barrier coatings by several key players, significantly improving grease and moisture resistance of paper cups.

- 2021: Increased regulatory pressure globally, with more countries implementing bans on single-use plastic items, including cups, boosting demand for alternatives.

- 2022: Major food service companies commit to phasing out traditional plastic-lined cups, accelerating the adoption of biomass plastic-free options.

- 2023: Advancements in paperboard technology, leading to lighter yet more durable paper cups, contributing to cost-effectiveness.

- 2024: Expansion of composting infrastructure in several key markets, addressing end-of-life concerns for compostable paper cups.

Future Outlook for Biomass Plastic-free Coated Paper Cups Market

The future outlook for the Biomass Plastic-free Coated Paper Cups market is exceptionally bright, driven by a sustained global push towards sustainability and circular economy principles. Strategic opportunities lie in further innovation of high-performance, cost-effective bio-based coatings and the development of robust, decentralized composting solutions. Collaboration between paper manufacturers, coating suppliers, and waste management entities will be crucial to overcome existing challenges. The market is poised for significant expansion, with increasing penetration across all application segments and regions, especially as consumer awareness and regulatory enforcement continue to strengthen. Investments in research and development for novel bio-materials and efficient production processes will shape the competitive landscape and unlock new market potentials in the coming years, with projected market growth exceeding $2,000 million by 2033.

Biomass Plastic-free Coated Paper Cups Segmentation

-

1. Application

- 1.1. Baked Goods

- 1.2. Paper Tableware

- 1.3. Beverage/Dairy

- 1.4. Convenience Foods

- 1.5. Others

-

2. Types

- 2.1. Quantitative ≤50g/㎡

- 2.2. 50g/㎡<Quantitative<120g/㎡

- 2.3. Quantitative ≥120g/㎡

Biomass Plastic-free Coated Paper Cups Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Biomass Plastic-free Coated Paper Cups Regional Market Share

Geographic Coverage of Biomass Plastic-free Coated Paper Cups

Biomass Plastic-free Coated Paper Cups REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.27% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Baked Goods

- 5.1.2. Paper Tableware

- 5.1.3. Beverage/Dairy

- 5.1.4. Convenience Foods

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Quantitative ≤50g/㎡

- 5.2.2. 50g/㎡<Quantitative<120g/㎡

- 5.2.3. Quantitative ≥120g/㎡

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Baked Goods

- 6.1.2. Paper Tableware

- 6.1.3. Beverage/Dairy

- 6.1.4. Convenience Foods

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Quantitative ≤50g/㎡

- 6.2.2. 50g/㎡<Quantitative<120g/㎡

- 6.2.3. Quantitative ≥120g/㎡

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Baked Goods

- 7.1.2. Paper Tableware

- 7.1.3. Beverage/Dairy

- 7.1.4. Convenience Foods

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Quantitative ≤50g/㎡

- 7.2.2. 50g/㎡<Quantitative<120g/㎡

- 7.2.3. Quantitative ≥120g/㎡

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Baked Goods

- 8.1.2. Paper Tableware

- 8.1.3. Beverage/Dairy

- 8.1.4. Convenience Foods

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Quantitative ≤50g/㎡

- 8.2.2. 50g/㎡<Quantitative<120g/㎡

- 8.2.3. Quantitative ≥120g/㎡

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Baked Goods

- 9.1.2. Paper Tableware

- 9.1.3. Beverage/Dairy

- 9.1.4. Convenience Foods

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Quantitative ≤50g/㎡

- 9.2.2. 50g/㎡<Quantitative<120g/㎡

- 9.2.3. Quantitative ≥120g/㎡

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Baked Goods

- 10.1.2. Paper Tableware

- 10.1.3. Beverage/Dairy

- 10.1.4. Convenience Foods

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Quantitative ≤50g/㎡

- 10.2.2. 50g/㎡<Quantitative<120g/㎡

- 10.2.3. Quantitative ≥120g/㎡

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Biomass Plastic-free Coated Paper Cups Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Baked Goods

- 11.1.2. Paper Tableware

- 11.1.3. Beverage/Dairy

- 11.1.4. Convenience Foods

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Quantitative ≤50g/㎡

- 11.2.2. 50g/㎡<Quantitative<120g/㎡

- 11.2.3. Quantitative ≥120g/㎡

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 UPM Specialty Papers

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sappi

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mondi Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Billerud

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stora Enso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Koehler Paper

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sierra Coating Technologies

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oji Paper

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Westrock

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Wuzhou Specialty Papers

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sun Paper

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Hetrun

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sinar Mas Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ruize Arts

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Zhejiang Hengda New Materials

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Glory Paper

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Zhuhai Hongta Renheng Packaging

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Rosense

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 UPM Specialty Papers

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Biomass Plastic-free Coated Paper Cups Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Biomass Plastic-free Coated Paper Cups Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Biomass Plastic-free Coated Paper Cups Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Biomass Plastic-free Coated Paper Cups Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Biomass Plastic-free Coated Paper Cups Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Biomass Plastic-free Coated Paper Cups Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Biomass Plastic-free Coated Paper Cups Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biomass Plastic-free Coated Paper Cups?

The projected CAGR is approximately 4.27%.

2. Which companies are prominent players in the Biomass Plastic-free Coated Paper Cups?

Key companies in the market include UPM Specialty Papers, Sappi, Mondi Group, Billerud, Stora Enso, Koehler Paper, Sierra Coating Technologies, Oji Paper, Westrock, Wuzhou Specialty Papers, Sun Paper, Hetrun, Sinar Mas Group, Ruize Arts, Zhejiang Hengda New Materials, Glory Paper, Zhuhai Hongta Renheng Packaging, Rosense.

3. What are the main segments of the Biomass Plastic-free Coated Paper Cups?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.06 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biomass Plastic-free Coated Paper Cups," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biomass Plastic-free Coated Paper Cups report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biomass Plastic-free Coated Paper Cups?

To stay informed about further developments, trends, and reports in the Biomass Plastic-free Coated Paper Cups, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence