Key Insights

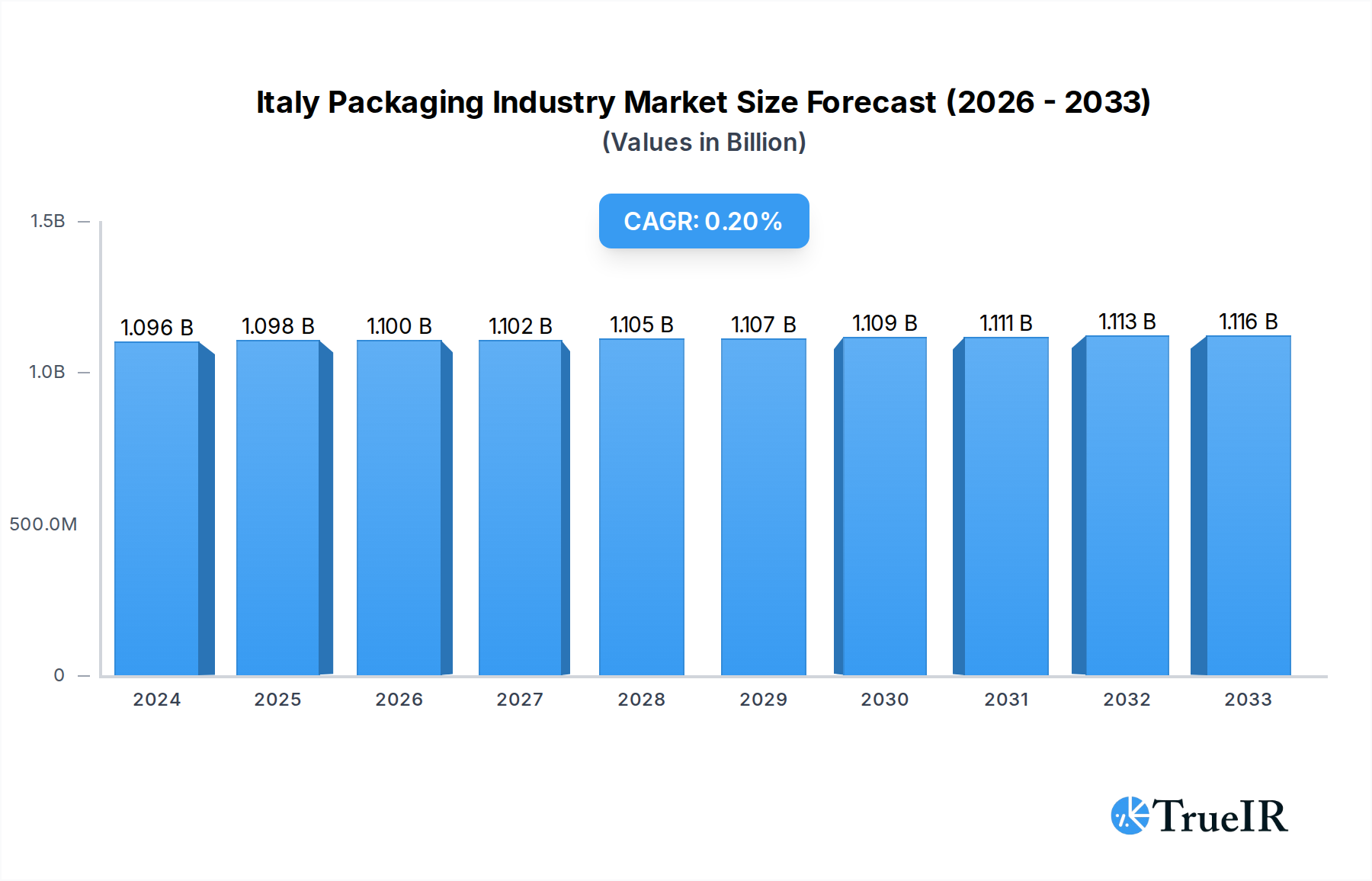

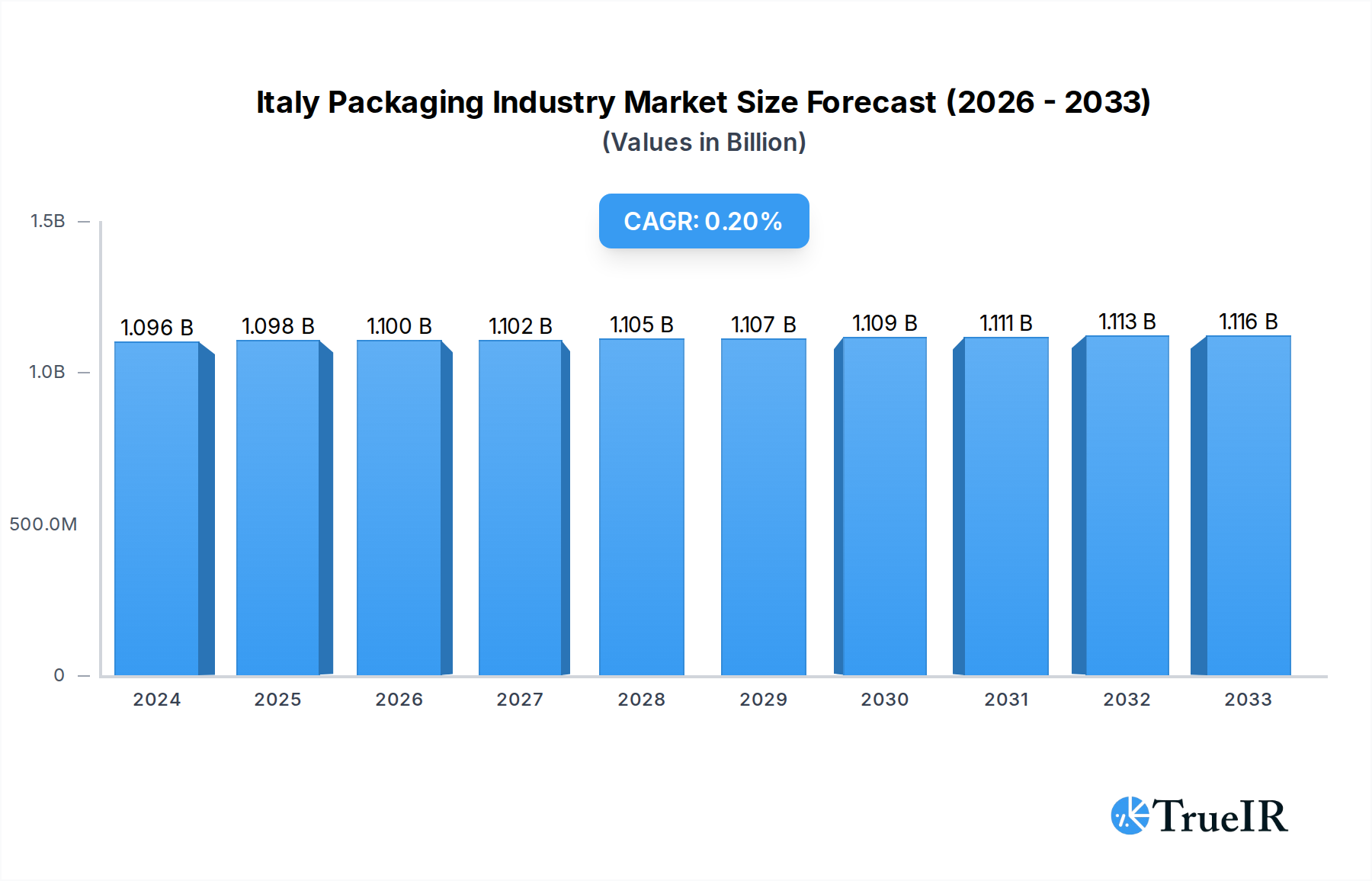

The Italian packaging industry is poised for steady, albeit modest, growth, with an estimated market size of 1095.8 million in 2024. The projected Compound Annual Growth Rate (CAGR) of 0.2% over the forecast period (2025-2033) indicates a mature market characterized by incremental advancements rather than explosive expansion. This stability is underpinned by the persistent demand from essential end-user industries such as food, beverages, and pharmaceuticals, which rely heavily on robust and innovative packaging solutions. While the overall growth rate is low, specific segments are likely to experience varied dynamics. For instance, the increasing consumer focus on sustainability and regulatory pressures are driving a shift towards more eco-friendly materials like paper and advanced plastic formulations, even as traditional materials like glass and metal maintain their strong presence in specific applications. The rigid packaging segment, offering superior protection and premium appeal, is expected to continue its dominance, supported by the consistent needs of industries valuing product integrity and shelf presence.

Italy Packaging Industry Market Size (In Billion)

The Italian packaging market's restrained growth can be attributed to several factors. While innovations in materials and design are ongoing, the mature nature of many end-user industries and the saturation of certain packaging types limit significant upswings. Furthermore, the economic climate and evolving consumer preferences for minimal or reusable packaging present challenges. However, the industry is not stagnant. Key drivers include the ongoing pursuit of enhanced product protection, increased shelf-life, and the demand for visually appealing and informative packaging that resonates with consumers. Trends such as the integration of smart packaging technologies for traceability and consumer engagement, as well as a growing emphasis on recyclability and the circular economy, are shaping the future landscape. Companies within the Italian packaging sector are actively investing in research and development to address these evolving demands, focusing on both material innovation and operational efficiency to maintain competitiveness within this stable yet dynamic market.

Italy Packaging Industry Company Market Share

This in-depth report provides a definitive look into the burgeoning Italy Packaging Industry, offering critical insights for stakeholders seeking to capitalize on its vast opportunities. Spanning the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this analysis delves into market dynamics, technological advancements, and evolving consumer demands. Leverage high-volume keywords such as Italian packaging market, packaging solutions Italy, food packaging Italy, flexible packaging Italy, and sustainable packaging Italy to understand the competitive landscape and future trajectory of this vital sector. The report is meticulously structured to provide actionable intelligence, covering everything from dominant segments to key players shaping the industry.

Italy Packaging Industry Market Structure & Competitive Landscape

The Italian packaging market exhibits a moderately concentrated structure, characterized by a blend of large multinational corporations and agile domestic players. Innovation is a critical differentiator, driven by the constant pursuit of sustainable materials and advanced functionalities. Regulatory frameworks, particularly those concerning recyclable packaging and environmental impact, are increasingly influencing market dynamics, pushing companies towards eco-friendly solutions. Product substitutes are emerging, especially from advancements in bioplastics and innovative paper-based alternatives, prompting established players to diversify their offerings. End-user segmentation reveals the Food and Beverages sector as a dominant force, followed closely by Personal Care and Pharmaceuticals, each with unique packaging requirements. Mergers and Acquisitions (M&A) activity, though subject to economic fluctuations, remains a significant trend, aimed at consolidating market share, acquiring new technologies, and expanding geographical reach. Concentration ratios indicate a substantial market share held by the top 5-10 players, underscoring the competitive intensity within key Italian packaging segments. The drive towards a circular economy is paramount, influencing investment in R&D for sustainable packaging solutions Italy.

Italy Packaging Industry Market Trends & Opportunities

The Italy Packaging Industry is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period. This expansion is fueled by increasing consumer demand for convenience, enhanced product shelf-life, and aesthetically pleasing packaging. Technological shifts are profoundly impacting the sector, with a significant move towards smart packaging solutions that offer traceability, anti-counterfeiting features, and interactive capabilities. The rise of e-commerce has spurred demand for specialized e-commerce packaging Italy, emphasizing durability and lightweight designs. Consumer preferences are increasingly leaning towards sustainable and eco-friendly packaging. This includes a growing appetite for recycled content packaging, biodegradable materials, and minimized packaging waste. The Italian packaging market is responding by investing in advanced recycling technologies and innovative material science. Competitive dynamics are intensifying, with companies differentiating themselves through superior design, customization options, and a strong commitment to environmental stewardship. Opportunities abound in developing innovative solutions for niche markets, enhancing the sustainability profile of existing products, and leveraging digital technologies for supply chain optimization and customer engagement. The penetration rate of advanced packaging technologies is steadily increasing across all end-user industries, presenting a fertile ground for technological innovation and market penetration. The demand for flexible packaging Italy for on-the-go consumption and the resurgence of rigid packaging Italy for premium products highlight the diverse needs shaping market trends.

Dominant Markets & Segments in Italy Packaging Industry

The Italian packaging industry is dominated by several key segments, each contributing significantly to the overall market value.

Material Dominance:

- Plastic: Remains the largest segment by volume and value, driven by its versatility, durability, and cost-effectiveness for a wide array of applications, particularly in food packaging Italy and personal care packaging Italy. The ongoing development of advanced, recyclable, and bio-based plastics further solidifies its position.

- Paper & Paperboard: A rapidly growing segment, propelled by the strong emphasis on sustainability and the demand for eco-friendly packaging Italy. Its widespread use in beverage packaging Italy and secondary packaging highlights its importance. Policies promoting recycling and the use of recycled content are key growth drivers.

- Glass: Continues to hold a significant share, especially in the beverage packaging Italy and food packaging Italy sectors, prized for its inertness and premium appeal. Innovations in lightweighting and design are helping to maintain its competitiveness.

- Metal: Primarily utilized in the food packaging Italy and beverage packaging Italy sectors, particularly for cans and aerosols. Its recyclability and durability make it a preferred choice for long-term storage and preservation.

Packaging Type Dominance:

- Flexible Packaging: This segment is witnessing substantial growth, driven by its lightweight nature, cost-efficiency, and suitability for single-serving and on-the-go products in food packaging Italy and personal care packaging Italy. Innovations in barrier properties and recyclability are key growth drivers.

- Rigid Packaging: While facing competition from flexible alternatives, rigid packaging, including bottles, jars, and cartons, continues to be vital for products requiring robust protection and premium presentation, particularly in the beverage packaging Italy and pharmaceutical packaging Italy sectors.

End-User Industry Dominance:

- Food: This is the largest and most influential end-user industry, accounting for a substantial portion of the Italian packaging market. Demand is driven by the need for preservation, safety, convenience, and appealing presentation of a wide range of food products.

- Beverages: A consistently strong segment, encompassing alcoholic and non-alcoholic drinks. Packaging requirements range from bulk containers to single-serve bottles and cans, with a growing emphasis on sustainability.

- Personal Care: This sector requires specialized packaging for cosmetics, toiletries, and personal hygiene products, with a focus on aesthetics, functionality, and consumer appeal.

- Pharmaceuticals: Characterized by stringent regulatory requirements, this segment demands high levels of safety, tamper-evidence, and child-resistance in its packaging solutions.

Key growth drivers across these dominant segments include supportive government policies promoting recycling and sustainable practices, increasing disposable incomes driving demand for packaged goods, and significant investments in R&D for innovative and environmentally friendly packaging solutions.

Italy Packaging Industry Product Analysis

The Italian packaging industry is characterized by continuous product innovation, aimed at enhancing functionality, sustainability, and consumer appeal. Key advancements include the development of advanced barrier films for extended shelf-life in food packaging Italy, lightweight glass bottles for improved logistics, and smart packaging solutions with embedded RFID tags for enhanced traceability. Competitive advantages are being secured through the integration of recycled content, the adoption of biodegradable materials, and the creation of novel dispensing mechanisms. The industry is actively developing packaging tailored for specific end-user needs, from tamper-evident closures for pharmaceuticals to visually striking containers for premium cosmetics, all while striving to meet increasingly stringent environmental regulations.

Key Drivers, Barriers & Challenges in Italy Packaging Industry

Key Drivers: The growth of the Italy Packaging Industry is propelled by several critical factors.

- Technological Advancements: Innovations in material science, automation, and smart packaging technologies are driving efficiency and new product development.

- Consumer Demand for Sustainability: A growing awareness of environmental issues is creating significant demand for recyclable, biodegradable, and reusable packaging solutions.

- Economic Growth & Consumer Spending: An expanding economy and increased disposable income directly correlate with higher consumption of packaged goods.

- Evolving Retail Landscape: The rise of e-commerce necessitates robust and adaptable packaging solutions.

Barriers & Challenges: The industry faces several impediments.

- Regulatory Complexities: Stringent environmental regulations and varying recycling infrastructure across regions can create compliance challenges and increase operational costs.

- Supply Chain Disruptions: Global events and geopolitical factors can lead to volatility in raw material prices and availability, impacting production schedules and costs. For instance, fluctuating plastic resin prices can significantly impact the profitability of plastic packaging manufacturers.

- Competitive Pressures: Intense competition among domestic and international players necessitates continuous innovation and cost management. The high cost of implementing new, sustainable technologies can also be a significant barrier for smaller enterprises.

Growth Drivers in the Italy Packaging Industry Market

The Italy Packaging Industry is experiencing significant growth fueled by several interconnected drivers. Technological advancements in material science are enabling the creation of lighter, stronger, and more sustainable packaging options. The increasing consumer consciousness towards environmental impact is a paramount driver, pushing demand for recycled packaging Italy and biodegradable alternatives, thereby fostering innovation in sustainable packaging solutions Italy. Furthermore, economic stability and a rising consumer spending capacity directly translate into higher demand for packaged goods across all sectors, particularly in food packaging Italy and personal care packaging Italy. Government initiatives and regulations aimed at promoting circular economy principles also play a crucial role in shaping market growth by incentivizing sustainable practices and investments in recycling infrastructure. The expansion of the e-commerce sector is another critical growth catalyst, demanding specialized, durable, and efficient packaging solutions.

Challenges Impacting Italy Packaging Industry Growth

Despite its growth trajectory, the Italy Packaging Industry grapples with several challenges. The complexity and ever-evolving nature of environmental regulations, including packaging waste directives and carbon footprint targets, pose significant compliance hurdles for manufacturers. Volatility in the prices and availability of raw materials, such as petroleum-based resins for plastics and pulp for paper, can lead to unpredictable cost fluctuations and impact profit margins. Intense competition within the market, coupled with the substantial capital investment required for adopting new, sustainable technologies, creates pressure on businesses to maintain competitiveness and innovate effectively. Furthermore, managing intricate global and local supply chains, susceptible to disruptions from unforeseen events, remains a constant operational challenge. The cost associated with developing and implementing truly circular packaging solutions can also be a significant barrier to widespread adoption.

Key Players Shaping the Italy Packaging Industry Market

- Cartotecnica Olimpia

- Wipak Bordi SRL

- DS Smith Packaging Italia SpA

- Rotofil SRL

- Zignago Vetro

- Tetra Pak Italiana SpA

- SAIDA Group

- Vetroelite S r l

- Smurfit Kappa Italia SpA

- Vetreria Etrusca

Significant Italy Packaging Industry Industry Milestones

- July 2022: Zignago Vetro's site at Fossalta di Portogruaro started up a new furnace, significantly increasing production capacity for F&B containers in flint glass, including jars and bottles.

- June 2022: IPV PACK inaugurated its first international branch in Serbia, marking a strategic expansion into new markets and responding to anticipated demand for its plastic processing and high-quality packaging solutions.

- April 2022: Zignago Vetro introduced the 100 ml LAMA glass bottle with a screw neck, expanding its product range for the perfumery sector and catering to specific industry standards.

Future Outlook for Italy Packaging Industry Market

The future outlook for the Italy Packaging Industry remains exceptionally positive, driven by innovation and a strong commitment to sustainability. The market will continue to witness a surge in demand for eco-friendly packaging Italy, including compostable and biodegradable materials, and a significant increase in the adoption of circular economy principles. Technological advancements in smart packaging and advanced recycling will redefine product offerings, enhancing traceability and consumer engagement. The food and beverage sectors will remain dominant, but growth in personal care and pharmaceuticals, driven by specialized packaging needs, will also be substantial. Strategic opportunities lie in developing customized solutions for emerging markets, investing in research for novel sustainable materials, and leveraging digital technologies for optimized supply chain management and customer interaction. The industry is poised for sustained growth, driven by a confluence of consumer demand, technological progress, and a proactive approach to environmental responsibility.

Italy Packaging Industry Segmentation

-

1. Material

- 1.1. Paper

- 1.2. Plastic

- 1.3. Metal

- 1.4. Glass

-

2. Packaging Type

- 2.1. Rigid Packaging

- 2.2. Flexible Packaging

-

3. End-User Industry

- 3.1. Food

- 3.2. Beverages

- 3.3. Pharmaceuticals

- 3.4. Personal Care

- 3.5. Other End-User Industries

Italy Packaging Industry Segmentation By Geography

- 1. Italy

Italy Packaging Industry Regional Market Share

Geographic Coverage of Italy Packaging Industry

Italy Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.94% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Paper

- 5.1.2. Plastic

- 5.1.3. Metal

- 5.1.4. Glass

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Rigid Packaging

- 5.2.2. Flexible Packaging

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Food

- 5.3.2. Beverages

- 5.3.3. Pharmaceuticals

- 5.3.4. Personal Care

- 5.3.5. Other End-User Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Italy

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Italy Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Paper

- 6.1.2. Plastic

- 6.1.3. Metal

- 6.1.4. Glass

- 6.2. Market Analysis, Insights and Forecast - by Packaging Type

- 6.2.1. Rigid Packaging

- 6.2.2. Flexible Packaging

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Food

- 6.3.2. Beverages

- 6.3.3. Pharmaceuticals

- 6.3.4. Personal Care

- 6.3.5. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Cartotecnica Olimpia

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Wipak Bordi SRL

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DS Smith Packaging Italia SpA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Rotofil SRL

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zignago Vetro

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Tetra Pak Italiana SpA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SAIDA Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Vetroelite S r l

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Smurfit Kappa Italia SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Vetreria Etrusca

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Cartotecnica Olimpia

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italy Packaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Italy Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Italy Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Italy Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 3: Italy Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 4: Italy Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Italy Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 6: Italy Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 7: Italy Packaging Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 8: Italy Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italy Packaging Industry?

The projected CAGR is approximately 3.94%.

2. Which companies are prominent players in the Italy Packaging Industry?

Key companies in the market include Cartotecnica Olimpia, Wipak Bordi SRL, DS Smith Packaging Italia SpA, Rotofil SRL, Zignago Vetro, Tetra Pak Italiana SpA, SAIDA Group, Vetroelite S r l, Smurfit Kappa Italia SpA, Vetreria Etrusca.

3. What are the main segments of the Italy Packaging Industry?

The market segments include Material, Packaging Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 28.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Environmental Concerns; Government Regulations for Consumables.

6. What are the notable trends driving market growth?

Plastic Packaging to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

; High Costs Compared to Normal Plastic.

8. Can you provide examples of recent developments in the market?

July 2022: Zignago Vetro's site at Fossalta di Portogruaro started up a new furnace, which can produce up to 370 tonnes thanks to its four lines, two of which can manage products in tandem. It specializes in F&B containers in flint glass, mainly jars but also bottles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italy Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italy Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italy Packaging Industry?

To stay informed about further developments, trends, and reports in the Italy Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence