Key Insights

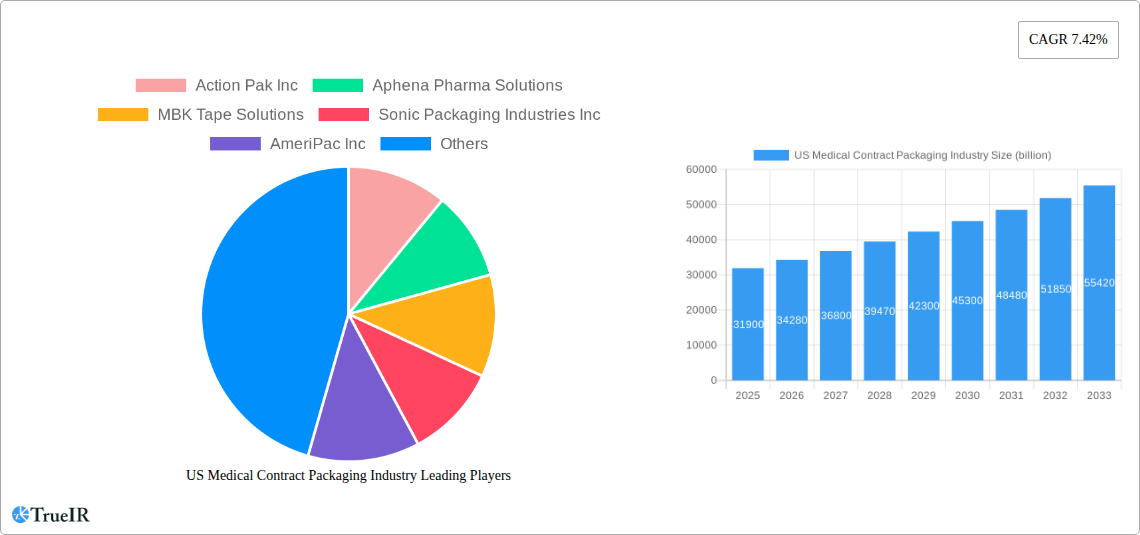

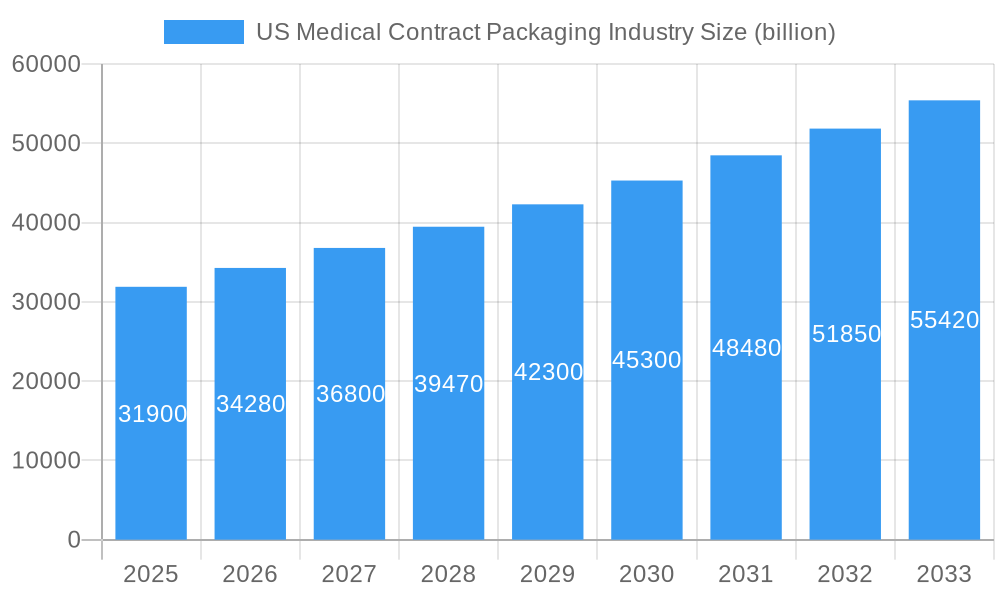

The US medical contract packaging market is poised for significant growth, projected to reach $31.9 billion in 2025 with a robust CAGR of 7.42% through 2033. This expansion is fueled by a confluence of factors, including the increasing outsourcing of packaging services by pharmaceutical and medical device manufacturers to specialized contract organizations. This trend is driven by the need for cost efficiencies, enhanced regulatory compliance, and access to advanced packaging technologies. The growing demand for sterile and tamper-evident packaging solutions, coupled with the expanding healthcare sector and an aging population requiring more medical products, further propels the market forward. Furthermore, the rise in biopharmaceuticals and complex drug delivery systems necessitates specialized packaging expertise, a niche that contract packagers are well-positioned to fill. The market's dynamism is also evident in the diverse range of services and product types, from primary packaging like medical pouches and blister packs to secondary and tertiary solutions, catering to a broad spectrum of industry needs.

US Medical Contract Packaging Industry Market Size (In Billion)

Innovation in materials science and a growing emphasis on sustainability are also shaping the US medical contract packaging landscape. While plastic remains a dominant material due to its versatility and cost-effectiveness, there's a discernible shift towards more eco-friendly alternatives like paper and paperboard, driven by regulatory pressures and increasing consumer awareness. The market is characterized by the presence of established players and emerging companies, all vying for market share through strategic partnerships, acquisitions, and investments in advanced manufacturing capabilities. Restraints such as stringent regulatory hurdles and the high cost of implementing advanced packaging technologies are present but are being navigated by industry leaders through continuous adaptation and investment. The market's trajectory indicates a future where sophisticated, compliant, and increasingly sustainable packaging solutions will be paramount for success in the US medical sector.

US Medical Contract Packaging Industry Company Market Share

This comprehensive report delves into the dynamic US Medical Contract Packaging industry, offering in-depth analysis, market trends, and future outlook. Leveraging high-volume keywords such as "medical contract packaging," "pharmaceutical packaging solutions," "medical device packaging," and "sterile packaging services," this report is designed to provide actionable insights for industry stakeholders, investors, and decision-makers. The study covers the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, building upon historical data from 2019–2024.

US Medical Contract Packaging Industry Market Structure & Competitive Landscape

The US medical contract packaging market exhibits a moderately concentrated structure, with key players continuously innovating to gain market share. The industry's competitive landscape is shaped by stringent regulatory requirements, the demand for specialized packaging solutions, and a growing trend towards outsourcing by pharmaceutical and medical device manufacturers. Innovation drivers include advancements in material science, serialization and track-and-trace technologies, and the development of patient-centric packaging designs. Regulatory impacts, such as those from the FDA, necessitate adherence to Good Manufacturing Practices (GMP) and strict quality control protocols, influencing packaging material selection and manufacturing processes. Product substitutes, while present, often struggle to match the specialized functionalities and regulatory compliance offered by dedicated medical contract packaging providers. End-user segmentation primarily includes pharmaceutical companies, biotechnology firms, and medical device manufacturers, each with distinct packaging needs. Mergers and acquisitions (M&A) trends are evident, as larger players seek to expand their service offerings, geographical reach, and technological capabilities. Over the historical period (2019-2024), an estimated xx billion dollars in M&A activity has occurred, reflecting ongoing consolidation and strategic partnerships. Concentration ratios are estimated to be between xx% and xx% for the top 5 players, highlighting the significant presence of established entities.

US Medical Contract Packaging Industry Market Trends & Opportunities

The US medical contract packaging market is experiencing robust growth, driven by several interconnected trends and opportunities. The market size is projected to reach an impressive xx billion dollars by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period. This expansion is fueled by the increasing complexity of drug formulations, the rise of biologics and personalized medicine, and the persistent need for sterile and tamper-evident packaging. Technological shifts are paramount, with a growing emphasis on smart packaging solutions that incorporate features like temperature monitoring, authentication capabilities, and patient compliance aids. The integration of serialization and track-and-trace technologies to combat counterfeit drugs and ensure supply chain integrity is a significant development. Consumer preferences are also evolving, with a greater demand for user-friendly, convenient, and sustainable packaging options, prompting contract packagers to invest in eco-friendly materials and innovative designs. The competitive dynamics within the market are intensifying, characterized by strategic alliances, capacity expansions, and a relentless focus on quality and regulatory compliance. Opportunities abound for companies that can offer specialized services, such as aseptic filling, cold chain packaging, and combination product packaging. The increasing outsourcing of packaging operations by pharmaceutical and medical device companies, driven by cost efficiencies and a desire to focus on core competencies, presents a substantial growth avenue. Furthermore, the burgeoning telehealth and home healthcare sectors are creating new demands for convenient and safe packaging for medications and medical devices intended for at-home use. The market penetration of advanced packaging technologies is expected to rise significantly, creating opportunities for early adopters and innovators.

Dominant Markets & Segments in US Medical Contract Packaging Industry

The dominant markets and segments within the US medical contract packaging industry are characterized by specific service types, product categories, and material preferences, each contributing significantly to overall market value.

Dominant Service Types

Primary Packaging: This segment holds the largest market share, driven by the direct contact of packaging with the medical product.

- Medical Pouches: Essential for a wide range of sterile medical devices and pharmaceuticals, their demand is consistently high due to their versatility and cost-effectiveness. Key growth drivers include the increasing use of single-use medical devices and the need for sterile barrier protection.

- Blister Packs: Widely utilized for solid dosage forms (tablets and capsules) and small medical devices, blister packs offer excellent product visibility, tamper evidence, and dose protection. Their dominance is supported by robust manufacturing processes and consumer familiarity.

- Cartridges and Syringes: With the rise of injectable drugs and biologics, the demand for pre-filled syringes and cartridges is surging. This segment is critical for advanced drug delivery systems and requires high precision and sterile manufacturing. Growth drivers include advancements in biopharmaceuticals and the increasing preference for self-administration of medications.

- Vials and Ampoules: Traditional yet vital, vials and ampoules remain indispensable for liquid pharmaceuticals and sterile solutions. Their demand is sustained by the established use in hospitals and clinics for a variety of injectable medications.

- Others: This category encompasses specialized primary packaging like bottles, sachets, and specialized containers for diagnostic kits, reflecting the diverse needs of the medical industry.

Secondary Packaging: This layer provides additional protection, branding, and bundling of primary packages. It is crucial for unit dose packaging, multi-packs, and combination products, supporting logistical efficiency and product information dissemination. Growth is driven by regulatory requirements for patient information and the need for tamper-evident seals at the secondary level.

Tertiary Packaging: Primarily focused on bulk shipping and distribution, tertiary packaging (e.g., corrugated boxes, pallets) ensures product integrity during transit. Its importance is underscored by the need to protect large volumes of packaged medical products from damage during national and international logistics.

Dominant Material Types

Plastic: This material segment dominates the US medical contract packaging market due to its versatility, durability, barrier properties, and cost-effectiveness.

- Key Growth Drivers: High demand for flexible packaging, rigid containers, and specialized films for sterile barrier applications. Innovations in polymer science are enabling the development of more sustainable and functional plastic packaging.

Paper & Paperboard: While not as dominant as plastics for direct sterile contact, paper and paperboard are widely used in secondary and tertiary packaging, as well as for labels and inserts.

- Key Growth Drivers: Increasing preference for recyclable and biodegradable materials, particularly in secondary packaging solutions and for pharmaceutical cartons.

Glass: Essential for sterile vials and ampoules, glass remains a critical material for specific pharmaceutical and biological applications where inertness and barrier properties are paramount.

- Key Growth Drivers: The ongoing need for high-purity packaging for sensitive pharmaceuticals and biologics, especially for injectable drugs.

The dominance of plastic, particularly in primary packaging, is a testament to its adaptability to diverse medical product requirements. However, a growing awareness of sustainability is fostering innovation in paper-based solutions for secondary applications and driving research into advanced recycled plastics.

US Medical Contract Packaging Industry Product Analysis

The US medical contract packaging industry is characterized by a constant stream of product innovations aimed at enhancing patient safety, improving drug efficacy, and streamlining supply chain management. Key product advancements include the development of advanced barrier films for extended shelf-life, tamper-evident sealing technologies, and child-resistant packaging solutions. Serialization and track-and-trace features are increasingly integrated into packaging to combat counterfeiting and ensure product authenticity throughout the supply chain. Furthermore, there is a growing focus on patient-centric designs, such as unit-dose packaging for improved medication adherence and ease of use for elderly or disabled patients. Competitive advantages are derived from the ability to offer customized solutions, meet stringent regulatory standards, and provide integrated services from primary packaging to final product distribution. The market fit for these innovations is exceptionally strong, driven by the pharmaceutical and medical device sectors' unwavering commitment to quality, safety, and regulatory compliance.

Key Drivers, Barriers & Challenges in US Medical Contract Packaging Industry

The US medical contract packaging industry is propelled by several key drivers, including the rising global demand for pharmaceuticals and medical devices, the increasing complexity of drug formulations requiring specialized packaging, and the growing trend of outsourcing by manufacturers seeking cost efficiencies and expertise. Technological advancements in sterilization techniques, material science, and automation are also significant growth catalysts. Furthermore, favorable government policies promoting healthcare access and innovation indirectly support the industry.

However, the industry faces considerable barriers and challenges. Stringent and evolving regulatory requirements from bodies like the FDA can increase compliance costs and necessitate continuous adaptation. Supply chain disruptions, as experienced recently, pose a significant risk, impacting raw material availability and delivery timelines. Intense competition among contract packagers, coupled with pricing pressures from clients, can affect profitability. Moreover, the need for substantial capital investment in specialized equipment and sterile manufacturing facilities presents a financial hurdle for new entrants and smaller players.

Growth Drivers in the US Medical Contract Packaging Industry Market

The growth of the US medical contract packaging market is primarily driven by the relentless expansion of the global pharmaceutical and biotechnology sectors. The increasing prevalence of chronic diseases and an aging population are directly fueling the demand for a wider array of medications and medical devices, necessitating sophisticated packaging solutions. Technological innovations in drug delivery systems, such as biologics and personalized medicines, require specialized packaging that can maintain product integrity and efficacy, creating significant opportunities for contract packagers with advanced capabilities. Favorable regulatory environments that encourage innovation and product development also indirectly bolster growth. Economic factors, including increasing healthcare spending and the pursuit of cost-efficiency by manufacturers through outsourcing, are also key growth catalysts.

Challenges Impacting US Medical Contract Packaging Industry Growth

Despite robust growth prospects, the US medical contract packaging industry confronts several formidable challenges that can impede its expansion. Foremost among these are the ever-evolving and stringent regulatory landscapes governed by agencies like the FDA, which demand continuous investment in compliance and quality control systems, thereby increasing operational costs. Supply chain vulnerabilities, ranging from raw material shortages to logistical bottlenecks, can disrupt production schedules and impact delivery times, as evidenced by recent global events. Intense competition within the contract packaging sector also leads to significant pricing pressures, challenging profitability margins. Furthermore, the substantial capital investment required for advanced sterile manufacturing technologies and specialized equipment presents a high barrier to entry and a continuous cost for existing players.

Key Players Shaping the US Medical Contract Packaging Industry Market

- Action Pak Inc

- Aphena Pharma Solutions

- MBK Tape Solutions

- Sonic Packaging Industries Inc

- AmeriPac Inc

- Elitefill Inc

- Thermo-Pak Co Inc

- Assemblies Unlimited Inc

- Deluxe Packaging

- Tru Body Wellness

List Not Exhaustive

Significant US Medical Contract Packaging Industry Industry Milestones

January 2022: West Pharmaceutical Service, Inc., a global leader in innovative solutions for injectable drug administration, announced an exclusive supply and technology agreement with Corning Incorporated. This collaboration includes a multimillion-dollar investment to expand Corning's Valor Glass technology. The initiative aims to enable advanced injectable drug packaging and delivery systems for the pharmaceutical industry, with the overarching goals of advancing patient safety and expanding access to life-saving treatments.

February 2022: Moderna and Thermo Fisher announced a 15-year strategic collaboration agreement for the dedicated, large-scale manufacturing of Spikevax, Moderna's COVID-19 vaccine, in the United States. This agreement extends to other investigational messenger RNA (mRNA) therapeutic candidates in Moderna's pipeline. The partnership was crucial for the rapid scale-up of aseptic fill/finish services and the packaging of Moderna's COVID-19 vaccine, demonstrating significant agility and capacity in response to public health needs.

Future Outlook for US Medical Contract Packaging Industry Market

The future outlook for the US medical contract packaging industry is exceedingly positive, driven by an ongoing surge in demand for specialized pharmaceutical and medical device packaging. The increasing complexity of therapeutic molecules, including biologics and gene therapies, will necessitate advanced sterile packaging solutions, creating substantial opportunities for innovation and growth. Furthermore, the continued emphasis on patient safety, regulatory compliance, and supply chain integrity will ensure a sustained demand for high-quality contract packaging services. Strategic opportunities lie in the development of smart packaging technologies, sustainable packaging alternatives, and expanded capabilities in aseptic processing and cold chain logistics. The market is poised for continued expansion, fueled by technological advancements, evolving healthcare needs, and the persistent trend of outsourcing by medical product manufacturers.

US Medical Contract Packaging Industry Segmentation

-

1. Service Type

-

1.1. Primary

- 1.1.1. Medical Pouches

- 1.1.2. Blister Packs

- 1.1.3. Cartridges and Syringes

- 1.1.4. Vials

- 1.1.5. Ampoules

- 1.1.6. Others Product Types

- 1.2. Secondary

- 1.3. Tertiary

-

1.1. Primary

-

2. Material Type

- 2.1. Plastic

- 2.2. Paper & Paperboard

- 2.3. Glass

US Medical Contract Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

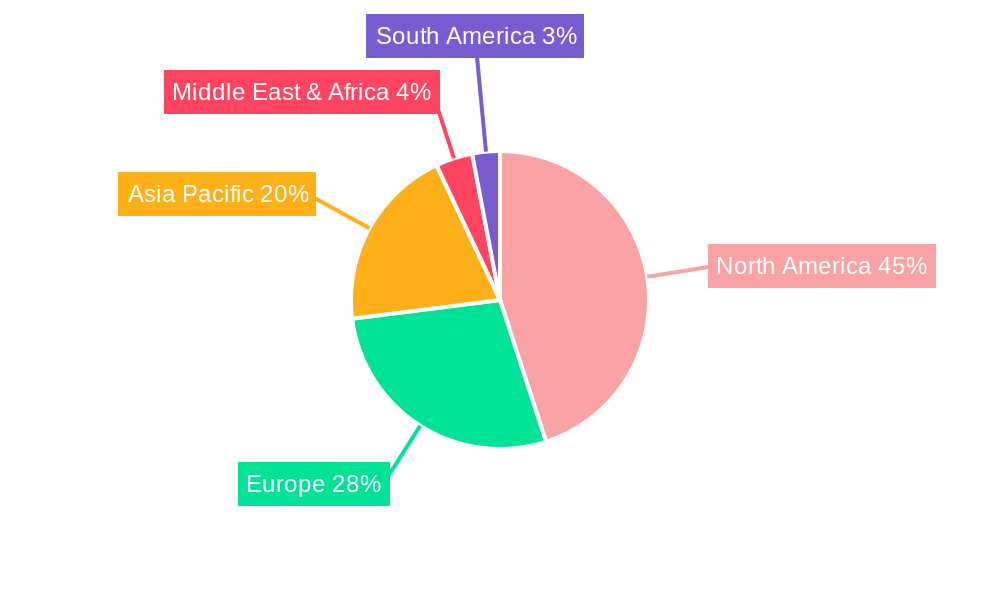

US Medical Contract Packaging Industry Regional Market Share

Geographic Coverage of US Medical Contract Packaging Industry

US Medical Contract Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Primary

- 5.1.1.1. Medical Pouches

- 5.1.1.2. Blister Packs

- 5.1.1.3. Cartridges and Syringes

- 5.1.1.4. Vials

- 5.1.1.5. Ampoules

- 5.1.1.6. Others Product Types

- 5.1.2. Secondary

- 5.1.3. Tertiary

- 5.1.1. Primary

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Plastic

- 5.2.2. Paper & Paperboard

- 5.2.3. Glass

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Primary

- 6.1.1.1. Medical Pouches

- 6.1.1.2. Blister Packs

- 6.1.1.3. Cartridges and Syringes

- 6.1.1.4. Vials

- 6.1.1.5. Ampoules

- 6.1.1.6. Others Product Types

- 6.1.2. Secondary

- 6.1.3. Tertiary

- 6.1.1. Primary

- 6.2. Market Analysis, Insights and Forecast - by Material Type

- 6.2.1. Plastic

- 6.2.2. Paper & Paperboard

- 6.2.3. Glass

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Primary

- 7.1.1.1. Medical Pouches

- 7.1.1.2. Blister Packs

- 7.1.1.3. Cartridges and Syringes

- 7.1.1.4. Vials

- 7.1.1.5. Ampoules

- 7.1.1.6. Others Product Types

- 7.1.2. Secondary

- 7.1.3. Tertiary

- 7.1.1. Primary

- 7.2. Market Analysis, Insights and Forecast - by Material Type

- 7.2.1. Plastic

- 7.2.2. Paper & Paperboard

- 7.2.3. Glass

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Primary

- 8.1.1.1. Medical Pouches

- 8.1.1.2. Blister Packs

- 8.1.1.3. Cartridges and Syringes

- 8.1.1.4. Vials

- 8.1.1.5. Ampoules

- 8.1.1.6. Others Product Types

- 8.1.2. Secondary

- 8.1.3. Tertiary

- 8.1.1. Primary

- 8.2. Market Analysis, Insights and Forecast - by Material Type

- 8.2.1. Plastic

- 8.2.2. Paper & Paperboard

- 8.2.3. Glass

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Primary

- 9.1.1.1. Medical Pouches

- 9.1.1.2. Blister Packs

- 9.1.1.3. Cartridges and Syringes

- 9.1.1.4. Vials

- 9.1.1.5. Ampoules

- 9.1.1.6. Others Product Types

- 9.1.2. Secondary

- 9.1.3. Tertiary

- 9.1.1. Primary

- 9.2. Market Analysis, Insights and Forecast - by Material Type

- 9.2.1. Plastic

- 9.2.2. Paper & Paperboard

- 9.2.3. Glass

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Primary

- 10.1.1.1. Medical Pouches

- 10.1.1.2. Blister Packs

- 10.1.1.3. Cartridges and Syringes

- 10.1.1.4. Vials

- 10.1.1.5. Ampoules

- 10.1.1.6. Others Product Types

- 10.1.2. Secondary

- 10.1.3. Tertiary

- 10.1.1. Primary

- 10.2. Market Analysis, Insights and Forecast - by Material Type

- 10.2.1. Plastic

- 10.2.2. Paper & Paperboard

- 10.2.3. Glass

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific US Medical Contract Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Primary

- 11.1.1.1. Medical Pouches

- 11.1.1.2. Blister Packs

- 11.1.1.3. Cartridges and Syringes

- 11.1.1.4. Vials

- 11.1.1.5. Ampoules

- 11.1.1.6. Others Product Types

- 11.1.2. Secondary

- 11.1.3. Tertiary

- 11.1.1. Primary

- 11.2. Market Analysis, Insights and Forecast - by Material Type

- 11.2.1. Plastic

- 11.2.2. Paper & Paperboard

- 11.2.3. Glass

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Action Pak Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Aphena Pharma Solutions

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 MBK Tape Solutions

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sonic Packaging Industries Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 AmeriPac Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Elitefill Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Thermo-Pak Co Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Assemblies Unlimited Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Deluxe Packaging*List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Tru Body Wellness

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Action Pak Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Medical Contract Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Medical Contract Packaging Industry Revenue (billion), by Service Type 2025 & 2033

- Figure 3: North America US Medical Contract Packaging Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 4: North America US Medical Contract Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 5: North America US Medical Contract Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 6: North America US Medical Contract Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Medical Contract Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Medical Contract Packaging Industry Revenue (billion), by Service Type 2025 & 2033

- Figure 9: South America US Medical Contract Packaging Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 10: South America US Medical Contract Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 11: South America US Medical Contract Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: South America US Medical Contract Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Medical Contract Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Medical Contract Packaging Industry Revenue (billion), by Service Type 2025 & 2033

- Figure 15: Europe US Medical Contract Packaging Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 16: Europe US Medical Contract Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 17: Europe US Medical Contract Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 18: Europe US Medical Contract Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Medical Contract Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Medical Contract Packaging Industry Revenue (billion), by Service Type 2025 & 2033

- Figure 21: Middle East & Africa US Medical Contract Packaging Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 22: Middle East & Africa US Medical Contract Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 23: Middle East & Africa US Medical Contract Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 24: Middle East & Africa US Medical Contract Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Medical Contract Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Medical Contract Packaging Industry Revenue (billion), by Service Type 2025 & 2033

- Figure 27: Asia Pacific US Medical Contract Packaging Industry Revenue Share (%), by Service Type 2025 & 2033

- Figure 28: Asia Pacific US Medical Contract Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 29: Asia Pacific US Medical Contract Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 30: Asia Pacific US Medical Contract Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Medical Contract Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 3: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 5: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 11: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 12: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 17: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 18: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 29: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 30: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 38: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 39: Global US Medical Contract Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Medical Contract Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Medical Contract Packaging Industry?

The projected CAGR is approximately 7.42%.

2. Which companies are prominent players in the US Medical Contract Packaging Industry?

Key companies in the market include Action Pak Inc, Aphena Pharma Solutions, MBK Tape Solutions, Sonic Packaging Industries Inc, AmeriPac Inc, Elitefill Inc, Thermo-Pak Co Inc, Assemblies Unlimited Inc, Deluxe Packaging*List Not Exhaustive, Tru Body Wellness.

3. What are the main segments of the US Medical Contract Packaging Industry?

The market segments include Service Type, Material Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 31.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Cost-Effectiveness Of The Outsourcing; Access to the advanced technologies and expertise.

6. What are the notable trends driving market growth?

Increasing Outsourcing Volumes by Major Pharmaceutical Companies.

7. Are there any restraints impacting market growth?

Monitoring issues and lack of standardization.

8. Can you provide examples of recent developments in the market?

January 2022 -West Pharmaceutical Service, Inc., a global player in innovative solutions for injectable drug administration, announced an exclusive supply and technology agreement with Corning Incorporated. The new collaboration includes a multimillion-dollar investment to expand Corning's Valor Glass technology to enable advanced injectable drug packaging and delivery systems for the pharmaceutical industry with the goal of advancing patient safety and expanding access to life-saving treatments.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Medical Contract Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Medical Contract Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Medical Contract Packaging Industry?

To stay informed about further developments, trends, and reports in the US Medical Contract Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence