Key Insights

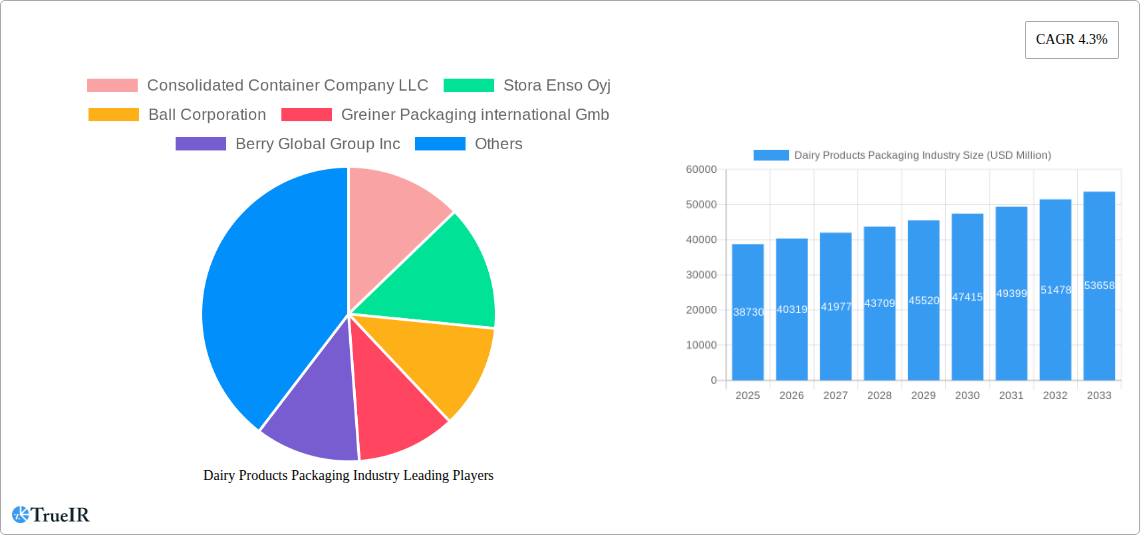

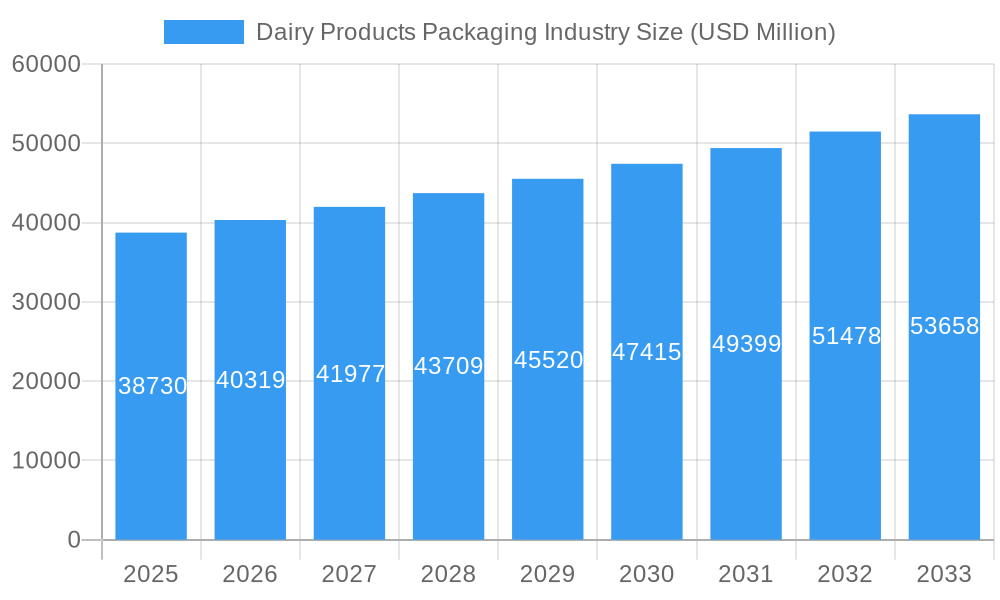

The global Dairy Products Packaging market is projected to reach USD 38.73 billion in 2025, exhibiting robust growth with a Compound Annual Growth Rate (CAGR) of 4.3% during the forecast period of 2025-2033. This expansion is primarily driven by the increasing global demand for dairy products, fueled by rising disposable incomes, a growing awareness of dairy's nutritional benefits, and evolving consumer preferences for convenient and sustainable packaging solutions. Key drivers for this market growth include the expanding processed dairy sector, particularly in emerging economies, and the continuous innovation in packaging materials and designs that enhance product shelf-life, maintain freshness, and offer improved user experience. The surge in yogurt and cultured products consumption, alongside the persistent popularity of milk and cheese, significantly contributes to the demand for specialized packaging formats.

Dairy Products Packaging Industry Market Size (In Billion)

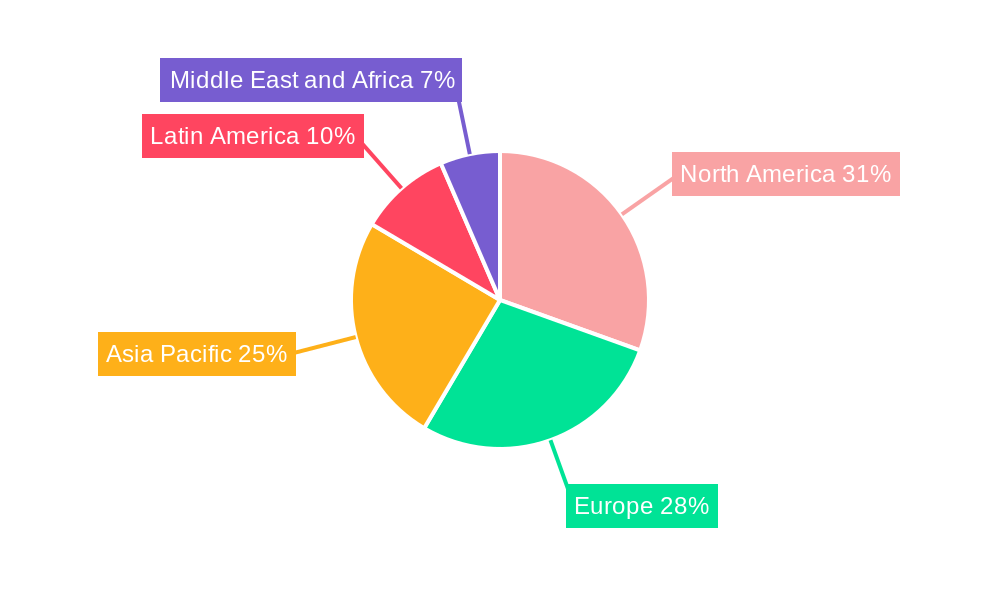

The market is segmented across various materials, with plastic emerging as a dominant segment due to its versatility, durability, and cost-effectiveness. However, there's a noticeable trend towards sustainable alternatives like paper and paperboard, glass, and metal, driven by environmental concerns and regulatory pressures. Product segmentation reveals milk, cheese, frozen foods, yogurt, and cultured products as key demand generators. Packaging types like bottles, pouches, cartons, boxes, and bags are widely adopted, with a growing emphasis on lightweight, recyclable, and tamper-evident designs. Geographically, North America and Europe currently hold significant market shares, but the Asia Pacific region is anticipated to witness the fastest growth, owing to rapid urbanization, a burgeoning middle class, and the increasing adoption of Western dietary habits. Companies are actively investing in R&D to develop innovative and eco-friendly packaging solutions, anticipating a strong future for the dairy products packaging industry.

Dairy Products Packaging Industry Company Market Share

This in-depth report provides a definitive analysis of the global Dairy Products Packaging Industry, offering strategic insights and actionable intelligence for stakeholders. The study encompasses a detailed examination of market dynamics, segmentation, competitive landscape, and future projections from 2019 to 2033, with a base year of 2025. Leveraging high-volume keywords such as "dairy packaging," "food packaging solutions," "sustainable packaging," "plastic packaging," "paperboard packaging," and "glass packaging," this report is meticulously crafted for optimal SEO performance and maximum industry relevance.

Dairy Products Packaging Industry Market Structure & Competitive Landscape

The Dairy Products Packaging Industry exhibits a moderately concentrated market structure, with key players investing heavily in innovation and sustainable solutions. Factors such as evolving consumer preferences for convenience and eco-friendliness, alongside stringent regulatory landscapes concerning food safety and material recyclability, significantly influence market dynamics. The presence of robust innovation drivers, including advancements in material science and packaging technology, fuels a competitive environment. Product substitutes, such as novel bioplastics and compostable materials, present both opportunities and challenges for incumbent packaging solutions. End-user segmentation, primarily driven by the demand for milk, cheese, frozen foods, yogurt, and cultured products, dictates regional and application-specific strategies. Merger and Acquisition (M&A) trends within the industry are on the rise, indicating consolidation efforts and strategic expansions by major entities. For instance, a significant volume of M&A activities, estimated at over $5 billion, has been observed during the historical period (2019-2024), as companies seek to expand their product portfolios and market reach. The concentration ratio for the top five players is estimated to be around 65% by 2025.

Dairy Products Packaging Industry Market Trends & Opportunities

The global Dairy Products Packaging Industry is poised for substantial growth, projected to reach a market size exceeding $200 billion by 2033. This expansion is driven by a confluence of factors, including an escalating global demand for dairy products, particularly in emerging economies, and a rising consumer consciousness towards health and wellness, leading to increased consumption of products like yogurt and cheese. Technological shifts are fundamentally reshaping the industry, with a pronounced trend towards sustainable and eco-friendly packaging solutions. This includes a surge in demand for recycled plastics, paper and paperboard alternatives, and innovative, lightweight materials that minimize environmental impact. Consumer preferences are increasingly aligning with brands that demonstrate a commitment to sustainability, pushing manufacturers to adopt greener packaging options. The competitive dynamics within the market are intensifying, characterized by strategic partnerships, product innovation, and a focus on cost-efficiency and supply chain optimization. The industry is also witnessing a significant CAGR of approximately 5.5% from 2025 to 2033. Market penetration rates for sustainable packaging solutions are projected to reach over 70% by 2033, presenting a considerable opportunity for forward-thinking companies. The development of smart packaging, incorporating features like shelf-life indicators and tamper-evident seals, also represents a significant growth avenue, enhancing product safety and consumer trust. The expansion of e-commerce channels for dairy products further necessitates robust and resilient packaging that can withstand transit challenges, creating a demand for specialized packaging designs and materials.

Dominant Markets & Segments in Dairy Products Packaging Industry

The Plastic segment is the undisputed leader in the Dairy Products Packaging Industry, commanding a significant market share of over 55% by 2025. This dominance is attributed to its versatility, cost-effectiveness, and advanced barrier properties crucial for preserving the freshness and extending the shelf-life of dairy products. Within the product segmentation, Milk packaging remains the largest application, followed closely by Yogurt and Cheese. The Bottles and Cartons & Boxes package types are particularly prevalent for milk and yogurt, respectively, due to their convenience and ease of use. Regionally, Asia Pacific is emerging as the most dominant market, driven by rapid urbanization, a growing middle class, and increasing disposable incomes, which are fueling the demand for packaged dairy goods. Key growth drivers in this region include robust infrastructure development, supportive government policies promoting food processing and packaging, and a burgeoning retail sector. The adoption of advanced packaging technologies, coupled with a growing awareness of food safety standards, further bolsters market growth. The market penetration of premium and functional dairy products, such as fortified yogurts and lactose-free milk, also contributes to the demand for specialized packaging solutions. The Paper and Paperboard segment is experiencing significant growth, driven by sustainability initiatives and increasing consumer preference for recyclable materials, especially for items like cheese and butter. The forecast period anticipates a market expansion of over $15 billion for paperboard packaging in dairy applications by 2033. The Metal segment, while smaller, plays a critical role in specific applications like condensed milk and certain types of cheese packaging, offering excellent barrier protection and recyclability. The Glass segment, though facing competition from lighter alternatives, maintains its niche for premium dairy products and beverages where perceived quality and recyclability are paramount.

Dairy Products Packaging Industry Product Analysis

Product innovations in the dairy packaging sector are centered around enhancing sustainability, functionality, and consumer appeal. Advancements in materials science are yielding lightweight, recyclable, and compostable packaging solutions that reduce environmental impact. Key innovations include the development of chemically recycled polypropylene for ready-to-drink iced coffee packaging and the exploration of fiber-based bottles as a viable alternative to traditional plastics and glass. These developments aim to offer superior barrier properties, extended shelf life, and improved product preservation while aligning with circular economy principles. Competitive advantages are being achieved through the integration of smart packaging features, such as enhanced tamper-evidence and temperature indicators, thereby increasing consumer confidence and product safety.

Key Drivers, Barriers & Challenges in Dairy Products Packaging Industry

Key Drivers:

- Growing Global Demand for Dairy Products: An expanding population and rising disposable incomes, particularly in emerging economies, are driving consistent demand for milk, cheese, yogurt, and other dairy items.

- Increasing Consumer Focus on Health and Convenience: The growing awareness of dairy's nutritional benefits and the demand for convenient, on-the-go consumption formats are propelling the market for pre-portioned and ready-to-eat dairy products.

- Technological Advancements in Packaging: Innovations in materials, design, and manufacturing processes are leading to more sustainable, functional, and cost-effective packaging solutions, including biodegradable and recycled content options.

- Sustainability and Environmental Concerns: Increasing consumer and regulatory pressure for eco-friendly packaging is a significant driver for the adoption of recyclable, reusable, and compostable materials.

Key Barriers & Challenges:

- Stringent Regulatory Landscape: Compliance with food safety regulations, labeling requirements, and evolving waste management policies can pose significant hurdles for packaging manufacturers.

- Volatility in Raw Material Prices: Fluctuations in the cost of key raw materials like plastics, paper pulp, and aluminum can impact profit margins and necessitate dynamic pricing strategies.

- Supply Chain Disruptions: Global events and geopolitical factors can lead to disruptions in the supply chain, affecting the availability and cost of raw materials and finished packaging products.

- Consumer Perception and Education: Educating consumers about the recyclability and environmental impact of different packaging materials is crucial, as misconceptions can influence purchasing decisions.

Growth Drivers in the Dairy Products Packaging Industry Market

The Dairy Products Packaging Industry is experiencing robust growth fueled by several interconnected factors. Technologically, the continuous innovation in materials science, leading to the development of more sustainable, lightweight, and functional packaging options, is a primary growth catalyst. Economically, the increasing global demand for dairy products, driven by rising disposable incomes and growing populations in developing nations, creates a consistent market expansion. Regulatory frameworks promoting the use of recycled content and extended producer responsibility are also nudging the industry towards greener solutions. For example, government initiatives mandating the use of a minimum percentage of recycled PET in beverage bottles are influencing the dairy sector as well.

Challenges Impacting Dairy Products Packaging Industry Growth

Despite the positive growth trajectory, the Dairy Products Packaging Industry faces significant challenges. Regulatory complexities surrounding food contact materials, recyclability standards, and waste management are constantly evolving, requiring continuous adaptation from manufacturers. Supply chain vulnerabilities, exacerbated by global logistics issues and geopolitical uncertainties, can lead to material shortages and increased costs. Competitive pressures from both established players and emerging innovators, particularly in the sustainable packaging space, necessitate constant investment in research and development to maintain market share. The capital expenditure required for transitioning to new, more sustainable materials can also be a considerable barrier for some smaller enterprises.

Key Players Shaping the Dairy Products Packaging Industry Market

- Amcor PLC

- Berry Global Group Inc

- Ball Corporation

- Huhtamaki Group

- Greiner Packaging international Gmb

- Stora Enso Oyj

- Sealed Air Corporation

- Winpak Ltd

- International Paper Company

- Consolidated Container Company LLC

- Saudi Basic Industries Corporation

Significant Dairy Products Packaging Industry Industry Milestones

- September 2021: Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

- August 2021: Huhtamaki announced the acquisition of Elif Holding A.S., which is a leader in producing and supplying sustainable, flexible packaging to major global FMCG brands in Africa, the Middle East, and Europe. This acquisition helps Huhtamaki to reinforce its position in emerging packaging markets.

- May 2021: Stora Enso announced a partnership with Pulpex to produce fiber-based bottles. The packaging technology of Pulpex will help to industrialize the production of containers made from wood fiber pulp and eco-friendly paper bottles, offering an alternative to glass and PET plastics bottles.

Future Outlook for Dairy Products Packaging Industry Market

The future outlook for the Dairy Products Packaging Industry is exceptionally bright, driven by sustained demand for dairy products and the burgeoning trend towards sustainable packaging solutions. Strategic opportunities lie in the development and adoption of innovative materials, such as advanced bio-plastics and high-barrier paperboard, to meet both consumer and regulatory demands for eco-friendliness. The continued expansion of convenience formats and the growth of e-commerce for dairy products will further fuel the need for resilient and well-designed packaging. Investments in advanced recycling technologies and circular economy models will be crucial for long-term success. The market potential is projected to exceed $250 billion by 2033, with a significant portion attributed to the increasing adoption of sustainable and smart packaging technologies.

Dairy Products Packaging Industry Segmentation

-

1. Material

- 1.1. Plastic

- 1.2. Paper and Paperboard

- 1.3. Glass

- 1.4. Metal

-

2. Product

- 2.1. Milk

- 2.2. Cheese

- 2.3. Frozen Foods

- 2.4. Yogurt

- 2.5. Cultured Products

-

3. Package Type

- 3.1. Bottles

- 3.2. Pouches

- 3.3. Cartons and Boxes

- 3.4. Bags and Wraps

- 3.5. Other Package Types

Dairy Products Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Dairy Products Packaging Industry Regional Market Share

Geographic Coverage of Dairy Products Packaging Industry

Dairy Products Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.2. Paper and Paperboard

- 5.1.3. Glass

- 5.1.4. Metal

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Milk

- 5.2.2. Cheese

- 5.2.3. Frozen Foods

- 5.2.4. Yogurt

- 5.2.5. Cultured Products

- 5.3. Market Analysis, Insights and Forecast - by Package Type

- 5.3.1. Bottles

- 5.3.2. Pouches

- 5.3.3. Cartons and Boxes

- 5.3.4. Bags and Wraps

- 5.3.5. Other Package Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Dairy Products Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.2. Paper and Paperboard

- 6.1.3. Glass

- 6.1.4. Metal

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Milk

- 6.2.2. Cheese

- 6.2.3. Frozen Foods

- 6.2.4. Yogurt

- 6.2.5. Cultured Products

- 6.3. Market Analysis, Insights and Forecast - by Package Type

- 6.3.1. Bottles

- 6.3.2. Pouches

- 6.3.3. Cartons and Boxes

- 6.3.4. Bags and Wraps

- 6.3.5. Other Package Types

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. North America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Plastic

- 7.1.2. Paper and Paperboard

- 7.1.3. Glass

- 7.1.4. Metal

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Milk

- 7.2.2. Cheese

- 7.2.3. Frozen Foods

- 7.2.4. Yogurt

- 7.2.5. Cultured Products

- 7.3. Market Analysis, Insights and Forecast - by Package Type

- 7.3.1. Bottles

- 7.3.2. Pouches

- 7.3.3. Cartons and Boxes

- 7.3.4. Bags and Wraps

- 7.3.5. Other Package Types

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Europe Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Plastic

- 8.1.2. Paper and Paperboard

- 8.1.3. Glass

- 8.1.4. Metal

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Milk

- 8.2.2. Cheese

- 8.2.3. Frozen Foods

- 8.2.4. Yogurt

- 8.2.5. Cultured Products

- 8.3. Market Analysis, Insights and Forecast - by Package Type

- 8.3.1. Bottles

- 8.3.2. Pouches

- 8.3.3. Cartons and Boxes

- 8.3.4. Bags and Wraps

- 8.3.5. Other Package Types

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Asia Pacific Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Plastic

- 9.1.2. Paper and Paperboard

- 9.1.3. Glass

- 9.1.4. Metal

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Milk

- 9.2.2. Cheese

- 9.2.3. Frozen Foods

- 9.2.4. Yogurt

- 9.2.5. Cultured Products

- 9.3. Market Analysis, Insights and Forecast - by Package Type

- 9.3.1. Bottles

- 9.3.2. Pouches

- 9.3.3. Cartons and Boxes

- 9.3.4. Bags and Wraps

- 9.3.5. Other Package Types

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Latin America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Plastic

- 10.1.2. Paper and Paperboard

- 10.1.3. Glass

- 10.1.4. Metal

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Milk

- 10.2.2. Cheese

- 10.2.3. Frozen Foods

- 10.2.4. Yogurt

- 10.2.5. Cultured Products

- 10.3. Market Analysis, Insights and Forecast - by Package Type

- 10.3.1. Bottles

- 10.3.2. Pouches

- 10.3.3. Cartons and Boxes

- 10.3.4. Bags and Wraps

- 10.3.5. Other Package Types

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Middle East and Africa Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Plastic

- 11.1.2. Paper and Paperboard

- 11.1.3. Glass

- 11.1.4. Metal

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Milk

- 11.2.2. Cheese

- 11.2.3. Frozen Foods

- 11.2.4. Yogurt

- 11.2.5. Cultured Products

- 11.3. Market Analysis, Insights and Forecast - by Package Type

- 11.3.1. Bottles

- 11.3.2. Pouches

- 11.3.3. Cartons and Boxes

- 11.3.4. Bags and Wraps

- 11.3.5. Other Package Types

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Consolidated Container Company LLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Stora Enso Oyj

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ball Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Greiner Packaging international Gmb

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Berry Global Group Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Huhtamaki Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Winpak Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Amcor PLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 International Paper Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sealed Air Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Saudi Basic Industries Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Consolidated Container Company LLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Dairy Products Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 3: North America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 5: North America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 7: North America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 8: North America Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 11: Europe Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 12: Europe Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 13: Europe Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 15: Europe Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 16: Europe Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 19: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 20: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 21: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 23: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 24: Asia Pacific Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 27: Latin America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 28: Latin America Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 29: Latin America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Latin America Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 31: Latin America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 32: Latin America Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Material 2025 & 2033

- Figure 35: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 36: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Product 2025 & 2033

- Figure 37: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Package Type 2025 & 2033

- Figure 39: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 40: Middle East and Africa Dairy Products Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 3: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 4: Global Dairy Products Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 6: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 7: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 8: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 10: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 11: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 12: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 14: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 15: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 16: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 18: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 19: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 20: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Dairy Products Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 22: Global Dairy Products Packaging Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 23: Global Dairy Products Packaging Industry Revenue billion Forecast, by Package Type 2020 & 2033

- Table 24: Global Dairy Products Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dairy Products Packaging Industry?

The projected CAGR is approximately 2.7%.

2. Which companies are prominent players in the Dairy Products Packaging Industry?

Key companies in the market include Consolidated Container Company LLC, Stora Enso Oyj, Ball Corporation, Greiner Packaging international Gmb, Berry Global Group Inc, Huhtamaki Group, Winpak Ltd, Amcor PLC, International Paper Company, Sealed Air Corporation, Saudi Basic Industries Corporation.

3. What are the main segments of the Dairy Products Packaging Industry?

The market segments include Material, Product, Package Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 33.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size.

6. What are the notable trends driving market growth?

Milk Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues.

8. Can you provide examples of recent developments in the market?

September 2021 - Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dairy Products Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dairy Products Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dairy Products Packaging Industry?

To stay informed about further developments, trends, and reports in the Dairy Products Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence