Key Insights

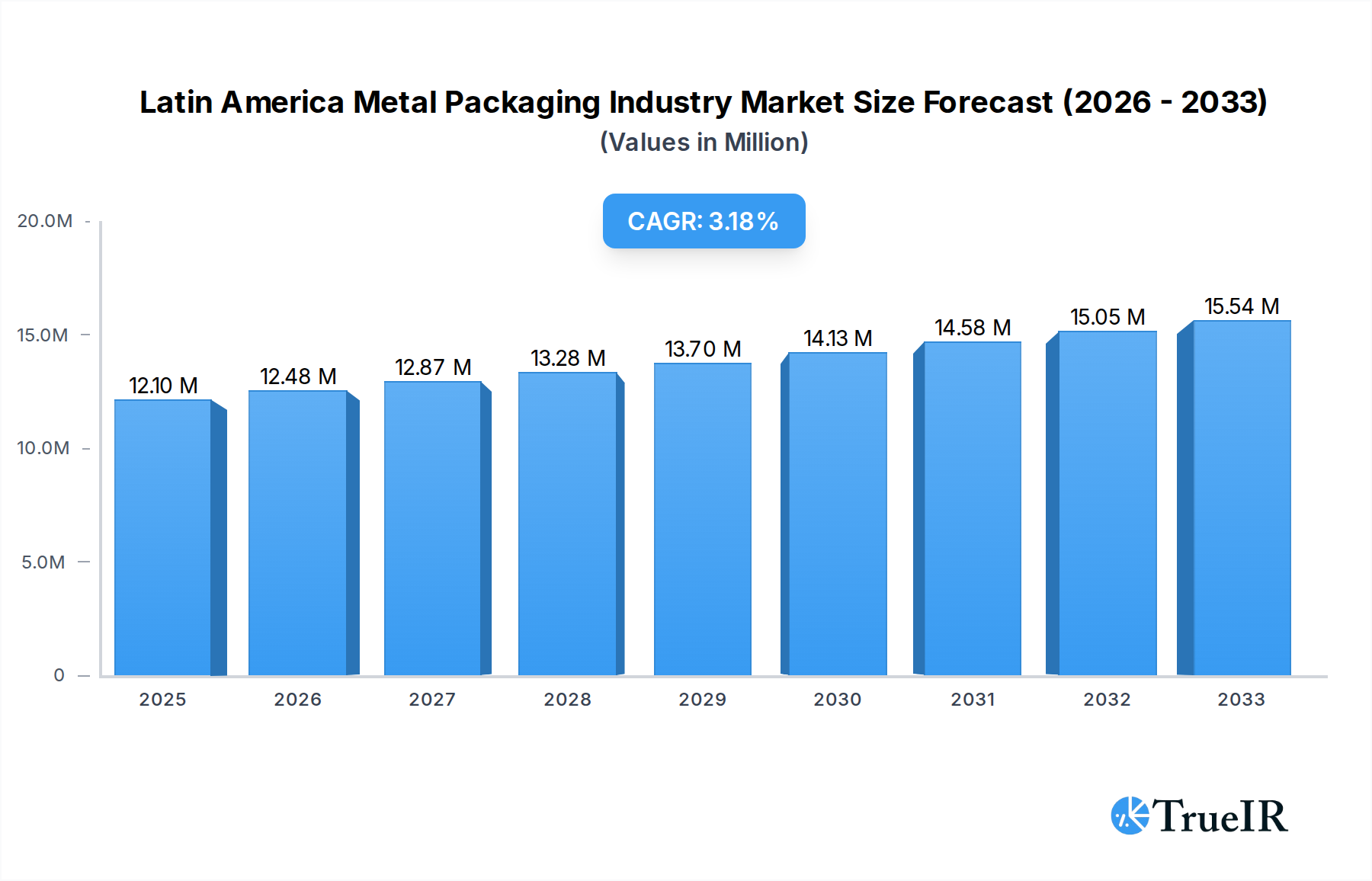

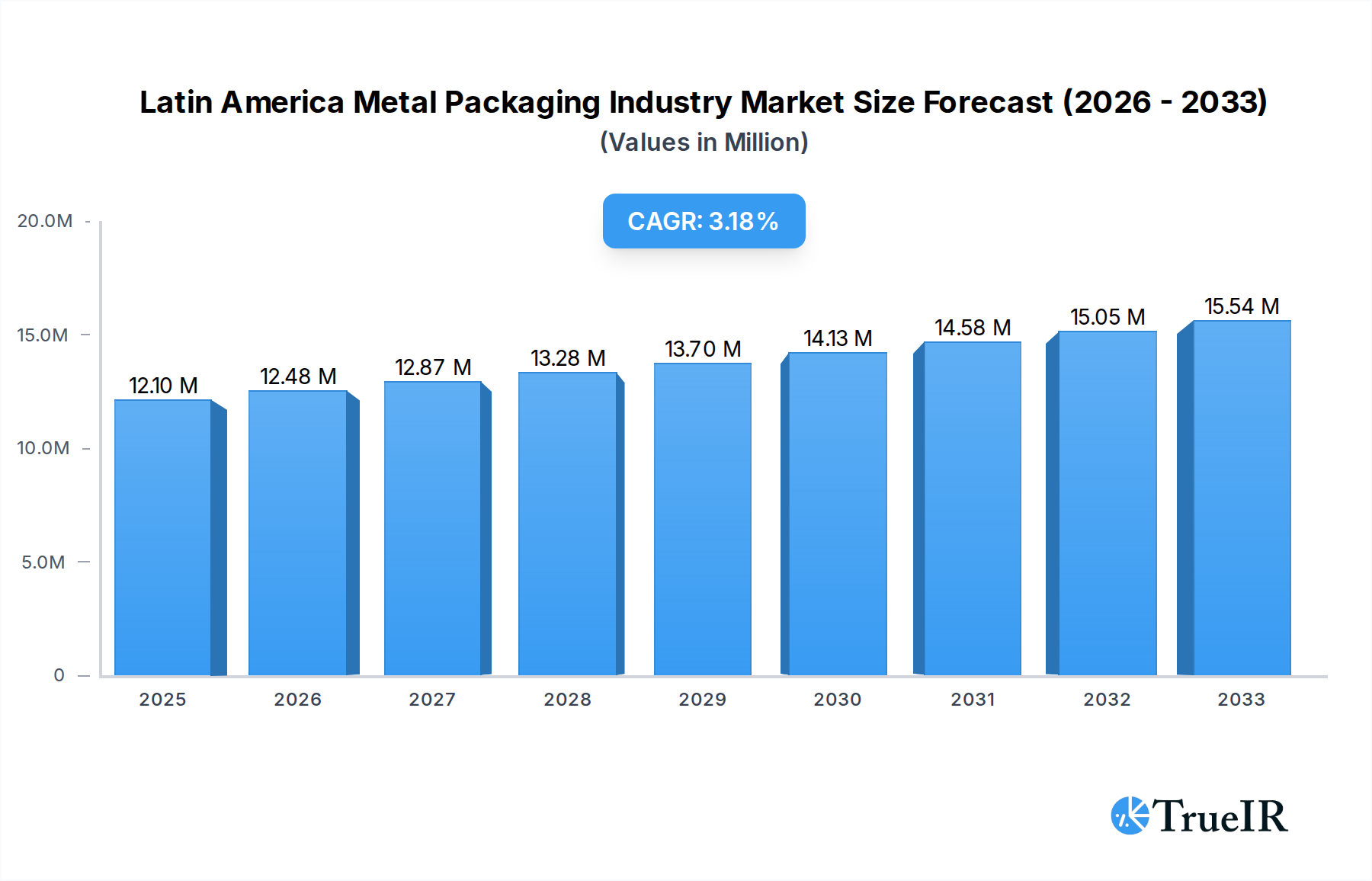

The Latin America Metal Packaging Industry is poised for steady expansion, projected to reach a market size of $12.10 Million by 2025, growing at a Compound Annual Growth Rate (CAGR) of 3.14% from 2019 to 2033. This growth is propelled by increasing consumer demand for packaged goods across various sectors, particularly beverages and food, which represent a significant portion of the market's end-user base. The burgeoning middle class in countries like Brazil, Mexico, and Colombia is driving consumption, leading to a greater need for durable and reliable packaging solutions. Furthermore, the inherent recyclability and premium perception of metal packaging, especially aluminum and steel, align with growing environmental consciousness among consumers and regulatory pushes towards sustainable practices. The expansion of e-commerce and the demand for convenient, single-serving options also contribute to the uptake of various metal packaging formats, including cans and smaller containers.

Latin America Metal Packaging Industry Market Size (In Million)

Key drivers fueling this market include the increasing disposable incomes and a shift towards processed and ready-to-eat food and beverage products. The cosmetics and personal care industry also presents a significant opportunity, with metal packaging offering an aesthetically pleasing and protective option for premium products. While the market shows resilience, potential restraints could emerge from fluctuations in raw material prices (aluminum and steel), and the competitive landscape from alternative packaging materials like plastic and glass. However, the industry's commitment to innovation, focusing on lightweighting, advanced barrier properties, and enhanced aesthetics, is expected to mitigate these challenges. Key players like Ball Corporation, Crown Holdings Inc., and Ardagh Metal Packaging SA are actively investing in capacity expansion and technological advancements across Latin America to capitalize on these growth opportunities and maintain their competitive edge.

Latin America Metal Packaging Industry Company Market Share

Latin America Metal Packaging Industry: Market Analysis and Forecast (2019-2033)

This comprehensive report delivers an in-depth analysis of the Latin America Metal Packaging Industry, providing critical insights for stakeholders navigating this dynamic market. Covering the historical period from 2019 to 2024, the base year of 2025, and a robust forecast period extending to 2033, this report offers a complete picture of market evolution, trends, and future potential. We leverage high-volume keywords to ensure optimal SEO performance and broad industry reach, targeting decision-makers within the beverage, food, cosmetics, household, and paints & varnishes sectors, among others.

Latin America Metal Packaging Industry Market Structure & Competitive Landscape

The Latin America Metal Packaging Industry is characterized by a moderately concentrated market structure, driven by significant capital investments required for manufacturing facilities and a strong emphasis on technological innovation to meet evolving consumer and regulatory demands. Key innovation drivers include the pursuit of lightweighting solutions, enhanced barrier properties for extended shelf life, and the development of sustainable packaging alternatives. Regulatory impacts, particularly concerning environmental standards and recycling mandates, play a crucial role in shaping product development and market entry strategies. While the demand for metal packaging remains strong, particularly for its durability and recyclability, potential product substitutes from flexible packaging and advanced plastics present a continuous challenge. End-user segmentation reveals a significant reliance on the Beverage and Food industries, which constitute the largest share of demand. Mergers and acquisitions (M&A) trends are notable as larger players seek to consolidate their market positions, expand geographical reach, and acquire specialized technological capabilities. For instance, the increasing focus on sustainable packaging solutions is driving M&A activities aimed at integrating companies with advanced recycling technologies or expertise in biodegradable metal coatings. The market concentration is estimated with a Herfindahl-Hirschman Index (HHI) of approximately 1800, indicating a moderately concentrated market. M&A volumes have seen a steady increase, with an estimated USD 150 Million in transactions recorded in the historical period (2019-2024).

- Innovation Drivers: Lightweighting, improved barrier properties, sustainable materials, smart packaging integration.

- Regulatory Impacts: Increased focus on recyclability targets, extended producer responsibility schemes, single-use plastic bans indirectly benefiting metal.

- Product Substitutes: Flexible pouches, advanced polymer films, composite packaging.

- End-user Dominance: Beverage, Food, Cosmetics & Personal Care.

- M&A Trends: Consolidation for scale, acquisition of sustainable technology, vertical integration.

Latin America Metal Packaging Industry Market Trends & Opportunities

The Latin America Metal Packaging Industry is projected to experience robust growth, driven by a confluence of escalating consumer demand for sustainable and premium packaging, coupled with an increasing awareness of metal's inherent recyclability. The market size is estimated to reach approximately USD 12,500 Million by 2025, with a projected Compound Annual Growth Rate (CAGR) of 5.8% during the forecast period of 2025–2033. Technological shifts are a significant trend, with advancements in manufacturing processes leading to lighter and more durable metal packaging, while also reducing the environmental footprint of production. The adoption of thin-wall technology in aluminum cans, for example, is a key innovation enabling greater material efficiency and cost-effectiveness. Consumer preferences are increasingly leaning towards brands that demonstrate environmental responsibility, making metal packaging, with its high recycling rates, a preferred choice. The beverage sector, in particular, is witnessing a surge in demand for aluminum cans for carbonated soft drinks, beer, and juices, owing to their portability, shelf appeal, and excellent preservation qualities. Furthermore, the growing middle class across Latin America is fueling demand for packaged goods across various end-user industries, including food, personal care, and household products, all of which heavily rely on metal packaging solutions for their integrity and market presentation. Opportunities abound for companies that can offer innovative, sustainable, and cost-effective metal packaging solutions. The expansion of e-commerce also presents a growing avenue, as metal packaging's durability ensures product protection during transit. The increasing penetration of aluminum beverage cans is expected to reach 65% by 2028, a significant increase from 50% in 2019.

Dominant Markets & Segments in Latin America Metal Packaging Industry

The Beverage segment stands as the dominant end-user industry within the Latin America Metal Packaging Industry, driven by robust demand for canned beverages across the region. Within this segment, Beverage Cans are the most significant product type, experiencing substantial growth attributed to their convenience, portability, and superior product preservation capabilities. The Aluminum material type is increasingly favored over steel for beverage cans due to its lighter weight and excellent recyclability, contributing to its market dominance. Brazil and Mexico emerge as the leading countries in terms of market size and consumption, owing to their large populations, developing economies, and established manufacturing bases. The Food Cans segment also holds a significant position, with increasing demand for processed and convenience foods necessitating reliable and safe packaging solutions.

- Leading End-user Industry: Beverage, followed closely by Food.

- Growth Drivers: Growing beverage consumption, demand for convenience foods, rising disposable incomes.

- Market Dominance Factors: Extensive beverage production, large food processing sector, favorable demographics.

- Dominant Product Type: Cans (Beverage Cans, Food Cans).

- Growth Drivers: Consumer preference for on-the-go consumption, extended shelf-life requirements, innovative product designs.

- Market Dominance Factors: Versatility, cost-effectiveness, high production volumes.

- Leading Material Type: Aluminum, especially for beverage applications, and Steel for food and bulk containers.

- Growth Drivers: Aluminum's lightweight and recyclability, steel's durability and cost-effectiveness for bulk packaging.

- Market Dominance Factors: Availability of raw materials, technological advancements in material processing.

- Key Geographic Markets: Brazil, Mexico, Argentina.

- Growth Drivers: Large consumer base, expanding middle class, supportive government policies for manufacturing and exports.

- Market Dominance Factors: Robust industrial infrastructure, established distribution networks.

Latin America Metal Packaging Industry Product Analysis

The Latin America Metal Packaging Industry is witnessing continuous product innovation focused on enhancing sustainability, functionality, and consumer appeal. Advancements in Aluminum Cans are leading to thinner walls and lighter weights, reducing material consumption and transportation costs without compromising structural integrity. For Steel Cans, innovations center on improved internal coatings to prevent corrosion and ensure food safety. The market is also seeing growth in specialized Caps & Closures that offer enhanced tamper-evidence and ease of use. The application of high-resolution printing and decorative finishes on metal packaging provides brands with superior shelf presence. Competitive advantages are being carved out through superior recyclability, extended product shelf-life, and tailored packaging solutions for diverse product needs, particularly within the food and beverage sectors.

Key Drivers, Barriers & Challenges in Latin America Metal Packaging Industry

Key Drivers: The Latin America Metal Packaging Industry is propelled by several key drivers, including the growing global and regional emphasis on sustainable packaging, with metal's high recyclability being a significant advantage. Economic growth and an expanding middle class across Latin American countries are increasing consumer spending on packaged goods, thereby boosting demand. Technological advancements in manufacturing processes are leading to more efficient and cost-effective production of metal packaging. Furthermore, favorable government regulations promoting recycling and reducing plastic waste indirectly support the metal packaging sector. The inherent durability and protective qualities of metal packaging make it ideal for preserving product quality and extending shelf life, a crucial factor for the food and beverage industries.

Barriers & Challenges: Despite the positive outlook, the industry faces significant barriers and challenges. Fluctuations in raw material prices, particularly for aluminum and steel, can impact manufacturing costs and profitability. The high capital investment required for setting up and maintaining metal packaging production facilities poses a barrier to entry for smaller players. Intense competition from alternative packaging materials like flexible plastics and glass, which may offer lower initial costs or different aesthetic appeals, presents a constant challenge. Supply chain disruptions, including logistical complexities and raw material availability issues in certain regions, can affect production timelines. Regulatory hurdles related to environmental compliance and waste management, while often supportive of metal, can also introduce operational complexities and costs. The need for continuous innovation to match the evolving demands for product functionality and design also presents an ongoing challenge.

Growth Drivers in the Latin America Metal Packaging Industry Market

Key growth drivers in the Latin America Metal Packaging Industry include the escalating consumer demand for environmentally friendly packaging solutions, with metal's inherent recyclability being a significant draw. Economic development and the expansion of the middle class across the region are fueling increased consumption of packaged goods across diverse sectors. Technological advancements in manufacturing are enabling the production of lighter, stronger, and more cost-effective metal packaging. Supportive government policies promoting recycling initiatives and reducing reliance on single-use plastics are also creating a more favorable market environment for metal packaging. The inherent protective qualities of metal, ensuring product integrity and extending shelf life, remain a critical advantage, especially for food and beverage products.

Challenges Impacting Latin America Metal Packaging Industry Growth

Challenges impacting Latin America Metal Packaging Industry growth include the volatility of raw material prices for aluminum and steel, which can significantly affect production costs and profit margins. The substantial capital investment required for advanced manufacturing facilities acts as a barrier to entry and expansion. Intense competition from alternative packaging materials such as flexible plastics and glass, often perceived as cheaper or more aesthetically versatile for certain applications, poses a continuous threat. Supply chain disruptions, including raw material sourcing issues and logistical complexities within the region, can lead to production delays and increased operational costs. Furthermore, navigating diverse and evolving regulatory landscapes across different Latin American countries, particularly concerning environmental standards and waste management, adds complexity to operations.

Key Players Shaping the Latin America Metal Packaging Industry Market

- Ardagh Metal Packaging SA (Ardagh Group)

- Ball Corporation

- Crown Holdings Inc

- CANPACK SA (CANPACK Group)

- Greif Inc

- Mauser Packaging Solutions

- Trivium Packaging

- Closure Systems International Inc (CSI)

- Guala Closures SpA

- Schutz GmbH & Co KGaA

Significant Latin America Metal Packaging Industry Industry Milestones

- February 2024: São Geraldo announced its partnership with CANPACK SA to launch its flagship beverage in 350 ml infinitely recyclable cans. São Geraldo included cans as a packaging solution for its cashew fruit-flavor drink, which was previously only available in PET or glass bottles.

- October 2023: Colep Packaging announced a joint venture with Envases Group for the construction of an aerosol packaging plant in Mexico. The new plant in Mexico would include three aluminum aerosol lines. With the construction of a new plant, the company can focus better on serving customers in Mexico as well as in Central America.

Future Outlook for Latin America Metal Packaging Industry Market

The future outlook for the Latin America Metal Packaging Industry is exceptionally promising, driven by an unwavering global and regional shift towards sustainable consumption patterns. The inherent recyclability of metal packaging aligns perfectly with increasing environmental consciousness and regulatory pressures to reduce waste. Growth catalysts include ongoing innovation in lightweighting technologies, enhancing material efficiency and cost-effectiveness. The expanding middle class across Latin America will continue to drive demand for packaged goods, with metal packaging serving as a preferred choice for its durability and premium perception. Opportunities for market expansion lie in catering to emerging product categories and in developing advanced functionalities such as smart packaging solutions. The industry is poised for sustained growth, with strategic investments in capacity expansion and technological upgrades being crucial for market leaders to capitalize on the burgeoning demand for sustainable and reliable metal packaging solutions.

Latin America Metal Packaging Industry Segmentation

-

1. Material Type

- 1.1. Aluminum

- 1.2. Steel

-

2. Product Type

-

2.1. Cans

- 2.1.1. Food Cans

- 2.1.2. Beverage Cans

- 2.1.3. Aerosol Cans

- 2.2. Bulk Containers

- 2.3. Shipping Barrels and Drums

- 2.4. Caps & Closures

- 2.5. Other Product Types

-

2.1. Cans

-

3. End-user Industry

- 3.1. Beverage

- 3.2. Food

- 3.3. Cosmetics & Personal Care

- 3.4. Household

- 3.5. Paints & Varnishes

- 3.6. Other End-user Industries

Latin America Metal Packaging Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Metal Packaging Industry Regional Market Share

Geographic Coverage of Latin America Metal Packaging Industry

Latin America Metal Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aluminum

- 5.1.2. Steel

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Cans

- 5.2.1.1. Food Cans

- 5.2.1.2. Beverage Cans

- 5.2.1.3. Aerosol Cans

- 5.2.2. Bulk Containers

- 5.2.3. Shipping Barrels and Drums

- 5.2.4. Caps & Closures

- 5.2.5. Other Product Types

- 5.2.1. Cans

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Beverage

- 5.3.2. Food

- 5.3.3. Cosmetics & Personal Care

- 5.3.4. Household

- 5.3.5. Paints & Varnishes

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Latin America Metal Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aluminum

- 6.1.2. Steel

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Cans

- 6.2.1.1. Food Cans

- 6.2.1.2. Beverage Cans

- 6.2.1.3. Aerosol Cans

- 6.2.2. Bulk Containers

- 6.2.3. Shipping Barrels and Drums

- 6.2.4. Caps & Closures

- 6.2.5. Other Product Types

- 6.2.1. Cans

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Beverage

- 6.3.2. Food

- 6.3.3. Cosmetics & Personal Care

- 6.3.4. Household

- 6.3.5. Paints & Varnishes

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ball Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Crown Holdings Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CANPACK SA (CANPACK Group)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Greif Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mauser Packaging Solutions

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Trivium Packaging

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Closure Systems International Inc (CSI)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guala Closures SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Schutz GmbH & Co KGaA*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Metal Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Latin America Metal Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Latin America Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 3: Latin America Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Latin America Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 5: Latin America Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Latin America Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Latin America Metal Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Latin America Metal Packaging Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Latin America Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 10: Latin America Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 11: Latin America Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Latin America Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 13: Latin America Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Latin America Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Latin America Metal Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Latin America Metal Packaging Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 17: Brazil Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Brazil Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Argentina Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Argentina Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: Chile Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Chile Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: Colombia Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Colombia Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Mexico Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Mexico Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: Peru Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Peru Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Venezuela Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Venezuela Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Ecuador Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Ecuador Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Bolivia Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Bolivia Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Paraguay Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Paraguay Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Metal Packaging Industry?

The projected CAGR is approximately 3.14%.

2. Which companies are prominent players in the Latin America Metal Packaging Industry?

Key companies in the market include Ardagh Metal Packaging SA (Ardagh Group), Ball Corporation, Crown Holdings Inc, CANPACK SA (CANPACK Group), Greif Inc, Mauser Packaging Solutions, Trivium Packaging, Closure Systems International Inc (CSI), Guala Closures SpA, Schutz GmbH & Co KGaA*List Not Exhaustive.

3. What are the main segments of the Latin America Metal Packaging Industry?

The market segments include Material Type, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.10 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing Beverage Consumption in Brazil Driving Sales of Metal Packaging Solutions.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2024: São Geraldo announced its partnership with CANPACK SA to launch its flagship beverage in 350 ml infinitely recyclable cans. São Geraldo included cans as a packaging solution for its cashew fruit-flavor drink, which was previously only available in PET or glass bottles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Metal Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Metal Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Metal Packaging Industry?

To stay informed about further developments, trends, and reports in the Latin America Metal Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence